1. What is the projected Compound Annual Growth Rate (CAGR) of the Mobile Operators Capital Expenditure?

The projected CAGR is approximately 5.2%.

Mobile Operators Capital Expenditure

Mobile Operators Capital ExpenditureMobile Operators Capital Expenditure by Application (Developed market integrated operator, Developed market mobile-centric operator, Emerging market integrated operator/incumbent, Emerging market established mobile operator, Emerging market disruptor), by Type (Infrastructure, RAN – BTS, antennas, Core and backhaul, Spectrum, IT/ data centre, CPE, Cost transformation capex), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2026-2034

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

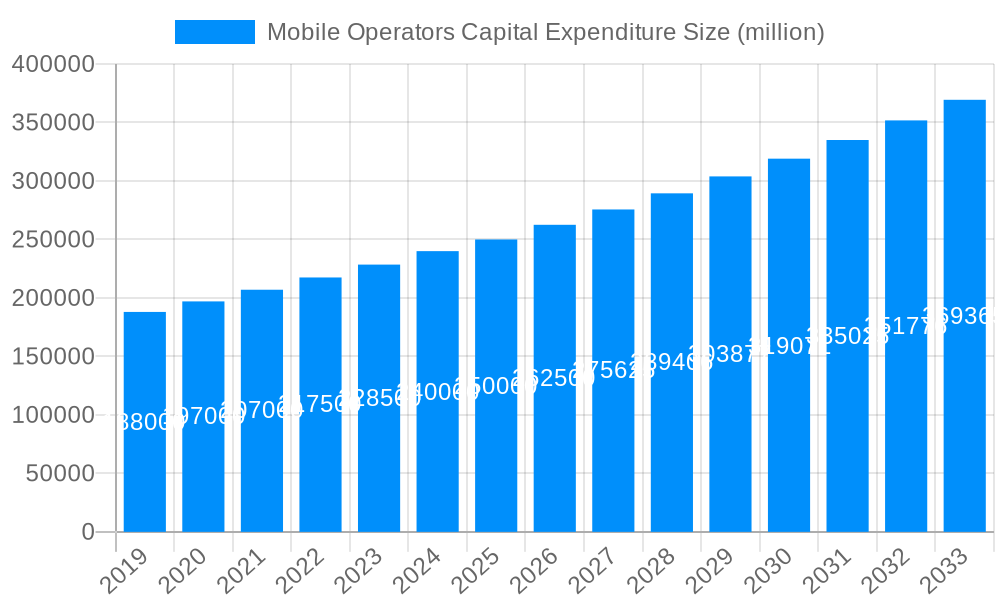

The global mobile operators' capital expenditure (CAPEX) market is experiencing robust growth, driven by the increasing demand for 5G infrastructure, the expansion of network capacity to accommodate rising data consumption, and the ongoing digital transformation across various sectors. The market, estimated at $500 billion in 2025, is projected to exhibit a Compound Annual Growth Rate (CAGR) of 7% from 2025 to 2033, reaching approximately $900 billion by 2033. This growth is fueled by several key factors. Firstly, the widespread adoption of 5G technology necessitates significant investments in new radio access network (RAN) equipment, including base transceiver stations (BTS), antennas, and core networks. Secondly, the surge in mobile data traffic necessitates capacity expansions, leading to substantial investments in backhaul infrastructure and data centers. Thirdly, competition among mobile operators is driving investments in advanced technologies and services, such as edge computing and network slicing, to enhance customer experience and attract new subscribers. Finally, emerging markets represent a significant growth opportunity, as operators invest heavily in deploying mobile infrastructure to connect underserved populations.

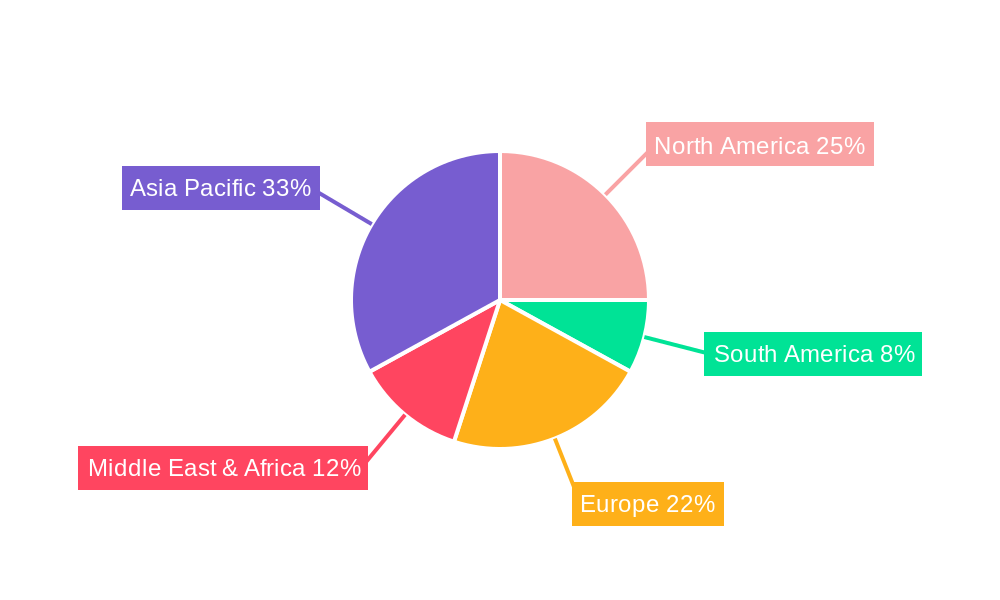

Significant regional variations exist. North America and Europe are currently leading the market due to higher network maturity and early 5G adoption. However, Asia Pacific, particularly China and India, is projected to witness the fastest growth over the forecast period due to expanding mobile subscriber bases and government initiatives promoting digital infrastructure development. Market segmentation reveals that investments in RAN infrastructure, including BTS and antennas, constitute the largest share of CAPEX. However, investments in core networks, backhaul infrastructure, and IT/data centers are also growing rapidly as operators prioritize network optimization and digital transformation. The competitive landscape is characterized by both established global players and regional operators, with strategic partnerships and mergers & acquisitions shaping market dynamics. Challenges include regulatory hurdles, spectrum allocation complexities, and the need for efficient cost management in a highly competitive environment.

The global mobile operators' capital expenditure (CAPEX) market is poised for significant transformation over the forecast period (2025-2033). Driven by the relentless expansion of 5G networks, the increasing demand for higher bandwidth, and the proliferation of connected devices, CAPEX is expected to witness substantial growth, though at a potentially moderating rate compared to the previous years' explosive expansion. The historical period (2019-2024) saw considerable investment, primarily focused on 4G network rollout and initial 5G deployments. However, the estimated year 2025 marks a transition point. While the overall investment remains substantial (projected at XXX million), the focus is shifting towards network optimization, 5G densification, and the integration of new technologies like edge computing and network slicing. This strategic realignment reflects a move beyond simple network expansion towards maximizing efficiency and delivering enhanced services. The market is witnessing a diversification of spending across various segments, with increased emphasis on software-defined networking (SDN), network function virtualization (NFV), and the development of private 5G networks for industrial applications. This strategic shift will impact the market dynamics, leading to greater competition and the emergence of specialized vendors catering to specific niche needs. Emerging markets will continue to drive a significant portion of the CAPEX, particularly from established and disruptive mobile operators aggressively expanding their infrastructure to meet surging demand. Developed markets will see a more focused investment, primarily on upgrades and modernization rather than widespread expansion. Ultimately, the successful players will be those that can strategically allocate their resources to balance expansion with optimization, leveraging technological advancements to enhance profitability and network efficiency.

Several factors are driving the substantial investments in mobile operators' capital expenditure. Firstly, the global rollout of 5G networks necessitates massive investment in infrastructure upgrades. This includes deploying new base stations (BTS), upgrading core networks to handle increased data traffic, and investing in advanced antenna technologies like Massive MIMO. The transition to 5G promises significantly higher speeds and lower latency, creating a demand for capacity that existing 4G networks cannot satisfy. Secondly, the exponential growth of mobile data consumption fuels the need for continuous network expansion and capacity enhancements. The increasing adoption of smartphones, IoT devices, and video streaming services leads to ever-growing bandwidth demands, forcing operators to continually invest in their infrastructure. Thirdly, the emergence of new technologies and services, such as edge computing and network slicing, requires substantial CAPEX. Edge computing brings processing closer to the user, reducing latency and enabling new applications. Network slicing allows operators to create virtual networks tailored to specific use cases, leading to improved network efficiency and service differentiation. Lastly, regulatory pressures and the race for spectrum licenses play a role in shaping CAPEX. Governments are actively promoting 5G deployment through spectrum auctions and regulatory frameworks, driving operators to invest in securing necessary licenses and building the required infrastructure.

Despite the significant growth opportunities, several challenges hinder mobile operators' capital expenditure. Firstly, the high cost of 5G infrastructure poses a substantial barrier. Deploying 5G networks is significantly more expensive than previous generations due to the need for more densely deployed base stations and advanced technologies. This cost can be particularly daunting for operators in emerging markets with limited financial resources. Secondly, securing sufficient spectrum licenses can be challenging and expensive, creating another significant hurdle for operators. Governments typically auction off spectrum licenses, leading to intense competition and potentially high costs. Thirdly, the increasing complexity of network management and operation poses another challenge. Managing large and sophisticated 5G networks requires specialized skills and tools, leading to increased operational expenses. Finally, regulatory uncertainties and changing technological landscapes add to the complexity. Governments may introduce new regulations impacting network deployment and operation, while the rapid pace of technological advancement requires operators to constantly adapt their infrastructure and strategies, adding risk and cost to their investment plans. The return on investment (ROI) for such large CAPEX is also a concern, requiring careful planning and efficient resource management.

The Asia-Pacific region, particularly China and India, is projected to dominate the mobile operators' CAPEX market due to the massive population and rapid adoption of mobile technologies. North America and Europe will also contribute significantly, although at a potentially slower growth rate compared to the emerging markets.

Dominant Segments:

Emerging Market Established Mobile Operator: These operators are experiencing massive growth in data consumption, pushing them to invest heavily in expanding their network capacity and upgrading their infrastructure to accommodate the increasing demand. This segment benefits from a less saturated market and rapid customer acquisition, creating high returns on investment.

RAN – BTS, antennas, Core and backhaul: The core components of any mobile network, these segments will witness the bulk of CAPEX investment as operators build out and upgrade their 5G infrastructure. The demand for new BTS (Base Transceiver Stations) and antennas will be especially strong due to the higher density requirements of 5G. Upgrades to core and backhaul networks will be necessary to handle the increased data traffic.

Spectrum: Securing sufficient spectrum licenses is crucial for 5G deployment. As governments allocate more spectrum for 5G, operators will need to invest heavily in acquiring these licenses, driving CAPEX in this segment.

The large population base and increasing smartphone penetration in emerging markets fuel demand, driving substantial CAPEX for network expansion. Meanwhile, developed markets focus on network upgrades and optimization for improved service quality and efficiency. Developed market integrated operators will continue to invest, but their expenditure will be more focused on efficiency gains and targeted upgrades, rather than on large-scale expansion.

The convergence of several technological advancements and market dynamics acts as a significant growth catalyst. The continued rollout of 5G networks, fueled by increasing data demands and government initiatives, represents the primary driver. Furthermore, the adoption of new technologies such as network slicing and edge computing opens avenues for increased efficiency and new revenue streams, prompting further investment. Finally, the emergence of private 5G networks for industrial applications and the Internet of Things (IoT) presents a significant opportunity for growth, requiring substantial CAPEX for deployment and infrastructure development.

This report provides a detailed analysis of the mobile operators' capital expenditure market, encompassing historical data, current market trends, and future projections. It offers in-depth insights into driving forces, challenges, and growth catalysts, along with a comprehensive overview of key players and regional market dynamics. The report serves as a valuable resource for industry stakeholders, investors, and anyone seeking a comprehensive understanding of this dynamic market.

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 5.2% from 2020-2034 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately 5.2%.

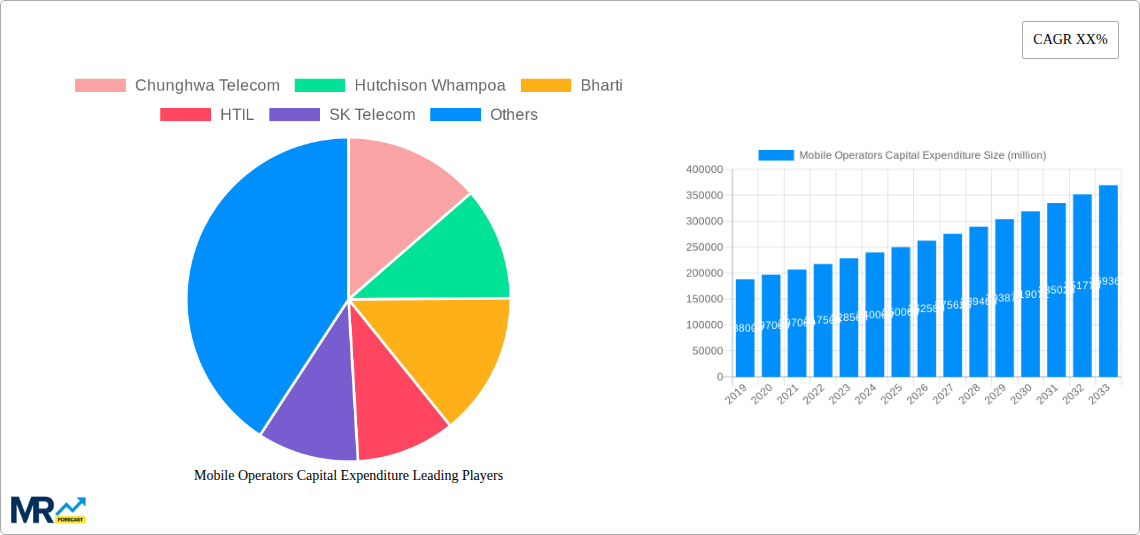

Key companies in the market include Chunghwa Telecom, Hutchison Whampoa, Bharti, HTIL, SK Telecom, Orange, China Mobile, NTT, LG, China Unicom, Vodafone, United Technologies, A1 Telekom Austria, Vivo, America Movil, Sprint, Alltel, Bell MTS, Rogers Wireless, MTN, Verizon, Telecom Italia, Telstra, China Telecom, Telenor, .

The market segments include Application, Type.

The market size is estimated to be USD 198.4 billion as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3480.00, USD 5220.00, and USD 6960.00 respectively.

The market size is provided in terms of value, measured in billion.

Yes, the market keyword associated with the report is "Mobile Operators Capital Expenditure," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Mobile Operators Capital Expenditure, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.