1. What is the projected Compound Annual Growth Rate (CAGR) of the Military Simulation Software?

The projected CAGR is approximately 6.7%.

Military Simulation Software

Military Simulation SoftwareMilitary Simulation Software by Type (Command and Management Simulation Software, Fight Simulation Software, Other), by Application (Warfighter, Commander, Military Engineer, Other), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2026-2034

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

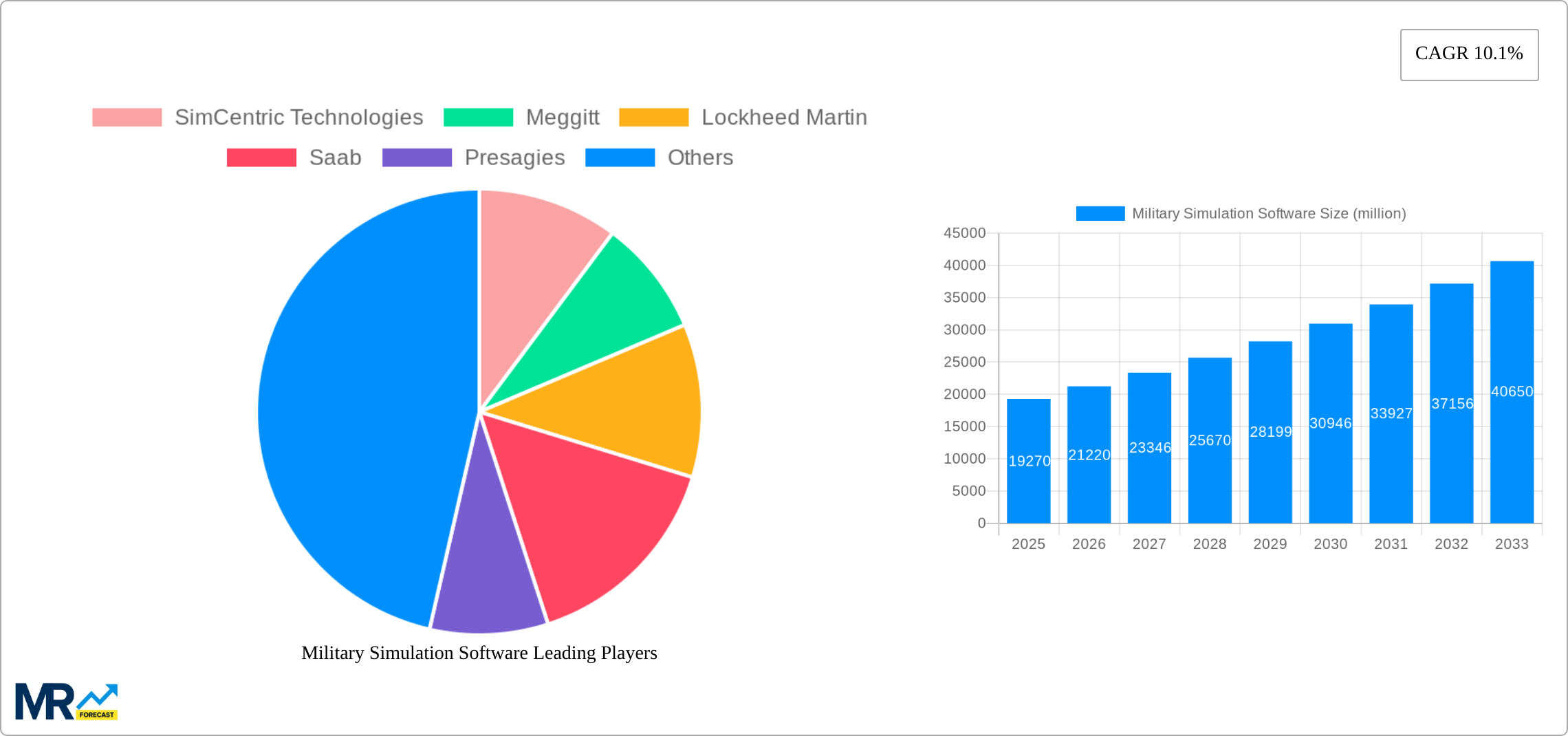

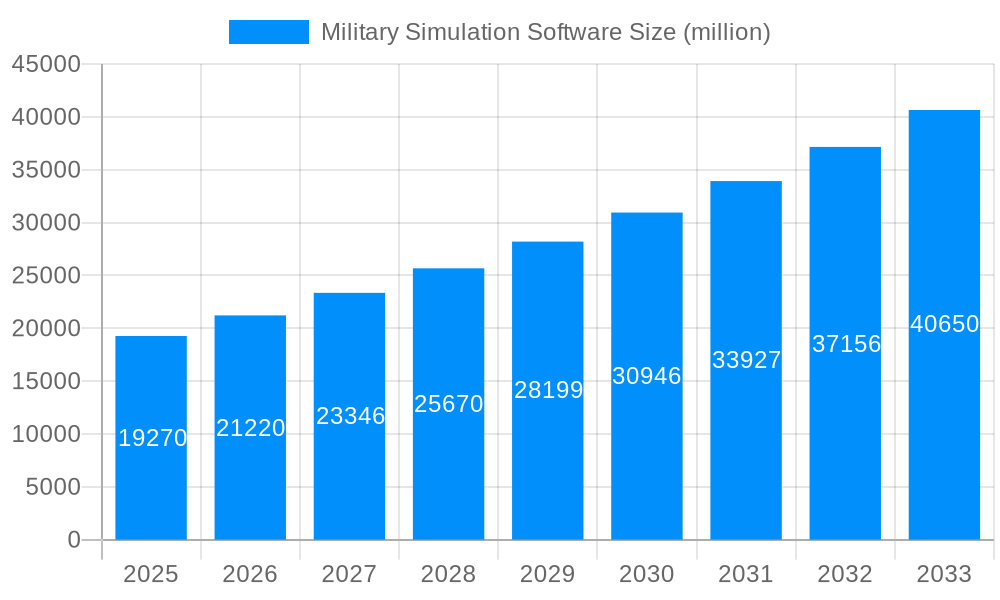

The Military Simulation Software market, valued at $12.99 billion in the base year of 2025, is projected to achieve a robust compound annual growth rate (CAGR) of 6.7%, expanding significantly by 2033. This growth is propelled by the escalating demand for advanced military training solutions, crucial for enhancing operational readiness and effectiveness. Technological innovations, notably the integration of Artificial Intelligence (AI), Virtual Reality (VR), and Augmented Reality (AR), are transforming simulation capabilities, delivering more immersive and realistic training environments. Heightened geopolitical instability and the imperative for strengthened defense postures worldwide are also driving substantial investments in this sector. The market's segmentation, encompassing command and management, combat, and specialized warfighter and engineering simulations, underscores its widespread applicability across diverse military roles and operational demands.

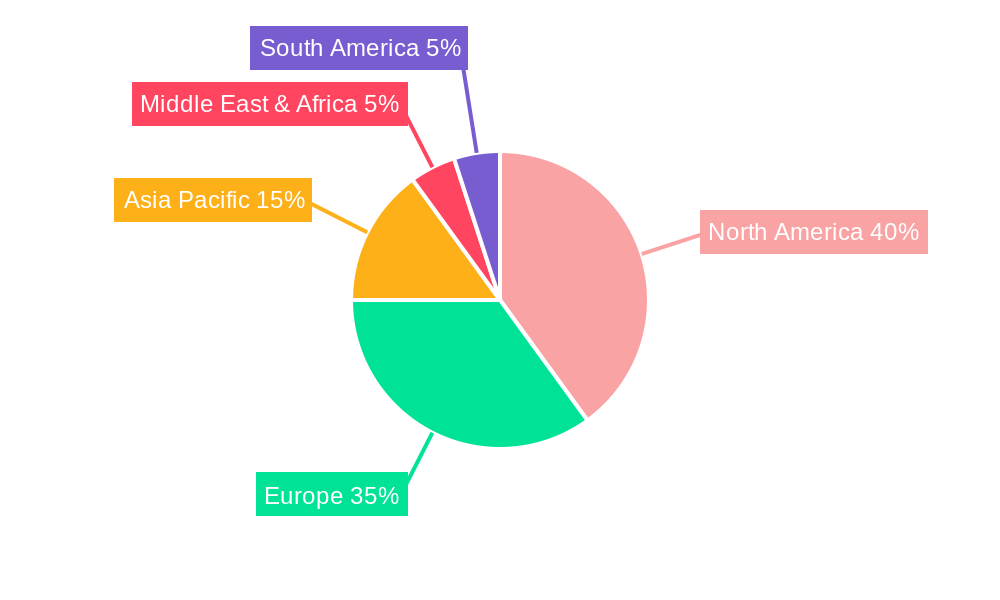

Key market trends include the adoption of scalable and accessible cloud-based simulation platforms and a growing emphasis on interoperability between diverse simulation systems to ensure seamless integration. However, challenges such as the high development and implementation costs of sophisticated simulation software, alongside the complexities of integrating legacy systems, warrant consideration. Despite these hurdles, the Military Simulation Software market exhibits a positive long-term outlook, fueled by ongoing technological advancements, increasing defense expenditures, and the persistent need to maintain a competitive technological edge. Leading entities such as Lockheed Martin, Saab, and SimCentric Technologies are strategically positioned to leverage this expansion through continuous innovation. While North America and Europe are expected to retain substantial market share, the Asia-Pacific region is poised for significant growth, attributed to escalating defense investments in nations like China and India.

The global military simulation software market is experiencing robust growth, projected to reach tens of billions of dollars by 2033. This surge is driven by several converging factors, including the increasing need for advanced training and operational planning capabilities within militaries worldwide. The historical period (2019-2024) saw a steady increase in adoption, particularly in the Command and Management Simulation Software segment, as nations recognize the cost-effectiveness and safety benefits of virtual training environments over live exercises. The estimated market value in 2025 is already in the multi-billion dollar range, highlighting the significant investment in this technology. Key market insights reveal a growing preference for software solutions that offer high fidelity, realistic scenarios, and interoperability with existing military systems. This demand is pushing vendors to develop more sophisticated algorithms and advanced graphics capabilities, leading to a more immersive and effective training experience. Furthermore, the integration of Artificial Intelligence (AI) and Machine Learning (ML) is revolutionizing the sector, enabling the creation of adaptive and dynamic simulations that respond to user actions in increasingly realistic ways. This allows for more efficient and effective training, as well as improved strategic planning capabilities. The forecast period (2025-2033) promises even greater expansion as technological advancements continue to refine simulation capabilities and address new military challenges. The increasing adoption of cloud-based solutions and the rise of collaborative training platforms are also key trends impacting the market landscape. Overall, the market showcases a clear shift toward more sophisticated, data-driven, and collaborative simulation environments that are crucial for modern military operations.

Several factors are accelerating the growth of the military simulation software market. Firstly, the rising need for cost-effective and safe training environments is a primary driver. Live exercises are expensive, logistically challenging, and can pose safety risks to personnel and equipment. Military simulation software offers a significantly cheaper and safer alternative, allowing troops to practice complex maneuvers and scenarios repeatedly without incurring substantial costs or risks. Secondly, technological advancements are playing a crucial role. Improvements in computing power, graphics processing, and AI are creating more realistic and immersive simulations. These advancements not only enhance the training value but also allow for more detailed analysis of training data, leading to improved training methodologies. Thirdly, the increasing complexity of modern warfare necessitates more sophisticated training solutions. Dealing with asymmetric threats, cyber warfare, and complex joint operations requires highly realistic and adaptable training programs which simulation software facilitates. Finally, geopolitical instability and the growing need for military readiness globally are driving investments in military training, thereby boosting the demand for advanced simulation software. This combination of cost savings, technological progress, and evolving military needs ensures a strong and sustained growth trajectory for the market.

Despite the market's promising growth, several challenges and restraints exist. One significant challenge is the high cost of developing and maintaining sophisticated simulation software. Creating realistic and detailed models requires substantial investment in software development, hardware, and ongoing maintenance. This can be a barrier to entry for smaller companies and limit the availability of such technology to larger defense organizations. Another restraint is the need for high levels of data security and cyber protection. Military simulations often contain sensitive information, making them vulnerable to cyberattacks. Ensuring the security and integrity of these systems is a paramount concern, requiring significant investment in cybersecurity infrastructure and protocols. Furthermore, the complexity of integrating various simulation platforms and systems can pose significant challenges. Military operations often involve diverse systems and platforms, and ensuring seamless interoperability between different simulation environments requires careful planning and coordination. Finally, the constant evolution of military tactics and technologies requires continuous updating and refinement of simulation software to maintain its relevance and effectiveness. This necessitates significant ongoing investment in research and development to stay ahead of the curve.

The Command and Management Simulation Software segment is poised to dominate the market throughout the forecast period (2025-2033). This is due to the increasing recognition of its value in improving strategic decision-making and command and control capabilities. The ability to simulate large-scale conflicts, complex logistical operations, and joint force engagements in a virtual environment provides invaluable training and operational planning benefits. This segment is significantly impacting the military training landscape, optimizing resource allocation and promoting seamless interoperability among different military branches.

Several key regions are anticipated to show substantial growth:

North America: The strong defense budget, coupled with ongoing technological advancements within the region, is driving significant adoption of command and management simulation software. Companies like Lockheed Martin and SimCentric Technologies are heavily invested in this sector.

Europe: European nations are similarly investing in modernizing their military training capabilities, particularly for combined forces operations, further fueling demand within the segment. Companies like Saab and Rheinmetall Defence Electronics GmbH contribute significantly to this regional market.

Asia-Pacific: The growing military modernization efforts in several Asia-Pacific countries are driving rapid growth in this segment, with strong domestic players emerging from China.

Furthermore, the Commander application segment will experience high growth as this software plays a pivotal role in training high-ranking officers in strategic decision-making under pressure and managing large-scale operations. The ability to analyze outcomes and test different strategies in a safe and controlled environment makes it a critical tool for modern military leadership.

In summary, the confluence of technological advancement, increased defense spending, and the need for improved command and control across key regions is driving the dominance of the Command and Management Simulation Software segment, particularly within the Commander application sector. The market's growth is a testament to the transformative potential of this technology in enhancing military readiness and effectiveness.

The military simulation software industry's growth is fueled by several key catalysts. Firstly, the increasing adoption of cloud-based solutions offers scalability and cost-effectiveness, enabling access to advanced simulation capabilities for organizations with varying budgets. Secondly, the integration of AI and ML technologies allows for the creation of more realistic and adaptive simulations that can evolve and adapt to user actions, ensuring more relevant and effective training. Lastly, the growing focus on joint and coalition operations necessitates interoperable simulation platforms that can effectively replicate the complexities of modern, multinational warfare scenarios, driving the demand for advanced software capable of supporting this collaboration.

This report provides a detailed analysis of the military simulation software market, covering key trends, drivers, restraints, and growth opportunities. It offers insights into leading players, emerging technologies, and regional market dynamics. The comprehensive nature of this report makes it a valuable resource for stakeholders looking to understand the current market landscape and future trajectory of this rapidly evolving sector. It utilizes data from the historical period (2019-2024), the base year (2025), and offers detailed forecasts extending to 2033, providing a comprehensive view of the market's potential for growth.

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 6.7% from 2020-2034 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately 6.7%.

Key companies in the market include SimCentric Technologies, Meggitt, Lockheed Martin, Saab, Presagies, MAK, Rheinmetall Defence Electronics GmbH, Ternion, TeledyneBrown, Beijing Huaru Technology, China Aerospace System Simulation Technology(Addsino), Beijing Appsoft Technology, VIRE Technologies, Beijing Shenzhou Zhihui Technology, Nanjing Ruichenxinchuang Network Technology, Beijing J&T Simulation Technology, Beijing Zhuoyi Intelligent Technology, .

The market segments include Type, Application.

The market size is estimated to be USD 12.99 billion as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3480.00, USD 5220.00, and USD 6960.00 respectively.

The market size is provided in terms of value, measured in billion.

Yes, the market keyword associated with the report is "Military Simulation Software," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Military Simulation Software, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.