1. What is the projected Compound Annual Growth Rate (CAGR) of the Marine Heavy Fuel Oil?

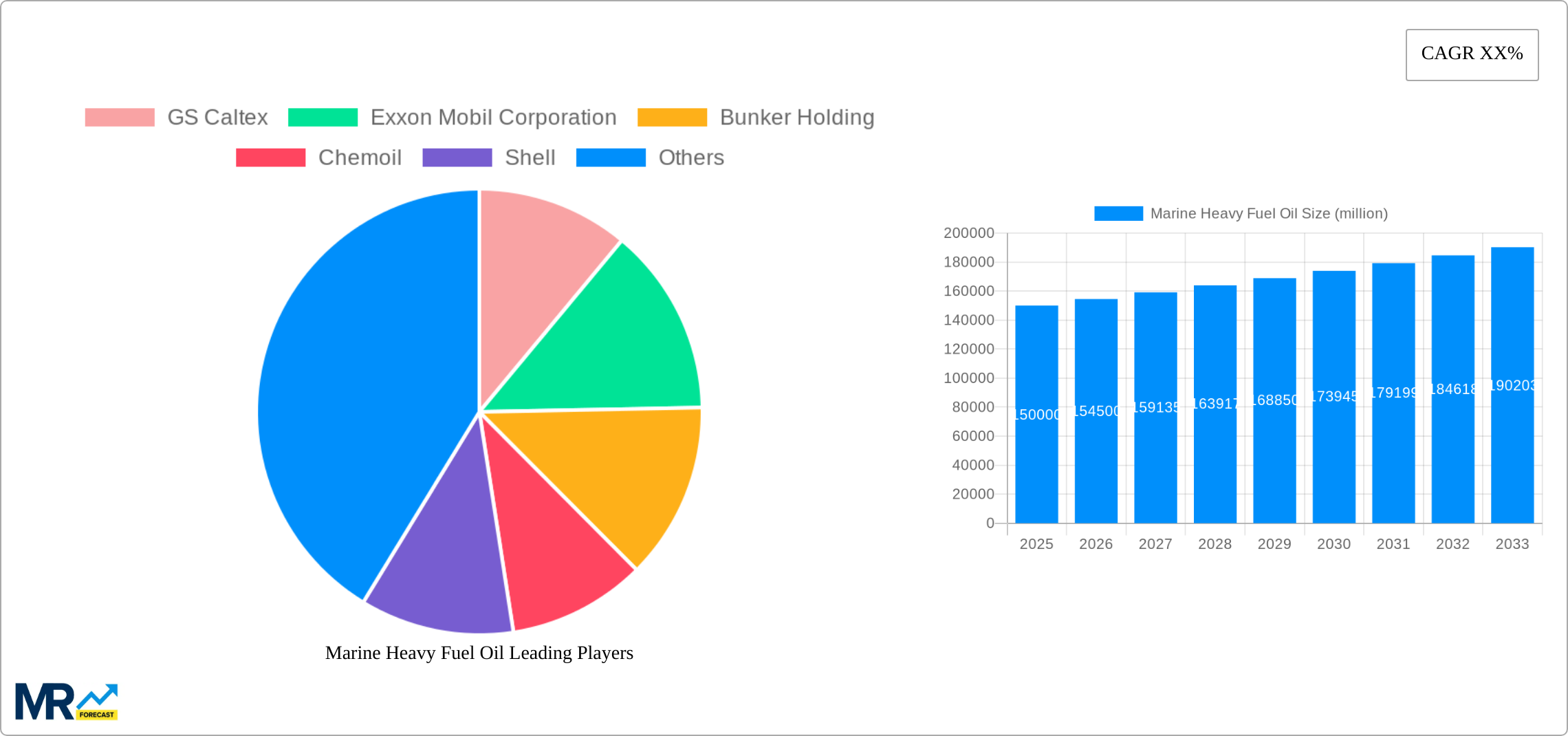

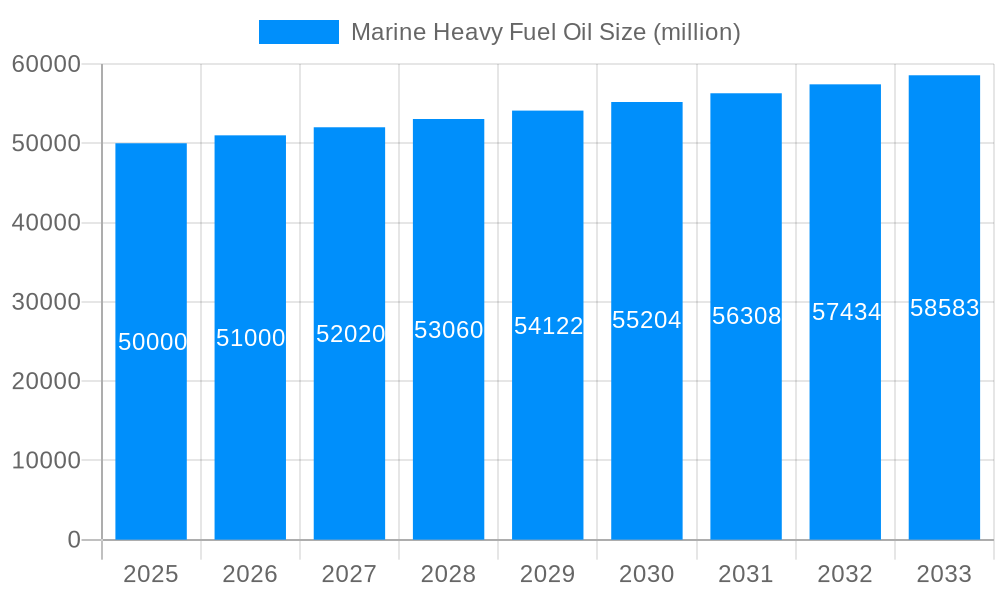

The projected CAGR is approximately 2.17%.

Marine Heavy Fuel Oil

Marine Heavy Fuel OilMarine Heavy Fuel Oil by Type (IFO 180, IFO 380), by Application (Commercial, Navy, Others), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2026-2034

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

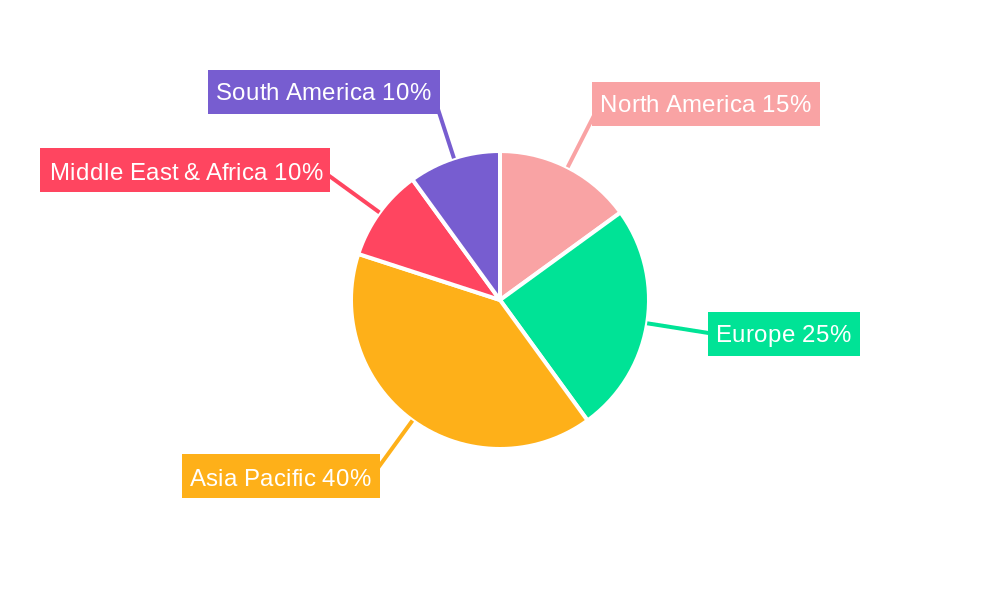

The global marine heavy fuel oil (HFO) market, including IFO 180 and IFO 380, is a vital segment of the maritime industry. Driven by escalating global shipping and trade volumes, the market is projected to reach a size of 108.2 billion by 2033, exhibiting a Compound Annual Growth Rate (CAGR) of 2.17% from a base year of 2025. While recent years saw market volatility influenced by crude oil price fluctuations and environmental mandates, sustained growth is anticipated. The market is segmented by application, with commercial shipping dominating due to its cost-effective fuel requirements. Leading companies such as ExxonMobil, Shell, and Total Marine Fuels are key competitors, offering diverse HFO grades and global bunkering services. Geographically, the Asia-Pacific region, propelled by extensive shipping activities, and Europe, with its robust maritime infrastructure, represent significant market concentrations. North and South America demonstrate moderate market presence with growth potential tied to expanding trade routes and cargo volumes.

Looking ahead to 2033, the marine HFO market will be shaped by evolving dynamics. Increasingly stringent environmental regulations, focused on reducing sulfur emissions and fostering cleaner fuel adoption, are expected to gradually decrease HFO consumption. The International Maritime Organization's (IMO) 2020 sulfur cap has already spurred a transition towards low-sulfur alternatives like very low sulfur fuel oil (VLSFO). Nevertheless, HFO is anticipated to retain its significance in specific applications, especially long-haul voyages where its cost advantage persists. The expansion of the liquefied natural gas (LNG) fueled vessel market poses a notable challenge to HFO's market share, though this transition will likely be gradual due to substantial infrastructure and vessel investment requirements. Furthermore, regional economic expansion, particularly in emerging economies, alongside dynamic crude oil pricing, will critically influence future demand patterns.

The global marine heavy fuel oil (HFO) market, valued at XXX million units in 2025, is projected to witness significant growth during the forecast period (2025-2033). Analysis of the historical period (2019-2024) reveals a complex interplay of factors influencing consumption. While the market experienced a period of relative stability initially, the introduction of stricter environmental regulations, particularly concerning sulfur emissions, significantly impacted demand. The International Maritime Organization's (IMO) 2020 sulfur cap led to a substantial shift towards compliant fuels, such as very low sulfur fuel oil (VLSFO), causing a temporary dip in HFO consumption. However, HFO continues to play a role, particularly in certain segments and regions where the cost advantage remains compelling despite stricter regulations. The market's future trajectory will depend heavily on the continued evolution of environmental policies, the price differential between HFO and cleaner alternatives, and technological advancements that might allow for HFO usage with reduced environmental impact. This report examines the intricacies of these trends, providing a detailed forecast alongside a granular analysis of various segments and geographical regions, considering factors such as shipping activity, economic growth, and the adoption of alternative fuels. The interplay between the price competitiveness of HFO, the stringency of environmental regulations and technological innovations in emission control systems presents a dynamic and evolving market landscape that will continue to shape future HFO demand. The report provides a comprehensive overview of the market's trajectory, outlining potential growth areas and challenges that will define its future. Moreover, we delve into the strategies adopted by major players, providing a competitive landscape analysis that assists stakeholders in understanding their position and charting their course in this ever-changing market.

Several factors propel the marine heavy fuel oil market, despite the increasing adoption of cleaner alternatives. Cost remains a primary driver. HFO traditionally offers a significant price advantage over other marine fuels. This cost-effectiveness is particularly attractive to shipping companies operating on longer routes or with tighter budgetary constraints. In certain regions and segments, this price differential often outweighs the added costs associated with compliance measures or potential penalties for exceeding emission limits. Furthermore, the established infrastructure for HFO handling and bunkering remains a significant factor. The extensive network of ports and bunkering facilities globally is largely geared towards HFO, making it a readily available and convenient fuel option for many vessels. While the transition to cleaner fuels is underway, the comprehensive infrastructure for HFO will likely continue to support its usage for some time. Finally, the existing fleet of vessels, many of which are not retrofitted for alternative fuels, contributes to continued HFO demand. The transition to a fully sustainable fleet is a gradual process, and HFO will continue to be a significant fuel source until significant fleet modernization occurs.

The marine heavy fuel oil market faces several challenges. The most significant is the tightening of environmental regulations globally. The IMO 2020 sulfur cap, along with future regulations targeting greenhouse gas emissions, is driving a shift towards cleaner fuels. This transition poses a significant threat to HFO demand, as the cost and environmental penalties associated with its use become increasingly prohibitive. Furthermore, the growing awareness of HFO's environmental impact is leading to increasing pressure from various stakeholders, including governments, environmental organizations, and consumers. This pressure translates into tighter regulations, increased scrutiny, and potentially stricter enforcement. The fluctuating price of crude oil, the primary feedstock for HFO, also presents a challenge. Price volatility affects the competitiveness of HFO relative to other fuels, creating uncertainty for shipping companies and hindering long-term planning. Finally, the development and adoption of alternative marine fuels, such as LNG, methanol, and biofuels, pose a direct threat to HFO's market share. The technological advancements and supportive policies driving the adoption of these alternatives are putting additional pressure on the HFO market.

The global marine heavy fuel oil market exhibits regional variations in consumption patterns. While precise figures vary depending on trade routes and shipping activity, regions with high volumes of heavy-duty shipping, such as Asia-Pacific and particularly countries like China and India, represent major consumption centers. The high density of shipping lanes, extensive port activity, and significant economic growth in these regions drives substantial demand for HFO. In terms of segments, the Commercial segment dominates HFO consumption. This segment encompasses a wide range of vessels, including bulk carriers, container ships, and tankers, which generally rely on HFO for its cost-effectiveness.

The dominance of the Commercial segment is attributable to the large-scale operations and fuel needs of these vessels. The cost-effectiveness of HFO in relation to its energy density remains a significant factor influencing its continued use within this segment, even with the pressure to adopt cleaner alternatives. The future of this segment depends heavily on the pace of fleet modernization and the implementation of effective emission reduction strategies.

Despite the challenges, several factors could contribute to future growth in specific niches. Technological advancements in emission control systems might allow for the continued use of HFO with reduced environmental impact. Moreover, in regions with less stringent regulations or where the cost advantage of HFO remains significantly higher, demand may persist, particularly for older vessels that are not easily retrofitted for cleaner fuels. Finally, price fluctuations in alternative fuels could temporarily increase the competitiveness of HFO, leading to a temporary surge in demand.

This report provides a comprehensive analysis of the marine heavy fuel oil market, covering historical data, current market trends, and future projections. It provides a detailed assessment of the factors influencing market growth, including environmental regulations, technological advancements, and economic conditions. The report also offers a competitive landscape analysis, profiling major players and highlighting their strategic initiatives. Finally, it provides valuable insights for stakeholders to make informed decisions regarding their investments and strategies in the evolving marine fuel market.

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 2.17% from 2020-2034 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately 2.17%.

Key companies in the market include GS Caltex, Exxon Mobil Corporation, Bunker Holding, Chemoil, Shell, Sinopec, Lukoil-Bunker, Total Marine Fuel, Gazpromneft.

The market segments include Type, Application.

The market size is estimated to be USD 108.2 billion as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3480.00, USD 5220.00, and USD 6960.00 respectively.

The market size is provided in terms of value, measured in billion and volume, measured in K.

Yes, the market keyword associated with the report is "Marine Heavy Fuel Oil," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Marine Heavy Fuel Oil, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.