1. What is the projected Compound Annual Growth Rate (CAGR) of the Marine Heavy Fuel Oil?

The projected CAGR is approximately 2.17%.

Marine Heavy Fuel Oil

Marine Heavy Fuel OilMarine Heavy Fuel Oil by Type (IFO 180, IFO 380, World Marine Heavy Fuel Oil Production ), by Application (Commercial, Navy, Others, World Marine Heavy Fuel Oil Production ), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2026-2034

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

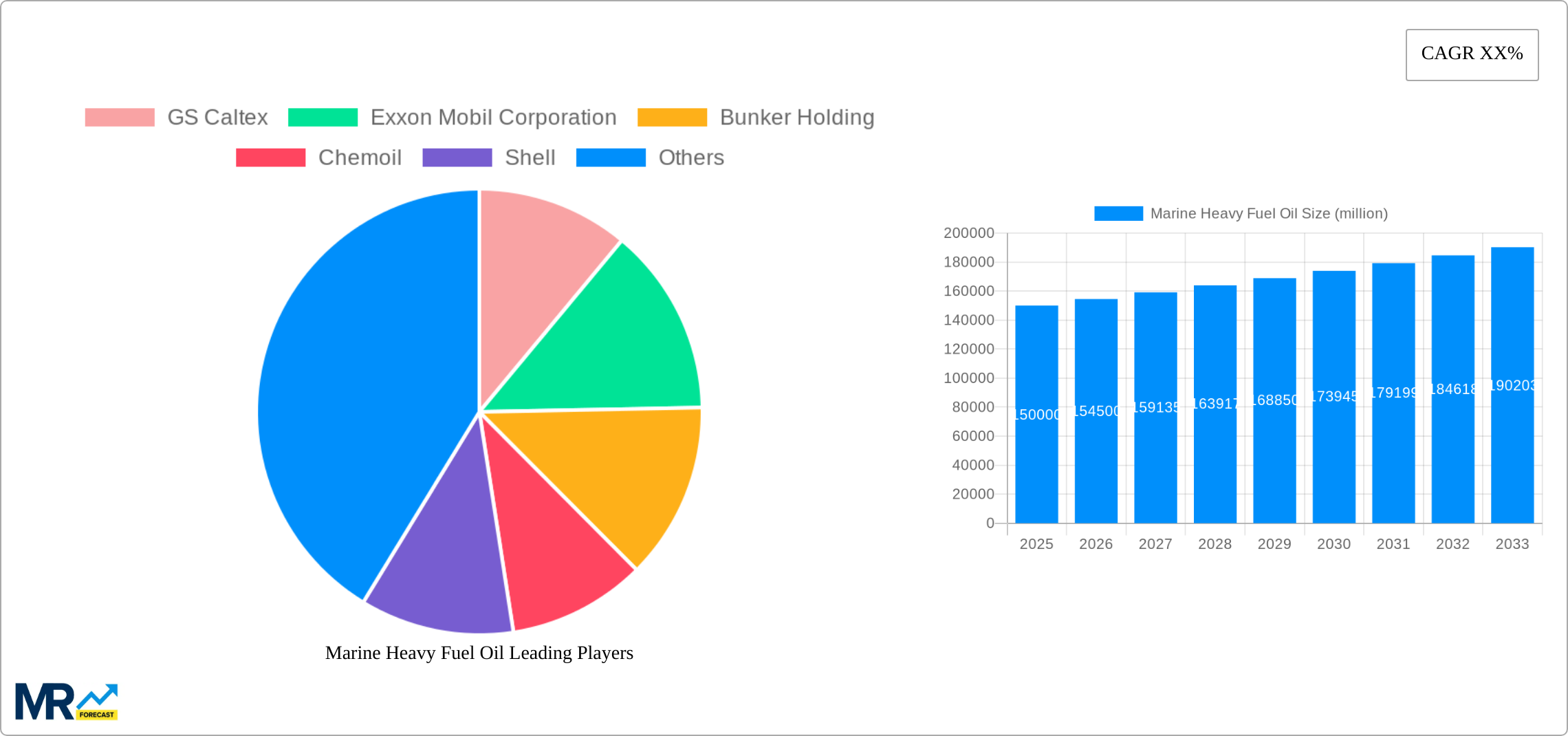

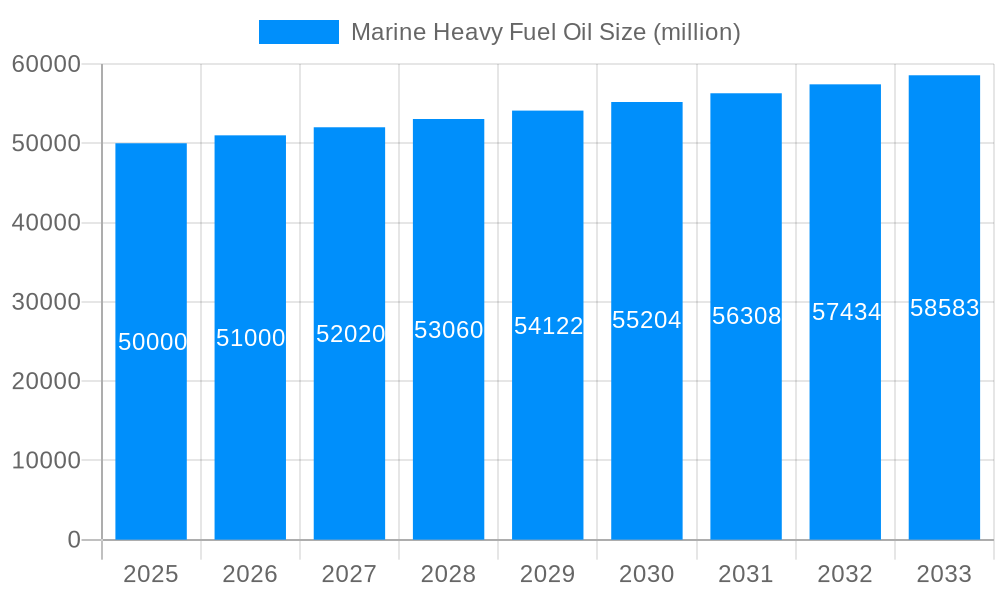

The global marine heavy fuel oil (HFO) market, a crucial component of the maritime industry, is propelled by the substantial energy requirements of large commercial and naval vessels. Despite facing increased environmental regulations and a shift towards cleaner alternatives such as liquefied natural gas (LNG) and low-sulfur fuels, the market is projected to expand at a moderate rate. The market size is estimated at 108.2 billion in the base year 2025, with a projected Compound Annual Growth Rate (CAGR) of 2.17% for the forecast period (2025-2033). This growth is underpinned by the ongoing expansion of global trade and maritime shipping. Key market restraints include the International Maritime Organization's (IMO) 2020 sulfur cap and the escalating adoption of cleaner fuel technologies. Market segmentation highlights a dominant reliance on IFO 180 and IFO 380 fuel grades, primarily within commercial shipping applications. Geographically, the market is concentrated in regions with significant port infrastructure and high shipping activity, notably Asia-Pacific and Europe. Leading industry players like Shell and ExxonMobil are actively strategizing to navigate this evolving landscape, including investments in low-sulfur fuel production and alternative fuel solutions.

The future trajectory of the marine HFO market is intricately linked to the adoption rate of alternative fuels and advancements in emissions reduction technologies. While HFO is anticipated to retain relevance in certain segments, particularly long-haul shipping lacking extensive LNG infrastructure, its market share is expected to progressively decrease. The industry's evolution will be characterized by sustained investment in research and development for cleaner fuel alternatives, strategic collaborations between fuel suppliers and shipping entities, and stringent enforcement of environmental regulations. Growth will be more measured, targeting specific niche applications and regions where HFO remains economically viable. The competitive environment will necessitate companies to prioritize diversification and strategic acquisitions to strengthen their portfolios and maintain market standing amidst this sector-wide transition.

The global marine heavy fuel oil (HFO) market, valued at XXX million units in 2024, is projected to witness significant growth during the forecast period (2025-2033). The market's trajectory is intricately linked to global shipping activity, economic growth, and evolving environmental regulations. While the historical period (2019-2024) showed a fluctuating trend influenced by factors like fluctuating oil prices and the initial impact of stricter emission standards, the forecast period anticipates a more nuanced picture. The International Maritime Organization's (IMO) 2020 sulfur cap significantly impacted the market, leading to a shift towards low-sulfur fuels like very low sulfur fuel oil (VLSFO). However, HFO continues to hold a substantial market share, particularly in regions with less stringent regulations or where the cost advantage of HFO remains compelling. The base year (2025) serves as a crucial point, reflecting the market’s adaptation to the new regulatory landscape and its response to persistent economic uncertainties impacting global trade. The estimated year (2025) will also reflect the ongoing balance between cost-effectiveness and environmental considerations, particularly as the global focus on reducing carbon emissions intensifies. This report analyzes the key market segments, including IFO 180 and IFO 380, and their contribution to the overall market volume. Detailed production and consumption data for the study period (2019-2033) provide insights into regional variations and market trends, allowing for a comprehensive understanding of this dynamic sector. The growth rate is expected to show a moderate increase, influenced by a combination of factors including the ongoing global economic recovery and the continued demand for shipping services. However, this growth will likely be tempered by the sustained push for decarbonization within the maritime industry.

Several factors propel the marine heavy fuel oil market. Cost remains a significant driver. HFO typically offers a lower price per unit compared to cleaner alternatives, making it economically attractive for shipping companies, particularly those operating in less regulated regions or on longer routes where fuel costs represent a substantial portion of operating expenses. Furthermore, the established infrastructure for HFO handling and bunkering in major ports globally contributes to its continued use. The existing fleet of vessels primarily designed for HFO combustion also plays a role; although the transition to alternative fuels is underway, the existing fleet represents a substantial demand that will persist for years. Finally, while the IMO 2020 regulations have impacted the market, the continued operation of older vessels, which may have limited compatibility with cleaner fuels, creates a residual demand for HFO. The geographic distribution of this demand varies, with regions having less stringent environmental standards and significant shipping activity showing greater reliance on HFO. This interplay of cost-effectiveness, existing infrastructure, and fleet composition ensures a sustained, albeit potentially contracting, market for marine HFO in the coming years.

The marine heavy fuel oil market faces significant challenges, primarily driven by stringent environmental regulations. The IMO 2020 sulfur cap drastically reduced the allowable sulfur content in marine fuels, prompting a shift away from HFO and towards cleaner alternatives like VLSFO. This regulatory pressure continues to intensify with the IMO's focus on reducing greenhouse gas emissions from shipping. Further regulations and potential carbon taxes are likely to increase the operating costs for vessels using HFO, making it less competitive. Fluctuations in crude oil prices, a key input cost, also present a major challenge. Price volatility impacts the profitability of using HFO, making it difficult for companies to accurately predict and manage their fuel expenses. Additionally, the technological advancements in alternative fuel technologies and the gradual shift towards more environmentally friendly options, such as LNG and biofuels, are gradually reducing the overall market share of HFO. The availability of bunkering infrastructure for alternative fuels also plays a role, especially in regions with limited access to these cleaner options. These combined factors create an increasingly challenging landscape for HFO, pushing it towards a niche role in the future of maritime fuel.

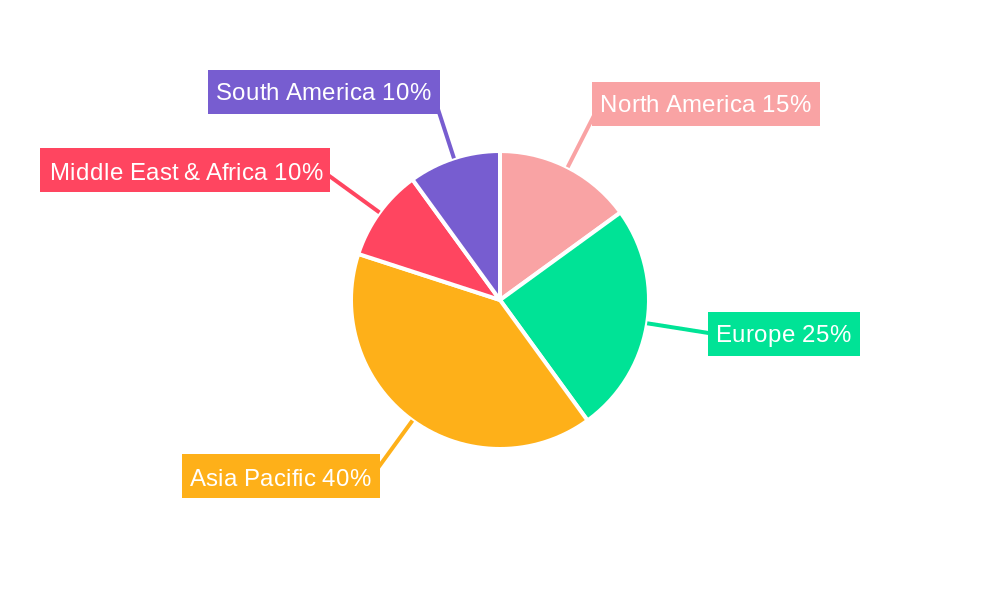

The Asia-Pacific region is anticipated to dominate the marine heavy fuel oil market throughout the forecast period due to its high volume of seaborne trade and substantial shipping activities. This region's rapid economic growth fuels increasing demand for maritime transportation, underpinning the strong consumption of HFO. Specifically, China, with its vast manufacturing and import-export operations, plays a crucial role in driving the demand for HFO.

Dominant Segment: IFO 380 is projected to maintain a larger market share compared to IFO 180 throughout the study period. This is because IFO 380 is more commonly used in larger, slower vessels, which still constitute a significant portion of the global shipping fleet.

Geographic Breakdown:

The continued use of HFO, primarily in IFO 380, is strongly influenced by economic factors and the existing fleet’s characteristics. While the transition towards cleaner fuels is undeniable, the sheer volume of existing ships using HFO ensures its persistence in the market for the foreseeable future, particularly in regions less susceptible to immediate environmental regulations. The market continues to be affected by the balance between cost pressures, existing infrastructure, and the urgency of global efforts to reduce greenhouse gas emissions.

Growth in the marine heavy fuel oil market will be driven by the continued expansion of global trade and shipping activities. While regulations are pushing toward cleaner alternatives, cost-effectiveness of HFO, especially in regions with less stringent standards, will continue to provide a base level of demand. The existing large fleet reliant on HFO is also a factor, albeit gradually declining as ships are replaced or retrofitted.

This report provides a detailed analysis of the marine heavy fuel oil market, incorporating historical data, current market trends, and future projections. It offers valuable insights for stakeholders, including manufacturers, shippers, and investors, aiding strategic decision-making in this evolving industry. The report's comprehensive coverage includes market sizing, segmentation analysis, regional breakdowns, competitive landscape assessment, and future outlook projections, enabling a well-informed understanding of the marine heavy fuel oil market's trajectory.

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 2.17% from 2020-2034 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately 2.17%.

Key companies in the market include GS Caltex, Exxon Mobil Corporation, Bunker Holding, Chemoil, Shell, Sinopec, Lukoil-Bunker, Total Marine Fuel, Gazpromneft.

The market segments include Type, Application.

The market size is estimated to be USD 108.2 billion as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4480.00, USD 6720.00, and USD 8960.00 respectively.

The market size is provided in terms of value, measured in billion and volume, measured in K.

Yes, the market keyword associated with the report is "Marine Heavy Fuel Oil," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Marine Heavy Fuel Oil, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.