1. What is the projected Compound Annual Growth Rate (CAGR) of the Lab Automation Software?

The projected CAGR is approximately 9.4%.

Lab Automation Software

Lab Automation SoftwareLab Automation Software by Type (/> Laboratory Information System (LIS), Chromatography Data System (CDS), Electronic Lab Notebook (ELN), Scientific Data Management System (SDMS), Others), by Application (/> Drug Discovery and Development, Clinical Diagnostics, Genomics, Proteomics, Others), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2026-2034

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

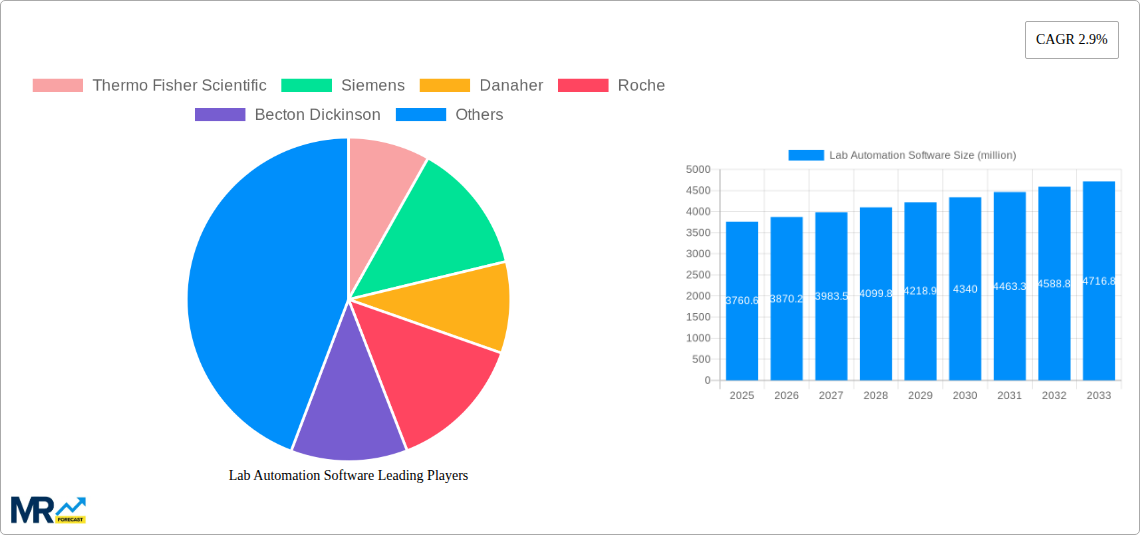

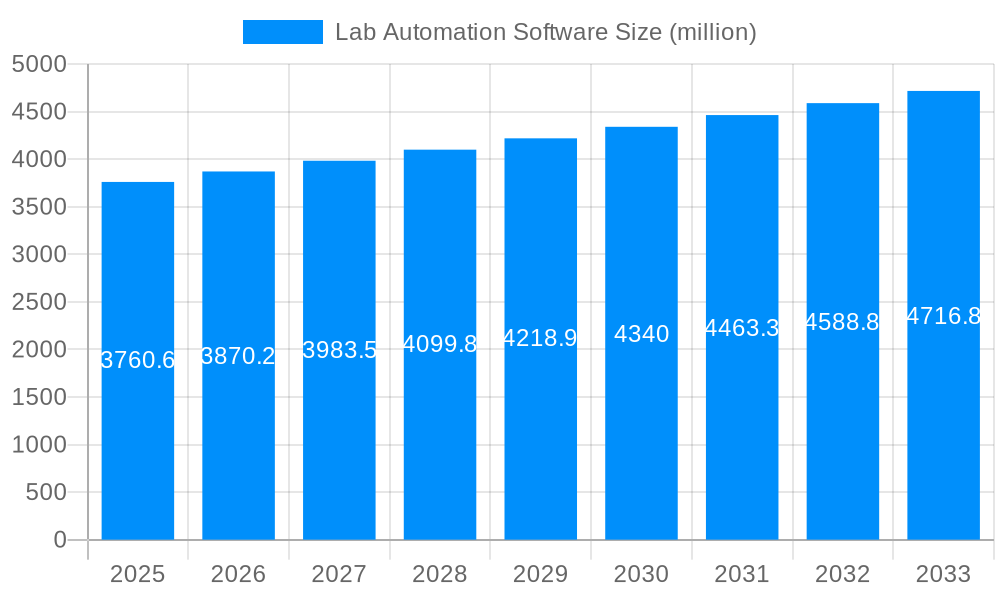

The lab automation software market, valued at $4,584.6 million in 2025, is poised for substantial growth. Driven by increasing demand for higher throughput, reduced operational costs, and improved data management in research and clinical laboratories, the market is experiencing a significant upswing. The adoption of cloud-based solutions, AI-powered analytics, and integration with other laboratory instruments are key trends shaping this market. Companies like Thermo Fisher Scientific, Siemens Healthineers, and Danaher are major players, constantly innovating to meet the evolving needs of diverse laboratory settings. While data security concerns and the high initial investment costs can pose challenges, the long-term benefits in terms of efficiency and accuracy are driving widespread adoption. The market segmentation likely includes various software types (LIMS, ELN, SDMS, etc.), deployment models (cloud, on-premise), and end-user segments (pharmaceutical, biotechnology, academic research, etc.). Competition is intense, with companies focusing on developing user-friendly interfaces, robust data analytics capabilities, and seamless integrations to maintain a competitive edge. We project a steady growth trajectory over the forecast period (2025-2033), fueled by the continuous advancements in technology and growing demand for automation solutions in diverse laboratory settings globally.

Considering the 2019-2024 historical period and the 2025 market size, and assuming a moderate CAGR (let's assume 8% for this example, a reasonable estimate for the tech sector given the stated drivers), we can project a Compound Annual Growth Rate (CAGR) that's plausible within the industry context. This CAGR translates into significant market expansion over the forecast period. The key growth drivers, as mentioned, remain the persistent need for higher efficiency, improved data analysis, and reduced human error in laboratories across various sectors. The restraints, while present, are being mitigated by continuous improvements in security protocols and more affordable and accessible cloud-based solutions. The regional breakdown would likely show strong performance across North America and Europe, followed by growth in Asia-Pacific and other developing regions as technology penetration increases.

The global lab automation software market is experiencing robust growth, projected to reach multi-billion dollar valuations by 2033. Driven by increasing demands for higher throughput, improved accuracy, and reduced operational costs within laboratories across various sectors, the market is witnessing a significant shift towards sophisticated software solutions. The historical period (2019-2024) saw steady expansion, with the base year (2025) already showcasing strong performance, indicating substantial future potential. Key trends include the integration of Artificial Intelligence (AI) and Machine Learning (ML) algorithms for predictive maintenance, data analysis, and automation optimization. Cloud-based solutions are gaining traction, offering enhanced accessibility, scalability, and collaborative capabilities. Furthermore, the market is witnessing a convergence of different software platforms, enabling seamless data exchange and integration across diverse laboratory instruments and workflows. This trend towards interconnectedness is streamlining processes and improving overall efficiency. The demand for specialized software tailored to specific applications, such as genomics, proteomics, and drug discovery, is also fueling market expansion. The increasing adoption of LIMS (Laboratory Information Management Systems) and ELN (Electronic Lab Notebooks) underscores the growing preference for digitalization in laboratory operations. These integrated systems contribute to improved data management, enhanced regulatory compliance, and reduced manual intervention. The estimated year (2025) reflects the market's current robust state, setting the stage for sustained growth throughout the forecast period (2025-2033). The market's evolution is propelled by the continuous need for accelerated research and development cycles, particularly within the pharmaceutical, biotechnology, and academic research sectors.

Several factors are contributing to the rapid expansion of the lab automation software market. The rising demand for increased efficiency and throughput in laboratories is a primary driver. As research and development activities intensify, particularly in fields like genomics and drug discovery, laboratories are increasingly burdened with large volumes of data and complex experiments. Lab automation software provides a crucial solution by automating repetitive tasks, streamlining workflows, and enabling rapid data processing. The escalating need for enhanced accuracy and reduced human error is another major factor. Automation minimizes the risk of manual errors, improving the reliability and reproducibility of experimental results, a critical consideration in regulated industries. Additionally, the increasing regulatory compliance requirements across various sectors necessitate the implementation of robust data management systems, thereby driving the adoption of lab automation software that ensures data integrity and traceability. Cost reduction is also a significant driving force, as automation minimizes labor costs and reduces the need for extensive manual intervention. Moreover, the availability of advanced technologies, such as AI and ML, is further enhancing the capabilities of lab automation software, making it more sophisticated and efficient. The integration of these technologies allows for predictive maintenance, optimized resource allocation, and advanced data analysis capabilities, further improving operational efficiency and cost-effectiveness.

Despite its significant growth potential, the lab automation software market faces certain challenges and restraints. High initial investment costs for implementing and integrating automation systems can be a deterrent for smaller laboratories or those with limited budgets. The complexity of integrating various instruments and software platforms within existing laboratory infrastructure can also pose a significant hurdle. Ensuring seamless data integration across different systems and platforms requires specialized expertise and careful planning, which can add to implementation costs and complexity. Data security and compliance with strict regulatory standards are crucial concerns. Protecting sensitive research data and ensuring compliance with regulations such as HIPAA and GDPR necessitate robust security measures and ongoing compliance efforts. The need for skilled personnel to operate and maintain these systems can also be a challenge. Finding and retaining individuals with the necessary expertise to manage and troubleshoot complex software and hardware integration can be difficult and expensive. Furthermore, the continuous evolution of laboratory technologies requires regular software updates and upgrades, which can be both time-consuming and costly. Finally, the resistance to change within some laboratories, a preference for traditional manual methods over the adoption of new technologies, can slow down market growth.

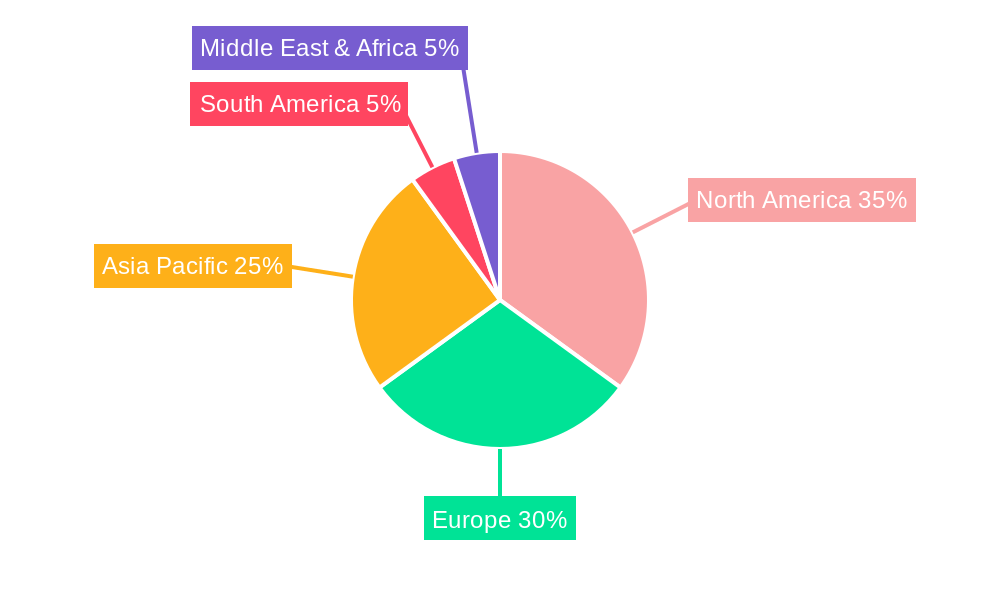

The North American market, particularly the United States, is currently a dominant force in the lab automation software market, driven by substantial investments in research and development, especially within the pharmaceutical and biotechnology sectors. The region's advanced technological infrastructure and the presence of major market players also contribute to its leading position. Europe is another significant market, with countries like Germany and the UK showcasing strong growth due to substantial government funding for research initiatives and a well-established life sciences sector. Asia-Pacific is experiencing rapid expansion, primarily driven by increasing investments in healthcare infrastructure and a growing pharmaceutical industry in countries like China, India, and Japan.

In terms of segments, the pharmaceutical and biotechnology industry holds the largest market share. This sector's substantial R&D investments and the increasing need for high-throughput screening and drug discovery drive strong demand for lab automation software. The academic research sector is also a substantial contributor to market growth, with universities and research institutions relying on automation to improve efficiency and accuracy in their research activities. The clinical diagnostics segment is also experiencing significant growth due to the rising demand for faster and more accurate diagnostic testing.

The integration of advanced technologies like AI and machine learning is significantly accelerating growth. These technologies enhance data analysis, predictive maintenance, and overall workflow optimization, leading to substantial cost savings and increased efficiency. Furthermore, the increasing demand for personalized medicine and precision diagnostics fuels the adoption of advanced lab automation software, catering to the need for sophisticated data analysis and customized workflows. The rising adoption of cloud-based solutions is also a key catalyst, offering improved accessibility, scalability, and enhanced collaboration across geographically dispersed teams.

This report provides a comprehensive analysis of the lab automation software market, covering market size, trends, drivers, challenges, key players, and future growth projections. It offers valuable insights for stakeholders, including manufacturers, software developers, investors, and end-users, enabling informed decision-making and strategic planning within this rapidly evolving sector. The report's detailed segmentation analysis allows for a granular understanding of market dynamics across various regions and application areas. The extensive data and projections presented provide a solid foundation for navigating the complexities of the lab automation software market and capitalizing on its significant growth opportunities.

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 9.4% from 2020-2034 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately 9.4%.

Key companies in the market include Thermo Fisher Scientific, Siemens, Danaher, Roche, Becton Dickinson, Agilent Technologies, Tecan, Perkinelmer, Bio-Rad Laboratories, Eppendorf, Shimadzu Corporation, Synchron Lab Automation, LabWare, Labman, Softlinx, Hudson Robotics, .

The market segments include Type, Application.

The market size is estimated to be USD XXX N/A as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4480.00, USD 6720.00, and USD 8960.00 respectively.

The market size is provided in terms of value, measured in N/A.

Yes, the market keyword associated with the report is "Lab Automation Software," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Lab Automation Software, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.