1. What is the projected Compound Annual Growth Rate (CAGR) of the Injury Prevention Service?

The projected CAGR is approximately XX%.

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

Injury Prevention Service

Injury Prevention ServiceInjury Prevention Service by Type (Participatory Ergonomics training, Office Ergonomic assessments, In-Cab Ergonomic assessments, Others), by Application (Schools, Fire Departments, Community Groups, Others), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2025-2033

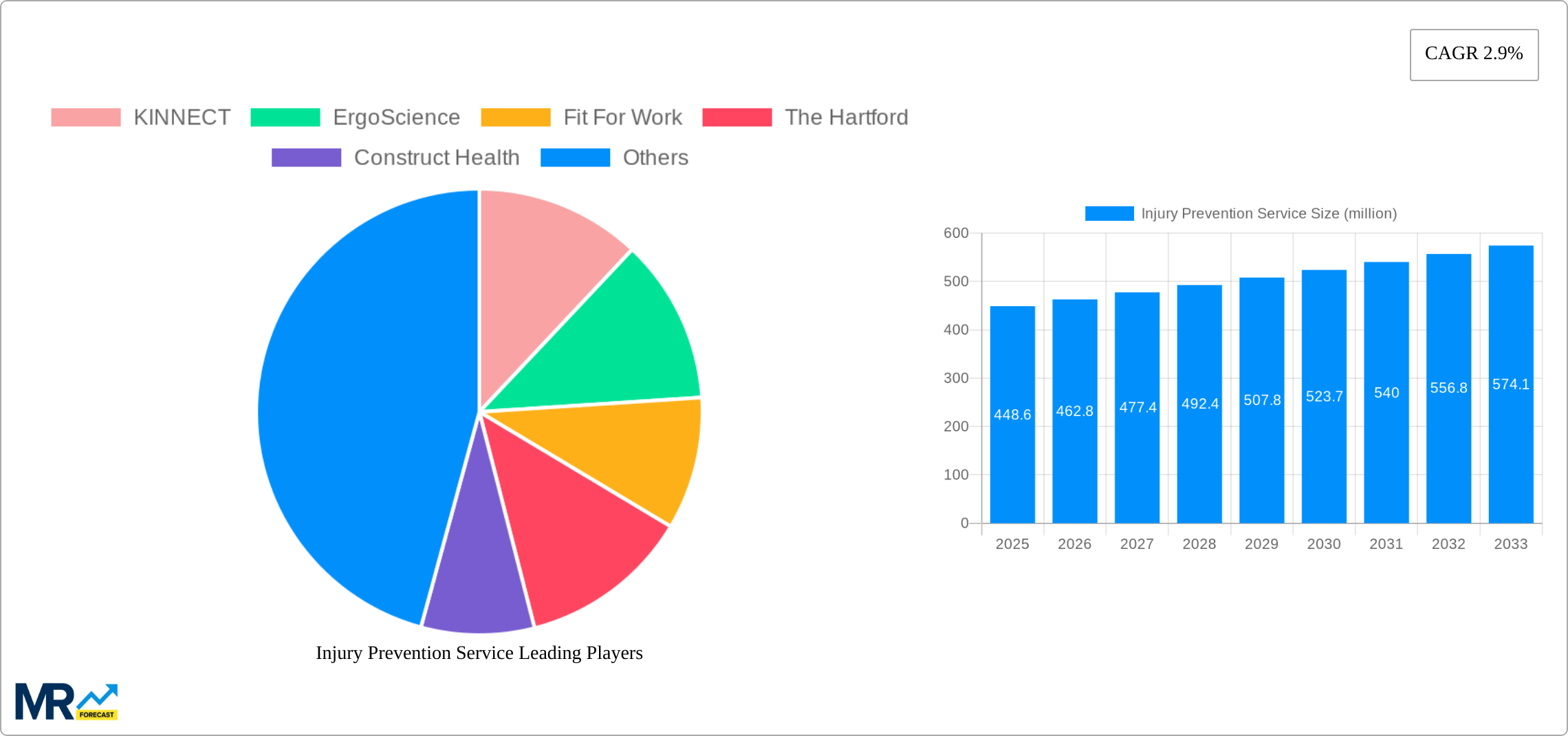

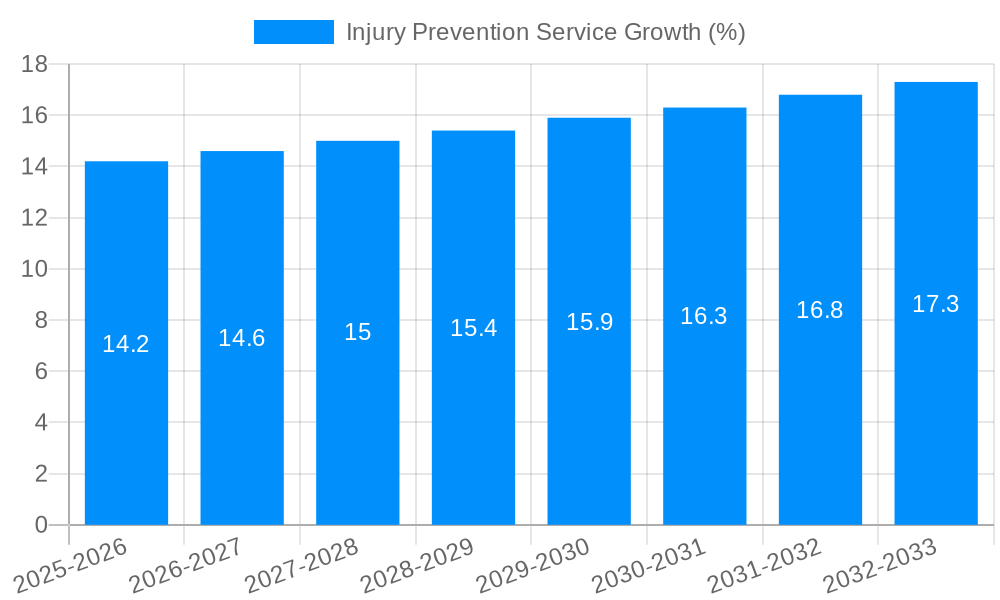

The Injury Prevention Service market, valued at $546.9 million in 2025, exhibits strong growth potential driven by increasing workplace safety regulations, rising awareness of ergonomic hazards, and a growing focus on employee well-being. The market's segmentation reveals a diverse range of services, including participatory ergonomics training, office and in-cab ergonomic assessments, catering to various sectors like schools, fire departments, and community groups. The prominent presence of numerous companies specializing in ergonomic solutions and injury prevention programs underscores the market's competitiveness and the ongoing innovation in this field. Future growth is likely to be fueled by technological advancements in ergonomic assessment tools, the increasing adoption of preventative measures in high-risk industries, and a greater emphasis on proactive health management within organizations. A projected CAGR (assuming a moderate growth rate of 7% based on industry averages for similar services) suggests significant market expansion over the forecast period (2025-2033). This growth will likely be geographically diverse, with North America and Europe leading initially due to established safety regulations and awareness, followed by growth in Asia Pacific as economies develop and prioritize worker safety.

The competitive landscape is characterized by a mix of established players and emerging companies, each offering specialized services and targeting specific market segments. The presence of large corporations alongside smaller, niche service providers creates a dynamic market where innovation and adaptation are crucial for success. Future growth will depend on the ability of companies to effectively leverage technological advancements, adapt to evolving industry needs, and effectively market their services to target segments. Factors such as increasing healthcare costs associated with workplace injuries and the growing demand for remote ergonomic assessments will shape the future trajectory of the market. The continued focus on preventative measures, rather than reactive treatments, will likely be a key driver of long-term sustainable growth within the injury prevention service sector.

The injury prevention service market is experiencing robust growth, projected to reach USD XX million by 2033, exhibiting a CAGR of XX% during the forecast period (2025-2033). The historical period (2019-2024) saw a steady increase in demand, driven by factors such as rising workplace injury rates, increasing awareness of ergonomic risks, and stringent government regulations promoting workplace safety. The base year of 2025 is estimated at USD XX million, reflecting the current market size and setting the stage for significant future expansion. Key market insights reveal a shift towards proactive injury prevention strategies, with companies increasingly prioritizing employee well-being and investing in comprehensive ergonomic assessments and training programs. This trend is particularly evident in sectors with high physical demands, such as manufacturing, healthcare, and construction. The increasing adoption of technology, such as wearable sensors and ergonomic software, is further fueling market growth by enabling more precise risk assessments and personalized intervention strategies. Moreover, the growing emphasis on return-to-work programs and the integration of injury prevention services into broader occupational health management systems are significant contributing factors. The market is also witnessing the emergence of specialized services catering to specific industries and demographics, reflecting a deeper understanding of industry-specific risks and the need for tailored solutions. The rising prevalence of musculoskeletal disorders (MSDs) globally is a major driver, leading to increased demand for services addressing this critical health concern. The market is also witnessing increased consolidation through mergers and acquisitions, with larger players acquiring smaller firms to expand their service portfolios and geographical reach.

Several factors are propelling the growth of the injury prevention service market. Firstly, the escalating costs associated with workplace injuries, including medical expenses, lost productivity, and legal liabilities, are motivating businesses to invest proactively in injury prevention measures. Secondly, a heightened awareness of ergonomic risks and their impact on employee health and well-being is driving demand for ergonomic assessments and training programs. This awareness is fuelled by increased media attention on workplace safety, stricter government regulations, and the growing understanding of the long-term health consequences of workplace injuries. Thirdly, advancements in technology are enabling more efficient and effective injury prevention strategies. Wearable sensors, virtual reality training, and sophisticated data analytics tools allow for more precise risk identification, personalized interventions, and improved monitoring of employee health. Government regulations mandating workplace safety standards and encouraging the adoption of injury prevention programs also contribute to market growth. Finally, the growing recognition of the long-term benefits of injury prevention, including improved employee morale, increased productivity, and reduced absenteeism, is further incentivizing businesses to invest in these services.

Despite the considerable growth potential, the injury prevention service market faces several challenges. High upfront costs associated with implementing comprehensive injury prevention programs can be a significant barrier for smaller businesses with limited budgets. The lack of awareness about the availability and benefits of injury prevention services, particularly among smaller companies and in certain geographic regions, remains a significant constraint. Moreover, effectively measuring the return on investment (ROI) of injury prevention programs can be challenging, making it difficult to justify the expense for some organizations. The variability in service quality across different providers can also pose a challenge, as it can lead to inconsistent outcomes and hinder the adoption of effective strategies. Finally, the need for skilled professionals with expertise in ergonomics, occupational health, and safety management creates a supply-demand imbalance in certain markets, limiting the accessibility of high-quality services. Overcoming these challenges requires collaborative efforts from government agencies, industry associations, and service providers to raise awareness, promote best practices, and improve accessibility.

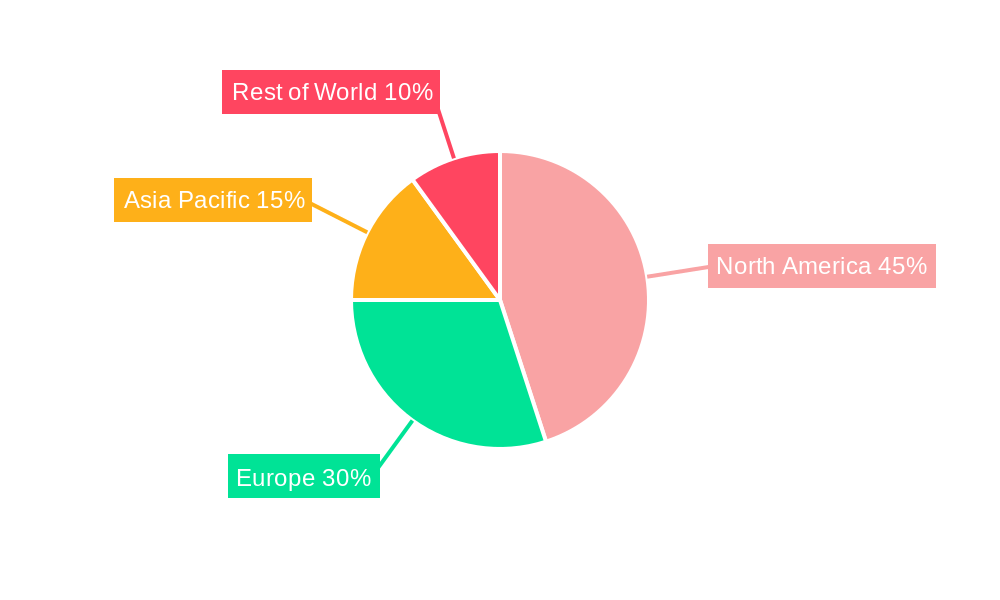

The North American market is expected to dominate the injury prevention service market throughout the forecast period. This dominance is driven by several factors: stringent workplace safety regulations, high awareness of ergonomic risks, and a significant presence of major players offering a wide range of services. Within North America, the United States is expected to hold the largest market share due to its large economy, high prevalence of workplace injuries, and substantial investment in occupational health and safety initiatives.

Dominant Segment: Office Ergonomic Assessments: This segment is poised for significant growth due to the increasing prevalence of sedentary office work and the associated risks of musculoskeletal disorders. The rising number of office workers, coupled with increased awareness of the long-term health implications of poor posture and inadequate workspace ergonomics, is driving demand for these assessments. The relatively straightforward implementation and cost-effectiveness of these assessments compared to other types of ergonomic interventions make them particularly attractive to businesses of all sizes.

Strong Performing Segment: Participatory Ergonomics Training: This segment's growth is driven by the recognition that involving employees in the design and implementation of ergonomic solutions enhances the effectiveness and sustainability of injury prevention programs. Participation boosts employee buy-in, leading to better compliance and a greater commitment to safe work practices. This approach also fosters a workplace culture of safety and proactively involves the workforce in addressing workplace hazards.

High-Growth Potential Segment: In-Cab Ergonomic Assessments: This sector is experiencing increasing demand as companies recognize the specific ergonomic challenges faced by drivers and other professionals who spend extended periods in vehicles. The rise of transportation and logistics industries, coupled with a greater awareness of the specific risks related to driving posture and vehicle design, is driving the adoption of these assessments.

The above segments will continue to drive market growth due to their relative cost-effectiveness and high impact on reducing workplace injuries.

Several factors are accelerating the growth of the injury prevention service industry. These include increasing government regulations, rising awareness of workplace safety, the growing prevalence of musculoskeletal disorders, and technological advancements. These factors collectively create a compelling case for businesses to prioritize employee well-being and invest in robust injury prevention strategies. The rising awareness among businesses regarding the cost savings associated with preventing injuries rather than managing them, further fuels market growth.

This report provides a comprehensive overview of the injury prevention service market, covering market size, trends, drivers, challenges, key players, and future growth prospects. It offers a detailed analysis of various segments, including the types of services offered and the industries served. The report also explores the impact of technological advancements and regulatory changes on the market, offering valuable insights for businesses, investors, and policymakers involved in this critical area of workplace safety and employee well-being. The projections are based on rigorous data analysis and incorporate expert industry opinions to provide a reliable forecast for future market growth.

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of XX% from 2019-2033 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately XX%.

Key companies in the market include KINNECT, ErgoScience, Fit For Work, The Hartford, Construct Health, Kinetik, WorkWell, Work-Fit, IPAR, Champion Sports Medicine, IPM Consulting Services, Cottage Health, Bodycare Workplace Solutions, The Micheli Center, Ergonomics Plus, Medcor, WorkCare, Briotix Health, ATI Worksite Solutions, Occupational Athletics, Workforce Occupational Health, .

The market segments include Type, Application.

The market size is estimated to be USD 546.9 million as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4480.00, USD 6720.00, and USD 8960.00 respectively.

The market size is provided in terms of value, measured in million.

Yes, the market keyword associated with the report is "Injury Prevention Service," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Injury Prevention Service, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.