1. What is the projected Compound Annual Growth Rate (CAGR) of the Industrial Embedded Software?

The projected CAGR is approximately 7.4%.

Industrial Embedded Software

Industrial Embedded SoftwareIndustrial Embedded Software by Application (Industrial Communication, Robot, Automotive Electronics, Equipment, Energy Industry, Others), by Type (OS X, Windows, Linux), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2026-2034

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

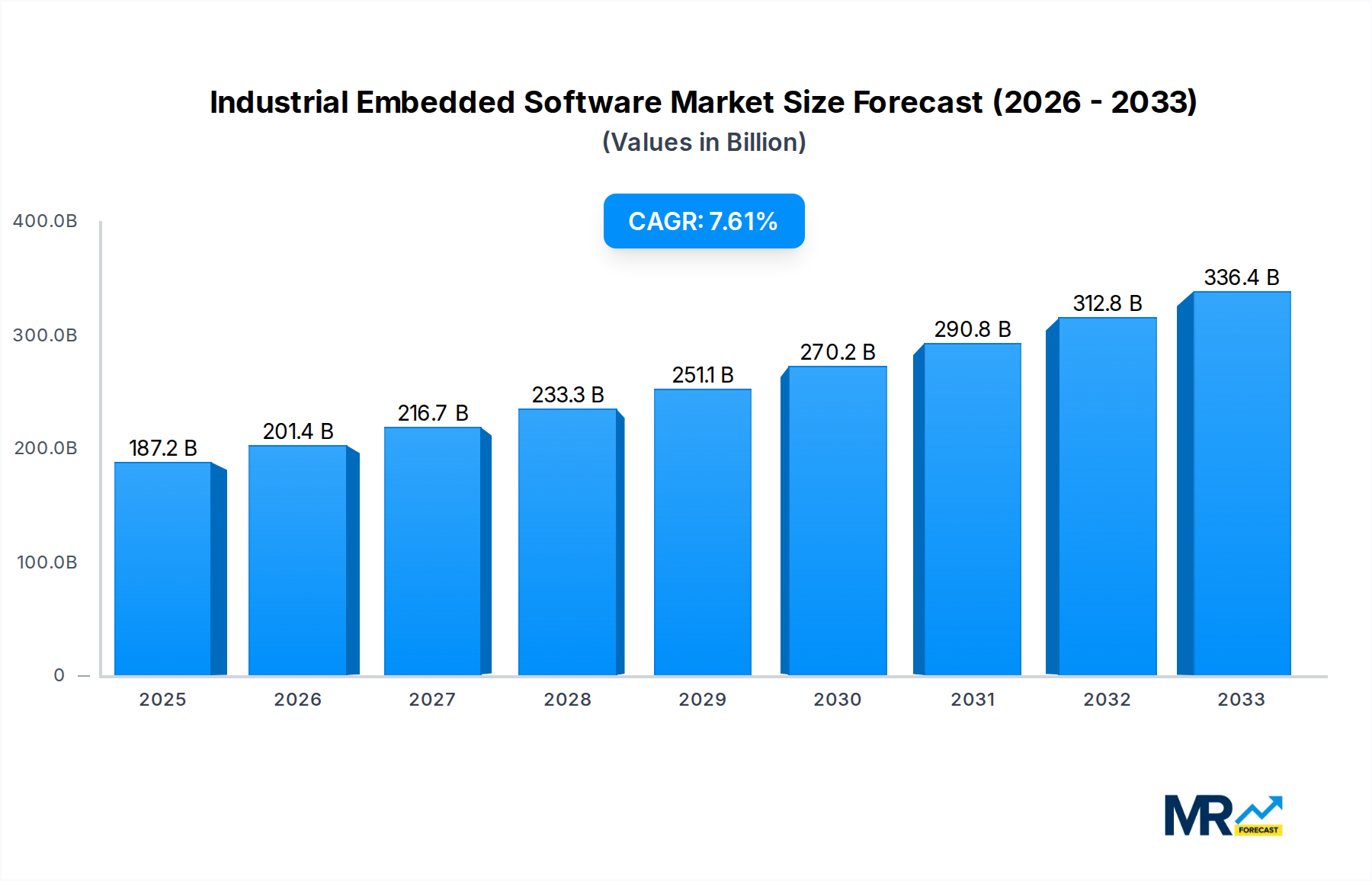

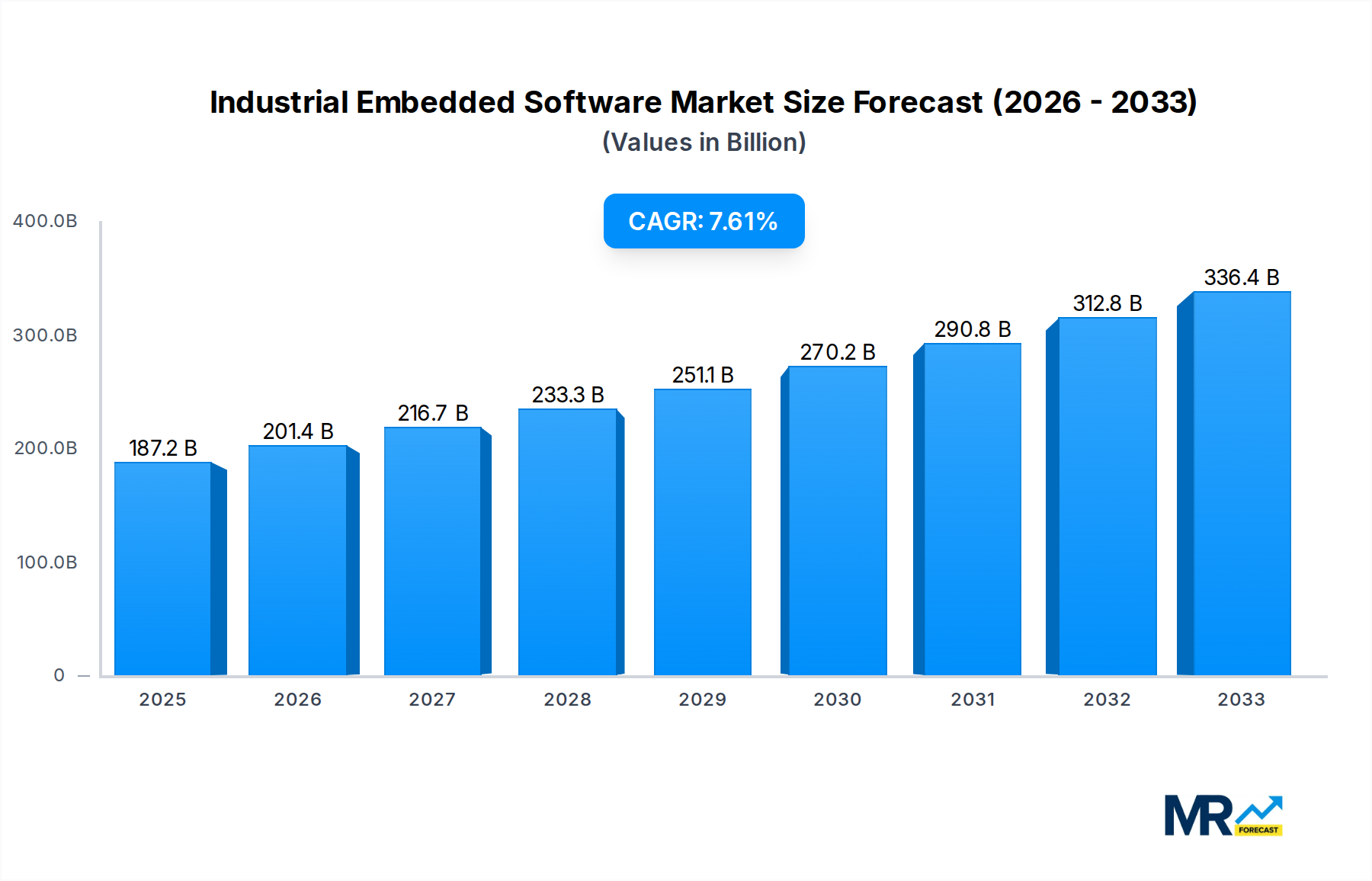

The global Industrial Embedded Software market is experiencing robust growth, estimated at $187.15 billion in 2025, and is projected to expand at a Compound Annual Growth Rate (CAGR) of 7.4% through 2033. This significant expansion is fueled by the increasing adoption of smart technologies across various industrial sectors, including industrial communication, robotics, automotive electronics, and the energy industry. The demand for sophisticated embedded software solutions is driven by the need for enhanced automation, real-time data processing, improved connectivity, and greater operational efficiency. Key growth drivers include the widespread implementation of the Industrial Internet of Things (IIoT), advancements in artificial intelligence and machine learning for industrial applications, and the growing complexity of industrial machinery requiring advanced software control. The trend towards edge computing, where data processing occurs closer to the source, is also a significant factor boosting the market as it reduces latency and improves responsiveness in critical industrial operations. Furthermore, the increasing focus on cybersecurity in industrial environments necessitates the use of advanced embedded software with robust security features.

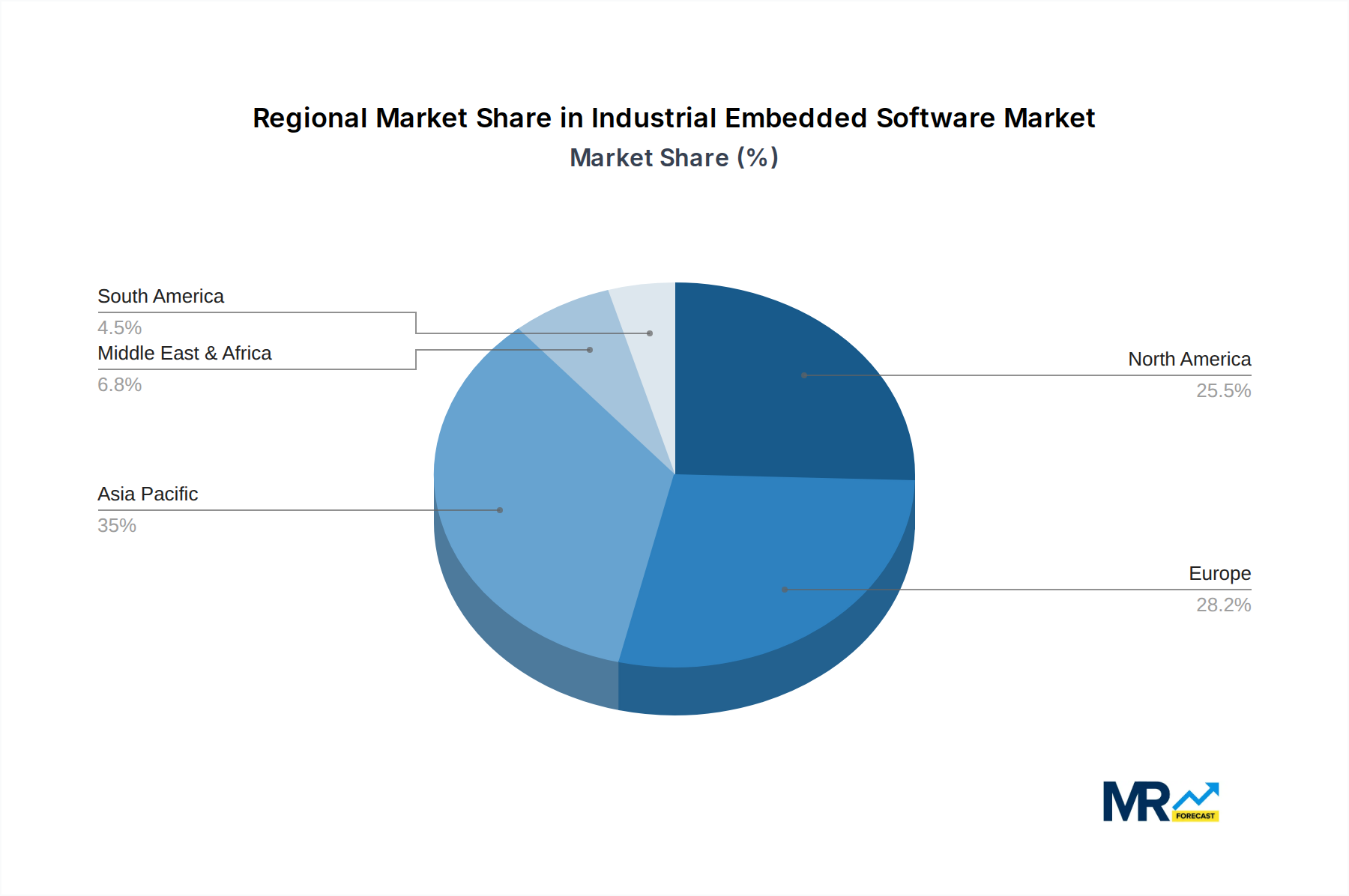

The market segmentation reveals a diverse landscape, with "Industrial Communication" and "Robotics" representing significant application areas. On the operating system front, Linux and Windows are anticipated to dominate, given their widespread adoption in industrial settings due to their flexibility, open-source nature, and extensive support. The competitive landscape is characterized by the presence of both established technology giants like Siemens, Intel, IBM, and Microsoft, as well as specialized embedded software providers such as Green Hills Software and ENEA AB. Regional analysis indicates that Asia Pacific, particularly China and Japan, is expected to be a leading market due to its strong manufacturing base and rapid technological adoption. North America and Europe also represent substantial markets, driven by significant investments in Industry 4.0 initiatives and automation. While the market presents strong growth opportunities, potential restraints include the complexity of integrating new software with legacy industrial systems and the evolving regulatory landscape surrounding industrial data and security.

The Industrial Embedded Software market is poised for substantial growth, projected to reach an estimated $130.5 billion by 2025, and is anticipated to expand to $285.2 billion by 2033, exhibiting a robust compound annual growth rate (CAGR) during the 2025-2033 forecast period. This surge is underpinned by the accelerating adoption of Industry 4.0 principles, the pervasive integration of the Industrial Internet of Things (IIoT), and the escalating demand for intelligent automation across diverse industrial sectors. Over the 2019-2024 historical period, the market has witnessed consistent expansion driven by digital transformation initiatives and the increasing complexity of industrial machinery. Key market insights reveal a significant shift towards real-time operating systems (RTOS) and specialized Linux distributions optimized for industrial environments, displacing traditional monolithic operating systems in many critical applications. The advent of edge computing is further fueling innovation, enabling data processing and decision-making closer to the point of data generation, thereby reducing latency and enhancing operational efficiency. Furthermore, the increasing sophistication of embedded AI and machine learning algorithms is empowering industrial systems with predictive maintenance capabilities, anomaly detection, and adaptive control, driving demand for software that can efficiently manage these intelligent functionalities. The cybersecurity landscape also continues to evolve, with a growing emphasis on secure coding practices, robust authentication mechanisms, and resilient network protocols to protect critical industrial infrastructure from evolving threats. The integration of 5G technology is another transformative trend, promising to unlock new possibilities for real-time industrial communication, remote monitoring, and control of a vast array of connected devices. The market is also seeing increased investment in software development tools and platforms that facilitate rapid prototyping, rigorous testing, and streamlined deployment of industrial embedded solutions. The growing emphasis on interoperability and standardization is leading to the development of middleware and communication stacks that ensure seamless data exchange between disparate industrial systems and devices. The convergence of operational technology (OT) and information technology (IT) is a defining characteristic of this era, and industrial embedded software is at the forefront of this integration, enabling a more connected and intelligent industrial ecosystem. The evolving regulatory landscape, particularly concerning safety and security standards, is also shaping the development and deployment of industrial embedded software, necessitating rigorous compliance and certification processes.

The trajectory of the Industrial Embedded Software market is being powerfully propelled by a confluence of transformative technological advancements and evolving industrial demands. The relentless march of Industry 4.0, characterized by the seamless integration of cyber-physical systems, is a primary catalyst. This paradigm shift necessitates sophisticated embedded software capable of managing complex interconnected machinery, facilitating real-time data exchange, and enabling intelligent decision-making at the edge. The burgeoning Industrial Internet of Things (IIoT) is another immense driver, connecting billions of devices within industrial settings. This expansion creates an insatiable appetite for embedded software that can manage device communication, data acquisition, processing, and secure transmission. Furthermore, the growing emphasis on automation and robotics in manufacturing, logistics, and other industrial sectors directly translates to a demand for advanced embedded software that controls robotic movements, integrates with sensor networks, and ensures collaborative operation with human workers. The increasing need for operational efficiency, predictive maintenance, and enhanced safety protocols across industries like energy, automotive, and heavy machinery is also fueling innovation in embedded software, enabling systems to self-diagnose, optimize performance, and preemptively address potential failures. The global push for sustainable practices and energy efficiency in industrial operations is also a significant factor, as embedded software plays a crucial role in optimizing energy consumption and resource management within industrial equipment and processes.

Despite the robust growth, the Industrial Embedded Software market grapples with significant challenges and restraints that warrant careful consideration. A paramount concern is the ever-evolving cybersecurity threat landscape. Industrial systems, often comprising legacy infrastructure, are increasingly targeted by sophisticated cyberattacks, necessitating highly secure and resilient embedded software. The complexity of integrating new embedded software solutions with existing legacy industrial systems can be a major hurdle, often requiring extensive customization and validation to ensure compatibility and avoid disruptions. The development and maintenance of highly specialized embedded software demand a skilled workforce with expertise in both software engineering and domain-specific industrial knowledge, a talent pool that is often in short supply. Furthermore, the stringent safety and reliability requirements in many industrial applications, particularly in sectors like aerospace, automotive, and energy, impose lengthy and rigorous testing and certification processes, which can significantly extend time-to-market and increase development costs. The fragmentation of hardware platforms and communication protocols within the industrial ecosystem also presents a challenge, requiring embedded software developers to manage a wide array of specifications and standards. The long lifecycle of industrial equipment, often in operation for decades, necessitates long-term support and maintenance for embedded software, adding to the ongoing operational expenses for manufacturers and end-users. Finally, the cost of implementing and upgrading to advanced embedded software solutions can be a significant barrier for some businesses, especially small and medium-sized enterprises (SMEs) seeking to modernize their operations.

The Asia Pacific region is projected to emerge as a dominant force in the Industrial Embedded Software market, driven by its rapidly expanding manufacturing base, substantial investments in Industry 4.0 initiatives, and the presence of a large number of key industrial players. Countries like China, South Korea, Japan, and India are at the forefront of this growth, benefiting from government support for technological innovation and the increasing adoption of smart manufacturing practices. The region's cost-effectiveness in manufacturing and its vast consumer markets further contribute to its dominance.

Within the application segments, Equipment is expected to command a significant share of the market. This broad category encompasses a wide array of industrial machinery, from manufacturing automation equipment and robotics to specialized tools used in construction, agriculture, and logistics. The increasing sophistication of industrial equipment, driven by the need for higher precision, efficiency, and automation, directly fuels the demand for advanced embedded software solutions to control, monitor, and optimize their operations. The integration of IIoT capabilities into this equipment, enabling remote diagnostics, predictive maintenance, and seamless integration into larger manufacturing workflows, further solidifies the dominance of this segment.

The Industrial Communication segment also holds substantial sway. As industrial environments become increasingly interconnected, the need for robust, reliable, and secure communication protocols is paramount. Embedded software plays a critical role in enabling this connectivity, powering everything from fieldbus systems and industrial Ethernet to wireless communication protocols for IIoT devices. The advent of 5G technology and its potential to revolutionize industrial communication networks is poised to further amplify the importance and market share of this segment.

Regarding operating systems, Linux is anticipated to be a key player in dominating the market share. Its open-source nature, flexibility, and cost-effectiveness make it an attractive choice for embedded systems in industrial applications. The availability of numerous specialized Linux distributions tailored for industrial environments, offering real-time capabilities, enhanced security features, and broad hardware support, further solidifies its position. While proprietary operating systems will continue to hold a niche, particularly in safety-critical applications, the cost-efficiency and adaptability of Linux are driving its widespread adoption across a diverse range of industrial embedded systems.

The Energy Industry segment is also a significant contributor, with embedded software playing a crucial role in smart grids, renewable energy management systems, and the control of oil and gas exploration and production equipment. The increasing focus on grid modernization, energy efficiency, and the integration of distributed energy resources is creating a substantial demand for sophisticated embedded software solutions.

The Industrial Embedded Software industry is fueled by several key growth catalysts. The accelerated adoption of Industry 4.0 and the Industrial Internet of Things (IIoT) is a primary driver, demanding intelligent and connected embedded systems. The rising need for automation, efficiency, and predictive maintenance across various industrial sectors also creates a strong demand for sophisticated software solutions. Furthermore, advancements in edge computing capabilities allow for localized data processing, enhancing real-time decision-making and responsiveness, thereby stimulating the development of specialized embedded software.

This report offers a comprehensive analysis of the global Industrial Embedded Software market, providing in-depth insights into market dynamics, key trends, and growth opportunities. The study meticulously covers the 2019-2033 period, with a detailed examination of the 2019-2024 historical period and projections for the 2025-2033 forecast period, using 2025 as the base and estimated year. It delves into critical market drivers such as the adoption of Industry 4.0 and IIoT, while also addressing significant restraints including cybersecurity threats and integration challenges. The report highlights the dominant regions and application segments, offering a strategic outlook for stakeholders. Furthermore, it identifies key growth catalysts and provides a detailed overview of leading companies and their significant developments, offering a holistic perspective for market participants.

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 7.4% from 2020-2034 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately 7.4%.

Key companies in the market include Siemens, Intel, IBM, Microsoft, ENEA AB, Green Hills Software, Advantech, Microchip, LG CNS, National Instruments, STMicroelectronics, Toshiba, Renasas, Qualcomm, Segger Microcontroller Systems, Huawei, ABB, ZTE, NARI Technology Development Limited Co, CRRC Times Elec, Haier, .

The market segments include Application, Type.

The market size is estimated to be USD XXX N/A as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3480.00, USD 5220.00, and USD 6960.00 respectively.

The market size is provided in terms of value, measured in N/A.

Yes, the market keyword associated with the report is "Industrial Embedded Software," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Industrial Embedded Software, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.