1. What is the projected Compound Annual Growth Rate (CAGR) of the High Speed Optical Transceiver Modules?

The projected CAGR is approximately 11.6%.

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

High Speed Optical Transceiver Modules

High Speed Optical Transceiver ModulesHigh Speed Optical Transceiver Modules by Type (200G, 400G, 800G), by Application (Telecom Operator, Data Operator, Private Network, Others), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2025-2033

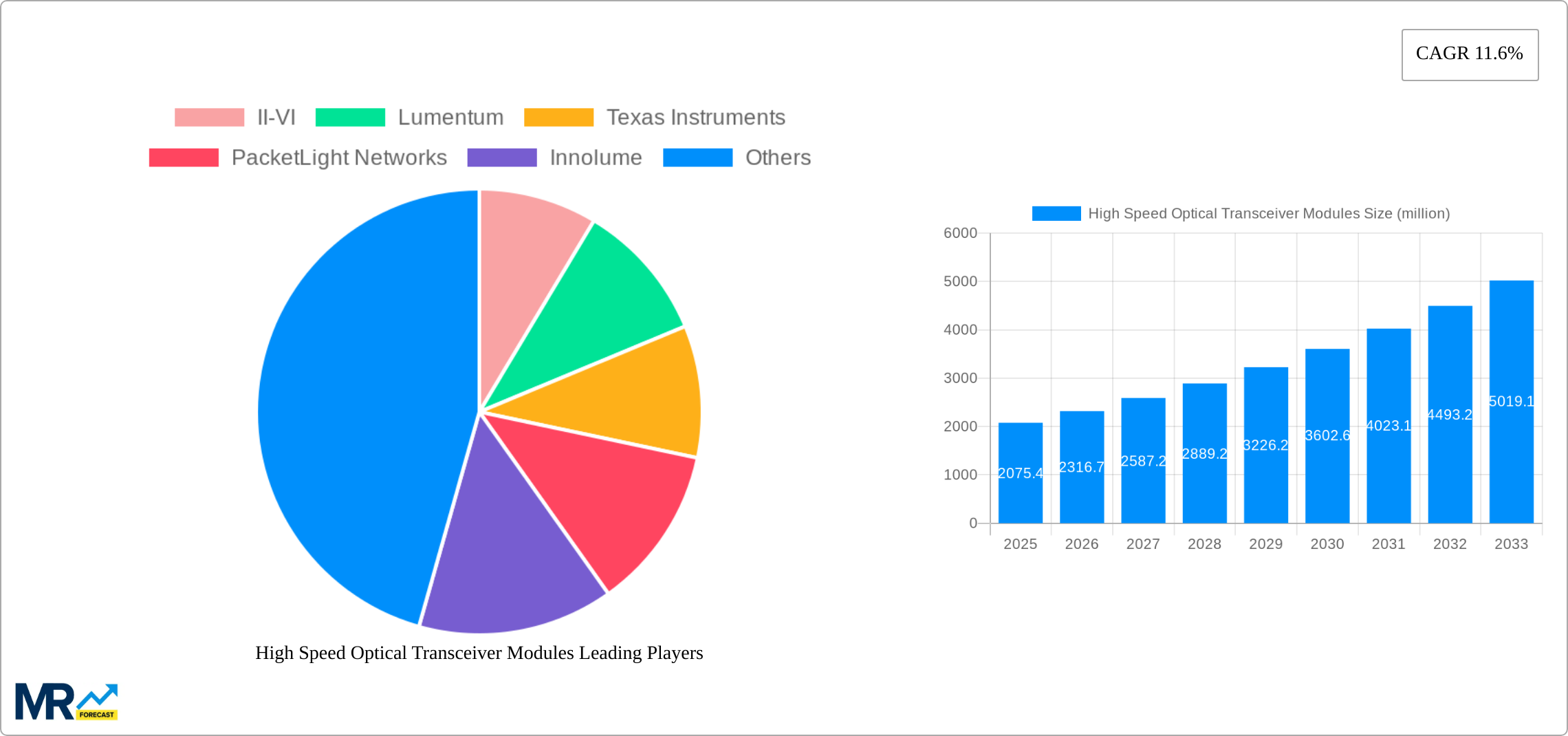

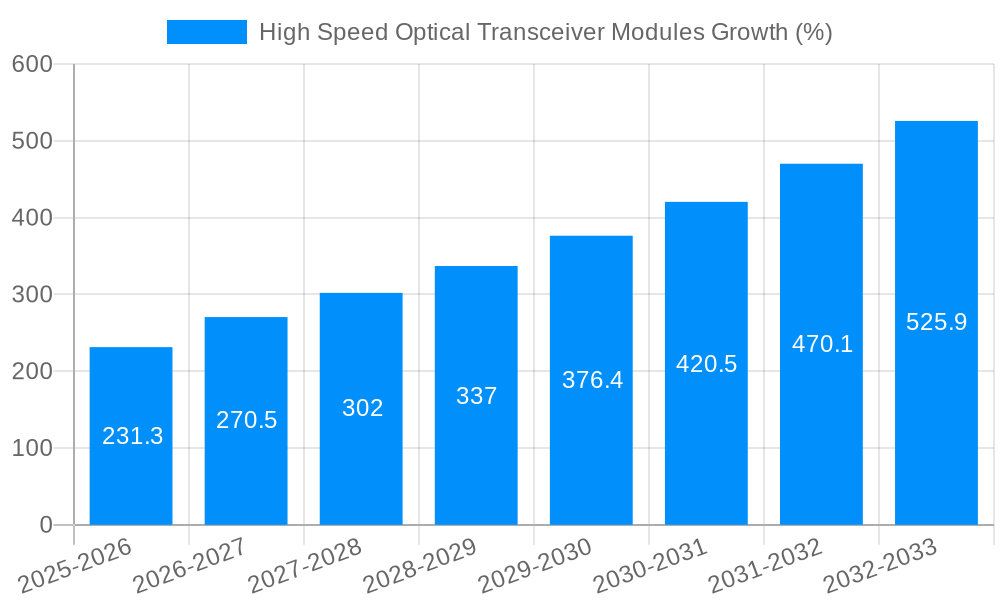

The high-speed optical transceiver module market is experiencing robust growth, projected to reach $2075.4 million in 2025 and exhibiting a Compound Annual Growth Rate (CAGR) of 11.6% from 2025 to 2033. This expansion is fueled by several key factors. The increasing demand for higher bandwidth and lower latency in data centers, fueled by cloud computing and the proliferation of 5G networks, is a significant driver. The transition to higher data rates (200G, 400G, and 800G) within telecommunication and data center infrastructure is another key contributor to market growth. Furthermore, the rising adoption of private networks in various industries, including finance and healthcare, requiring secure and high-speed connectivity, further strengthens market demand. Competition among major players like II-VI, Lumentum, and Cisco is intense, driving innovation and price reductions, making these modules more accessible to a wider range of users.

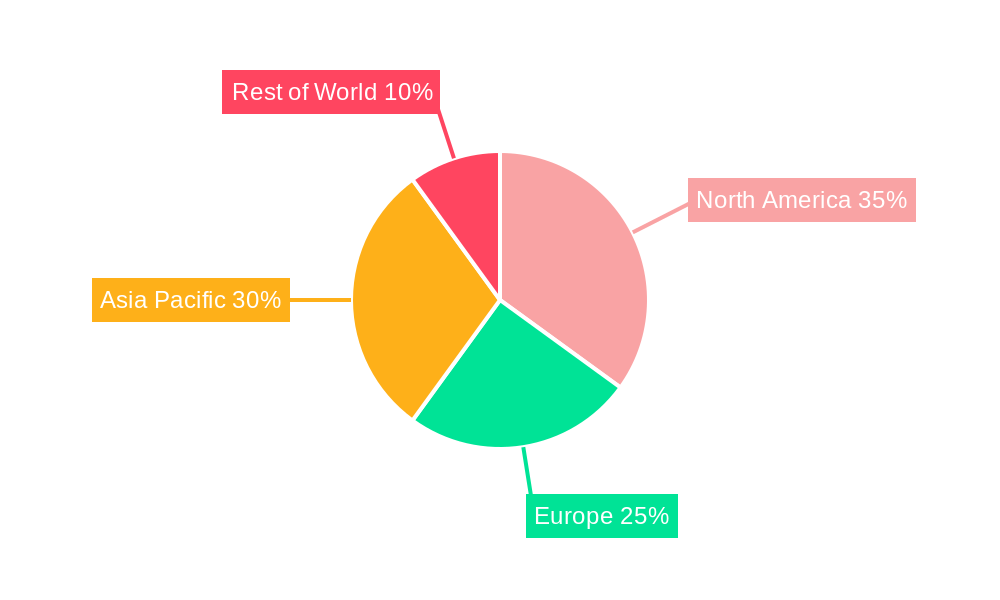

The market segmentation reveals a clear trend toward higher data rates, with 400G and 800G modules anticipated to dominate future growth. Geographically, North America and Asia Pacific are expected to lead the market, driven by strong technological advancements and high infrastructure investment in these regions. However, Europe and other regions are also demonstrating significant growth potential due to increased digitalization efforts and expanding data center capacity. While challenges exist, such as the cost of advanced technologies and potential supply chain disruptions, the overall market outlook remains positive, with consistent growth expected throughout the forecast period. The continuous advancements in technology and the ever-increasing demand for faster data transmission will continue to fuel the expansion of the high-speed optical transceiver module market.

The high-speed optical transceiver module market is experiencing explosive growth, driven by the insatiable demand for higher bandwidth and faster data transmission speeds. The market, valued at several billion dollars in 2024, is projected to reach tens of billions by 2033, exhibiting a Compound Annual Growth Rate (CAGR) exceeding 20% during the forecast period (2025-2033). This surge is fueled by the proliferation of cloud computing, 5G networks, and the increasing adoption of data-intensive applications such as video streaming, online gaming, and the Internet of Things (IoT). The historical period (2019-2024) saw significant advancements in technology, leading to the introduction of higher-speed modules like 400G and 800G, replacing older 100G and 200G variants in many applications. However, the shift isn't entirely linear. While 400G is currently dominant, the market is rapidly transitioning towards 800G and beyond, with early adoption of terabit solutions already underway. This rapid innovation cycle necessitates continuous investment in research and development to maintain competitiveness. Market segmentation reveals a dynamic interplay between module types (200G, 400G, 800G) and application segments (Telecom Operators, Data Operators, Private Networks, Others). While Telecom Operators historically dominated, Data Operators are rapidly catching up, driven by the expansion of hyperscale data centers and cloud infrastructure. The estimated market size in 2025 is projected to be in the multiple billions, underlining the market's maturity and robust growth trajectory. The forecast period (2025-2033) anticipates further consolidation, with key players focusing on strategic partnerships and acquisitions to expand their market share and product portfolios.

Several key factors are propelling the growth of the high-speed optical transceiver module market. The relentless increase in data traffic generated by cloud computing, the widespread adoption of 5G networks, and the burgeoning IoT ecosystem are primary drivers. These technologies demand significantly higher bandwidth capabilities than previous generations, creating a substantial need for faster and more efficient data transmission solutions. Furthermore, the continued miniaturization of these modules, leading to lower power consumption and cost reductions, makes them more attractive for a wider range of applications. The ongoing development of advanced optical technologies, such as coherent optical modulation formats and silicon photonics, is contributing to higher data rates and improved performance. These improvements allow for greater network capacity and reduced latency, critical elements for applications requiring real-time data processing. Finally, the increasing demand for high-bandwidth connectivity in private networks, driven by enterprises seeking to enhance their internal communication and data processing capabilities, is further boosting market growth. This diverse range of factors creates a synergistic effect, fostering a highly dynamic and expansive market.

Despite the promising growth trajectory, the high-speed optical transceiver module market faces several challenges. The high cost associated with the development and manufacturing of advanced modules remains a significant barrier to entry for smaller players. The rapid technological advancements require continuous investment in R&D, putting pressure on profit margins. The complexity of integrating these modules into existing network infrastructure can also pose significant challenges, especially for legacy systems needing upgrades. Competition is fierce, with a multitude of established and emerging players vying for market share. Maintaining consistent supply chain stability is crucial, as any disruptions can negatively impact production and delivery times. Finally, the standardization of technologies and protocols within the industry is essential for seamless interoperability, and any lack of coordination could hinder widespread adoption. Overcoming these hurdles requires strategic partnerships, continuous innovation, and robust supply chain management.

The 400G segment is currently dominating the market, accounting for a significant portion of shipments, followed by the faster 800G segment showing rapid growth. The shift is expected to continue towards even higher speeds (1.6T, etc.) in the coming years. This is primarily because 400G offers a sweet spot of performance and affordability compared to older and newer technologies.

The market is highly competitive, with established players alongside emerging innovators. This intense competition keeps prices down and pushes technological progress.

The paragraph above illustrates the dominance of 400G and 800G, the importance of North America and Asia-Pacific regions, and the key customer bases of telecom and data center operators. The Private Network segment highlights an emerging area of significant growth potential, presenting a new frontier for market expansion. This dynamic interplay of segments and geographical regions makes the high-speed optical transceiver module market incredibly complex and rewarding for those able to navigate its intricacies.

Several key factors are propelling the growth of the high-speed optical transceiver module market. The expansion of 5G infrastructure requires high-bandwidth capabilities, driving demand for these modules. The increasing adoption of cloud computing and the rise of data-intensive applications like video streaming and online gaming fuel the need for faster data transmission. Furthermore, technological advancements, such as the development of coherent optical modulation formats and silicon photonics, lead to higher data rates and improved module performance. Finally, the rising demand for private networks within enterprises boosts demand for secure and efficient high-speed connectivity.

This report offers a comprehensive overview of the high-speed optical transceiver module market, analyzing key trends, drivers, challenges, and opportunities. It provides detailed market segmentation by module type and application, covering historical data, current market estimations, and future projections. The report also profiles major market players, analyzing their strategies, market share, and competitive landscape. This information provides a valuable resource for businesses, investors, and stakeholders in the optical communications industry looking to understand the market dynamics and future growth prospects.

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 11.6% from 2019-2033 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately 11.6%.

Key companies in the market include II-VI, Lumentum, Texas Instruments, PacketLight Networks, Innolume, Avago, Cisco, Acacia, Intel, FOC, FOIT, Source Photonics, MPBC, Hisense, Fujitsu, American Microsemiconductor, Pan Dacom Direkt, Amonics, Wuxi Taclink Optoelectronics Technology, Acce Link, Zhongji InnoLight, HUAWEI, Eoptolink Technology, Sino Telecom, SONT, .

The market segments include Type, Application.

The market size is estimated to be USD 2075.4 million as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3480.00, USD 5220.00, and USD 6960.00 respectively.

The market size is provided in terms of value, measured in million and volume, measured in K.

Yes, the market keyword associated with the report is "High Speed Optical Transceiver Modules," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the High Speed Optical Transceiver Modules, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.