1. What is the projected Compound Annual Growth Rate (CAGR) of the General Data Protection Regulation Software?

The projected CAGR is approximately XX%.

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

General Data Protection Regulation Software

General Data Protection Regulation SoftwareGeneral Data Protection Regulation Software by Application (Large Enterprises, SMEs), by Type (On-premises, Cloud Based), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2025-2033

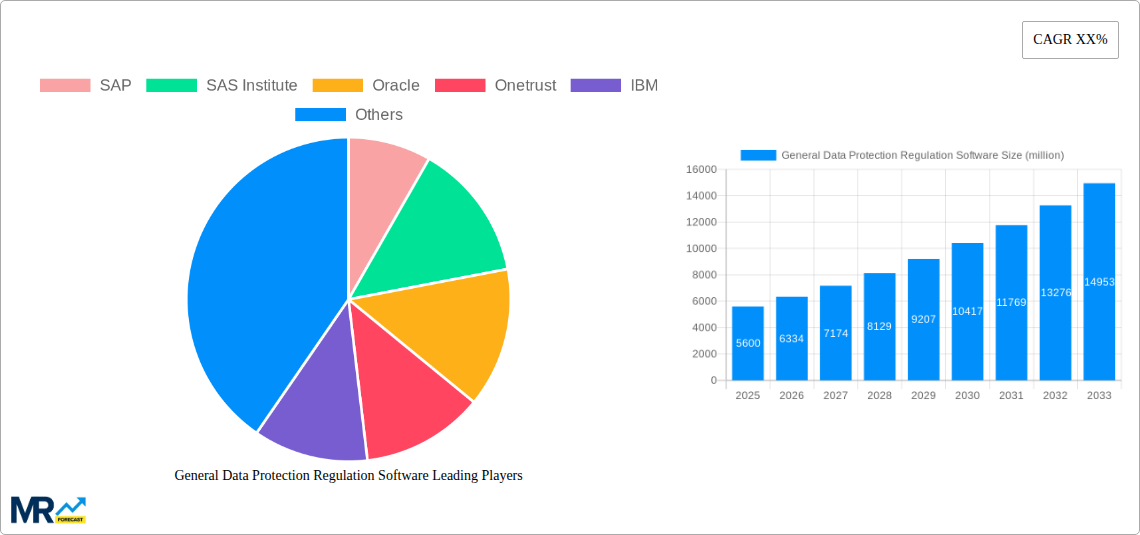

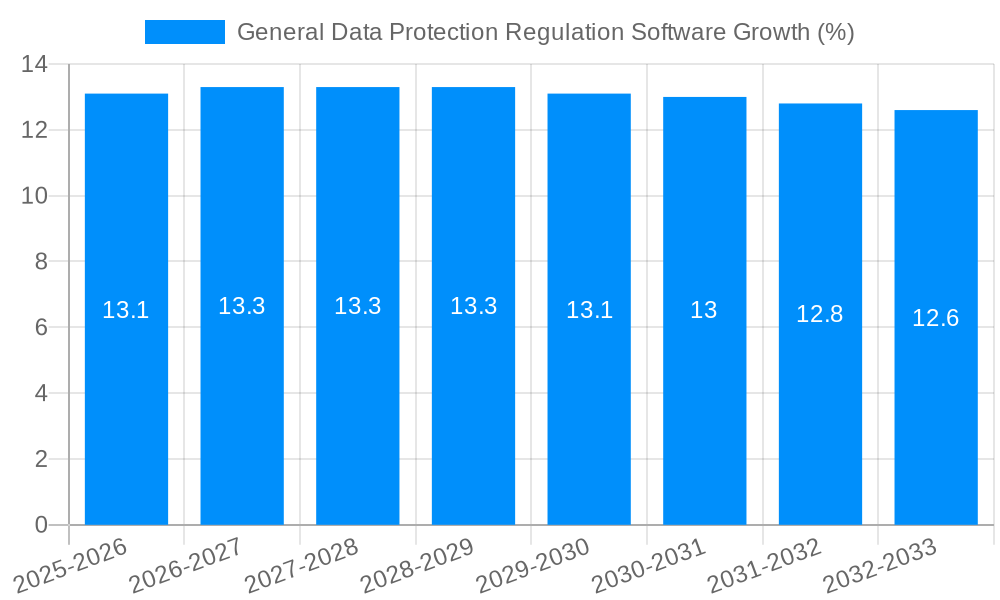

The General Data Protection Regulation (GDPR) Software market is experiencing robust growth, driven by increasing data privacy regulations globally and the rising need for organizations to ensure compliance. The market, estimated at $15 billion in 2025, is projected to exhibit a Compound Annual Growth Rate (CAGR) of 12% between 2025 and 2033, reaching approximately $45 billion by 2033. This expansion is fueled by several key factors. Firstly, the expanding scope of data privacy laws beyond the EU, such as the California Consumer Privacy Act (CCPA) and similar regulations worldwide, necessitates robust GDPR compliance software. Secondly, the increasing volume and sensitivity of data being processed by both large enterprises and SMEs demand sophisticated solutions for data governance, access control, and breach prevention. Thirdly, the cloud-based segment is rapidly gaining traction, offering scalable and cost-effective solutions to organizations of all sizes. The on-premises segment, however, continues to maintain a significant share owing to concerns around data security and control within specific organizational environments. Competition is fierce, with established players like SAP, Oracle, and IBM alongside specialized providers like OneTrust and Informatica vying for market share. The competitive landscape is characterized by continuous innovation, mergers, and acquisitions, driving improvements in functionality, integration, and user experience.

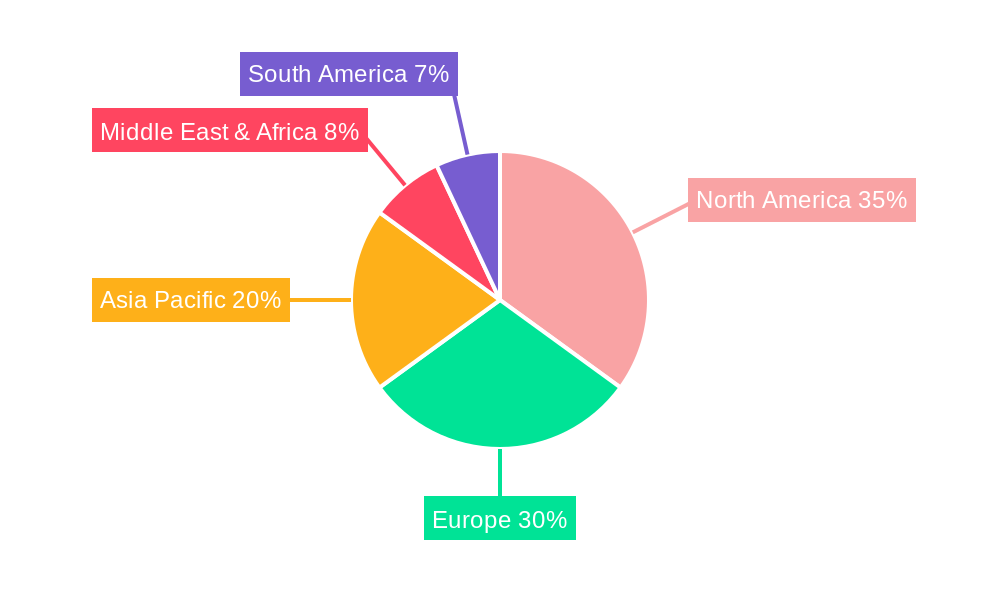

The geographical distribution of the GDPR Software market reflects the global nature of data privacy concerns. North America and Europe currently hold the largest market shares, driven by stringent regulations and high levels of digital adoption. However, the Asia-Pacific region is experiencing rapid growth, fueled by increasing digitalization and a rising awareness of data protection. The market segmentation by application (large enterprises and SMEs) showcases a distinct demand from both groups, though larger enterprises typically invest in more comprehensive and integrated solutions. Market restraints include the high cost of implementation and maintenance of GDPR software, particularly for smaller businesses, along with the ongoing evolution of data privacy regulations which necessitates continuous updates and adaptations of existing systems. Despite these challenges, the overall market outlook remains positive, driven by the critical need for robust data protection solutions in an increasingly data-driven world.

The General Data Protection Regulation (GDPR) software market is experiencing explosive growth, driven by escalating data privacy regulations globally and the increasing volume of sensitive data handled by organizations of all sizes. The market, valued at USD 12 billion in 2025, is projected to reach a staggering USD 45 billion by 2033, exhibiting a Compound Annual Growth Rate (CAGR) of over 15% during the forecast period (2025-2033). This robust expansion reflects a significant shift in organizational priorities, with data protection moving from a compliance-driven necessity to a strategic advantage. Businesses are increasingly recognizing that robust data protection not only mitigates regulatory penalties but also fosters customer trust, strengthens brand reputation, and improves operational efficiency. The historical period (2019-2024) saw substantial market maturation, with early adopters paving the way for broader adoption. The estimated year 2025 reveals a consolidated market with a higher concentration on cloud-based solutions due to their scalability and cost-effectiveness. The increasing sophistication of cyber threats and the growing prevalence of data breaches are further propelling demand for comprehensive GDPR compliance solutions. This trend is not limited to large enterprises; SMEs are rapidly adopting these technologies, recognizing the potential risks and financial implications of non-compliance. The market is witnessing a move beyond basic compliance tools towards integrated platforms that offer advanced functionalities such as data discovery, classification, masking, and monitoring, ensuring continuous compliance and proactive risk management. This evolution underlines a transition from reactive to proactive data security strategies, marking a critical turning point in the industry.

Several key factors are accelerating the growth of the GDPR software market. The stringent regulatory landscape imposed by GDPR and similar global data privacy regulations is a primary driver, compelling organizations to invest heavily in compliance solutions to avoid hefty penalties. The rising frequency and severity of data breaches are another significant impetus, as companies are increasingly recognizing the financial and reputational damage associated with data loss. The increasing sophistication of cyberattacks demands more advanced data protection technologies, fueling demand for comprehensive software solutions that go beyond basic compliance. Moreover, the growing awareness among consumers regarding their data privacy rights is putting pressure on businesses to demonstrate transparency and accountability in their data handling practices. This heightened consumer awareness creates a competitive advantage for organizations demonstrating strong commitment to data protection, translating into increased customer loyalty and trust. Finally, advancements in technology, such as artificial intelligence (AI) and machine learning (ML), are enabling the development of more intelligent and efficient GDPR software solutions, capable of automating complex tasks and providing real-time insights into data security posture.

Despite the robust growth, several challenges impede the widespread adoption of GDPR software. The complexity of GDPR regulations themselves poses a significant hurdle, making it difficult for organizations to fully understand and implement the necessary compliance measures. This complexity often necessitates specialized expertise and significant consulting fees, making compliance a costly undertaking, particularly for SMEs. The high cost of implementation and maintenance of these software solutions is another major deterrent, potentially exceeding the budget constraints of smaller businesses. Integration challenges with existing IT infrastructure represent another significant obstacle, requiring careful planning and potentially impacting operational efficiency during the transition. Data silos, prevalent in many organizations, hinder the effective implementation of GDPR compliance solutions and prevent a unified view of data security posture. Moreover, a lack of skilled professionals who possess the expertise to implement and manage these complex software solutions contributes to slow adoption rates and potential implementation failures. Finally, the ever-evolving nature of data privacy regulations requires continuous updates and upgrades to maintain compliance, imposing an ongoing financial burden on organizations.

The Cloud-Based segment is poised to dominate the GDPR software market. This dominance stems from several factors:

While both large enterprises and SMEs are significant contributors, Large Enterprises are expected to dominate the application segment due to their greater resources, heightened regulatory scrutiny, and a larger volume of sensitive data requiring protection. North America and Western Europe are currently leading regions, driven by stringent regulatory environments and high levels of awareness regarding data privacy. However, growth in the Asia-Pacific region is predicted to accelerate rapidly as regulations evolve and awareness increases across the emerging markets.

Several factors are driving significant market growth. Stringent regulatory enforcement, increasing data breach incidents, growing consumer awareness of data privacy, and technological advancements, such as AI and ML enhancing the capabilities of GDPR software, are all contributing to accelerated adoption.

This report provides a comprehensive overview of the GDPR software market, analyzing key trends, growth drivers, and challenges. It offers detailed insights into market segmentation, regional performance, competitive landscape, and significant industry developments, providing valuable information for stakeholders seeking to navigate this rapidly evolving market. The report's forecasts provide strategic guidance for investment decisions and business planning, offering a crucial resource for businesses seeking to enhance their data protection capabilities and achieve regulatory compliance.

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of XX% from 2019-2033 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately XX%.

Key companies in the market include SAP, SAS Institute, Oracle, Onetrust, IBM, Informatica, Nymity, Proofpoint, Symantec, Actiance, Snow Software, Talend, Swascan, AWS, Micro Focus, Mimecast, Protegrity, Capgemini, Hitachi Systems Security, Microsoft, Absolute Software, Metricstream, .

The market segments include Application, Type.

The market size is estimated to be USD XXX million as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4480.00, USD 6720.00, and USD 8960.00 respectively.

The market size is provided in terms of value, measured in million.

Yes, the market keyword associated with the report is "General Data Protection Regulation Software," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the General Data Protection Regulation Software, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.