1. What is the projected Compound Annual Growth Rate (CAGR) of the Gaming Software?

The projected CAGR is approximately XX%.

Gaming Software

Gaming SoftwareGaming Software by Type (Mobile Gaming, Console Gaming, PC Gaming), by Application (Amateur Gamer, Professional Gamer), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2026-2034

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

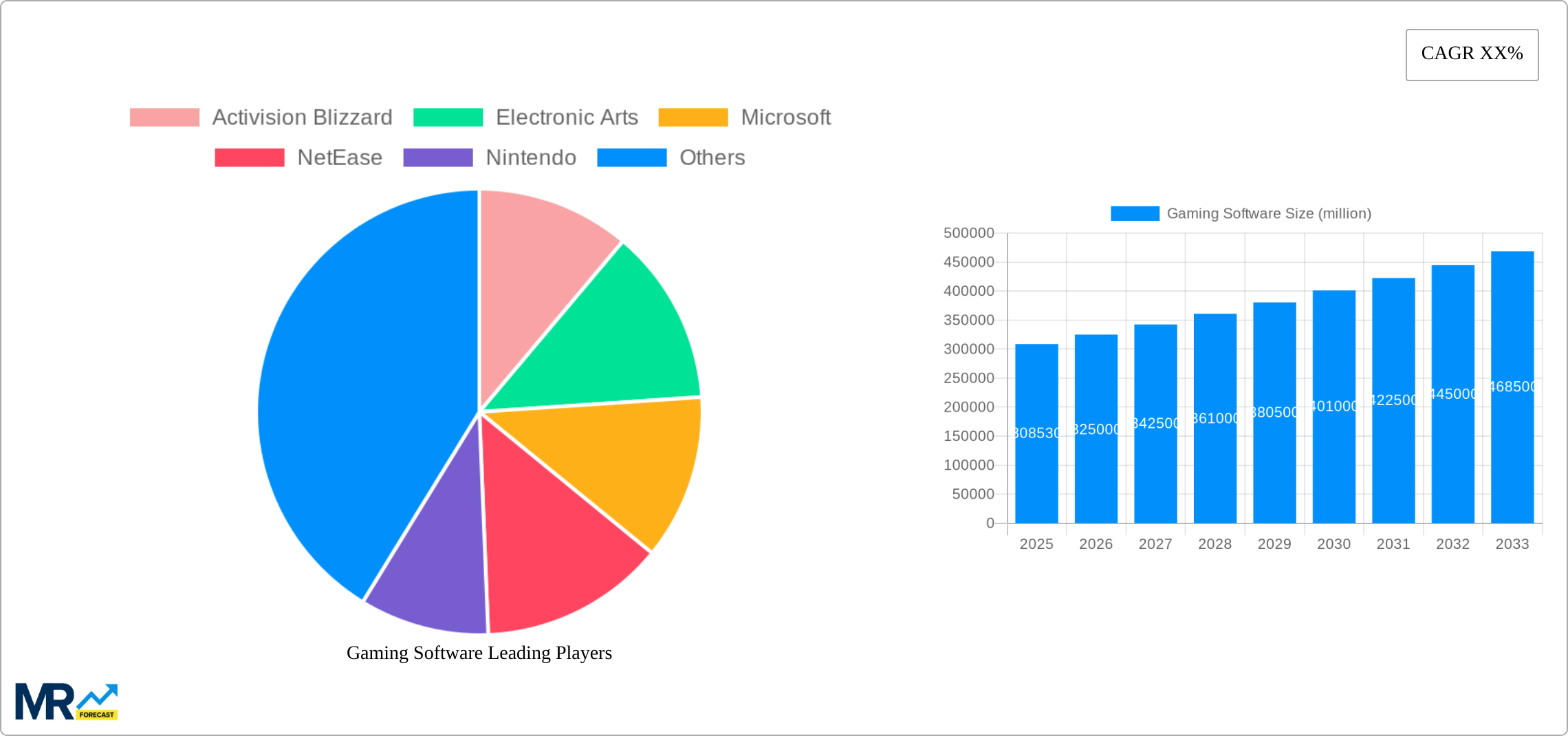

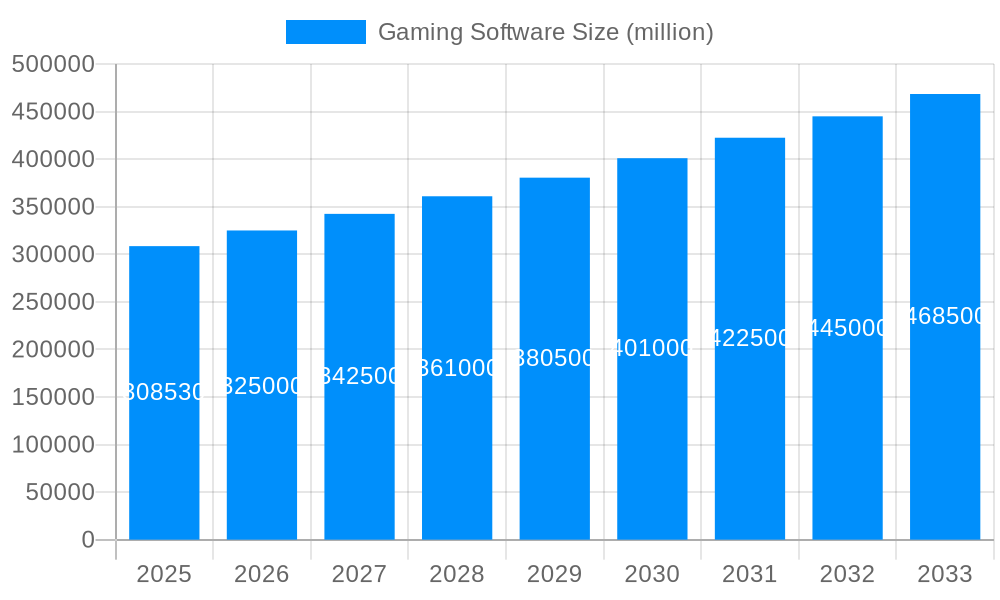

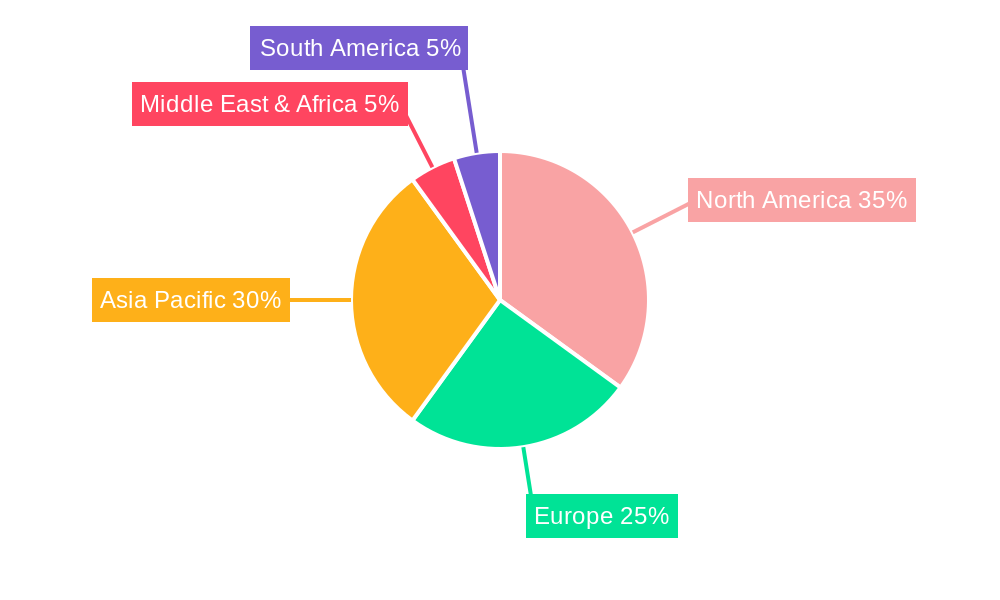

The global gaming software market, valued at $308.53 billion in 2025, is poised for significant growth. Driven by factors like increasing smartphone penetration, the rise of esports, and the continued development of immersive gaming experiences through advanced technologies such as virtual and augmented reality (VR/AR), the market is expected to exhibit substantial expansion. The mobile gaming segment dominates, fueled by the accessibility and affordability of mobile devices, while the PC and console gaming markets remain robust, catering to dedicated gamers seeking high-quality visuals and gameplay. The professional gamer segment is experiencing rapid growth, attracting substantial investment and sponsorship, while the amateur gamer segment remains the largest, driven by casual gaming's broad appeal. Geographic distribution reveals strong performance in North America and Asia-Pacific, particularly China, which is a major gaming market. However, emerging markets in South America, Africa, and other regions also present substantial growth opportunities. Competition is intense, with major players like Tencent, Activision Blizzard, and Sony competing alongside numerous independent developers and studios. The market's continued expansion will likely be shaped by ongoing technological advancements, evolving consumer preferences, and the development of innovative monetization strategies, including in-app purchases, subscriptions, and esports-related revenue streams.

The market's growth trajectory is influenced by several factors. Sustained innovation in game design, graphics, and storytelling constantly attracts new players and keeps existing ones engaged. The increasing accessibility of high-speed internet globally allows seamless online multiplayer experiences, fostering community engagement. Moreover, the integration of gaming with other entertainment forms, such as live streaming and social media, is further expanding the market's reach and influence. However, challenges remain, including concerns about game addiction, the need for robust cybersecurity measures to combat fraud and hacking, and the complexities of navigating diverse regulatory environments across different countries. Furthermore, the market's success will depend on addressing issues of accessibility and inclusivity, ensuring that gaming experiences are enjoyable and engaging for players of all backgrounds and skill levels. Looking ahead, the long-term outlook for the gaming software market remains positive, with the potential for substantial growth driven by technological advancements and evolving consumer behavior.

The global gaming software market, valued at $XXX million in 2024, is projected to reach $YYY million by 2033, exhibiting a robust CAGR of X% during the forecast period (2025-2033). This explosive growth is fueled by a confluence of factors, including the increasing affordability and accessibility of gaming hardware, the rise of mobile gaming, the expansion of esports, and the continuous evolution of game design and technology. The historical period (2019-2024) witnessed significant market expansion driven primarily by the mobile gaming segment's widespread adoption. However, the forecast period anticipates a more nuanced growth pattern, with the PC gaming segment experiencing a resurgence driven by technological advancements and the increasing popularity of PC-based esports titles. Furthermore, the blurring lines between casual and hardcore gaming, coupled with the increasing integration of cloud gaming services, is reshaping the competitive landscape and creating new opportunities for innovation and market penetration. The market is witnessing a shift towards subscription-based models, offering players access to a vast library of titles, thereby impacting revenue streams and user engagement strategies for gaming software developers. The increasing demand for immersive experiences, powered by advancements in virtual reality (VR) and augmented reality (AR) technologies, is also a key trend that promises substantial growth in the coming years. The evolving preferences of gamers, moving towards more social and interactive gaming experiences, will continue to be a major influence on the types of gaming software developed and marketed. This shift necessitates a focus on community building and cross-platform compatibility by developers.

Several key factors are propelling the growth of the gaming software market. The ever-increasing penetration of smartphones and readily available high-speed internet access has significantly boosted the mobile gaming sector, leading to a substantial surge in the number of mobile gamers globally. Simultaneously, advancements in gaming console technology, offering increasingly realistic and immersive experiences, are fueling the console gaming market's continued expansion. The burgeoning esports industry, with its massive viewership and lucrative prize pools, is attracting significant investment and driving innovation in competitive gaming software. This, in turn, fuels the demand for high-performance gaming PCs, contributing to the growth of the PC gaming segment. Moreover, the growing integration of cloud gaming services eliminates the need for high-end hardware, making gaming accessible to a broader audience, ultimately expanding the market reach. The increasing development of free-to-play models, supported by in-app purchases and microtransactions, broadens the appeal of gaming software and generates significant revenue streams for developers. Furthermore, continuous technological advancements, such as improved graphics engines, advanced artificial intelligence (AI) for non-player characters (NPCs), and enhanced game mechanics, contribute to the overall appeal and growth of the gaming software market.

Despite the significant growth potential, the gaming software market faces certain challenges. The highly competitive nature of the industry necessitates continuous innovation and adaptation to remain relevant. The emergence of new gaming platforms and technologies requires significant investment in research and development to maintain competitiveness. Furthermore, the prevalence of piracy and unauthorized software distribution poses a significant threat to revenue generation for developers. Maintaining data security and protecting user privacy are also significant concerns, especially with the increasing amount of personal information collected by gaming platforms. Regulatory hurdles and differing regional regulations concerning content and monetization strategies pose challenges to global market expansion. Fluctuations in consumer spending, particularly during economic downturns, can also impact the market's growth trajectory. Lastly, the increasing development costs associated with creating high-quality, immersive gaming experiences can constrain smaller developers and startups.

The mobile gaming segment is projected to dominate the market during the forecast period.

Asia-Pacific: This region is expected to lead in terms of revenue and user base due to the high penetration of smartphones and the burgeoning popularity of mobile esports. China, India, Japan, and South Korea are particularly important markets within this region. The sheer scale of the population base in these countries, combined with rising disposable incomes and increased access to mobile internet, provides a fertile ground for mobile gaming growth. The preference for mobile-first gaming in these regions, coupled with the widespread adoption of mobile payment systems, significantly influences the growth trajectory. The successful integration of mobile gaming into the daily lives of individuals, along with a supportive regulatory environment in some countries, further bolsters its dominance.

North America: While possessing a substantial and engaged gaming community, North America's mobile gaming market exhibits a more mature growth pattern compared to the Asia-Pacific region. However, the market is still experiencing consistent growth, driven by the increasing adoption of premium mobile games and the expanding esports ecosystem. The high average revenue per user (ARPU) in this region contributes significantly to its overall market value.

Europe: Europe shows a strong and steadily growing mobile gaming market, influenced by factors such as high smartphone penetration, robust internet infrastructure, and a diverse gaming culture. The regional variations in user preferences and gaming habits, however, require tailored strategies for effective market penetration.

The amateur gamer application segment will also show significant growth. The casual nature of gaming for many consumers, coupled with the easy accessibility of mobile and free-to-play titles, contributes greatly to the expansion of this segment. Amateur gamers represent a large and diverse population, driving the demand for a wide range of game types and genres, fueling innovation and market expansion.

Several factors are catalyzing growth. Technological advancements, especially in graphics rendering, artificial intelligence, and virtual reality, continually enhance the gaming experience. The rise of esports creates a powerful marketing engine and fuels demand for competitive titles. The growing adoption of cloud gaming platforms expands access to high-quality games, and mobile gaming's continued expansion drives market growth. Finally, innovative monetization strategies such as in-app purchases and subscription models boost revenue streams for developers.

This report offers a comprehensive analysis of the gaming software market, providing detailed insights into market trends, driving forces, challenges, and growth opportunities. It includes a detailed competitive landscape analysis, highlighting key players and their market share, as well as forecasts for revenue and growth across different segments and regions. The report is designed to be a valuable resource for industry stakeholders, including developers, publishers, investors, and market analysts.

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of XX% from 2020-2034 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately XX%.

Key companies in the market include Activision Blizzard, Electronic Arts, Microsoft, NetEase, Nintendo, Sony, Tencent, ChangYou, DeNA, GungHo, Apple, Google, Nexon, Sega, Warner Bros, Namco Bandai, Ubisoft, Square Enix, Take-Two Interactive.

The market segments include Type, Application.

The market size is estimated to be USD 308530 million as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4480.00, USD 6720.00, and USD 8960.00 respectively.

The market size is provided in terms of value, measured in million.

Yes, the market keyword associated with the report is "Gaming Software," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Gaming Software, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.