1. What is the projected Compound Annual Growth Rate (CAGR) of the Fourth Party Logistics?

The projected CAGR is approximately 5.97%.

Fourth Party Logistics

Fourth Party LogisticsFourth Party Logistics by Type (/> Synergy Plus Operating Model, Solution Integrator Model, Industry Innovator Model), by Application (/> Sea Food & Meat Products, Fruits & Vegetables, Cereals & Dairy Products, Oils & Beverages), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2026-2034

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

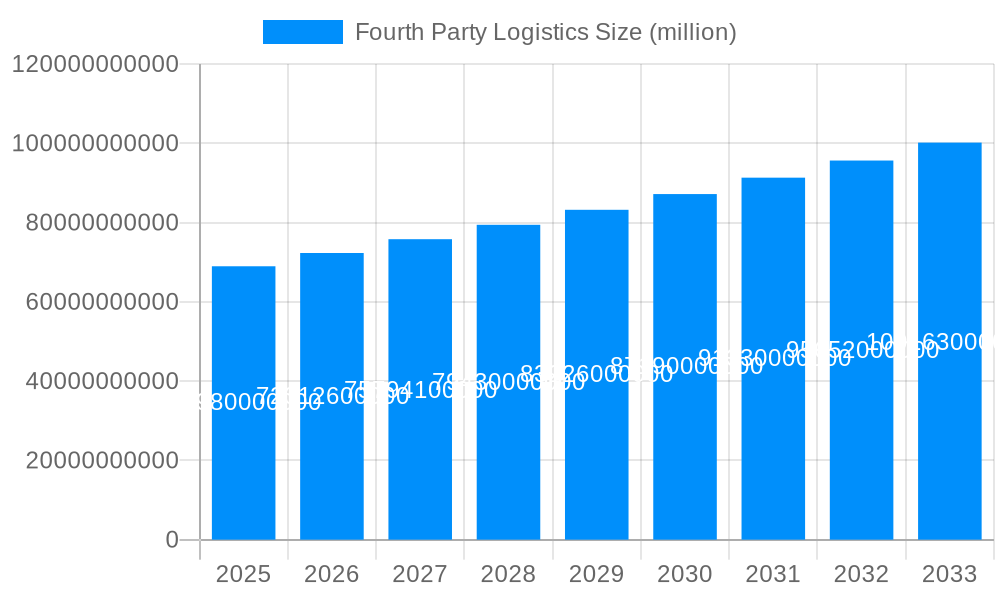

The global Fourth Party Logistics (4PL) market is poised for robust expansion, projected to reach an impressive valuation of $68.98 billion. This growth is underpinned by a compound annual growth rate (CAGR) of 4.85% throughout the forecast period of 2025-2033. This upward trajectory is largely driven by the increasing complexity of global supply chains and the escalating demand for integrated, technology-driven logistics solutions. Businesses are increasingly recognizing the strategic advantages of outsourcing their entire supply chain management to 4PL providers, who offer end-to-end visibility, optimization, and a single point of accountability. This allows companies to focus on their core competencies while benefiting from enhanced efficiency, reduced operational costs, and improved customer satisfaction. Key market drivers include the growing need for supply chain resilience, the proliferation of e-commerce, and the adoption of advanced technologies like AI, IoT, and blockchain within logistics operations.

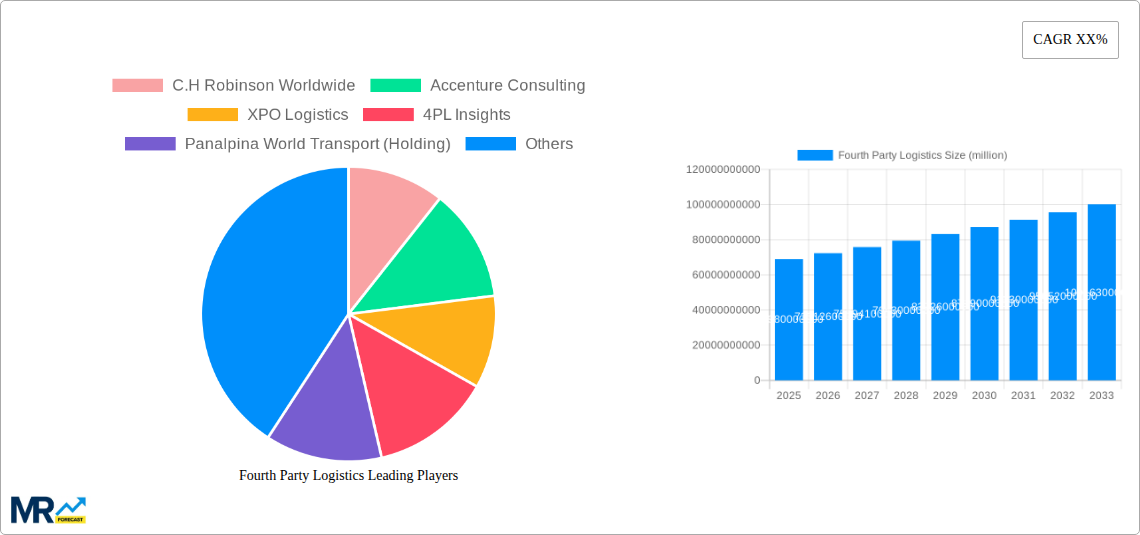

The market segmentation reveals distinct areas of opportunity. In terms of operating models, the Synergy Plus Operating Model is likely to witness significant adoption due to its emphasis on collaborative partnerships and integrated service delivery. The Solution Integrator Model also remains a strong contender, offering tailored solutions to complex logistical challenges. Industry-wise, the Sea Food & Meat Products segment, along with Fruits & Vegetables, is expected to be a key growth area, driven by the perishable nature of these goods and the associated stringent supply chain requirements. The increasing focus on efficient cold chain management and reducing spoilage further bolsters this segment. Geographically, North America and Europe are anticipated to maintain their dominance, owing to established infrastructure, high adoption rates of technology, and a strong presence of major players like C.H. Robinson Worldwide and Accenture Consulting. However, the Asia Pacific region, particularly China and India, is emerging as a critical growth hub, fueled by rapid industrialization and a burgeoning middle class. Restraints such as the high initial investment required for advanced technology implementation and the potential for data security concerns need to be addressed by providers to ensure sustained growth and market penetration.

This comprehensive report delves deep into the dynamic world of Fourth Party Logistics (4PL), offering a panoramic view of its current state and future trajectory. The study encompasses a significant period, spanning from 2019 to 2033, with a focus on the base year of 2025 and an extended forecast period from 2025 to 2033, building upon insights from the historical period of 2019-2024. The analysis will uncover critical market trends, examine the driving forces behind its expansion, identify prevailing challenges, and pinpoint the segments and regions poised for significant growth.

The Fourth Party Logistics (4PL) market is undergoing a profound transformation, moving beyond mere freight management to become a strategic enabler of end-to-end supply chain optimization. During the historical period (2019-2024), we observed a steady growth driven by increasing demand for supply chain visibility and efficiency. As we move into the base year of 2025, the market is valued at an estimated $85.3 billion, reflecting its substantial economic impact. Key market insights reveal a strong inclination towards technology integration, with Artificial Intelligence (AI) and Machine Learning (ML) becoming integral to demand forecasting, route optimization, and risk management. The emergence of the Synergy Plus Operating Model is a significant trend, emphasizing collaborative partnerships and integrated service offerings that go beyond traditional contractual relationships. Companies are increasingly adopting a Solution Integrator Model, where 4PL providers act as a single point of accountability, orchestrating a network of external providers to deliver seamless supply chain solutions. The Industry Innovator Model is also gaining traction, with 4PLs actively developing proprietary technologies and innovative processes to address complex supply chain challenges. The report will highlight how these models are being implemented across various industries, with a particular focus on the Application: /> Sea Food & Meat Products, Fruits & Vegetables, Cereals & Dairy Products, Oils & Beverages segments, where the demand for specialized handling, temperature control, and just-in-time delivery is paramount. We project the market to expand significantly, reaching an estimated $195.7 billion by 2033, indicating a compound annual growth rate (CAGR) of approximately 8.5% during the forecast period (2025-2033). This growth is fueled by a growing recognition among businesses of all sizes that a well-managed and agile supply chain is a crucial competitive advantage. The shift from a transactional approach to a strategic, value-added partnership is the defining characteristic of the current and future 4PL landscape.

The exponential growth of the Fourth Party Logistics (4PL) market is underpinned by a confluence of powerful drivers, fundamentally reshaping how businesses manage their supply chains. A primary catalyst is the ever-increasing complexity and globalization of supply chains. Companies are facing intricate networks of suppliers, manufacturers, distributors, and customers spread across vast geographical distances, making traditional in-house management increasingly challenging and inefficient. This complexity necessitates a specialized, strategic approach that 4PL providers are uniquely positioned to offer. Furthermore, the relentless pursuit of operational efficiency and cost reduction remains a central tenet for businesses. 4PLs, with their expertise in optimizing logistics networks, leveraging economies of scale, and negotiating better rates with carriers, can deliver significant cost savings that are often difficult to achieve independently. The rapid advancements in technology, particularly in areas like big data analytics, IoT, AI, and blockchain, are also acting as significant propellers. These technologies enable enhanced visibility, predictive capabilities, and real-time decision-making, all of which are core competencies of effective 4PL services. The growing emphasis on customer-centricity and the demand for faster, more reliable delivery also push businesses towards 4PL solutions, as these providers can orchestrate intricate fulfillment strategies to meet stringent customer expectations. Finally, the increasing regulatory landscape and the need for compliance across international borders add another layer of complexity that 4PLs are equipped to navigate efficiently.

Despite its robust growth trajectory, the Fourth Party Logistics (4PL) market is not without its inherent challenges and restraints that can impede its full potential. A significant hurdle is the perceived loss of control by businesses when outsourcing their entire logistics function to a third party. This can stem from a lack of trust or a fear of not being able to intervene effectively in critical situations, leading to hesitation in adopting 4PL models. The complexity of integration is another major challenge. Successfully integrating a 4PL provider into a company's existing systems, processes, and culture requires significant effort, time, and investment, and a poorly executed integration can lead to operational disruptions and unmet expectations. The high initial investment required for implementing advanced technologies and the specialized expertise needed to manage them can also be a restraining factor, particularly for smaller and medium-sized enterprises (SMEs). Furthermore, the dependency on technology can also be a double-edged sword; any downtime or cybersecurity breaches can have severe consequences for the entire supply chain, highlighting the critical need for robust security measures and contingency plans. The availability of skilled talent capable of managing complex 4PL operations is also a concern, as the demand for experienced supply chain professionals continues to outpace supply. Finally, resistance to change within an organization, particularly from departments that have historically managed logistics, can create internal friction and slow down the adoption of 4PL strategies.

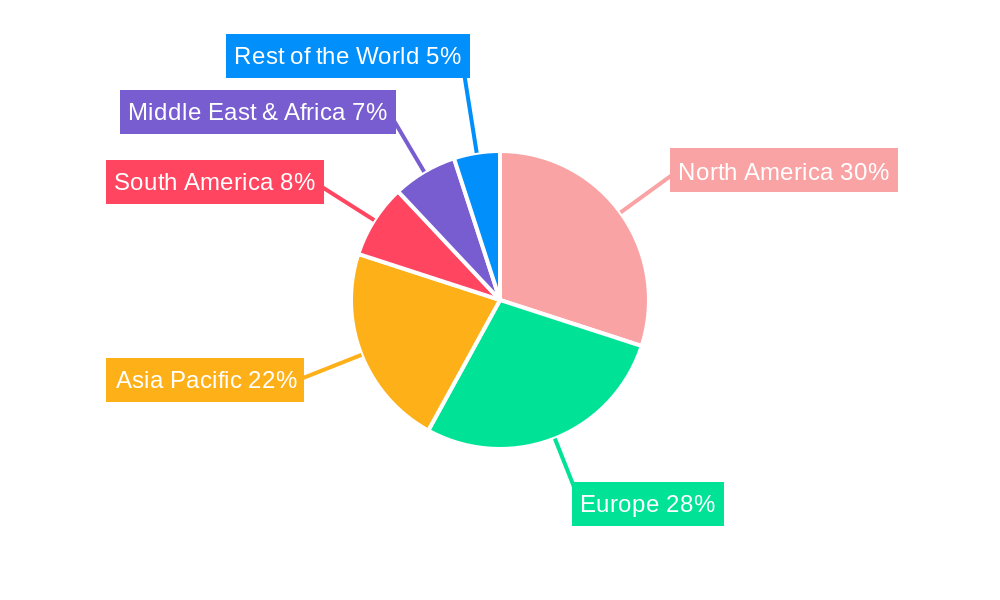

The global Fourth Party Logistics (4PL) market is characterized by regional dominance and segment specialization, with North America emerging as a frontrunner in adoption and investment, projected to hold a significant market share of approximately 35-40% by 2025, estimated at $30-$34 billion. This dominance is attributed to the region's highly developed infrastructure, advanced technological adoption, and the presence of a large number of global enterprises that require sophisticated supply chain solutions. The United States, in particular, is a key driver, with its robust manufacturing and retail sectors constantly seeking efficiency and cost optimization in their logistics operations.

Within the broader market, the Application: /> Sea Food & Meat Products, Fruits & Vegetables, Cereals & Dairy Products, Oils & Beverages segments are poised for substantial growth and are expected to collectively account for a significant portion of the 4PL market value, estimated to reach upwards of $25-$30 billion by 2025.

The Solution Integrator Model is expected to be a dominant operating model across these segments, with businesses increasingly seeking 4PLs that can act as a single point of contact to manage all aspects of their supply chain, including warehousing, transportation, inventory management, and information technology. Companies like C.H. Robinson Worldwide, XPO Logistics, and CEVA Logistics are well-positioned to leverage their extensive networks and technological capabilities to cater to the specific needs of these food and beverage-related industries.

The Fourth Party Logistics (4PL) industry's growth is significantly propelled by a burgeoning demand for enhanced supply chain visibility and control across increasingly complex global networks. The rapid acceleration of digitalization and technological adoption, particularly in areas like AI, ML, IoT, and blockchain, is providing 4PL providers with unprecedented tools for optimization, predictive analytics, and real-time decision-making. Furthermore, the persistent pressure for cost reduction and operational efficiency within businesses, coupled with a growing focus on customer satisfaction and faster delivery times, compels companies to seek strategic partnerships with specialized 4PL providers who can deliver these outcomes. The ongoing globalization of trade and the need to navigate intricate international regulations also act as potent growth catalysts, as 4PLs possess the expertise to manage these complexities effectively.

This report offers an exhaustive examination of the Fourth Party Logistics (4PL) market, meticulously dissecting its nuances from 2019 to 2033. It provides a granular analysis of market dynamics, including projected market sizes in billions of dollars for the base year of 2025 and the forecast period of 2025-2033, alongside insights derived from the historical period of 2019-2024. The report delves into critical aspects such as prevailing trends, the underlying driving forces, and the significant challenges that shape the industry's landscape. It also identifies key regions and segments poised for dominance, with a particular focus on sectors like Sea Food & Meat Products, Fruits & Vegetables, Cereals & Dairy Products, Oils & Beverages, and operational models such as the Synergy Plus Operating Model, Solution Integrator Model, and Industry Innovator Model. Furthermore, the report highlights significant developments and profiles the leading players, offering a holistic understanding of this vital sector.

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 5.97% from 2020-2034 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately 5.97%.

Key companies in the market include C.H Robinson Worldwide, Accenture Consulting, XPO Logistics, 4PL Insights, Panalpina World Transport (Holding), Deloitte Touche Tohmatsu, Global4PL Supply Chain Services, 4PL Group, Logistics Plus, CEVA Logistics.

The market segments include Type, Application.

The market size is estimated to be USD 86.2 billion as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4480.00, USD 6720.00, and USD 8960.00 respectively.

The market size is provided in terms of value, measured in billion.

Yes, the market keyword associated with the report is "Fourth Party Logistics," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Fourth Party Logistics, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.