1. What is the projected Compound Annual Growth Rate (CAGR) of the Food Rigid Packaging?

The projected CAGR is approximately 5%.

Food Rigid Packaging

Food Rigid PackagingFood Rigid Packaging by Type (Plastic, Metal, Paper, Glass, Others, World Food Rigid Packaging Production ), by Application (Fruits and Vegetables, Bakery & Confectionery, Meat, Seafood & Poultry, Dairy Foods, Ready to Eat Food, World Food Rigid Packaging Production ), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2026-2034

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

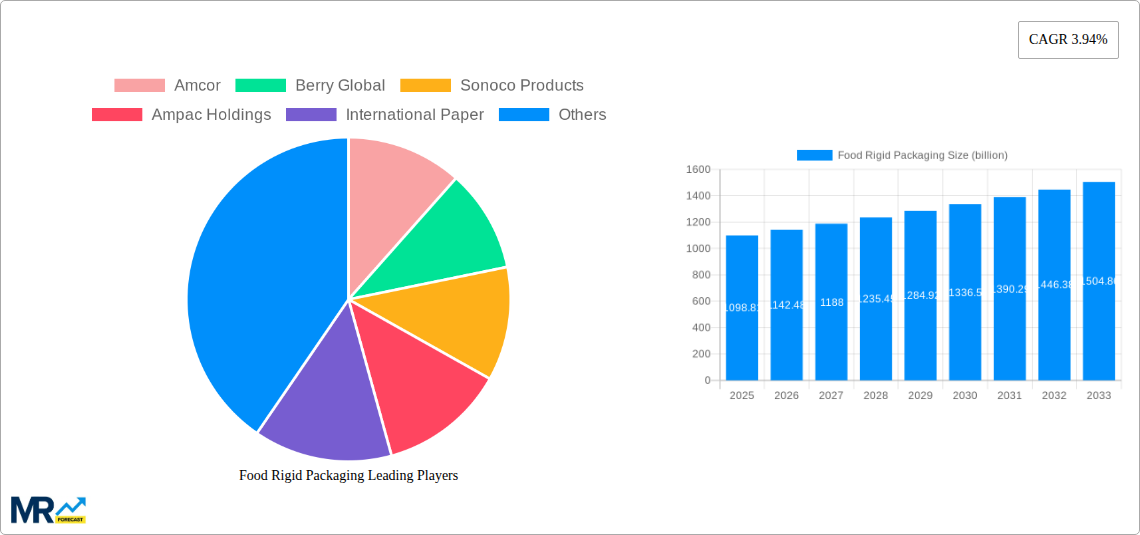

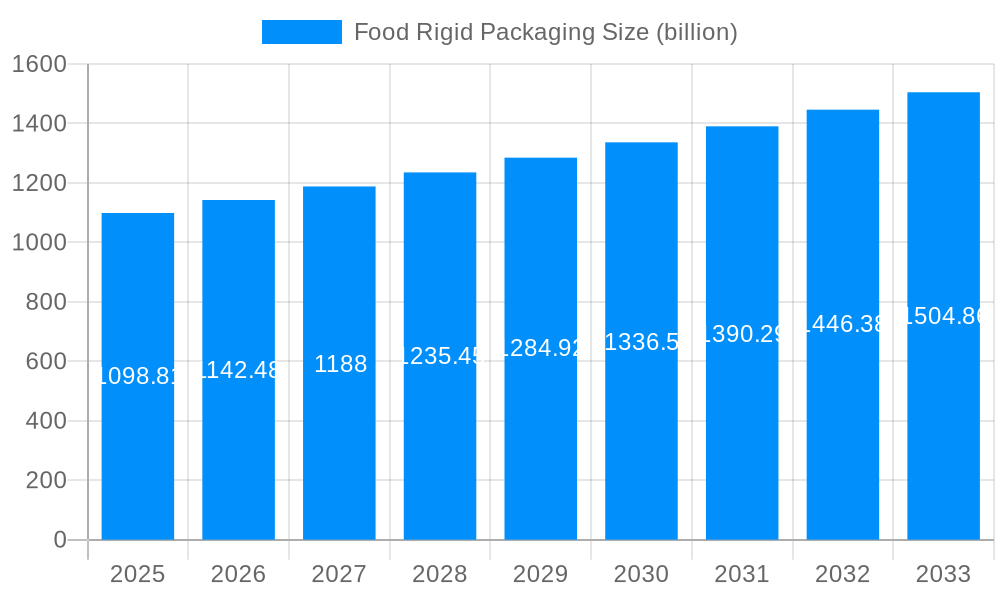

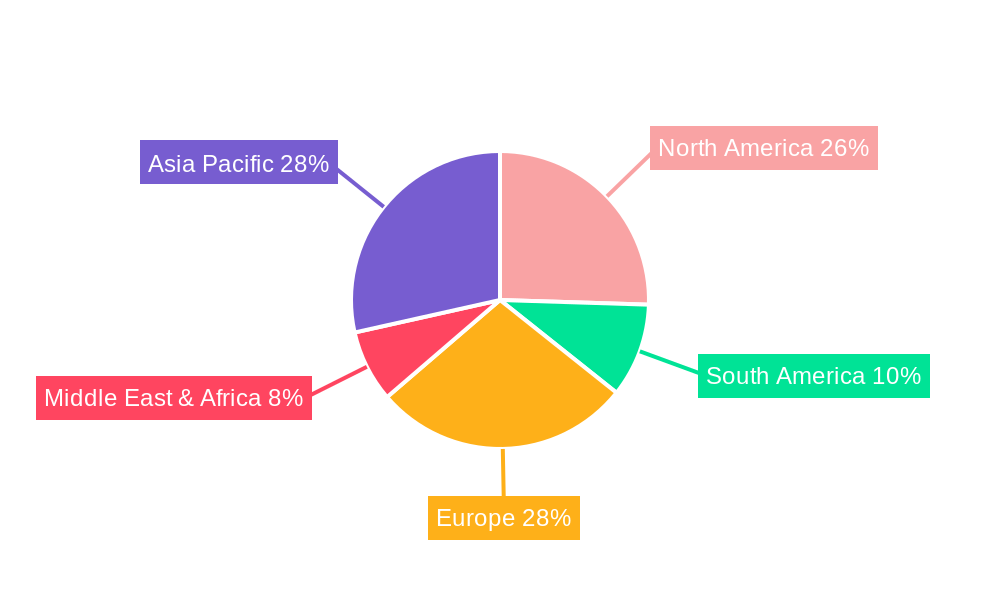

The global rigid food packaging market is poised for significant expansion, projected to reach $1,098.81 billion by 2025, with an estimated compound annual growth rate (CAGR) of 5% from 2025 to 2033. This growth trajectory is underpinned by rising consumer demand for convenience, an increased focus on food safety and preservation, and the burgeoning popularity of ready-to-eat meals. Rigid packaging offers superior protection and extended shelf life, crucial for maintaining the quality of diverse food products, from fresh produce to dairy and meat items. Emerging economies, particularly in Asia Pacific, will be key growth drivers due to expanding middle-class populations and evolving dietary habits. Technological advancements in materials and manufacturing are also contributing to the development of more sustainable and cost-effective packaging solutions.

The market is segmented by material type, including plastic, metal, paper, and glass. Plastic remains dominant due to its versatility and cost-effectiveness, while metal provides excellent barrier properties. Paper-based solutions are gaining traction due to environmental concerns, and glass is a premium option for specific food categories. Key applications include fruits and vegetables, bakery & confectionery, meat, seafood & poultry, dairy foods, and ready-to-eat food segments. Major industry players are actively investing in R&D for sustainable materials and enhanced functionality. The competitive landscape is shaped by strategic mergers, acquisitions, and partnerships aimed at global expansion and supply chain optimization.

This report offers an in-depth analysis of the global rigid food packaging market from 2019 to 2033. With 2025 as the base year, it forecasts market dynamics from 2025 to 2033, building on historical data. The global market size is projected to reach $219.95 billion, driven by consumer preferences, food safety regulations, and packaging technology advancements.

The report covers market segmentation by:

It also profiles key industry players and highlights significant industry developments and market influencers.

The global Food Rigid Packaging market is undergoing a significant transformation, driven by a confluence of consumer demands, regulatory pressures, and technological innovations. XXX, the market is witnessing a pronounced shift towards sustainable packaging solutions. Consumers are increasingly aware of the environmental impact of single-use plastics, fueling a demand for recyclable, compostable, and biodegradable alternatives. This trend is directly influencing material choices, with a growing preference for paper-based and advanced recycled plastics. The circular economy principles are gaining traction, pushing manufacturers to invest in closed-loop systems and explore novel materials that minimize waste and maximize resource utilization. Beyond sustainability, convenience and shelf-life extension remain paramount. Rigid packaging, by its nature, offers superior protection against physical damage, contamination, and spoilage, thereby reducing food waste throughout the supply chain. This is particularly crucial for perishable goods like dairy products and ready-to-eat meals. The rise of e-commerce and direct-to-consumer models is also shaping packaging trends, demanding robust and secure packaging that can withstand the rigors of shipping. Smart packaging solutions, incorporating features like temperature indicators, anti-counterfeiting measures, and even interactive elements through QR codes, are emerging as a key differentiator, enhancing consumer engagement and providing valuable product information. Furthermore, the aesthetic appeal of packaging plays a vital role in consumer purchasing decisions. Brands are investing in innovative designs, high-quality printing, and premium finishes to capture consumer attention on crowded retail shelves. The demand for transparency in ingredient sourcing and ethical production practices is also translating into packaging designs that convey these values. This multifaceted evolution underscores the dynamic nature of the Food Rigid Packaging market, where innovation and adaptation are critical for success.

The robust growth of the global Food Rigid Packaging market is underpinned by several powerful driving forces. Foremost among these is the escalating global population coupled with rising disposable incomes in emerging economies. This demographic shift directly translates into increased demand for packaged food products, as consumers seek convenience, safety, and longer shelf life. Furthermore, stringent government regulations pertaining to food safety and hygiene are compelling food manufacturers to adopt high-quality, protective packaging solutions. Rigid packaging, with its inherent barrier properties and tamper-evident features, plays a crucial role in meeting these regulatory requirements, thereby preventing contamination and ensuring consumer well-being. The burgeoning e-commerce sector also acts as a significant catalyst. The online retail of groceries and food products necessitates packaging that is not only visually appealing but also durable enough to withstand the transit process, minimizing product damage and returns. This has spurred innovation in the design and material composition of rigid packaging to ensure product integrity from warehouse to doorstep. Moreover, the increasing consumer awareness regarding food waste reduction is indirectly boosting the demand for rigid packaging. Its ability to preserve food freshness for extended periods contributes significantly to minimizing spoilage at both the retail and household levels, aligning with broader sustainability goals.

Despite the promising growth trajectory, the Food Rigid Packaging market faces a set of considerable challenges and restraints that could temper its expansion. The most prominent of these is the escalating cost of raw materials. Fluctuations in the prices of petrochemicals, metals, and paper pulp, which are the primary inputs for rigid packaging, can significantly impact manufacturing costs and, consequently, the final price of packaged goods. This volatility can affect profit margins for packaging manufacturers and potentially lead to price increases for consumers, which might dampen demand for certain product categories. Another significant hurdle is the growing consumer and regulatory pressure concerning environmental sustainability. While the market is moving towards greener alternatives, the widespread adoption of truly sustainable and cost-effective rigid packaging solutions is still in its nascent stages. The disposal and recycling infrastructure for certain types of rigid packaging, particularly complex multi-material structures, remains inadequate in many regions, leading to landfill waste and environmental concerns. This necessitates substantial investment in recycling technologies and consumer education campaigns. Furthermore, the capital-intensive nature of setting up advanced rigid packaging manufacturing facilities can act as a barrier to entry for smaller players and limit the pace of innovation. The complex supply chains involved in sourcing raw materials and distributing finished packaging also present logistical challenges that can lead to delays and increased operational costs.

The Plastic segment, particularly driven by its versatility and cost-effectiveness, is poised to dominate the global Food Rigid Packaging market. Within this segment, PET (Polyethylene Terephthalate) and PP (Polypropylene) containers will see substantial demand, especially for applications like dairy products, ready-to-eat meals, and baked goods. The inherent properties of PET, such as its clarity, strength, and barrier capabilities, make it ideal for showcasing the product and extending its shelf life. PP, on the other hand, offers excellent heat resistance, making it suitable for microwaveable and hot-fill applications, a growing trend in the ready-to-eat food segment. The North America region is expected to emerge as a dominant force in the Food Rigid Packaging market. This dominance will be fueled by a confluence of factors including a highly developed food processing industry, a strong consumer preference for convenient and pre-packaged foods, and a well-established retail infrastructure that supports a wide variety of packaged goods. The region's significant per capita disposable income also translates into a higher spending capacity for premium and convenience food options, which often rely on rigid packaging for their presentation and preservation. Furthermore, North America is at the forefront of adopting advanced packaging technologies, driven by both consumer demand for sustainability and stringent regulatory frameworks that encourage innovation in material science and recycling. The presence of major food manufacturers and packaging companies within the region also fosters a competitive environment that spurs continuous product development and market expansion. The application segment of Ready to Eat Food is also a key growth area and is expected to witness significant market share. The increasing pace of modern life, coupled with a growing demand for convenience and on-the-go consumption, has propelled the ready-to-eat food market to new heights. Rigid packaging plays a pivotal role in this segment by ensuring the freshness, safety, and aesthetic appeal of these products. From single-serving meals to meal kits, rigid containers provide the necessary protection against spoilage, contamination, and physical damage during transit and storage. The ability of rigid packaging, particularly plastic and metal containers, to withstand various temperatures and processing methods, such as retort or sterilization, makes them indispensable for a wide range of ready-to-eat food items, including soups, pasta dishes, and ethnic cuisines. The continued innovation in design and functionality of these containers, such as microwaveable features and easy-open mechanisms, further enhances their appeal to consumers seeking quick and hassle-free meal solutions.

The Food Rigid Packaging industry is experiencing significant growth catalysts that are shaping its future trajectory. A primary driver is the increasing global demand for convenience and ready-to-eat meals, necessitating robust and protective packaging. Furthermore, evolving consumer preferences towards sustainable and eco-friendly packaging solutions are pushing manufacturers to invest in recyclable, biodegradable, and compostable materials. Stringent food safety regulations worldwide are also compelling the adoption of high-quality rigid packaging that ensures product integrity and prevents contamination, thereby reducing food waste.

This comprehensive report provides an exhaustive overview of the Food Rigid Packaging market, delving into key trends, driving forces, and challenges that shape its landscape. It meticulously analyzes market segmentation by type and application, offering granular insights into the performance and outlook of various materials like plastic, metal, and paper, and their adoption across fruits and vegetables, bakery, dairy, and ready-to-eat food categories. The report further illuminates significant industry developments and strategic initiatives undertaken by leading players such as Amcor, Berry Global, and Sonoco Products, with a dedicated section profiling these key stakeholders. Its detailed market forecasts from 2025-2033, coupled with historical data analysis, equip stakeholders with actionable intelligence for strategic decision-making.

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 5% from 2020-2034 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately 5%.

Key companies in the market include Amcor, Berry Global, Sonoco Products, Ampac Holdings, International Paper, Sealed Air, Linpac Packaging, .

The market segments include Type, Application.

The market size is estimated to be USD 219.95 billion as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4480.00, USD 6720.00, and USD 8960.00 respectively.

The market size is provided in terms of value, measured in billion and volume, measured in K.

Yes, the market keyword associated with the report is "Food Rigid Packaging," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Food Rigid Packaging, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.