1. What is the projected Compound Annual Growth Rate (CAGR) of the Food & Drink Packaging?

The projected CAGR is approximately 5.4%.

Food & Drink Packaging

Food & Drink PackagingFood & Drink Packaging by Type (/> Paper & Board, Plastic, Glass, Metal), by Application (/> Food, Drink), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2026-2034

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

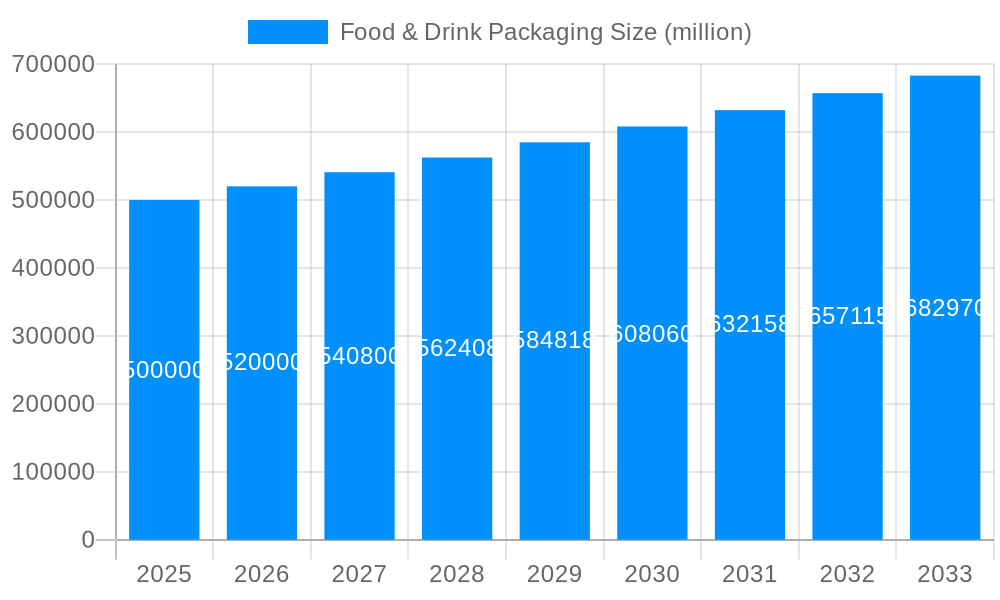

The global Food & Drink Packaging market is poised for robust expansion, projected to reach an estimated USD 421.38 billion in 2025, with a healthy Compound Annual Growth Rate (CAGR) of 5.4% expected throughout the forecast period of 2025-2033. This significant market size underscores the indispensable role of packaging in preserving product integrity, extending shelf life, enhancing consumer appeal, and facilitating efficient distribution within the food and beverage industries. Key drivers fueling this growth include the burgeoning global population, leading to increased demand for packaged food and beverages, alongside a rising middle class with greater disposable income and a preference for convenience. Furthermore, evolving consumer lifestyles, characterized by a demand for on-the-go consumption and smaller portion sizes, are actively shaping the packaging landscape. Innovations in material science, such as the development of lighter, more durable, and sustainable packaging solutions, are also playing a crucial role in market expansion. The convenience and safety offered by modern packaging continue to be paramount for consumers worldwide.

The market is segmented by material into Paper & Board, Plastic, Glass, and Metal, with Plastic and Paper & Board likely dominating due to their versatility, cost-effectiveness, and recyclability attributes, especially given the growing emphasis on sustainability. Application-wise, Food and Drink segments are the primary end-users, reflecting the pervasive need for packaging across all consumable categories. Emerging trends such as the rise of e-commerce and the demand for personalized and smart packaging solutions are creating new avenues for growth. Smart packaging, incorporating features like temperature indicators or QR codes, offers enhanced traceability and consumer engagement. However, the market also faces certain restraints, including stringent regulatory frameworks concerning food safety and environmental impact, and the volatility of raw material prices. Despite these challenges, the concerted efforts towards developing eco-friendly and recyclable packaging alternatives, coupled with the continuous innovation by key players like Amcor, Tera Pak, and Ball Corporation, are expected to steer the market towards sustained and dynamic growth.

This comprehensive report delves into the dynamic and ever-evolving Food & Drink Packaging market, offering a detailed analysis of its trajectory from 2019 to 2033. With the Base Year and Estimated Year set at 2025, the report provides in-depth insights into the market's current state and future projections, encompassing a robust Forecast Period of 2025-2033 and a thorough examination of the Historical Period from 2019-2024. The global market is anticipated to witness substantial growth, projected to reach an estimated $1,150 billion by 2025, with significant expansion expected throughout the forecast period. This report will equip stakeholders with critical intelligence on market dynamics, competitive landscapes, and strategic opportunities.

XXX, the global food and drink packaging market is on a significant growth trajectory, poised to reach an estimated $1,150 billion by 2025. This expansion is fueled by a confluence of factors, with sustainability emerging as the undisputed frontrunner in shaping consumer preferences and industry innovation. The escalating awareness surrounding environmental impact has propelled the demand for eco-friendly packaging solutions, including recyclable, compostable, and biodegradable materials. This trend is evident in the increasing adoption of paper and board packaging, which offers a compelling alternative to traditional plastics for a wide range of food and beverage products. Furthermore, advancements in material science are enabling the development of lighter yet more durable plastic alternatives, addressing concerns about plastic waste while maintaining product integrity and shelf life.

The drive towards convenience and on-the-go consumption continues to underpin market growth. Single-serving packs, resealable containers, and easy-to-open formats are increasingly sought after by busy consumers, influencing packaging design and material choices across both food and drink sectors. This translates into a higher demand for flexible packaging, particularly for snacks, beverages, and ready-to-eat meals, where its versatility and cost-effectiveness are paramount. Simultaneously, the burgeoning e-commerce sector for food and beverages presents a unique set of packaging challenges and opportunities. Robust, protective, and appealing packaging is crucial for ensuring products reach consumers in pristine condition, driving innovation in corrugated board solutions and specialized protective inserts.

A significant undercurrent within the food and drink packaging market is the increasing emphasis on enhanced product visibility and brand storytelling. Transparent packaging, vibrant graphics, and interactive elements are being employed to capture consumer attention on crowded retail shelves and online platforms. This also extends to the use of smart packaging technologies, which offer functionalities like temperature monitoring, freshness indicators, and anti-counterfeiting measures, adding value and reassurance for both consumers and manufacturers. The growing focus on health and wellness also influences packaging decisions, with a rise in demand for packaging that clearly communicates nutritional information, allergen warnings, and ingredient transparency, often utilizing clear labeling and consumer-friendly designs. The integration of these diverse trends is reshaping the entire value chain, from material sourcing to end-of-life disposal, creating a complex yet exciting landscape for industry players.

The food and drink packaging market is being propelled by a powerful synergy of macroeconomic shifts and evolving consumer behaviors. A fundamental driver is the global population growth, which directly translates into an increased demand for packaged food and beverages to ensure food security, facilitate distribution, and extend shelf life. As populations expand, particularly in emerging economies, the need for efficient and accessible food supply chains escalates, making effective packaging indispensable.

Furthermore, the ongoing trend of urbanization and a rising middle class are significant contributors. Urban dwellers typically have busier lifestyles, leading to a greater reliance on convenience foods and ready-to-drink beverages. This demographic shift creates a sustained demand for single-serving packs, portable packaging, and products that require minimal preparation, all of which are heavily reliant on innovative packaging solutions. The economic empowerment of this growing middle class also translates into increased purchasing power, allowing for greater expenditure on a wider variety of packaged goods, including premium and specialty items.

The e-commerce revolution has also emerged as a critical growth engine. The rapid expansion of online grocery and food delivery services necessitates specialized packaging that can withstand the rigors of transit and maintain product integrity from warehouse to doorstep. This has spurred innovation in protective packaging, cushioning materials, and tamper-evident seals. Additionally, the increasing global trade and complex supply chains for food and beverages necessitate robust packaging to prevent spoilage, damage, and contamination during long-distance transportation. This ensures that products remain safe and appealing for consumers across diverse geographical locations.

Despite the robust growth, the food and drink packaging industry faces several significant challenges and restraints that can impede its progress. The most prominent of these is the increasingly stringent regulatory landscape. Governments worldwide are implementing stricter regulations concerning packaging materials, recyclability, and waste management, driven by environmental concerns. These regulations can lead to higher compliance costs for manufacturers, requiring investment in new technologies and materials, and potentially restricting the use of certain conventional packaging formats.

The volatility of raw material prices presents another substantial hurdle. The cost of key materials used in packaging, such as paper pulp, petroleum-based plastics, and aluminum, is subject to fluctuations influenced by global supply and demand dynamics, geopolitical events, and energy prices. These price swings can significantly impact the profitability of packaging manufacturers and create uncertainty in long-term planning and pricing strategies.

The growing consumer and societal pressure for sustainability, while a driving force, also acts as a restraint if not managed effectively. While demand for eco-friendly options is high, the cost of implementing and scaling up sustainable packaging solutions can be prohibitive for some companies. The perception that sustainable packaging is more expensive or less effective can also deter adoption. Furthermore, the availability and scalability of advanced recycling infrastructure remain a bottleneck. Even with the best intentions for recyclable materials, if the infrastructure for collecting, sorting, and processing these materials is insufficient, the overall environmental benefit is diminished, leading to potential consumer skepticism and regulatory scrutiny.

Finally, the complexities of global supply chains and potential disruptions, exacerbated by events like pandemics or geopolitical conflicts, can impact the timely and cost-effective delivery of packaging materials and finished products. These disruptions can lead to material shortages, increased transportation costs, and delays, affecting the entire value chain. Addressing these challenges requires a strategic approach, balancing innovation with economic viability and regulatory compliance.

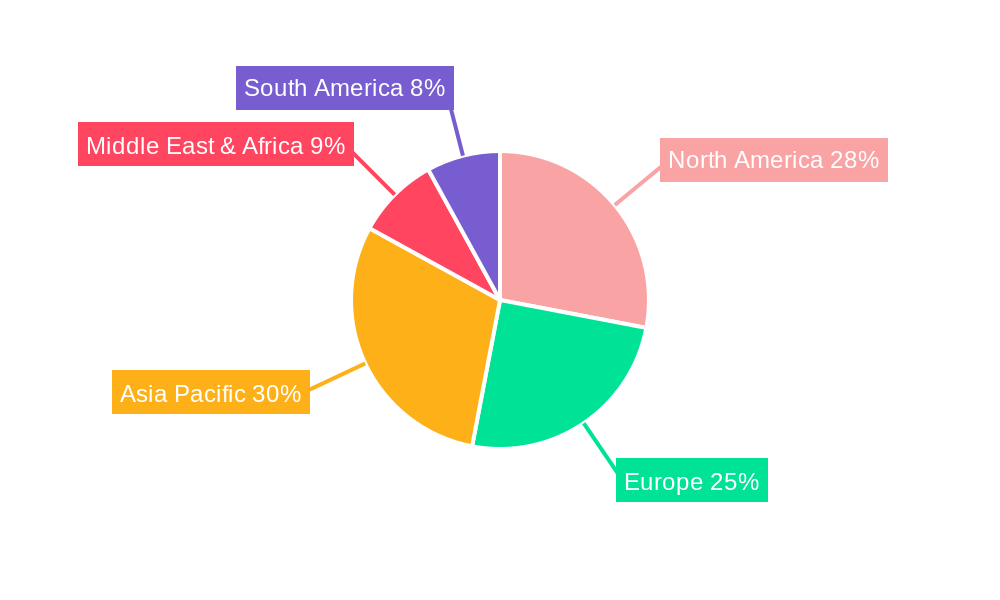

The global Food & Drink Packaging market is characterized by a diverse regional and segmental landscape, with several key players poised for dominance. Geographically, North America and Europe have historically been strongholds for the food and drink packaging industry, driven by high consumer spending, advanced technological adoption, and well-established manufacturing bases. However, the Asia-Pacific region is rapidly emerging as the most dominant force, propelled by its massive and growing population, rapid economic development, increasing disposable incomes, and a burgeoning middle class with a heightened demand for packaged food and beverages. Countries like China, India, and Southeast Asian nations are witnessing unprecedented growth in consumption, driving substantial investments in packaging infrastructure and innovation.

Within the Application segment, the Food application is expected to continue its dominance, accounting for the largest share of the market. This is attributed to the sheer volume and diversity of food products requiring packaging, including fresh produce, dairy, meat, poultry, seafood, bakery goods, confectionery, and ready-to-eat meals. The increasing demand for convenience foods, processed snacks, and value-added food items, particularly in emerging economies, further solidifies the food application's leading position. The Drink application also represents a significant and growing segment, encompassing beverages like carbonated soft drinks, juices, water, dairy drinks, alcoholic beverages, and hot drinks. The beverage industry's continuous product innovation, including the introduction of new flavors, functional drinks, and extended shelf-life options, fuels a consistent demand for diverse and specialized packaging solutions.

Examining the Type segment, Plastic packaging is projected to maintain its leading position throughout the forecast period. Its versatility, cost-effectiveness, excellent barrier properties, and lightweight nature make it an ideal choice for a wide array of food and drink applications, from flexible pouches and films to rigid containers and bottles. The ongoing advancements in plastic material science, including the development of biodegradable and recyclable plastics, are further strengthening its market presence. However, the Paper & Board segment is experiencing robust growth, driven by the escalating demand for sustainable packaging. Its recyclability, biodegradability, and renewable nature make it an attractive alternative for many applications, particularly in the food and beverage sectors. Rigid paperboard packaging, such as folding cartons and corrugated boxes, plays a crucial role in protecting and presenting a vast array of products. The Metal packaging segment, primarily aluminum and steel, remains vital for certain products like beverages (cans), preserved foods (cans), and aerosols, owing to its excellent barrier properties, recyclability, and durability. While facing competition from other materials, its established infrastructure and performance benefits ensure its continued significance. The Glass packaging segment, while facing pressure from lighter alternatives, retains its premium appeal for specific applications like premium beverages, sauces, and baby food, owing to its inertness, inertness, and perceived quality. Regions and countries with a strong focus on sustainable packaging initiatives and those experiencing rapid urbanization and income growth are expected to drive the dominance of specific segments.

Several key factors are acting as significant growth catalysts for the food and drink packaging industry. The persistent global demand for convenience, driven by busy lifestyles and urbanization, fuels the need for single-serving packs, easy-to-open formats, and ready-to-consume products. Furthermore, the burgeoning e-commerce sector for food and beverages necessitates specialized, protective, and appealing packaging to ensure safe and satisfactory delivery. Innovations in material science, leading to lighter, stronger, and more sustainable packaging options such as biodegradable plastics and enhanced paperboard solutions, are not only meeting regulatory demands but also appealing to environmentally conscious consumers. The increasing focus on health and wellness also encourages packaging that clearly communicates nutritional information and allergen details, driving demand for transparent and informative designs.

This report offers a holistic examination of the food and drink packaging market, providing a detailed analysis of market size, trends, and projections. It meticulously breaks down the market by packaging type (Paper & Board, Plastic, Glass, Metal) and application (Food, Drink), offering granular insights into segment-specific growth drivers and challenges. The report also investigates industry developments, including technological innovations, sustainability initiatives, and regulatory impacts, providing a forward-looking perspective. By analyzing the competitive landscape and identifying key players, stakeholders will gain a strategic advantage in understanding market dynamics and formulating effective business strategies within this vital and expanding sector. The comprehensive coverage ensures that businesses are well-equipped to navigate the complexities and capitalize on the opportunities present in the global food and drink packaging market.

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 5.4% from 2020-2034 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately 5.4%.

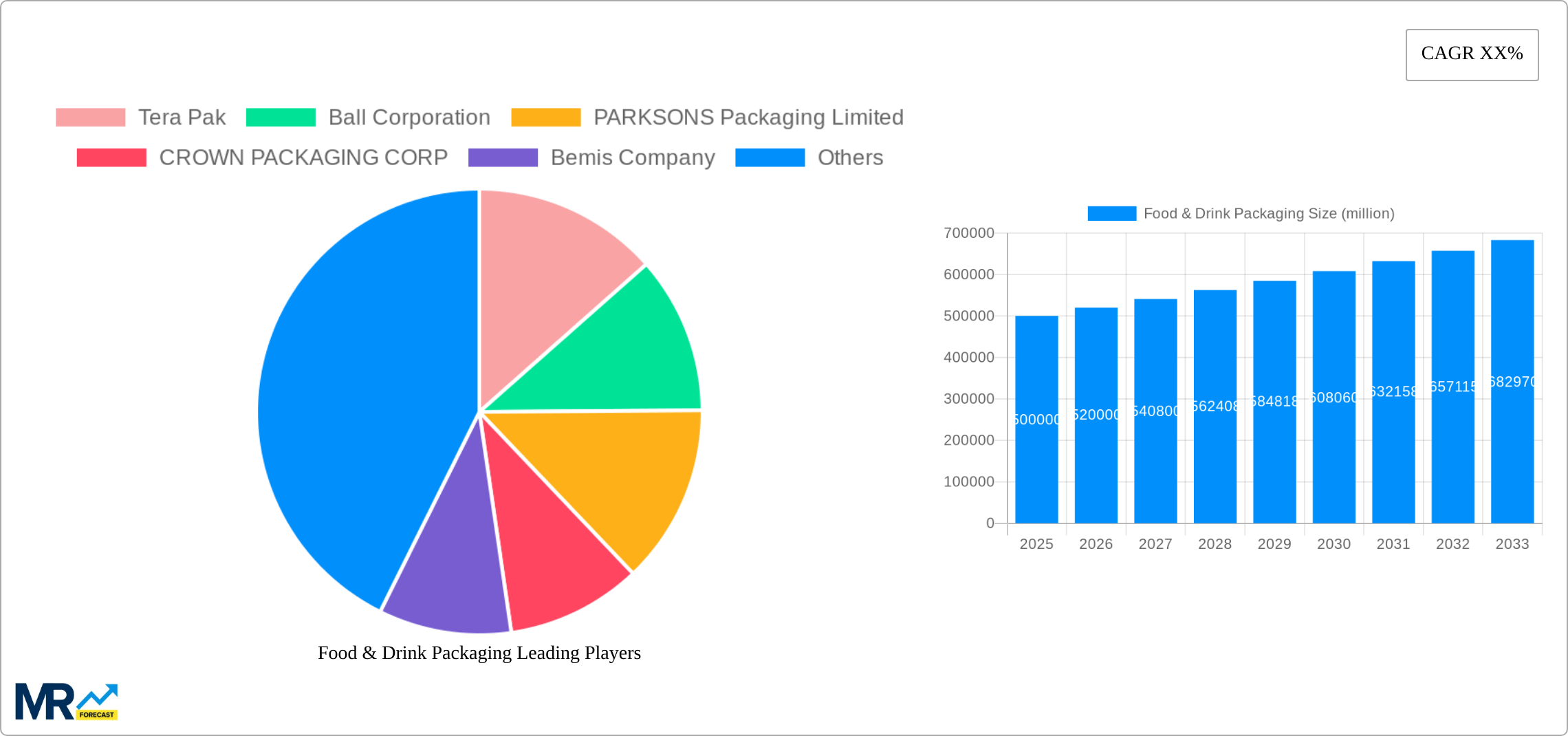

Key companies in the market include Tera Pak, Ball Corporation, PARKSONS Packaging Limited, CROWN PACKAGING CORP, Bemis Company, Amcor, Sealed Air Corporation, Sonoco Products Company, Ukrplastic, Wipak Group, Constantia Flexibles International GmbH, Flextrus AB, Huhtamaki, Mondi Group, WestRock.

The market segments include Type, Application.

The market size is estimated to be USD 421.38 billion as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4480.00, USD 6720.00, and USD 8960.00 respectively.

The market size is provided in terms of value, measured in billion.

Yes, the market keyword associated with the report is "Food & Drink Packaging," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Food & Drink Packaging, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.