1. What is the projected Compound Annual Growth Rate (CAGR) of the ESports Club?

The projected CAGR is approximately XX%.

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

ESports Club

ESports ClubESports Club by Type (/> League of Legends, Dota2, PUBG, CS:GO, Overwatch, Hearthstone, Others), by Application (/> Match Broadcast, AD Endorsement, Bonus, Others), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2025-2033

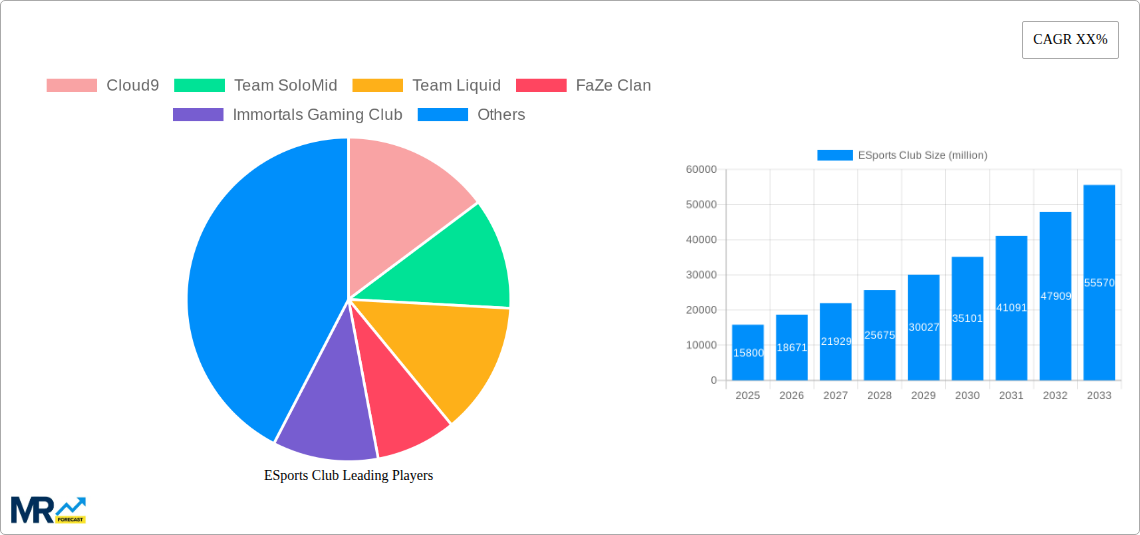

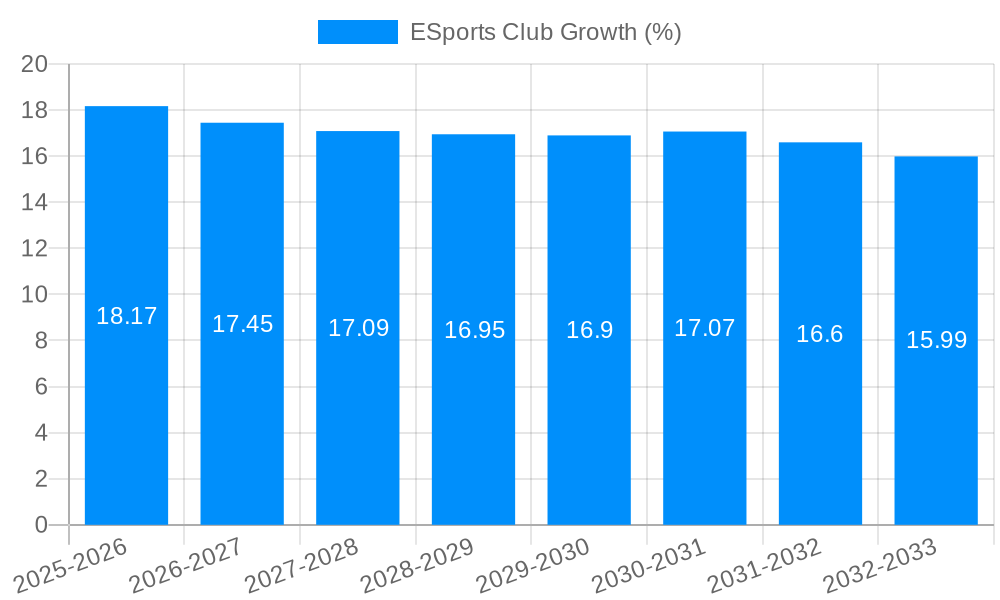

The global esports club market is experiencing robust expansion, projected to reach an estimated USD 15,800 million by 2025 with a Compound Annual Growth Rate (CAGR) of 18.5% throughout the forecast period of 2025-2033. This remarkable growth is fueled by a confluence of factors, including the escalating popularity of esports titles like League of Legends, Dota 2, and PUBG, which have cultivated massive global player bases and viewership. The increasing professionalization of esports, characterized by organized leagues, sophisticated tournament structures, and significant prize pools, is attracting substantial investment and sponsorships. Furthermore, advancements in streaming technology and the widespread accessibility of high-speed internet have made esports more engaging and convenient for a broader audience, further driving market penetration. The burgeoning esports ecosystem is also supported by dedicated fan bases who actively participate in viewing, discussing, and even investing in their favorite clubs and players, creating a self-sustaining growth cycle.

Key drivers propelling this market surge include substantial AD endorsements from major brands seeking to tap into the lucrative and engaged youth demographic, alongside increasing bonus payouts for top-tier teams and players. The market is segmented by popular game titles, with League of Legends, Dota 2, and PUBG leading the charge in terms of player engagement and viewership, contributing significantly to club revenue streams. Application segments such as match broadcasts and AD endorsements are becoming increasingly critical for monetization, attracting significant capital. Restrains such as the potential for game saturation and the need for continuous content innovation to retain audience interest are present, but are largely outweighed by the overwhelming growth potential. Regionally, the Asia Pacific, particularly China, and North America are expected to lead market expansion due to their mature esports infrastructure and fervent fan bases, though Europe and other emerging markets are also showing promising growth trajectories. The competitive landscape features prominent clubs like Cloud9, TSM, and FaZe Clan, actively vying for market share through talent acquisition, brand building, and strategic partnerships.

This comprehensive report delves into the dynamic and rapidly evolving global ESports Club industry, providing a robust analysis of market trends, driving forces, challenges, and future growth trajectories. Spanning a study period from 2019 to 2033, with a base and estimated year of 2025 and a forecast period of 2025-2033, this report leverages historical data from 2019-2024 to offer unparalleled insights. The market is projected to witness substantial expansion, driven by increasing viewership, professionalization, and diverse revenue streams.

The global ESports Club market is experiencing a paradigm shift, evolving from a niche hobby into a multi-billion dollar industry. XXX, the key market insight, is the accelerating professionalization and mainstream adoption of competitive gaming. This is evidenced by the exponential growth in viewership figures, with major tournaments attracting audiences that rival traditional sporting events. The study period highlights a transformative journey for ESports Clubs, with revenues escalating from hundreds of millions in the historical period to projected billions within the forecast period. This surge is fueled by a widening fan base, particularly among younger demographics, who are increasingly engaging with ESports content across various digital platforms. The integration of ESports into mainstream media, with dedicated channels and broadcast deals, further amplifies its reach and commercial viability. Strategic partnerships between ESports organizations and established brands across diverse sectors, from technology and apparel to beverages and automotive, underscore the growing attractiveness of this sector for advertisers and sponsors. The report meticulously examines the market's segmentation by game titles, revealing the dominance of established giants like League of Legends and CS:GO, alongside the rising prominence of newer titles like PUBG and Overwatch. Furthermore, the analysis of revenue streams, including match broadcasts, AD endorsements, and direct player earnings, demonstrates a mature and diversified monetization landscape. The continuous influx of investment from venture capitalists and traditional sports franchises indicates a strong belief in the long-term sustainability and profitability of the ESports Club ecosystem. The study period's data reveals a significant upward trend in player salaries and prize pools, reflecting the increasing financial stakes and the commitment to developing top-tier professional talent. Looking ahead, the forecast period anticipates further innovation in content creation, immersive fan experiences through virtual and augmented reality, and the continued expansion of the global ESports calendar. The report also scrutinizes the impact of technological advancements, such as improved streaming technology and data analytics, on enhancing player performance and fan engagement. Overall, the ESports Club market is characterized by its dynamic nature, continuous innovation, and a compelling growth narrative, poised to redefine the entertainment and sports industries in the coming years.

The explosive growth of the ESports Club industry is propelled by a confluence of powerful driving forces, collectively reshaping the entertainment landscape. The primary catalyst is the ever-increasing global viewership and fan engagement. As digital connectivity expands and younger generations increasingly embrace online content, ESports tournaments are drawing hundreds of millions of viewers worldwide, often surpassing traditional sporting events in terms of online reach. This massive audience base presents an unparalleled opportunity for advertisers and sponsors seeking to connect with a highly engaged and digitally native demographic. Furthermore, the professionalization of the industry has been a critical factor. The establishment of well-structured leagues, organized training facilities, substantial prize pools, and lucrative player contracts has transformed ESports from a casual pursuit into a viable and attractive career path for aspiring athletes. This professional environment attracts significant investment and talent, further elevating the quality of competition and the overall spectacle. The proliferation of streaming platforms and digital content creation has democratized access to ESports, allowing fans to follow their favorite teams and players seamlessly. Platforms like Twitch and YouTube have become central hubs for ESports content, fostering vibrant communities and enabling direct interaction between players and their fan bases. This accessibility, coupled with the inherent excitement and strategic depth of competitive gaming, creates a virtuous cycle of engagement and growth.

Despite its meteoric rise, the ESports Club industry faces a distinct set of challenges and restraints that could temper its trajectory. A significant hurdle is the perceived lack of mainstream recognition and legitimacy compared to traditional sports. While viewership is high, broader societal acceptance as a legitimate sport is still developing, which can impact sponsorship acquisition and talent development pipelines. The highly competitive and volatile nature of game popularity also presents a challenge. ESports clubs are heavily reliant on specific game titles, and a decline in the popularity of a flagship game can severely impact a club's viewership, player base, and revenue. This necessitates constant adaptation and diversification across multiple titles. Player burnout and mental health concerns are increasingly being recognized as critical issues. The intense training schedules, high-pressure environments, and the fleeting nature of peak performance can take a toll on professional players, requiring robust support systems and welfare programs, which are still maturing within the industry. Furthermore, regulatory and governance complexities are emerging. As the industry grows, the need for standardized regulations, anti-cheating measures, and player welfare standards becomes paramount. The absence of a unified global governing body similar to FIFA or the NBA can lead to fragmentation and inconsistencies. Finally, monetization challenges beyond sponsorships and broadcast rights persist. While AD endorsements and match broadcasts are significant revenue streams, diversifying income through merchandise, ticketing, and other avenues remains a work in progress for many clubs, particularly those outside the top tier.

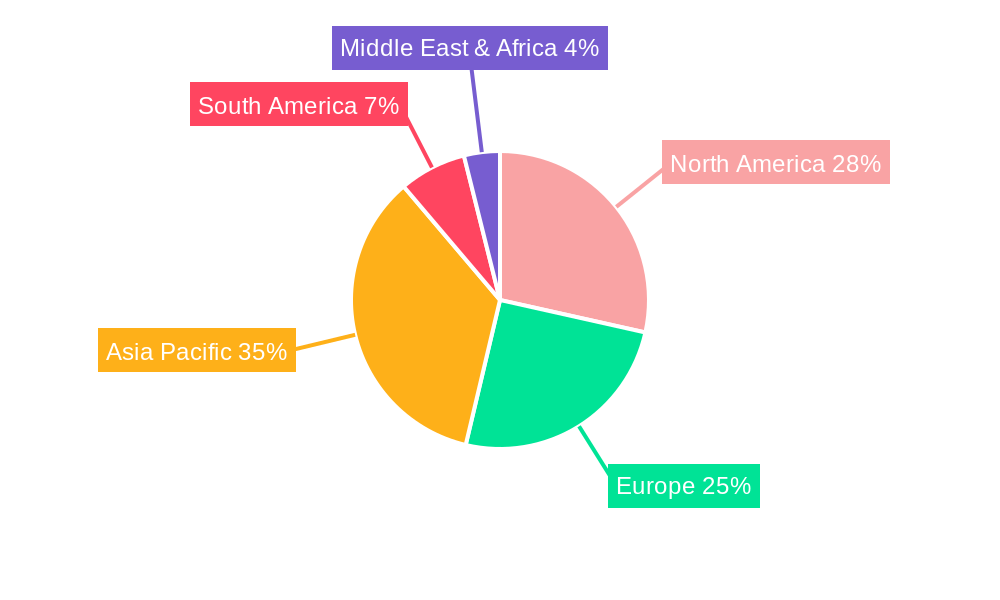

The global ESports Club market is characterized by regional dominance and segment specific growth. In terms of key regions, Asia-Pacific is poised to continue its reign as the dominant market throughout the study period, driven by its massive internet-savvy population and a deeply ingrained gaming culture. Countries like China and South Korea are not only pioneers in the ESports landscape but also represent the largest consumer bases for gaming and competitive play. China, in particular, boasts an enormous market size for video games and ESports, with significant government support and a vast number of professional clubs and leagues. South Korea has a long-standing history of professional gaming, having nurtured some of the earliest ESports stars and organized leagues. Southeast Asia is also emerging as a significant growth engine within the region, with countries like Indonesia, Vietnam, and Thailand experiencing rapid increases in ESports adoption and viewership.

Within the segmentation by game type, League of Legends is projected to remain a colossal force, consistently driving substantial viewership and revenue. Its established professional ecosystem, global appeal, and regular updates ensure its enduring popularity. Alongside League of Legends, Dota 2 will also maintain its strong presence, particularly in regions with a passionate player base and a history of significant tournament prize pools. The tactical depth and strategic complexity of Dota 2 continue to captivate a dedicated audience.

The CS:GO (Counter-Strike: Global Offensive) segment is expected to continue its strong performance, benefiting from its evergreen competitive nature and a robust community that has supported the franchise for decades. Its accessibility across a wide range of PC hardware further contributes to its widespread appeal.

Emerging and growing segments include PUBG (PlayerUnknown's Battlegrounds) and Overwatch. PUBG has seen significant traction, particularly in Asian markets, and its battle royale format resonates with a broad audience. Overwatch, while facing some fluctuations, maintains a dedicated following and offers a unique team-based shooter experience that appeals to competitive players.

The Application segment, specifically Match Broadcast and AD Endorsement, will continue to be the primary revenue drivers. The increasing number of professional matches being broadcast across various platforms, coupled with the high engagement rates of ESports audiences, makes them highly attractive for advertisers. AD endorsements from global brands are expected to escalate significantly, as companies recognize the marketing potential of reaching millions of digitally connected consumers.

Several key growth catalysts are propelling the ESports Club industry forward. The increasing accessibility of gaming hardware and high-speed internet globally allows a wider demographic to participate and consume ESports content. The growing acceptance and integration of ESports into mainstream culture, with media coverage and celebrity endorsements, are broadening its appeal beyond traditional gaming communities. Furthermore, significant investment from venture capitalists, traditional sports organizations, and major corporations is providing the financial fuel for team infrastructure, player development, and marketing initiatives. The continuous innovation in game development and platform technology, leading to more engaging and visually appealing ESports titles and enhanced streaming experiences, also plays a crucial role.

This report provides an exhaustive analysis of the ESports Club industry, meticulously covering market dynamics, growth drivers, potential impediments, and future projections. It meticulously examines key segments like League of Legends, Dota 2, CS:GO, and emerging titles, alongside crucial application areas such as match broadcasts and AD endorsements. With a detailed historical overview from 2019-2024 and a comprehensive forecast extending to 2033, the report offers strategic insights for stakeholders, investors, and industry participants. The emphasis on regional dominance, particularly the Asia-Pacific market, and the identification of leading players and significant developments ensure a holistic understanding of the ESports Club ecosystem.

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of XX% from 2019-2033 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately XX%.

Key companies in the market include Cloud9, Team SoloMid, Team Liquid, FaZe Clan, Immortals Gaming Club, Gen.G, Fnatic, Envy Gaming, G2 Esports, 100 Thieves, NRG Esports, Misfits Gaming, OverActive Media.

The market segments include Type, Application.

The market size is estimated to be USD XXX million as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4480.00, USD 6720.00, and USD 8960.00 respectively.

The market size is provided in terms of value, measured in million.

Yes, the market keyword associated with the report is "ESports Club," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the ESports Club, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.