1. What is the projected Compound Annual Growth Rate (CAGR) of the Electronic Warfare Systems?

The projected CAGR is approximately 4.1%.

Electronic Warfare Systems

Electronic Warfare SystemsElectronic Warfare Systems by Type (Electronic Support, Electronic Attack, Electronic Protection), by Application (Airborne, Naval, Land), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2026-2034

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

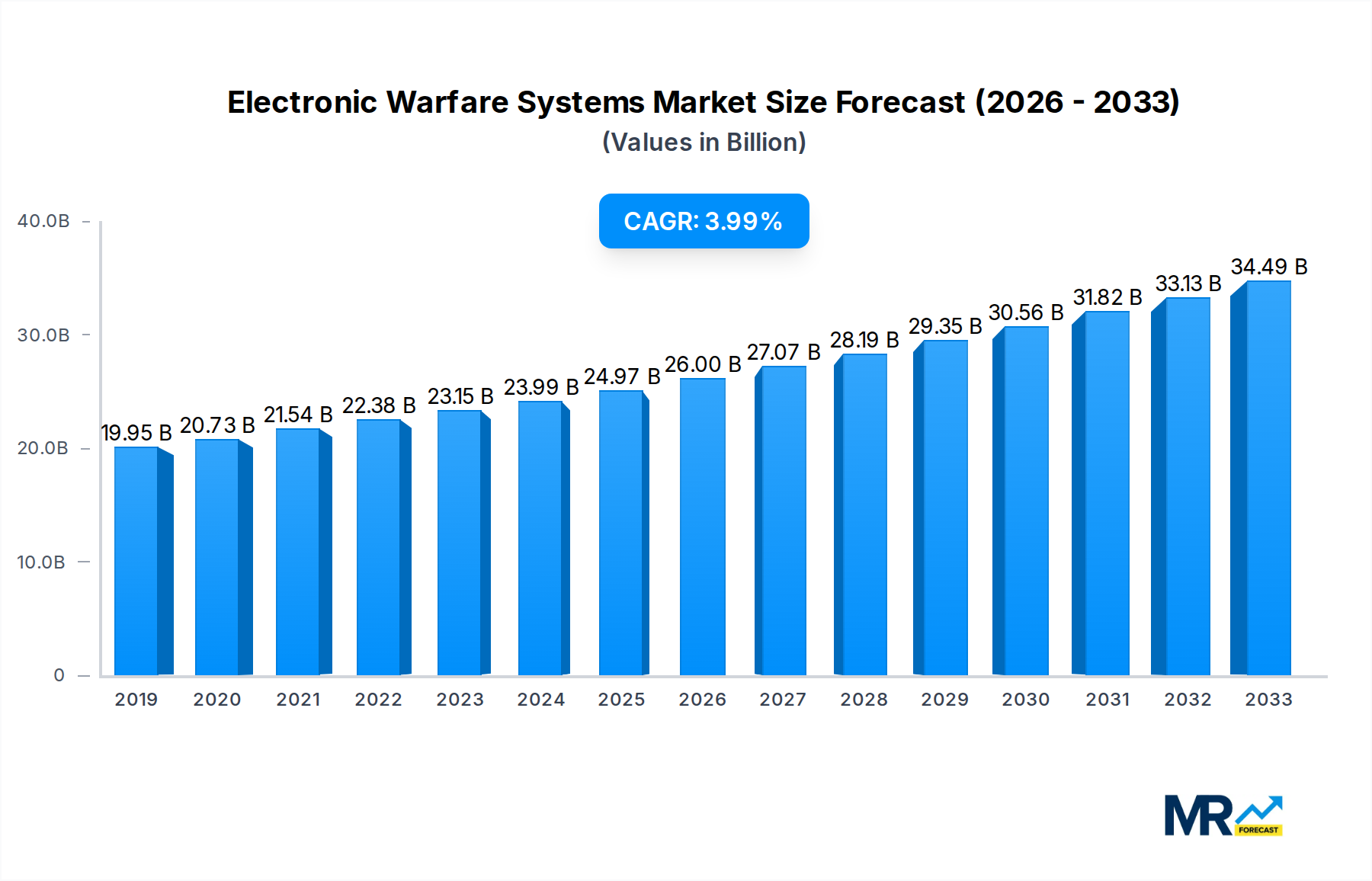

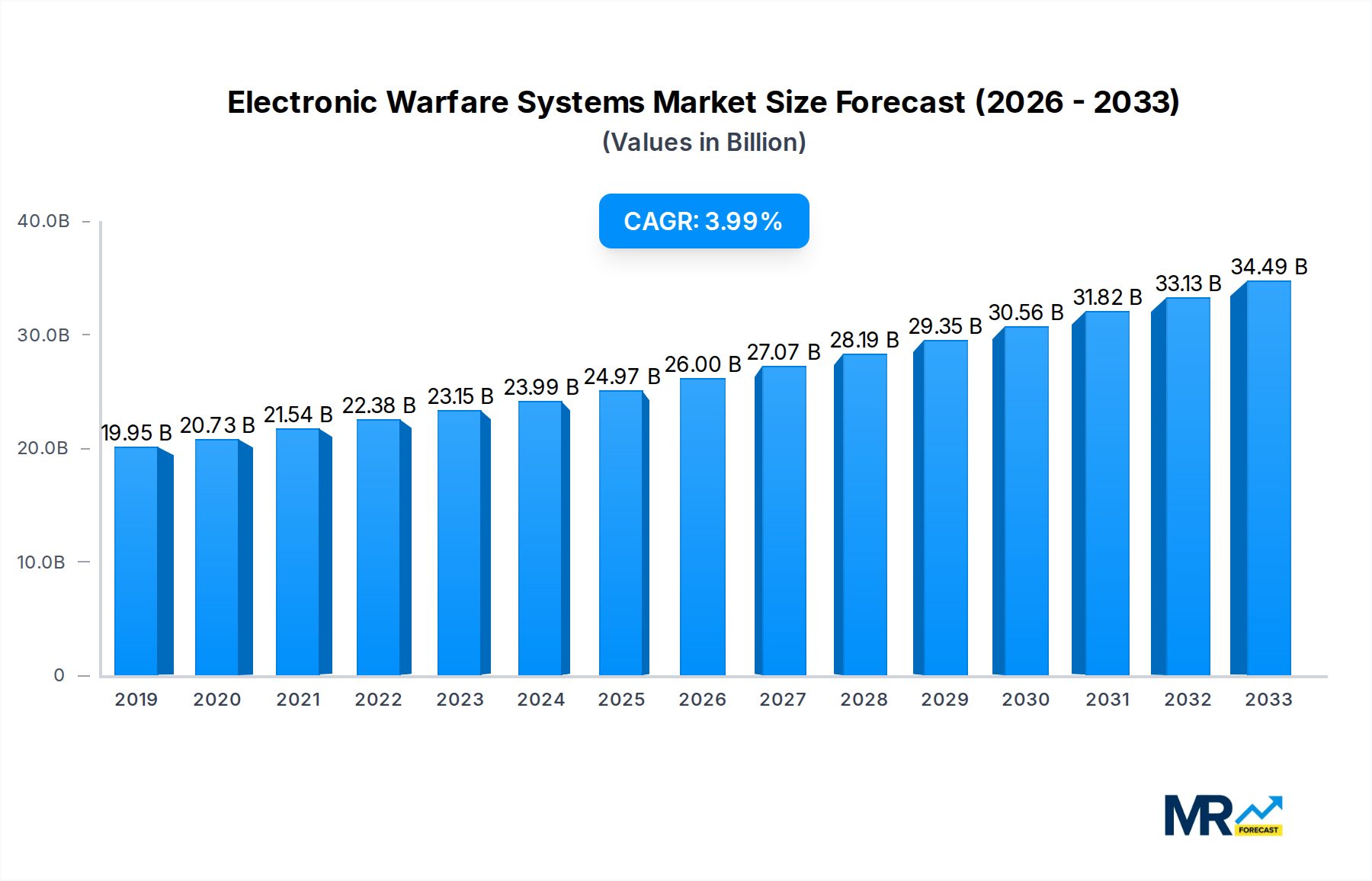

The global Electronic Warfare (EW) Systems market is poised for substantial growth, projected to reach an estimated USD 23,990 million by 2025, expanding at a Compound Annual Growth Rate (CAGR) of 4.1% through 2033. This robust expansion is fueled by escalating geopolitical tensions and the increasing reliance on advanced technologies for national security and defense across airborne, naval, and land applications. The market encompasses critical segments such as Electronic Support, Electronic Attack, and Electronic Protection, each playing a vital role in modern warfare capabilities. Key growth drivers include the continuous need for superior situational awareness, effective countermeasures against evolving threats, and the integration of artificial intelligence and machine learning into EW platforms. Nations worldwide are investing heavily in modernizing their defense infrastructure, recognizing EW systems as indispensable for maintaining a strategic advantage in contested environments.

The evolving landscape of warfare, characterized by sophisticated cyber threats and the proliferation of advanced sensor and communication technologies, underscores the indispensable nature of Electronic Warfare Systems. Major defense contractors like BAE Systems, Northrop Grumman, Raytheon, and Lockheed Martin are at the forefront of innovation, developing next-generation EW solutions. Trends such as the miniaturization of EW components, the development of directed energy weapons, and the increasing adoption of software-defined EW architectures are shaping market dynamics. While the market benefits from strong government funding and a constant demand for technological superiority, potential restraints include the high cost of research and development, complex regulatory frameworks, and the lengthy procurement cycles within defense industries. However, the strategic imperative to counter advanced threats and ensure battlefield dominance is expected to sustain the market's upward trajectory, with significant opportunities arising in emerging markets and for innovative, adaptable EW solutions.

Here's a unique report description on Electronic Warfare Systems, incorporating your specified elements:

This comprehensive report delves into the dynamic and rapidly evolving global Electronic Warfare (EW) Systems market. The Study Period spans from 2019 to 2033, with the Base Year and Estimated Year both set as 2025. The Forecast Period extends from 2025 to 2033, building upon the Historical Period of 2019-2024. We project the global EW systems market to reach a valuation of over $20 million by the end of the forecast period, reflecting sustained growth driven by geopolitical imperatives and technological advancements.

XXX The global Electronic Warfare (EW) Systems market is experiencing a significant surge, driven by an increasing recognition of its critical role in modern defense strategies and the escalating complexity of electromagnetic spectrum operations. Key market insights reveal a pronounced shift towards integrated EW solutions that offer a synergistic combination of Electronic Support (ES), Electronic Attack (EA), and Electronic Protection (EP) capabilities. This integration is paramount as adversaries are increasingly employing sophisticated jamming, spoofing, and cyber-warfare techniques, necessitating equally advanced countermeasures. The demand for airborne EW platforms, particularly unmanned aerial vehicles (UAVs) equipped with EW suites, is on a steep upward trajectory, driven by their agility, persistent presence, and ability to operate in high-threat environments. Naval EW systems are also witnessing substantial investment, with a focus on enhancing vessel survivability against sophisticated anti-ship missile threats and the need for effective electronic intelligence gathering in contested maritime domains. The land segment, while traditionally less focused on EW, is now seeing increased adoption for battlefield situational awareness, electronic intelligence, and protection against directed energy threats. Emerging technologies such as artificial intelligence (AI) and machine learning (ML) are being rapidly integrated into EW systems to enable faster threat detection, adaptive jamming, and automated decision-making, allowing forces to operate more effectively in the congested and contested electromagnetic spectrum. Furthermore, the increasing digitization of military operations and the rise of fifth and sixth-generation fighter aircraft, which rely heavily on the electromagnetic spectrum for communication, navigation, and targeting, are creating new frontiers and demands for advanced EW capabilities. The market is also characterized by a growing emphasis on directed energy weapons and cyber-EW convergence, blurring the lines between traditional EW and cyber warfare. This comprehensive approach to EW is no longer a niche requirement but a fundamental pillar of modern military effectiveness, driving innovation and market expansion across all segments.

The global Electronic Warfare (EW) Systems market is being propelled by a confluence of powerful driving forces. Foremost among these is the escalating geopolitical instability and the resurgence of great power competition. Nations are increasingly investing in advanced EW capabilities to maintain a decisive edge in the electromagnetic spectrum, which is now recognized as a critical battleground. The proliferation of advanced adversaries' electronic warfare technologies, including sophisticated jamming and anti-access/area denial (A2/AD) systems, is compelling military forces worldwide to upgrade their own EW arsenals. Furthermore, the rapid pace of technological innovation, particularly in areas like artificial intelligence, machine learning, software-defined radio (SDR), and directed energy, is enabling the development of more potent and adaptable EW systems. The increasing reliance of modern military platforms on the electromagnetic spectrum for communication, navigation, and targeting makes them inherently vulnerable to EW threats, thus necessitating robust protection and offensive capabilities. The rise of unmanned systems, both autonomous and remotely piloted, is also a significant driver, as these platforms are ideal for EW operations due to their expendability, persistence, and ability to operate in high-risk environments. Growing defense budgets in key regions, coupled with a focus on modernizing legacy military hardware with advanced EW functionalities, further fuels market expansion. The need for enhanced intelligence, surveillance, and reconnaissance (ISR) capabilities, with EW playing a crucial role in gathering electronic intelligence (ELINT) and signals intelligence (SIGINT), also contributes to market growth.

Despite the robust growth trajectory, the Electronic Warfare (EW) Systems market faces several significant challenges and restraints. The sheer complexity and rapidly evolving nature of EW technology necessitate continuous and substantial investment in research and development, which can be a significant hurdle for some nations and smaller defense contractors. The integration of new EW systems with existing legacy platforms often proves to be an intricate and costly process, requiring extensive testing and validation to ensure interoperability and prevent unintended consequences. The escalating costs associated with developing and procuring advanced EW systems can strain defense budgets, potentially leading to prioritization challenges and delays in deployment. Furthermore, the dual-use nature of certain EW technologies raises concerns regarding their potential proliferation to non-state actors or adversary nations, leading to stringent export controls and licensing requirements that can slow down international market penetration. The talent gap in specialized fields such as signal processing, artificial intelligence, and cyber security is another considerable restraint, as acquiring and retaining skilled personnel to design, develop, and operate sophisticated EW systems is becoming increasingly difficult. The evolving threat landscape, characterized by the rapid development of new jamming techniques and counter-EW measures by adversaries, requires constant adaptation and innovation, making it challenging for EW system developers to stay ahead of the curve. Finally, the electromagnetic spectrum itself is becoming increasingly congested and contested, with civilian and military users competing for bandwidth, which can complicate EW operations and necessitate more sophisticated spectrum management techniques.

The Airborne segment is poised to dominate the global Electronic Warfare (EW) Systems market throughout the forecast period. This dominance stems from several interconnected factors that underscore the indispensable nature of airborne EW in contemporary military operations.

Strategic Importance of Air Superiority and ISR: Achieving and maintaining air superiority is a foundational element of modern warfare. Airborne EW platforms, ranging from dedicated EW aircraft to integrated systems on fighter jets and unmanned aerial vehicles (UAVs), are critical for achieving this. They provide essential capabilities for Electronic Support (ES), enabling the detection, identification, and geolocation of enemy radar and communication signals, thereby enhancing situational awareness. Furthermore, Electronic Attack (EA) capabilities from airborne platforms can effectively neutralize enemy air defense systems and communication networks, paving the way for friendly air operations. The persistent Intelligence, Surveillance, and Reconnaissance (ISR) provided by airborne EW assets is unparalleled, offering real-time intelligence critical for dynamic battlefield decision-making.

Technological Advancement and Platform Integration: The airborne segment is at the forefront of technological innovation in EW. The development of sophisticated EW suites for next-generation fighter aircraft (e.g., F-35, Eurofighter Typhoon) and the increasing integration of EW capabilities into UAVs are significant market drivers. These platforms are designed from the ground up with EW in mind, allowing for more streamlined integration of advanced technologies such as AI-powered threat analysis, advanced jamming techniques, and robust Electronic Protection (EP) measures. The miniaturization of EW components also allows for their integration into a wider array of airborne platforms, from tactical fighters to strategic bombers and reconnaissance drones.

Threat Landscape and Operational Requirements: The modern battlefield is characterized by sophisticated and layered air defense systems and evolving electronic threats. Airborne EW is essential for penetrating these defenses, protecting friendly aircraft from missile threats, and disrupting enemy communications. The demand for EW capabilities that can operate effectively in contested electromagnetic environments, such as those encountered in potential conflicts involving peer or near-peer adversaries, directly fuels the growth of the airborne segment. The ability of airborne platforms to project EW power over vast distances and provide persistent electronic jamming or deception is a critical operational requirement.

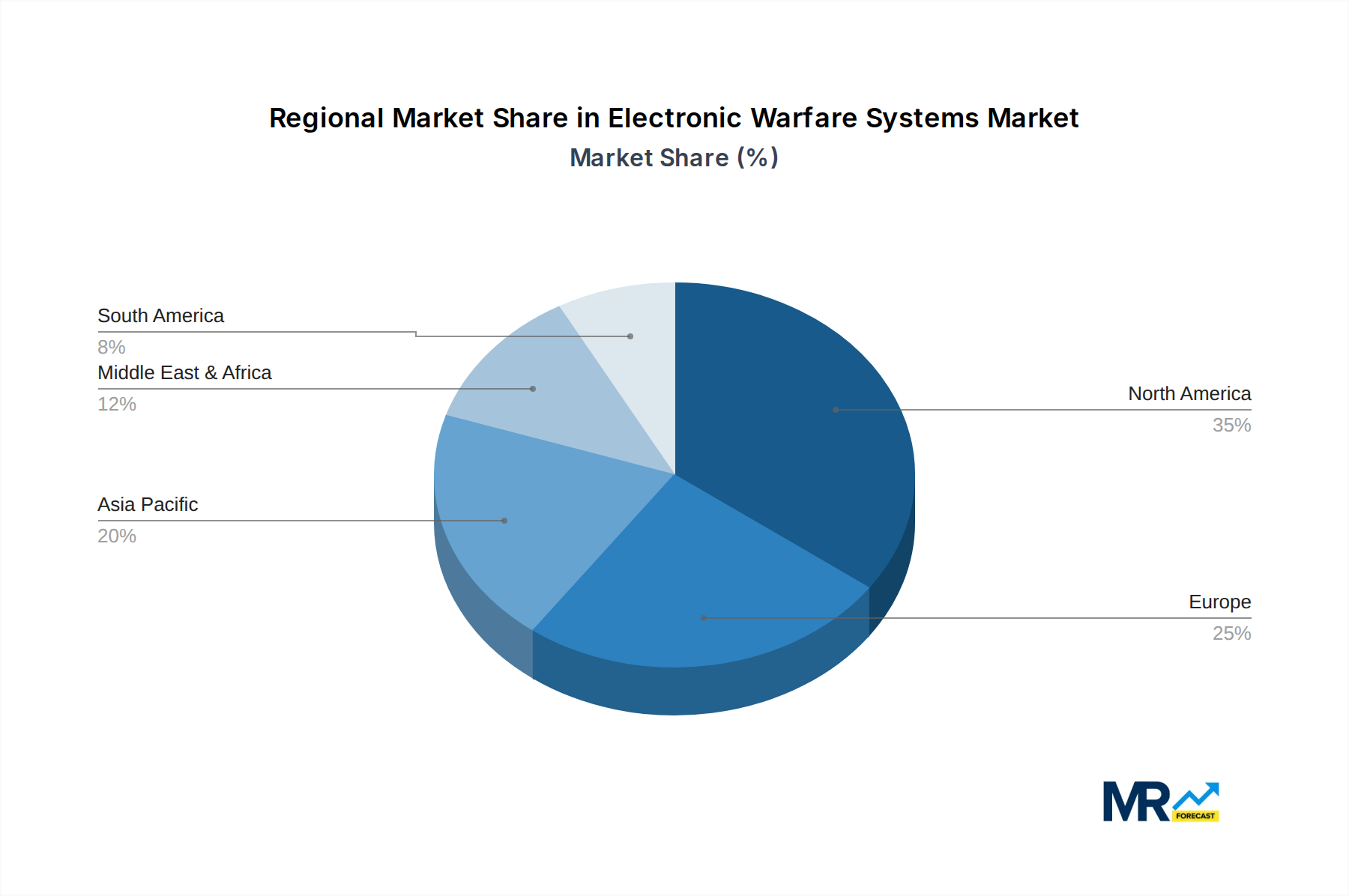

North America and Europe as Key Markets: Geographically, North America, led by the United States, and Europe are anticipated to be the dominant regions in the airborne EW market. This is due to the substantial defense spending in these regions, the presence of leading EW system manufacturers (e.g., Northrop Grumman, BAE Systems, Raytheon, Lockheed Martin), and the continuous modernization programs undertaken by their respective armed forces. These regions are actively investing in advanced airborne EW technologies to counter emerging threats and maintain their technological superiority. The ongoing conflicts and heightened geopolitical tensions globally also necessitate robust airborne EW capabilities, further solidifying the dominance of this segment and these regions in the EW market.

Several factors are acting as significant growth catalysts for the Electronic Warfare (EW) Systems industry. The escalating geopolitical tensions and the increasing threat perception from near-peer adversaries are compelling nations to bolster their EW capabilities, leading to increased defense spending in this sector. The rapid advancements in artificial intelligence (AI) and machine learning (ML) are enabling the development of more intelligent, adaptive, and autonomous EW systems capable of real-time threat identification and response. The burgeoning drone market, both military and civilian, presents a dual-edged sword, necessitating robust counter-drone EW solutions while also opening avenues for EW payloads on friendly drones. Furthermore, the digital transformation within militaries, emphasizing networked warfare and reliance on the electromagnetic spectrum, makes EW an indispensable component for maintaining operational effectiveness.

This report provides an exhaustive analysis of the global Electronic Warfare (EW) Systems market, offering a holistic view of its current landscape and future trajectory. It encompasses detailed market segmentation by type (Electronic Support, Electronic Attack, Electronic Protection), application (Airborne, Naval, Land), and region. The analysis includes in-depth insights into historical trends, current market dynamics, and robust forecasts up to 2033, with a base year of 2025. It identifies and elaborates on the key driving forces, challenges, and growth catalysts shaping the industry. Furthermore, the report presents a comprehensive overview of leading market players, significant technological developments, and strategic initiatives undertaken by key companies. This extensive coverage ensures that stakeholders gain a thorough understanding of the EW market's complexities, opportunities, and the strategic imperatives for success in this critical defense domain.

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 4.1% from 2020-2034 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately 4.1%.

Key companies in the market include BAE Systems, Thales Group, Northrop Grumman, Raytheon, Lockheed Martin, Leonardo, General Dynamics, Elbit Systems, L3Harris Technologies, Cobham, Mercury Systems, Saab, Hensoldt.

The market segments include Type, Application.

The market size is estimated to be USD 23990 million as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3480.00, USD 5220.00, and USD 6960.00 respectively.

The market size is provided in terms of value, measured in million.

Yes, the market keyword associated with the report is "Electronic Warfare Systems," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Electronic Warfare Systems, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.