1. What is the projected Compound Annual Growth Rate (CAGR) of the Electronic Home Video?

The projected CAGR is approximately 8%.

Electronic Home Video

Electronic Home VideoElectronic Home Video by Application (Family, Public, Others), by Type (Subscription-based, Time-based), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2026-2034

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

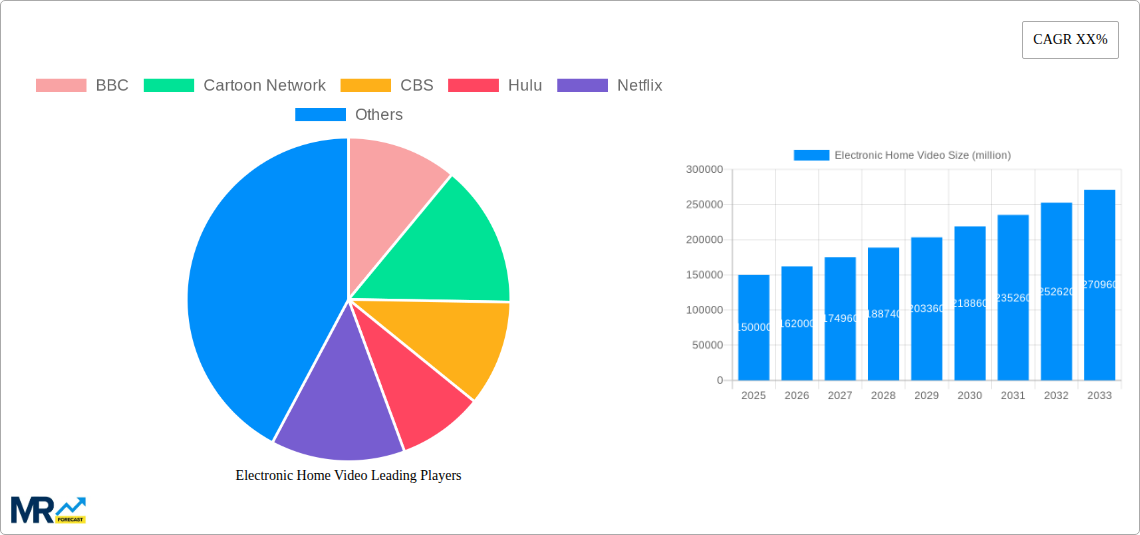

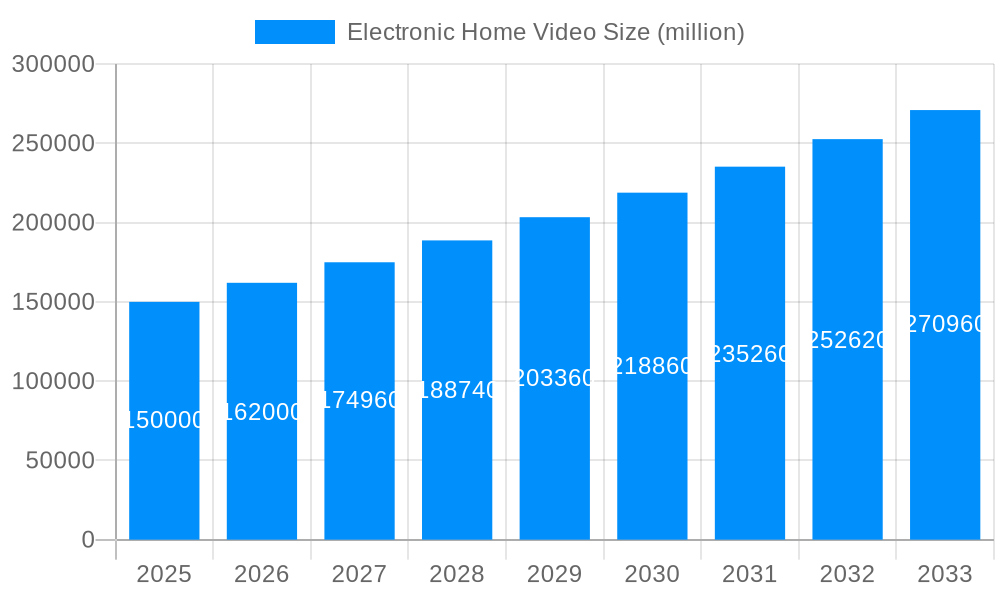

The global Electronic Home Video market is projected to reach $250 billion by 2025, exhibiting a Compound Annual Growth Rate (CAGR) of 8% from 2019 to 2025. This expansion is propelled by rising disposable incomes, increased internet penetration, and the widespread adoption of streaming services. Demand for high-quality video content across subscription-based platforms and traditional rental/purchase models fuels this growth. The proliferation of smart TVs and connected devices enhances content accessibility. Subscription-based services represent the dominant segment, expected to command approximately 70% of the market value by 2025, as consumers increasingly transition from traditional cable. The family segment leads in application, driven by the popularity of family-oriented content and dedicated streaming platforms.

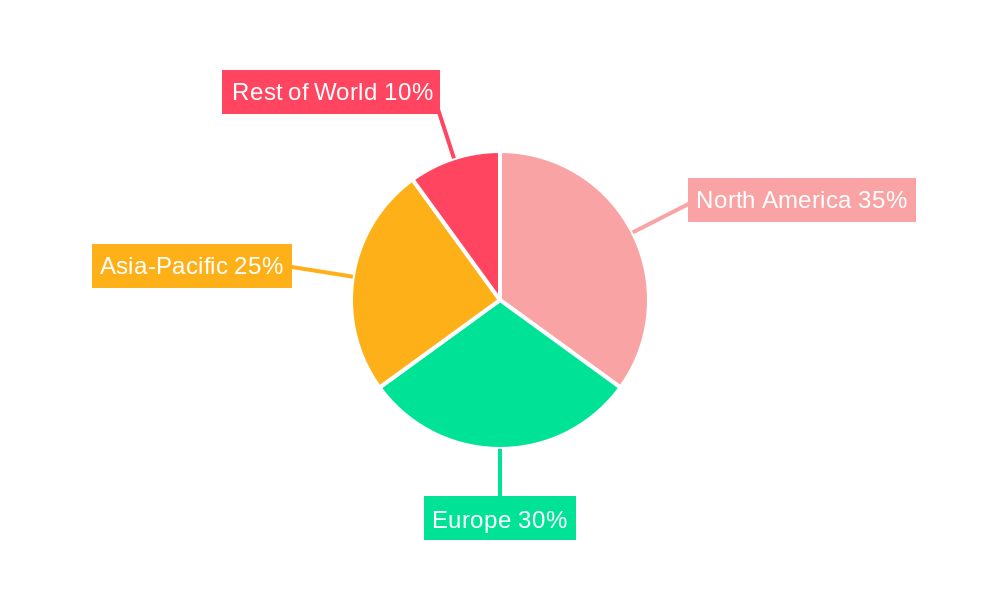

Geographic expansion is a significant growth catalyst. While North America currently dominates due to high internet penetration and streaming service preference, the Asia-Pacific region, particularly India and China, is poised for substantial growth with improving internet connectivity and purchasing power. Market challenges include data security and privacy concerns, intense competition among service providers, and the risk of piracy. Industry leaders are addressing these issues through enhanced security measures, diverse content libraries, and technological innovations to foster user loyalty and combat piracy. Major players like Netflix, Amazon, and Disney+ are prioritizing original content development and technological advancements to sustain market leadership. The market is anticipated to maintain its upward trend, supported by technological evolution, shifting consumer preferences, and expanding reach in emerging markets.

The electronic home video market, encompassing streaming services, smart TVs, and associated hardware, experienced significant growth from 2019 to 2024, driven primarily by increasing internet penetration, affordable devices, and the rise of on-demand content. The market's value surpassed 100 million units in 2024, reflecting a substantial increase over the previous years. The shift towards streaming services like Netflix and Hulu, fueled by their vast content libraries and convenient accessibility, has fundamentally altered how consumers engage with video entertainment. This trend has been further accelerated by the integration of smart technologies into televisions, allowing for seamless streaming and personalized viewing experiences. While subscription-based services dominate, time-based models still maintain a niche, particularly for specific events or niche content. Furthermore, the market is segmented across diverse applications: family entertainment, public viewing settings (like bars and restaurants), and others, encompassing corporate use or specialized applications. The historical period (2019-2024) shows an upward trajectory, while the forecast period (2025-2033) projects continued expansion, albeit potentially at a moderated rate due to market saturation in certain segments. The estimated market value for 2025 is projected to be significantly higher than 2024, further demonstrating the enduring appeal of home video entertainment. Competition amongst providers, however, is intense, leading to constant innovation in content, technology, and pricing strategies to maintain market share. The convergence of gaming, streaming, and social media platforms is shaping the future of home video, creating a dynamic and ever-evolving landscape.

Several key factors are driving the growth of the electronic home video market. The widespread adoption of high-speed internet, particularly broadband and fiber optic connections, is fundamental, allowing for seamless streaming of high-definition and 4K content. The affordability of smart TVs and streaming devices has democratized access to this technology, extending its reach beyond affluent consumers. The ever-expanding content libraries offered by streaming services, including original programming, exclusive releases, and vast catalogs of movies and TV shows, have made them increasingly attractive alternatives to traditional cable television. Furthermore, the convenience factor of on-demand viewing, personalized recommendations, and the ability to watch content across multiple devices is a major draw. Technological advancements, such as improved picture quality (HDR, 8K), immersive audio (Dolby Atmos), and AI-powered features, enhance the viewing experience, thereby boosting demand. The rising popularity of over-the-top (OTT) platforms further fuels this growth as they provide consumers with more flexible and affordable options. Finally, the increasing integration of streaming services into other smart home devices strengthens the overall ecosystem.

Despite its strong growth trajectory, the electronic home video market faces several challenges. The intense competition among streaming platforms necessitates continuous investment in content creation and technological innovation to maintain a competitive edge. Price sensitivity remains a significant factor, with consumers increasingly evaluating the value proposition of different subscription services. Piracy continues to pose a threat, undermining the revenue streams of content creators and distributors. The digital divide, characterized by unequal access to high-speed internet, limits market penetration in certain regions and demographics. Furthermore, concerns about data privacy and security associated with streaming services need to be addressed to maintain consumer trust. The increasing prevalence of ad-supported tiers on streaming platforms could negatively impact the user experience and subscription revenue. Regulatory changes and evolving copyright laws also pose potential hurdles for the industry. Lastly, managing the increasing amount of data generated by streaming activity requires robust infrastructure and efficient data management solutions.

The North American and Western European markets are currently leading the global electronic home video market, driven by high internet penetration, disposable incomes, and early adoption of new technologies. However, significant growth is projected in developing economies in Asia and Latin America as internet access expands and disposable incomes rise.

Dominant Segment: Subscription-based Services: This segment holds the largest market share due to the convenience, vast content libraries, and relatively predictable revenue streams. The subscription model allows for consistent revenue generation and enables providers to invest in high-quality content. The ease of access and multiple device support are further contributing factors to the dominance of this segment. Netflix, Hulu, and other major players have firmly established their presence in this space, leading to increased market competition and innovation. The ease of switching between services, however, requires providers to constantly curate appealing content and innovate to retain users.

Dominant Application: Family: This segment is substantial, reflecting the increasing importance of home entertainment for families. Family-friendly content, including children's programming, and the ability to share viewing experiences are crucial factors in this segment's dominance. This segment drives a significant portion of market demand, leading to more family-focused offerings and parental control features from providers and manufacturers.

Geographic Dominance: North America remains the dominant region, characterized by high internet penetration, widespread adoption of smart TVs, and a preference for on-demand entertainment. The substantial number of subscribers to subscription-based services in North America further solidifies its position as a leading market. However, the Asia-Pacific region is rapidly emerging as a key growth driver due to increasing internet adoption, rising disposable incomes, and a younger demographic with high engagement with digital media.

The dominance of these segments reflects the broader trends in consumer behavior, technology adoption, and the ongoing evolution of the home entertainment landscape.

The convergence of technologies, such as the integration of AI and VR/AR experiences into home entertainment systems, will create new revenue streams and enhance user engagement. The introduction of higher resolutions (8K) and advanced audio technologies will drive sales of premium devices. Continued expansion of 5G and fiber optic networks will further enhance streaming capabilities, leading to greater adoption.

This report provides a detailed analysis of the electronic home video market, including historical data, market forecasts, and in-depth insights into key trends and drivers. The report covers various segments of the market, including different applications, types of services, and geographic regions. It also highlights the leading players in the industry and their competitive strategies. The information presented offers valuable insights for stakeholders interested in the growth and development of this dynamic market.

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 8% from 2020-2034 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately 8%.

Key companies in the market include BBC, Cartoon Network, CBS, Hulu, Netflix, YouTube, Samsung Electronics Co. Ltd., Panasonic Corporation, Sony Corporation, LG Electronics Inc., Mitsubishi Electric Corporation, Sennheiser electronic GmbH & Co. KG, Bose Corporation, Koninklijke Philips N.V., Haier Inc., Microsoft Corporation, .

The market segments include Application, Type.

The market size is estimated to be USD 250 billion as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3480.00, USD 5220.00, and USD 6960.00 respectively.

The market size is provided in terms of value, measured in billion.

Yes, the market keyword associated with the report is "Electronic Home Video," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Electronic Home Video, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.