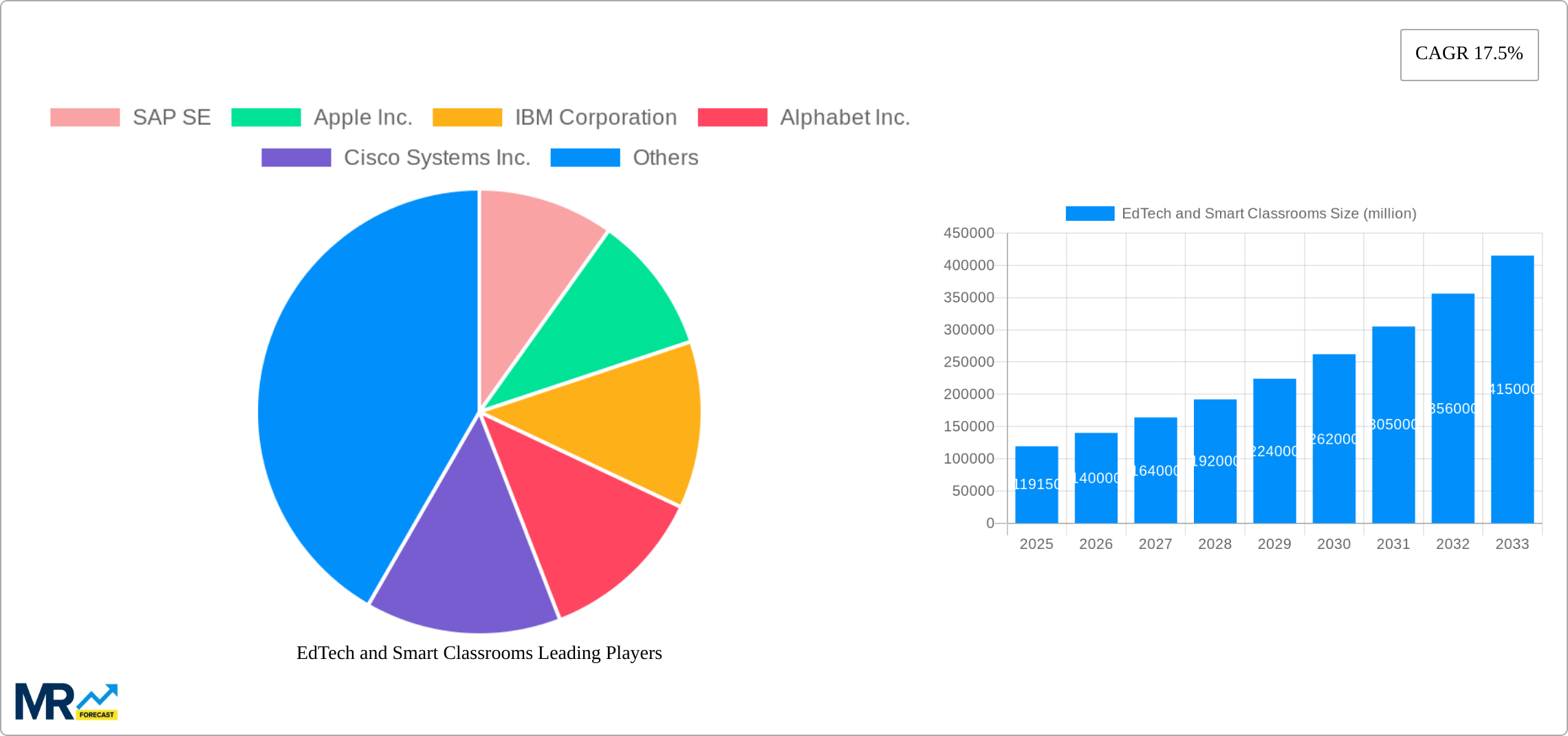

1. What is the projected Compound Annual Growth Rate (CAGR) of the EdTech and Smart Classrooms?

The projected CAGR is approximately 17.5%.

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

EdTech and Smart Classrooms

EdTech and Smart ClassroomsEdTech and Smart Classrooms by Type (Hardware, Software, Serve), by Application (Higher Education, K-12, Kindergarten), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2025-2033

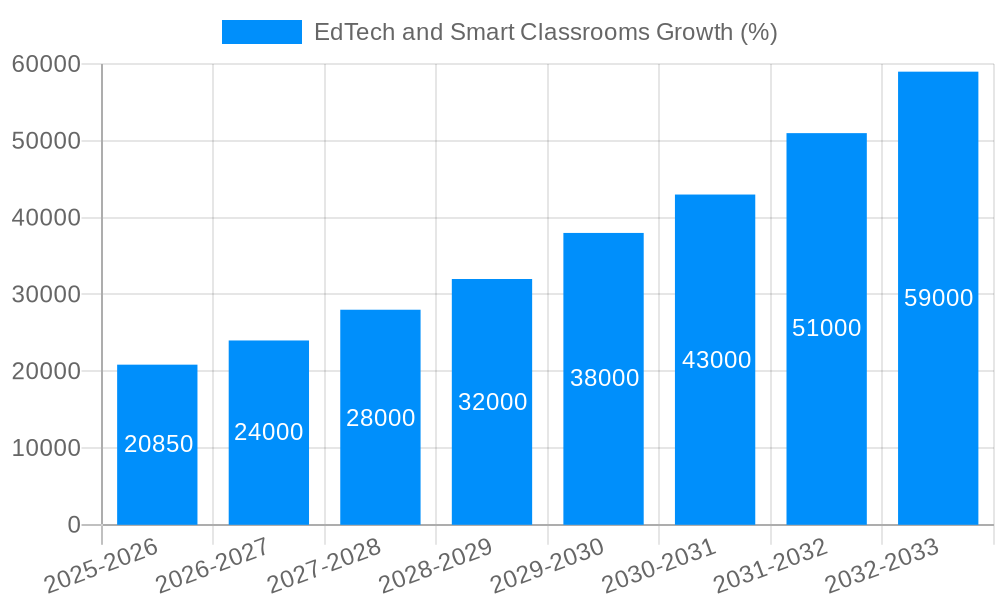

The EdTech and Smart Classrooms market is experiencing robust growth, projected to reach a market size of $119.15 billion in 2025 and maintain a Compound Annual Growth Rate (CAGR) of 17.5% from 2025 to 2033. This expansion is fueled by several key factors. Firstly, the increasing adoption of technology in education, driven by a need for improved learning outcomes and engaging educational experiences, is a primary driver. Governments worldwide are investing heavily in digital infrastructure and educational technology initiatives, further accelerating market growth. Secondly, the rising demand for personalized learning and blended learning models necessitates the implementation of smart classroom solutions that provide customized learning paths and real-time feedback. The integration of Artificial Intelligence (AI) and data analytics into EdTech tools allows for better assessment of student performance and tailored educational interventions. Finally, the shift towards online and remote learning, accelerated by recent global events, has significantly broadened the market's reach and created new avenues for EdTech companies. The hardware segment, encompassing interactive whiteboards, tablets, and laptops, forms a substantial part of this market, while the software segment, including Learning Management Systems (LMS) and educational apps, is witnessing exponential growth.

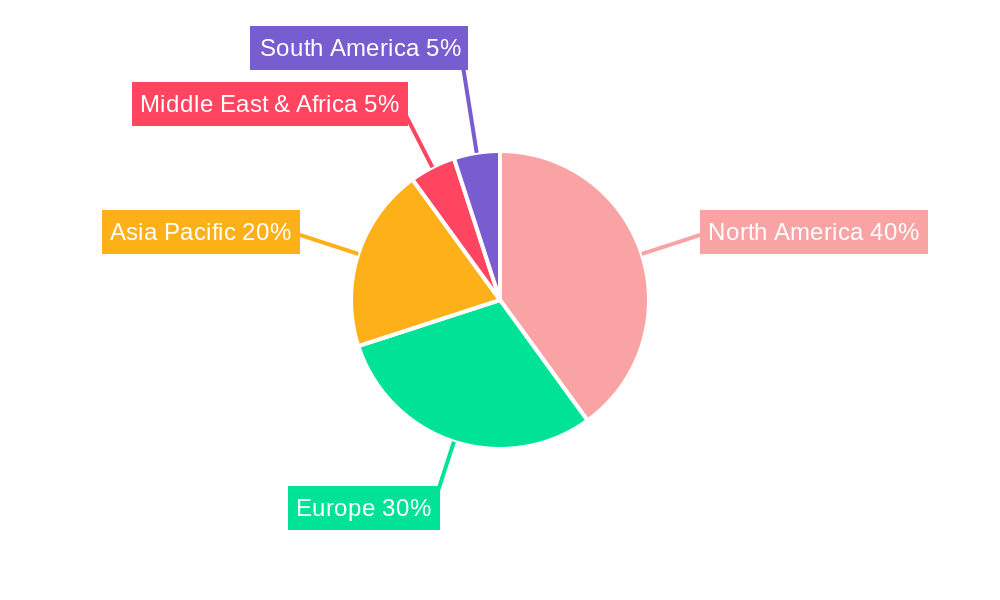

The market segmentation reveals significant opportunities across various educational levels. Higher education institutions are early adopters of advanced technologies, while the K-12 and Kindergarten segments are showing rapid growth potential as institutions increasingly integrate smart classroom technologies to improve teaching efficacy and student engagement. Geographic distribution reflects a strong presence in North America and Europe, driven by robust technological infrastructure and higher levels of investment in education. However, the Asia-Pacific region, particularly India and China, is poised for significant growth, fueled by increasing government support and a large, digitally-savvy student population. Key players such as SAP, Apple, IBM, Google, Cisco, Amazon, Microsoft, SMART Technologies, Dell, and Fujitsu are shaping the market landscape through continuous innovation and expansion of their product portfolios. The competitive landscape is dynamic, characterized by strategic partnerships, mergers and acquisitions, and the development of innovative EdTech solutions catering to the evolving needs of the educational sector.

The EdTech and smart classroom market is experiencing explosive growth, projected to reach multi-billion dollar valuations by 2033. From 2019 to 2024 (historical period), the industry witnessed a significant surge driven by increasing internet penetration, the proliferation of mobile devices, and a growing emphasis on personalized learning. The base year of 2025 marks a crucial point, with the market already demonstrating robust expansion. Our forecast period, 2025-2033, anticipates continued, albeit perhaps more tempered, growth, fueled by ongoing technological advancements and evolving pedagogical approaches. Key market insights reveal a strong preference for integrated solutions combining hardware, software, and services, tailored to specific educational segments like K-12, higher education, and even kindergarten. The shift towards hybrid and online learning models, accelerated by recent global events, is significantly impacting market dynamics, boosting demand for virtual reality (VR), augmented reality (AR), and artificial intelligence (AI)-powered educational tools. Competition is fierce, with major technology players like Microsoft, Apple, and Google vying for market share alongside specialized EdTech companies. This competition fosters innovation and drives down costs, ultimately benefiting educational institutions and students alike. The market is segmented by hardware (interactive whiteboards, laptops, tablets), software (learning management systems, educational apps), services (training, support), and application (K-12, higher education). Each segment contributes uniquely to the overall market value, with certain segments, particularly software and services, demonstrating particularly strong growth trajectories. The increasing adoption of cloud-based solutions and the integration of data analytics for personalized learning are further shaping the market landscape. The estimated market value for 2025 places the industry at a substantial level, indicating its significant economic impact and widespread adoption across various educational settings worldwide.

Several factors are accelerating the adoption of EdTech and smart classrooms. Firstly, the increasing need for personalized learning experiences is a major driver. Traditional "one-size-fits-all" teaching methods are increasingly being replaced by tailored approaches leveraging technology to cater to individual student needs and learning styles. Secondly, the demand for improved educational outcomes is pushing institutions to adopt innovative technologies that enhance engagement and knowledge retention. Smart classrooms offer interactive learning environments, fostering active participation and collaboration among students. Thirdly, technological advancements themselves are a powerful driving force. The continuous development of user-friendly software, affordable hardware, and robust cloud-based solutions makes EdTech more accessible and affordable to a wider range of educational institutions. Furthermore, the growing adoption of blended learning models, combining online and in-person instruction, necessitates the integration of technology into the classroom. This shift is particularly pronounced in higher education, where online courses and digital resources are becoming increasingly prevalent. Finally, government initiatives and funding programs aimed at promoting digital literacy and improving educational infrastructure are playing a significant role in boosting the market's growth. These programs often provide financial incentives for schools and universities to adopt EdTech solutions, accelerating the overall market expansion.

Despite the significant growth, the EdTech and smart classroom market faces several challenges. A primary concern is the digital divide, with unequal access to technology and internet connectivity creating disparities between different socioeconomic groups and geographic locations. This inequitable access hinders the potential benefits of EdTech, potentially exacerbating existing educational inequalities. Furthermore, the high cost of implementing and maintaining smart classroom technologies can be a significant barrier for many schools and universities, especially those with limited budgets. The initial investment in hardware, software, teacher training, and ongoing technical support can be substantial. Another challenge is the effective integration of technology into the curriculum and pedagogical approaches. Simply introducing technology into the classroom is not sufficient; teachers require adequate training and support to effectively utilize these tools to enhance learning outcomes. Concerns about data privacy and security are also growing, as the use of EdTech involves collecting and storing sensitive student data. Ensuring the responsible and ethical use of this data is crucial to maintain trust and avoid potential risks. Finally, the rapid pace of technological change requires continuous updates and upgrades, adding to the ongoing costs and demanding continuous professional development for educators. Addressing these challenges is crucial to ensure the equitable and effective implementation of EdTech across all educational settings.

The North American market, particularly the United States and Canada, is expected to dominate the EdTech and smart classroom sector during the forecast period (2025-2033). This dominance stems from high technological adoption rates, substantial investments in education, and a strong presence of major EdTech companies. Furthermore, the K-12 segment is anticipated to experience significant growth, driven by increasing government initiatives to improve educational infrastructure and a rising awareness of the benefits of technology-integrated learning at the foundational levels of education.

North America (United States and Canada): High technological adoption rates, substantial investment in education, and a concentration of major EdTech companies contribute significantly to this region's market dominance. Government initiatives focused on enhancing digital literacy further propel the market’s expansion.

Europe: While slightly behind North America, Europe exhibits significant growth potential, fueled by increasing government funding for digital education initiatives and expanding technological adoption across various educational levels. Specific countries like the United Kingdom and Germany are expected to be major contributors within this region.

Asia-Pacific: This region is experiencing rapid growth, primarily driven by increasing urbanization, a rising middle class, and a focus on improving educational quality through technology integration. Countries like India, China, and Japan are key markets within this region.

K-12 Segment: This segment exhibits the highest growth potential due to the increasing adoption of technology in primary and secondary education globally. The need to enhance learning outcomes and adapt to evolving learning styles among younger generations boosts this segment’s prominence. The focus on early childhood education and the digitalization of learning materials make it highly dynamic.

Software Segment: The software component of EdTech has become a significant driver of overall market growth. This is largely due to the rising adoption of Learning Management Systems (LMS) and educational software applications, which offer a wide array of features, making them valuable across all educational levels. Furthermore, the transition to cloud-based software solutions has been impactful.

Services Segment: The demand for professional services and support related to EdTech implementation and training is also driving market growth. This segment includes services like teacher training, technical support, and customized solutions designed to optimize technology usage within educational settings.

Several key factors are accelerating the growth of the EdTech and smart classrooms industry. Increased government funding and initiatives aimed at improving digital literacy are creating a favorable environment for adoption. The rising popularity of blended and online learning models further boosts demand for technology-based educational solutions. Furthermore, continuous advancements in artificial intelligence, virtual reality, and augmented reality are providing innovative tools for personalized and engaging learning experiences. The availability of cost-effective and user-friendly software and hardware solutions is broadening the accessibility of EdTech to a wider range of institutions and learners.

This report offers a comprehensive analysis of the EdTech and smart classrooms market, providing valuable insights into market trends, driving forces, challenges, and key players. It covers various segments including hardware, software, services, and application areas like K-12, higher education, and kindergarten, providing a detailed overview of the market's structure and dynamics. The report also includes forecasts for the period 2025-2033, offering valuable projections for market growth and future trends. This detailed analysis allows stakeholders to make informed decisions and capitalize on the significant opportunities within this rapidly expanding sector.

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 17.5% from 2019-2033 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately 17.5%.

Key companies in the market include SAP SE, Apple lnc., IBM Corporation, Alphabet lnc., Cisco Systems Inc., Amazon.com lnc., Microsoft Corporation, SMARTTechnologies ULC, Dell lnc., Fujitsu Limited, .

The market segments include Type, Application.

The market size is estimated to be USD 119150 million as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3480.00, USD 5220.00, and USD 6960.00 respectively.

The market size is provided in terms of value, measured in million.

Yes, the market keyword associated with the report is "EdTech and Smart Classrooms," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the EdTech and Smart Classrooms, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.