1. What is the projected Compound Annual Growth Rate (CAGR) of the Direct Bank?

The projected CAGR is approximately 7.5%.

Direct Bank

Direct BankDirect Bank by Type (Neo Bank, Challenger Bank), by Application (Business, Personal), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2026-2034

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

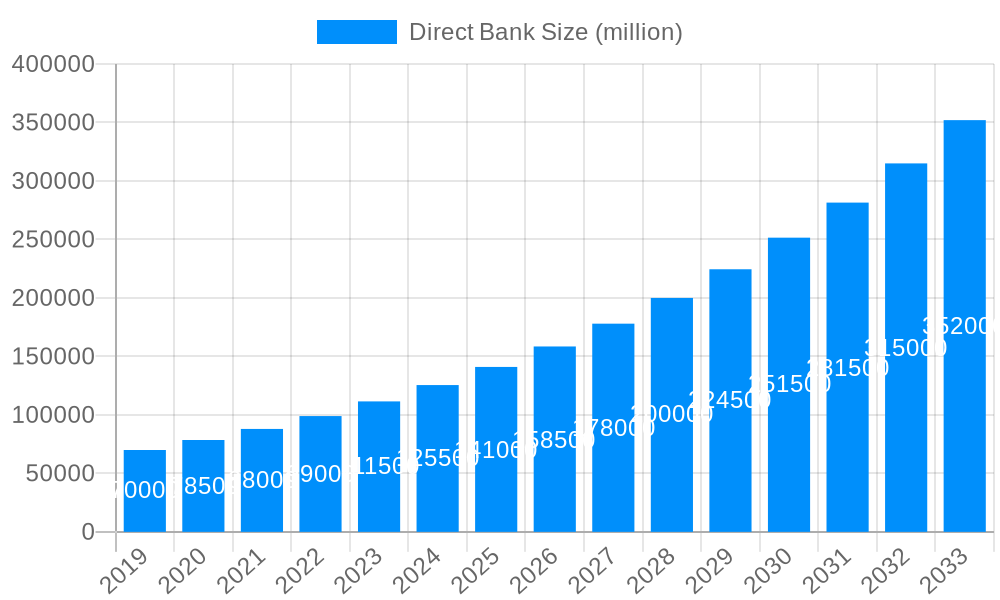

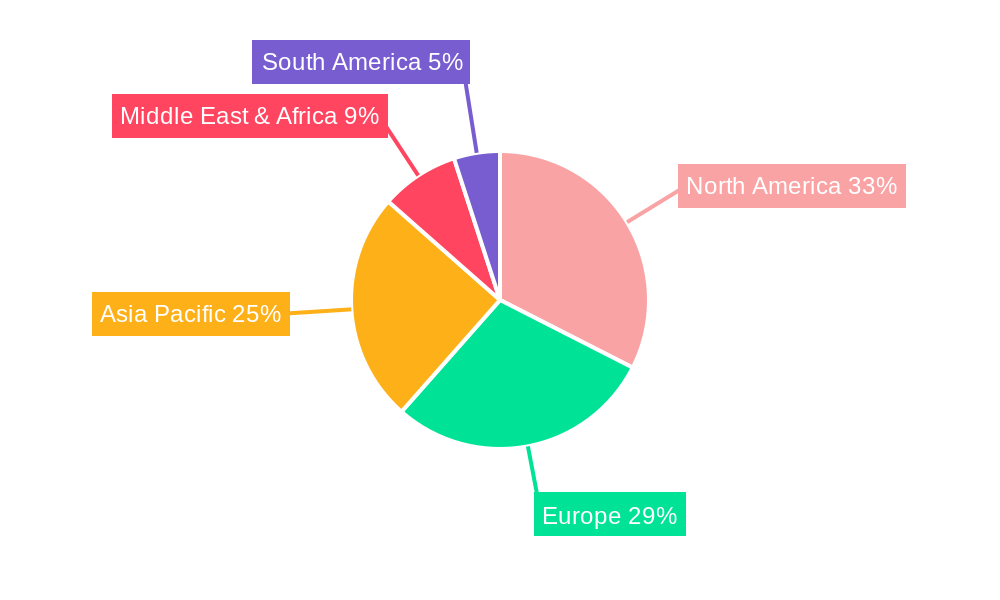

The global direct banking market is experiencing robust growth, driven by the increasing adoption of digital technologies and the rising demand for convenient and personalized financial services. The shift towards mobile-first banking experiences, coupled with the appeal of lower fees and streamlined processes offered by direct banks, is attracting a significant customer base, particularly among millennials and Gen Z. Neo-banks and challenger banks are leading this disruption, leveraging innovative technologies like AI and machine learning to enhance customer experience and offer customized financial products. While the market size in 2025 is estimated at $150 billion (based on inferred growth from available data and industry trends), a compound annual growth rate (CAGR) of 15% is projected for the forecast period of 2025-2033, indicating a substantial expansion of this market. This growth is further fueled by factors such as increasing smartphone penetration, improved internet connectivity, and growing financial literacy globally. The Personal banking segment dominates the application type, while geographically, North America and Europe hold significant market shares, although Asia-Pacific is expected to witness the fastest growth in the coming years due to its large and rapidly digitalizing population.

However, the market faces certain restraints. Stringent regulatory requirements and cybersecurity concerns pose challenges to market expansion. Competition from established traditional banks, who are investing heavily in digital transformation, is another factor impacting the growth trajectory. Furthermore, maintaining customer trust and managing operational efficiency are crucial for direct banks to sustain their growth. Successful players are investing heavily in robust security measures, seamless customer onboarding processes, and personalized financial solutions to gain a competitive edge. The market will continue to evolve, with a focus on enhancing financial inclusion, offering innovative products and services, and strengthening customer relationships. The increasing adoption of open banking APIs is also expected to fuel innovation and competition in this market. Successful direct banks will be those that adapt quickly to changing customer demands, leverage technological advancements, and prioritize security and regulatory compliance.

The direct banking sector, encompassing both neo-banks and challenger banks, experienced a period of explosive growth between 2019 and 2024, fueled by technological advancements, shifting consumer preferences, and increasing dissatisfaction with traditional banking models. The market witnessed a significant influx of new entrants, each vying for a slice of the rapidly expanding digital banking pie. This surge resulted in heightened competition, driving innovation in areas such as mobile banking applications, personalized financial management tools, and streamlined account opening processes. The historical period (2019-2024) showcased a clear shift in market share, with established players adapting their strategies to compete against agile newcomers offering superior digital experiences. By 2025 (estimated year), the direct banking market is projected to reach a valuation of several billion USD, reflecting the sustained popularity and growing adoption of digital banking solutions. This growth is expected to continue throughout the forecast period (2025-2033), albeit at a potentially moderated pace as the market matures and consolidation occurs. Key market insights suggest a rising demand for niche services catering to specific demographic groups and business needs, along with an increasing emphasis on security and regulatory compliance. The integration of AI and machine learning is revolutionizing customer service and risk management, further differentiating direct banks from traditional institutions. The expansion into underserved markets and geographical regions also presents significant opportunities for growth, particularly in developing economies with high mobile penetration rates. Overall, the direct banking market demonstrates remarkable resilience and transformative potential, poised for continued expansion and evolution over the long term.

Several key factors are driving the remarkable growth trajectory of the direct banking sector. Firstly, the increasing adoption of smartphones and mobile technology has created a fertile ground for digital banking services. Customers are demanding seamless, user-friendly banking experiences accessible anytime, anywhere, which direct banks excel at delivering. Secondly, the inherent agility and innovation of these institutions allow them to respond quickly to evolving market trends and customer needs, a significant advantage over their more bureaucratic traditional counterparts. This nimbleness enables them to launch new products and services rapidly, often capitalizing on emerging fintech solutions and personalized banking options. Furthermore, the comparatively lower overhead costs associated with operating a digital-first model enable direct banks to offer competitive pricing and attractive incentives to customers. This cost-effectiveness is a powerful draw for both individuals and businesses seeking to optimize their banking expenses. Finally, the increasing demand for transparent, ethical, and customer-centric banking practices is fueling the growth of direct banks, which frequently prioritize these values in their marketing and service delivery. The shift in consumer sentiment towards more accessible and personalized financial services creates a favorable environment for these institutions to flourish.

Despite the significant growth and potential of the direct banking sector, several challenges and restraints could impede its progress. Cybersecurity threats remain a significant concern, as these institutions handle sensitive financial data and are vulnerable to increasingly sophisticated cyberattacks. Maintaining robust security measures and consumer trust is paramount for the long-term success of direct banks. Regulatory compliance also poses a significant challenge, especially as the industry evolves rapidly and regulations struggle to keep pace. Navigating the complex web of financial regulations across different jurisdictions requires considerable resources and expertise. Furthermore, building and maintaining customer trust, especially in the initial stages of operation, can be difficult. Direct banks need to demonstrate their reliability and stability to compete effectively with established institutions that benefit from decades of brand recognition. Competition, both within the direct banking sector and from traditional banks that are adopting digital strategies, is fierce. Differentiation and innovation are crucial for survival and growth in this competitive landscape. Finally, achieving profitability can be challenging, particularly for newer entrants that require significant investment in technology and infrastructure before generating substantial revenue. Managing expenses and achieving sustainable profitability remains a critical factor influencing the long-term viability of many direct banking businesses.

The direct banking market is experiencing significant growth across several regions and segments, making it difficult to definitively declare a single dominant force. However, several factors point to strong performance in specific areas:

Key Segment: Personal Banking: The personal banking segment is currently experiencing the most substantial growth due to widespread smartphone adoption and the increasing demand for user-friendly, mobile-first banking solutions. The convenience and personalized features offered by direct banks are particularly appealing to younger demographics. This segment is projected to contribute a substantial portion of the overall market value throughout the forecast period, driving overall growth. The projected market value for personal banking services from direct banks is expected to be several billion USD by 2033.

Key Region/Country: North America & Europe: These regions have mature financial technology ecosystems, high mobile penetration rates, and a significant population receptive to digital banking services. The regulatory environments in these regions, while demanding, also offer a degree of stability and clarity, facilitating the growth of both neo-banks and challenger banks. Further, the presence of well-established venture capital and investment opportunities contributes to the success of direct banks in these regions. The substantial user base and technological advancement fuel innovation and market expansion within the direct banking sector.

Asia-Pacific (specific countries like China, India): While the regulatory landscape may present greater challenges, the immense potential of these markets is undeniable. With a large population and rapidly increasing smartphone penetration, the Asia-Pacific region presents a lucrative opportunity for direct banks that can successfully navigate the local regulatory environment and build trust with consumers. The significant growth potential is offset by market-specific challenges, particularly around financial literacy and cybersecurity concerns.

In summary, the personal banking segment is currently dominating the market, with North America and Europe leading the way in terms of adoption and investment. The Asia-Pacific region presents significant growth potential despite challenges. The direct bank market is a dynamic and rapidly evolving ecosystem, with different segments and regions demonstrating unique opportunities and growth trajectories.

The direct banking industry’s growth is fueled by several key catalysts, including the rising adoption of mobile and digital technologies, increasing customer demand for personalized and convenient banking services, and the innovative use of artificial intelligence and machine learning in financial service delivery. The ability of direct banks to offer competitive pricing and streamlined processes further enhances their appeal to cost-conscious consumers.

This report provides a comprehensive overview of the direct banking industry, analyzing historical trends, current market dynamics, and future growth prospects. It offers valuable insights into key drivers, challenges, and growth catalysts shaping the industry, highlighting leading players and significant developments, and projecting market growth across various segments and geographic regions. The report aids stakeholders in making informed decisions and strategies for success within the dynamic direct banking landscape.

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 7.5% from 2020-2034 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately 7.5%.

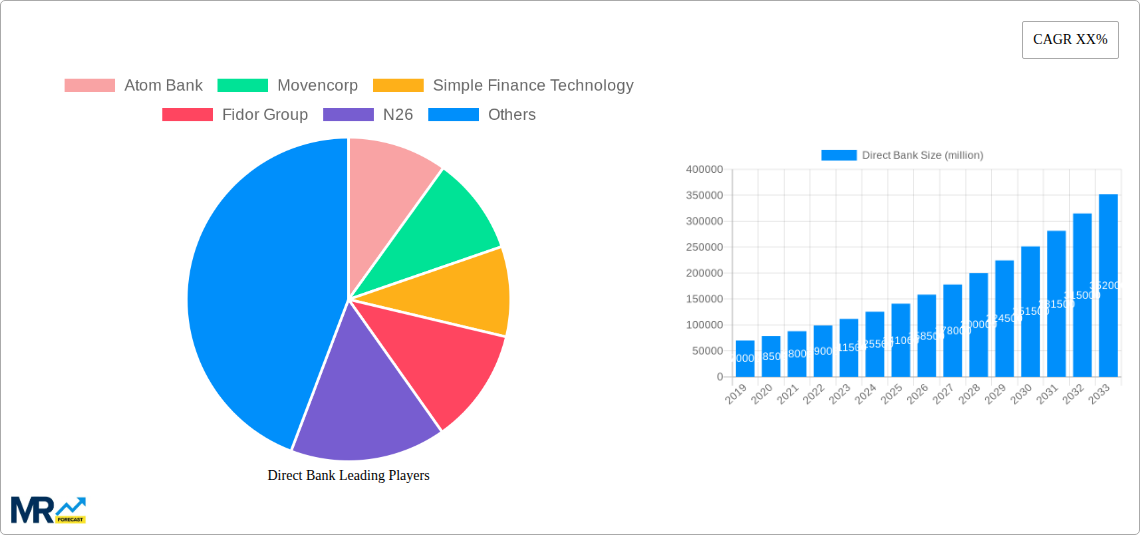

Key companies in the market include Atom Bank, Movencorp, Simple Finance Technology, Fidor Group, N26, Pockit, Ubank, Monzo Bank, MyBank (Alibaba Group), Holvi Bank, WeBank (Tencent Holdings Limited), Hello Bank, Koho Bank, Rocket Bank, Soon Banque, Digibank, Timo, Jibun, Jenius, K Bank, Kakao Bank, Starling Bank, Tandem Bank, .

The market segments include Type, Application.

The market size is estimated to be USD XXX N/A as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3480.00, USD 5220.00, and USD 6960.00 respectively.

The market size is provided in terms of value, measured in N/A.

Yes, the market keyword associated with the report is "Direct Bank," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Direct Bank, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.