1. What is the projected Compound Annual Growth Rate (CAGR) of the Debt Collection Agency?

The projected CAGR is approximately XX%.

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

Debt Collection Agency

Debt Collection AgencyDebt Collection Agency by Type (Early Out Debt, Bad Debt), by Application (Healthcare, Student Loans, Financial Services, Government, Retail, Telecom & Utility, Mortgage & Others), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2025-2033

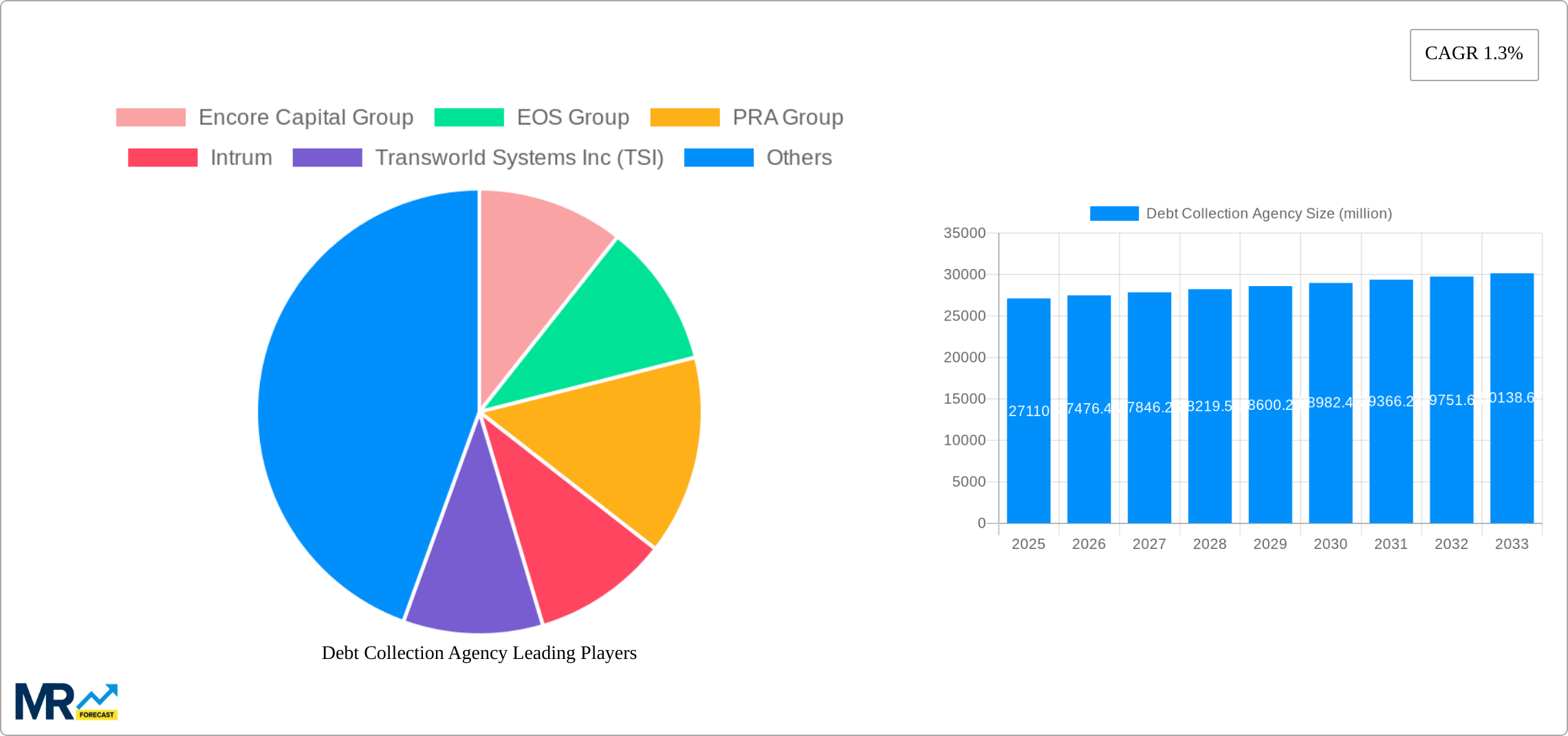

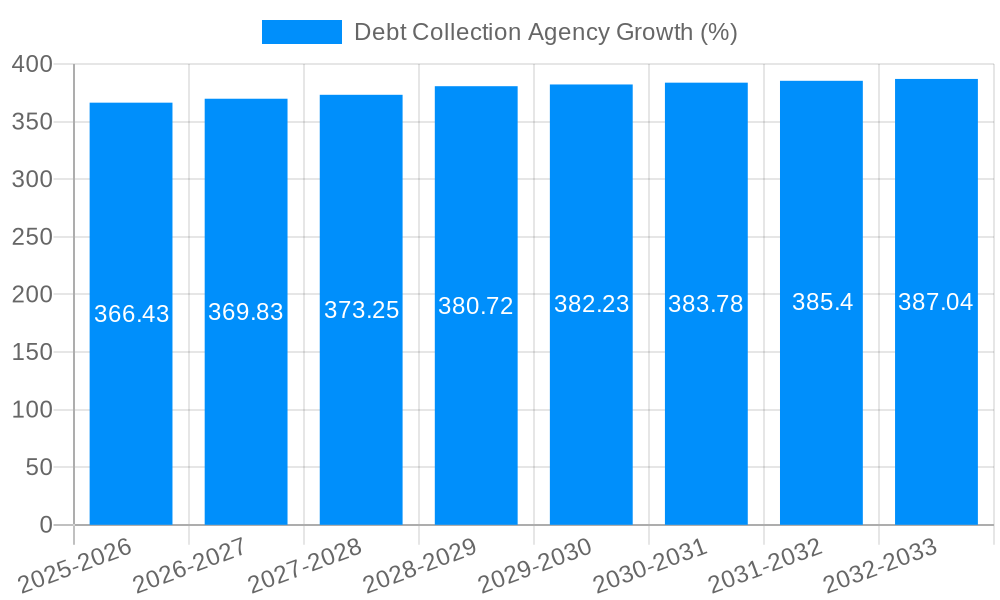

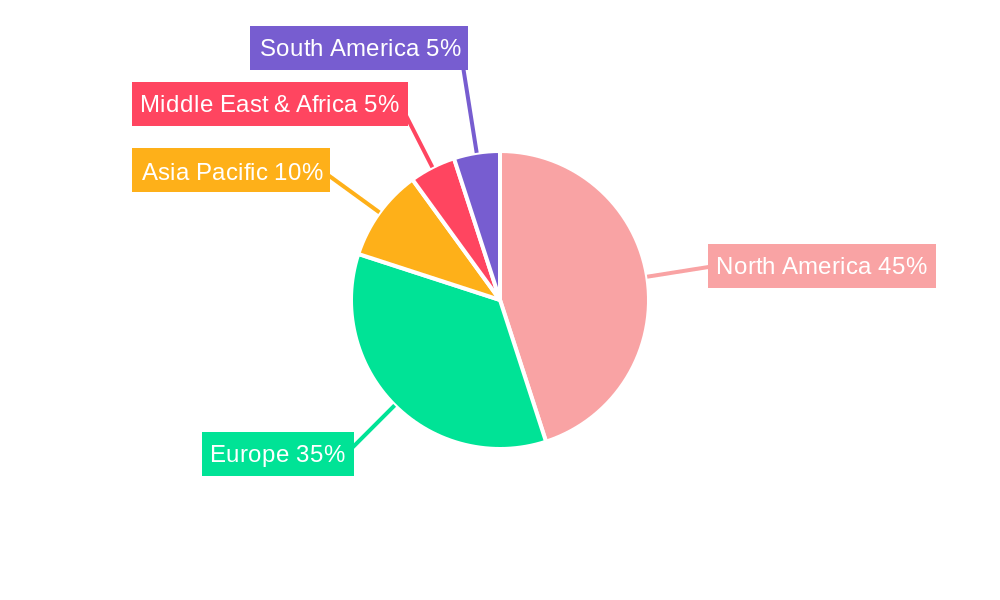

The global debt collection agency market, currently valued at approximately $29.6 billion (2025), is poised for significant growth over the next decade. While a precise CAGR isn't provided, considering the consistent demand driven by rising consumer debt across various sectors (healthcare, student loans, mortgages, etc.), a conservative estimate places the annual growth rate between 5% and 7%. This growth is fueled by several key factors. Increasing levels of consumer debt, particularly in developing economies experiencing rapid economic expansion, are creating a larger pool of delinquent accounts. Furthermore, technological advancements in debt collection, including the implementation of AI-powered analytics and automated systems, are improving efficiency and recovery rates for agencies. The growing sophistication of debt collection strategies, alongside a rise in outsourcing by financial institutions, is another significant driver. However, stringent regulatory environments in many regions, along with growing consumer protection concerns and associated litigation risks, act as significant restraints on market expansion. Market segmentation shows significant opportunity across various debt types and applications. Healthcare debt collection and student loan recovery are expected to experience robust growth due to persistent increases in these forms of debt. The market is highly competitive with numerous established players (Encore Capital Group, EOS Group, PRA Group, etc.) vying for market share alongside smaller, specialized firms. Geographic distribution is diverse, with North America and Europe currently holding the largest market shares, followed by Asia Pacific exhibiting significant growth potential.

The market landscape is dynamic, with companies constantly adapting to changes in regulations and technological advancements. Strategic mergers and acquisitions are likely to occur, further shaping the competitive landscape and leading to consolidation. The future will see increased focus on ethical and compliant collection practices, a demand driven by increased consumer awareness and stronger regulatory scrutiny. Companies that successfully integrate technology to streamline operations while maintaining ethical practices will be best positioned for growth in the coming years. The ongoing evolution of data analytics and predictive modeling will allow for more targeted and effective debt recovery strategies. Successful players will leverage these advancements to offer more efficient and customized solutions to clients in different sectors, creating a competitive advantage in this complex market.

The global debt collection agency market is experiencing robust growth, projected to reach several billion dollars by 2033. The historical period (2019-2024) witnessed a steady increase in demand driven by rising consumer debt across various sectors like healthcare, student loans, and financial services. The base year of 2025 shows a significant market size in the billions, indicating a sustained upward trajectory. This growth is primarily fueled by increasing non-performing assets (NPAs) globally, particularly in developing economies with burgeoning credit markets. The forecast period (2025-2033) anticipates further expansion, driven by technological advancements, regulatory changes, and the evolving strategies of debt collection agencies themselves. We observe a shift towards more sophisticated debt recovery methods, including data analytics and digital communication channels, replacing traditional, often intrusive methods. The market is also witnessing consolidation, with larger players acquiring smaller agencies to expand their reach and service offerings. This consolidation is improving operational efficiencies and allowing agencies to offer more comprehensive debt recovery solutions to clients across various industries. The increasing adoption of automation and AI further enhances efficiency and reduces operational costs. Finally, the growing awareness of ethical debt collection practices is shaping the industry, leading to better consumer relations and reduced legal risks for agencies. The market's future will depend on navigating regulatory changes, technological advancements, and maintaining a balance between efficient debt recovery and consumer rights.

Several factors are propelling the expansion of the debt collection agency market. The ever-increasing consumer debt levels worldwide are a primary driver. Across various segments – from healthcare and student loans to credit cards and mortgages – individuals and businesses are accumulating substantial debts, creating a significant pool of non-performing assets. This necessitates the services of debt collection agencies to recover these outstanding payments. Furthermore, the growing complexity of debt portfolios, often involving multiple creditors and jurisdictions, necessitates specialized expertise and resources offered by professional debt collection agencies. Technological advancements, particularly the use of AI and machine learning in debt recovery strategies, are improving efficiency and reducing costs for both agencies and their clients. Data analytics allows for better targeting of debtors and optimizing collection strategies, leading to higher recovery rates. The rising adoption of digital communication channels allows for more efficient and cost-effective interaction with debtors, enhancing overall efficiency and reducing the operational expenses. Finally, the increasing demand for outsourcing debt collection services by financial institutions and other businesses due to cost savings and the need for specialized expertise further fuels this market's growth.

Despite the positive growth outlook, the debt collection agency market faces several challenges. Stringent regulations and increasing consumer protection laws worldwide pose significant hurdles. Compliance costs are rising as agencies need to adapt to ever-changing legal frameworks, impacting profitability. Negative public perception of debt collection practices, often associated with aggressive or unethical methods, remains a major concern. This can lead to reputational damage for agencies and increased scrutiny from regulatory bodies. The fluctuating economic conditions also pose a challenge, impacting debt levels and the ability of debtors to repay. Recessions or economic downturns typically lead to an increase in NPAs, but simultaneously, debtor's ability to repay declines, making the debt collection process more difficult. Maintaining a skilled workforce is also crucial, as experienced debt collectors are in high demand. Competition within the industry is fierce, with both established players and new entrants vying for market share, requiring agencies to continuously innovate and optimize their services. Finally, technological advancements, while beneficial in many ways, require significant investments in training and infrastructure, which can be a challenge for smaller agencies.

The Financial Services segment is projected to dominate the debt collection agency market during the forecast period (2025-2033). This is due to the substantial volume of outstanding debt in the financial services sector, encompassing credit cards, personal loans, mortgages, and other forms of consumer and commercial credit. The high value of these loans translates to significant revenue potential for debt collection agencies.

The combination of the financial services segment and North America/Europe's developed infrastructure and regulatory environment creates a powerful synergistic effect for market dominance.

Technological advancements such as AI-powered analytics for improved debt recovery strategies, the adoption of digital communication channels for increased efficiency, and data-driven decision-making are key catalysts. Furthermore, the increasing outsourcing of debt collection activities by financial institutions and corporations, driven by cost optimization and expertise, fuels substantial growth.

This report provides a comprehensive overview of the debt collection agency market, offering detailed insights into market trends, growth drivers, challenges, and key players. It includes historical data (2019-2024), base-year estimates (2025), and future forecasts (2025-2033), providing a comprehensive understanding of this dynamic industry and the factors shaping its future. The report segments the market by type of debt, application area, and geographical region, enabling a granular analysis of specific market segments. It also offers profiles of leading players, highlighting their strategies and market positions.

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of XX% from 2019-2033 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately XX%.

Key companies in the market include Encore Capital Group, EOS Group, PRA Group, Intrum, Transworld Systems Inc (TSI), Midland Credit Management, TCM Group, GC Services, Hoist Finance, Arrow Global, Creditreform, Axactor, B2Holding, KRUK Group, Lowell, Arvato (Bertelsmann Group), Alorica, Cerved, iQera, iQor, IC System, coeo Inkasso GmbH, Altus GTS Inc., Weltman, Weinberg & Reis, Atradius Collections, Bierens Debt Recovery Lawyers, Link Financial, UNIVERSUM Group, Prestige Services Inc (PSI), Asta Funding, .

The market segments include Type, Application.

The market size is estimated to be USD 29600 million as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4480.00, USD 6720.00, and USD 8960.00 respectively.

The market size is provided in terms of value, measured in million.

Yes, the market keyword associated with the report is "Debt Collection Agency," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Debt Collection Agency, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.