1. What is the projected Compound Annual Growth Rate (CAGR) of the DAC High Speed Cable?

The projected CAGR is approximately 36.1%.

DAC High Speed Cable

DAC High Speed CableDAC High Speed Cable by Type (Passive DAC Cable, Active DAC Cable), by Application (Data Center, High Performance Computing (HPC) Center), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2026-2034

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

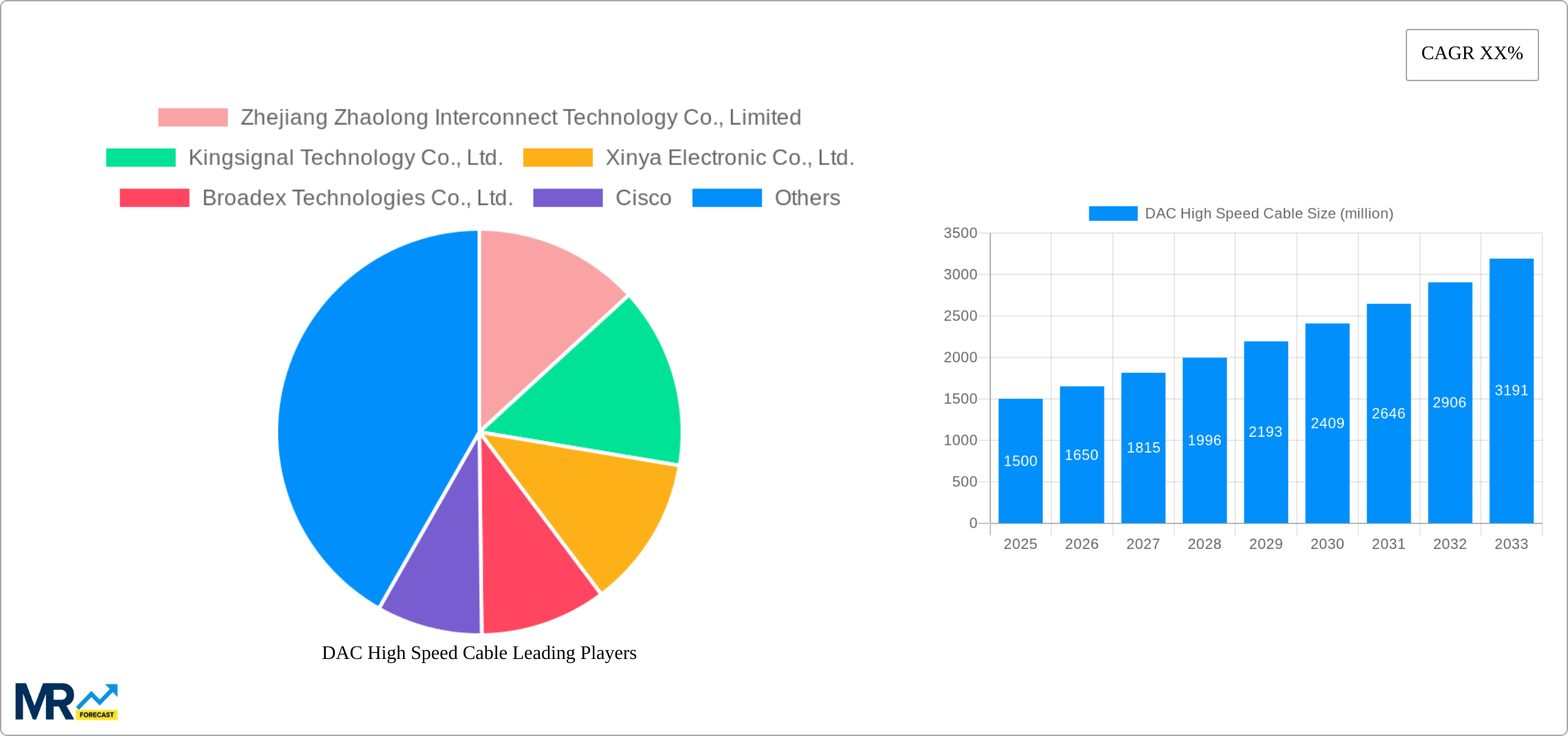

The global High-Speed Direct Attach Copper (DAC) cable market is poised for significant expansion, driven by escalating demands for high-bandwidth connectivity within data centers and high-performance computing (HPC) environments. Key growth catalysts include the widespread adoption of cloud computing, big data analytics, and artificial intelligence, all necessitating robust data transfer capabilities. The increasing density of server deployments and the transition to 400GbE and 800GbE technologies are further accelerating market momentum. Active DAC cables, offering superior reach and signal amplification, are increasingly favored in larger data center architectures. The market is characterized by intense competition from industry leaders such as Cisco, Nvidia, and Hewlett Packard Enterprise, alongside specialized emerging interconnect technology providers. Geographically, North America and Asia-Pacific represent dominant markets, with emerging economies demonstrating substantial growth potential through infrastructure investments. Despite potential supply chain challenges and raw material price volatility, the outlook for High-Speed DAC cables is strong, with an anticipated Compound Annual Growth Rate (CAGR) of 36.1% from a market size of $12.67 billion in the base year 2025.

Segmentation analysis highlights a clear trend towards active DAC cables for applications requiring extended reach, such as large-scale data centers and HPC facilities. Passive DAC cables continue to be a cost-effective solution for shorter connections in smaller data centers and local area networks. Future segmentation is expected to evolve with the development of specialized cables catering to specific networking protocols and applications. The competitive landscape will likely intensify with ongoing innovation focused on enhancing signal integrity, power efficiency, and cable management. Strategic collaborations and M&A activities among key players are anticipated to reshape market dynamics. Continuous research and development will be vital for manufacturers to maintain a competitive edge and meet the evolving needs of the high-speed networking industry.

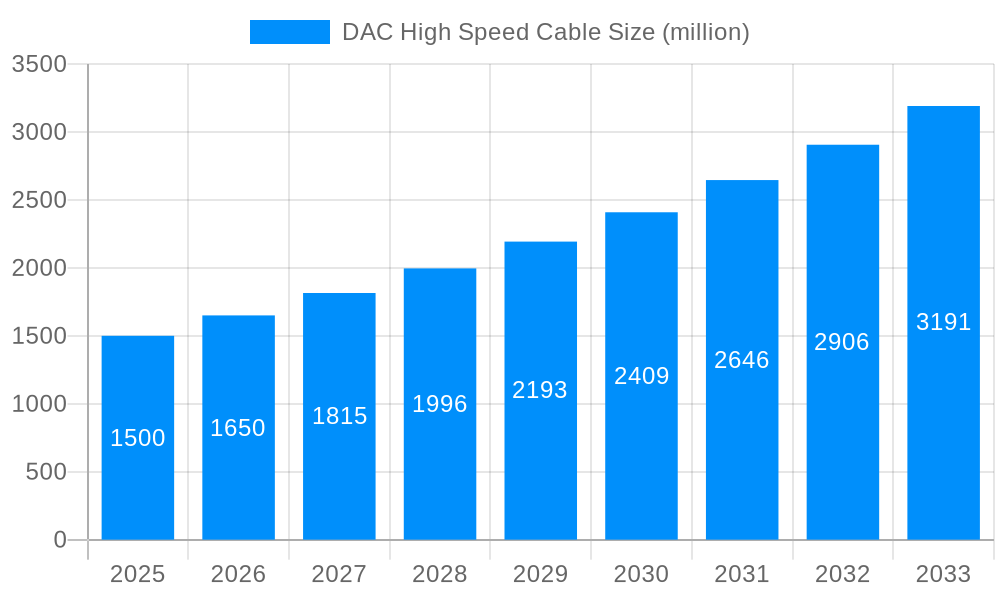

The global DAC (Direct Attach Copper) high-speed cable market is experiencing explosive growth, driven by the insatiable demand for higher bandwidth and lower latency in data centers and high-performance computing (HPC) environments. Over the study period (2019-2033), the market has witnessed a dramatic increase in sales, exceeding several million units annually. While the historical period (2019-2024) saw significant adoption, the estimated year (2025) projects even more substantial growth, setting the stage for a robust forecast period (2025-2033). This expansion is fueled by several converging factors: the proliferation of cloud computing, the rise of artificial intelligence (AI) and machine learning (ML) applications, and the increasing adoption of 400G, 800G, and beyond Ethernet technologies. The market is witnessing a shift towards higher-speed cables, reflecting the growing need for faster data transmission in modern networks. This trend is further accelerated by the increasing deployment of high-density servers and switches, demanding more efficient and cost-effective interconnect solutions. Passive DAC cables currently dominate the market due to their lower cost and simpler design, but active DAC cables are gaining traction as data rates climb beyond 400G, where signal attenuation becomes a significant constraint. The competitive landscape is dynamic, with both established players and emerging companies vying for market share through innovation in cable design, manufacturing efficiency, and strategic partnerships. The ongoing miniaturization of electronic components and packaging technologies is also playing a crucial role in improving the performance and reducing the size of DAC cables, leading to greater scalability and density in data centers. The market's evolution reflects a continual push towards higher speeds, lower power consumption, and enhanced reliability, shaping the future of high-speed data transmission.

Several key factors are driving the phenomenal growth of the DAC high-speed cable market. The explosive growth of cloud computing and data centers is a primary driver, as these facilities require massive bandwidth to support ever-increasing workloads. The expanding adoption of high-performance computing (HPC) for scientific research, financial modeling, and AI/ML applications further fuels demand for high-speed interconnects. The transition to higher Ethernet speeds (400G, 800G, and beyond) necessitates the use of DAC cables, as traditional optical solutions become less cost-effective at these speeds. Cost advantages compared to optical cabling are a major draw for many businesses, especially in data centers where hundreds or thousands of connections are required. The continued miniaturization of electronics leads to more compact and efficient DAC cables, increasing their appeal for space-constrained data center deployments. Furthermore, technological advancements in materials science and cable design have enhanced the performance and reliability of DAC cables, ensuring their continued suitability for demanding applications. Finally, strong support from key industry players, including large technology companies and data center operators, is pushing the market forward through investments in research, development, and large-scale deployments.

Despite the considerable growth, the DAC high-speed cable market faces several challenges. Signal attenuation limits the maximum cable length, especially at higher data rates. This necessitates the use of active DAC cables in certain applications, increasing costs and complexity. The market is intensely competitive, leading to price pressures and making it difficult for smaller players to establish a significant market share. Technological advancements are rapid, requiring manufacturers to continuously innovate and adapt to remain competitive. Ensuring consistent quality and reliability across a large-scale production environment is essential to avoid costly failures in critical data center infrastructure. Furthermore, the market is sensitive to global economic fluctuations, with downturns potentially impacting investment and demand. Meeting ever-increasing demands for higher bandwidth and lower latency requires constant technological breakthroughs and continuous improvement in cable design and manufacturing processes. Regulatory compliance and environmental concerns related to material sourcing and end-of-life cable disposal also pose challenges that manufacturers need to address effectively.

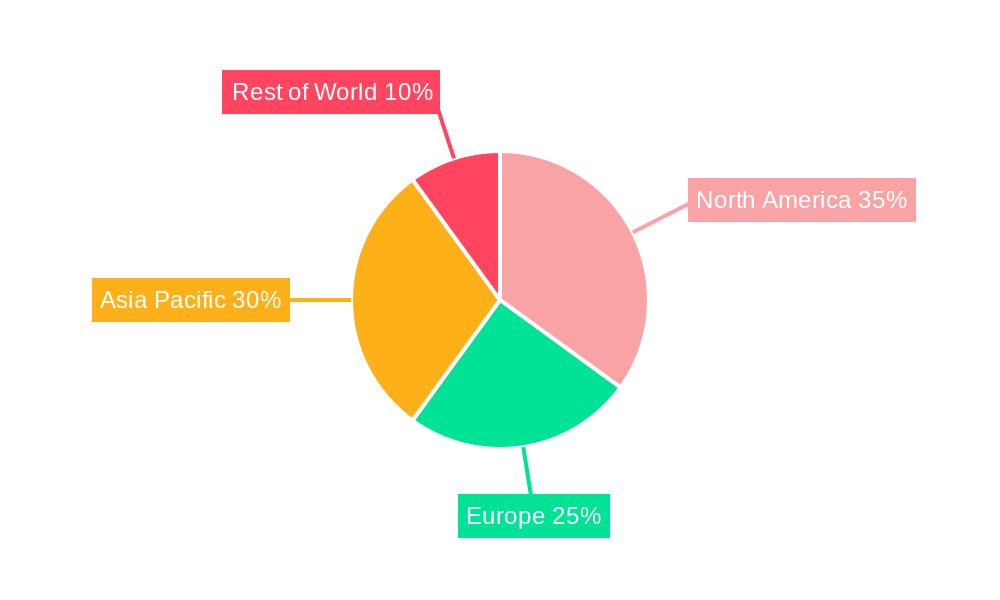

The data center segment is expected to dominate the DAC high-speed cable market, accounting for a significant portion of total sales in the millions of units. This is attributed to the explosive growth of cloud computing and the associated demand for high-bandwidth interconnects within data centers. The North American and Asia-Pacific regions are projected to be the leading markets, driven by the high concentration of data centers and HPC facilities in these areas. Within the data center segment, passive DAC cables hold a larger market share in the lower speed categories (e.g., 100G and 200G), due to their cost-effectiveness. However, as data rates increase to 400G and beyond, the share of active DAC cables will increase significantly because of their ability to overcome signal attenuation limitations at longer cable lengths.

Data Center Segment Dominance: The immense growth of cloud services and hyperscale data centers is driving unprecedented demand for high-speed interconnects. This segment is projected to consume millions of DAC cables annually, significantly contributing to market expansion.

North American and Asia-Pacific Regions Leading: The presence of major technology companies, hyperscale data centers, and robust HPC infrastructure in North America and the Asia-Pacific region positions them as dominant markets.

Passive DAC Cable Market Share: While active DAC cables are gaining traction, passive DAC cables maintain a significant market share, particularly in applications where cost-effectiveness is prioritized and cable lengths are relatively short.

Active DAC Cable Growth: The increasing demand for higher data rates and longer reach necessitates the adoption of active DAC cables. This segment is projected to experience significant growth over the forecast period, driven by the transition towards 400G, 800G, and beyond Ethernet technologies.

The DAC high-speed cable industry benefits from several growth catalysts. The relentless growth of data centers fueled by cloud computing is a primary driver. The increasing adoption of high-performance computing (HPC) applications across various industries, such as scientific research, finance, and artificial intelligence, also significantly boosts demand. Technological advancements in cable design and materials science lead to higher bandwidth, longer reach, and improved reliability, further fueling market growth. Furthermore, strategic partnerships between cable manufacturers and major technology companies help accelerate the adoption of these essential components in large-scale deployments.

This report provides a comprehensive overview of the DAC high-speed cable market, encompassing detailed analysis of market trends, driving forces, challenges, key players, and future projections. The report offers valuable insights into the various segments of the market, including passive and active DAC cables, along with applications in data centers and HPC environments. This information enables businesses to make informed strategic decisions, identify growth opportunities, and navigate the competitive landscape effectively. It utilizes a robust methodology based on extensive primary and secondary research, ensuring the accuracy and reliability of presented data and forecasts.

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 36.1% from 2020-2034 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately 36.1%.

Key companies in the market include Zhejiang Zhaolong Interconnect Technology Co., Limited, Kingsignal Technology Co., Ltd., Xinya Electronic Co., Ltd., Broadex Technologies Co., Ltd., Cisco, Nvidia, C-Flink, Hewlett Packard Enterprise (HPE), Juniper Networks, Mellanox Technologies, Arista Networks, Supermicro, QLogic Corporation, Brocade Communications Systems, Avago Technologies.

The market segments include Type, Application.

The market size is estimated to be USD 12.67 billion as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3480.00, USD 5220.00, and USD 6960.00 respectively.

The market size is provided in terms of value, measured in billion and volume, measured in K.

Yes, the market keyword associated with the report is "DAC High Speed Cable," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the DAC High Speed Cable, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.