1. What is the projected Compound Annual Growth Rate (CAGR) of the Cybersecurity in Aerospace?

The projected CAGR is approximately XX%.

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

Cybersecurity in Aerospace

Cybersecurity in AerospaceCybersecurity in Aerospace by Type (Solutions, Services), by Application (Avionics, In-flight Entertainment Systems, Air Traffic Management Systems, Aviation Maintenance Systems, Aviation Supply Chains, Airport Operations, Aerospace Operations), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2025-2033

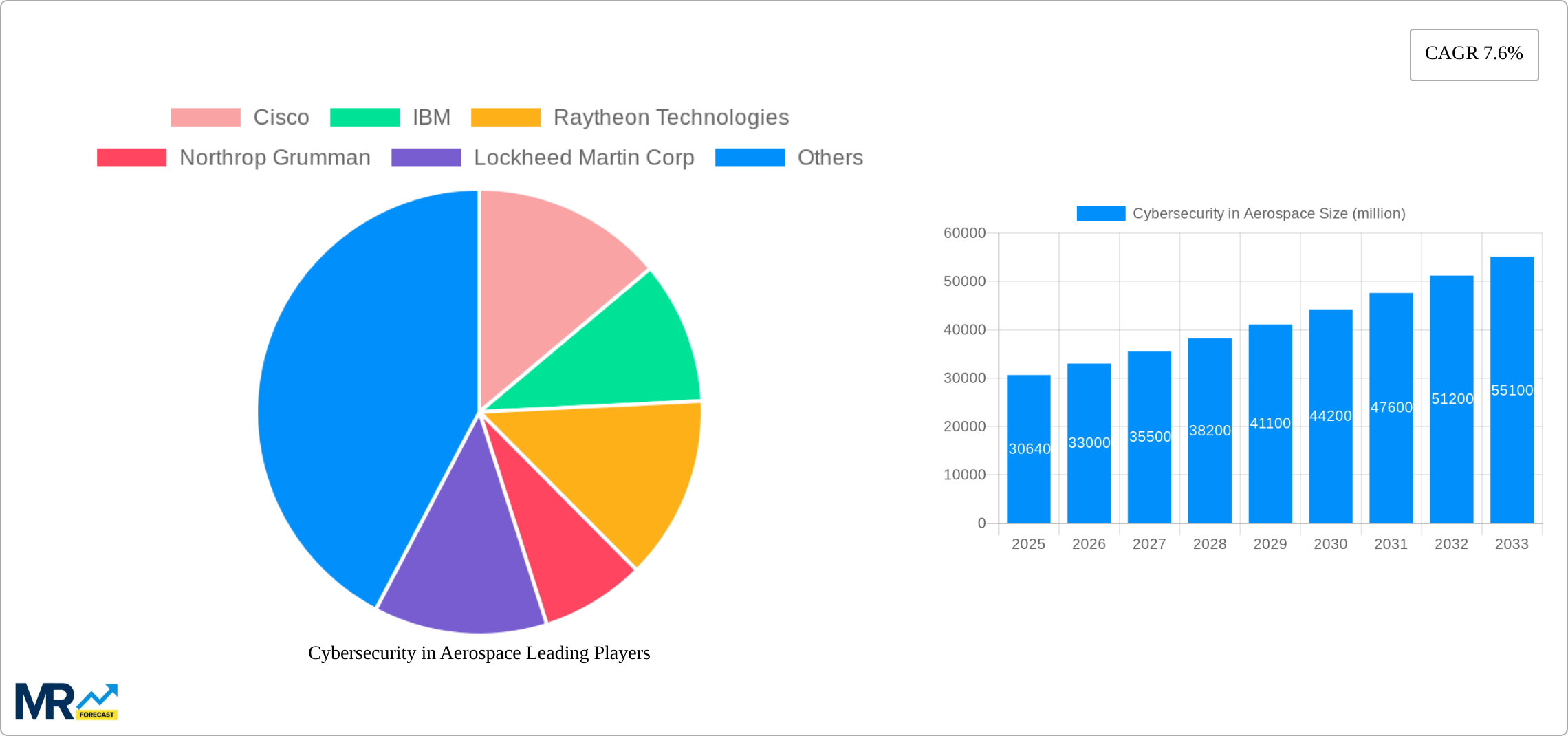

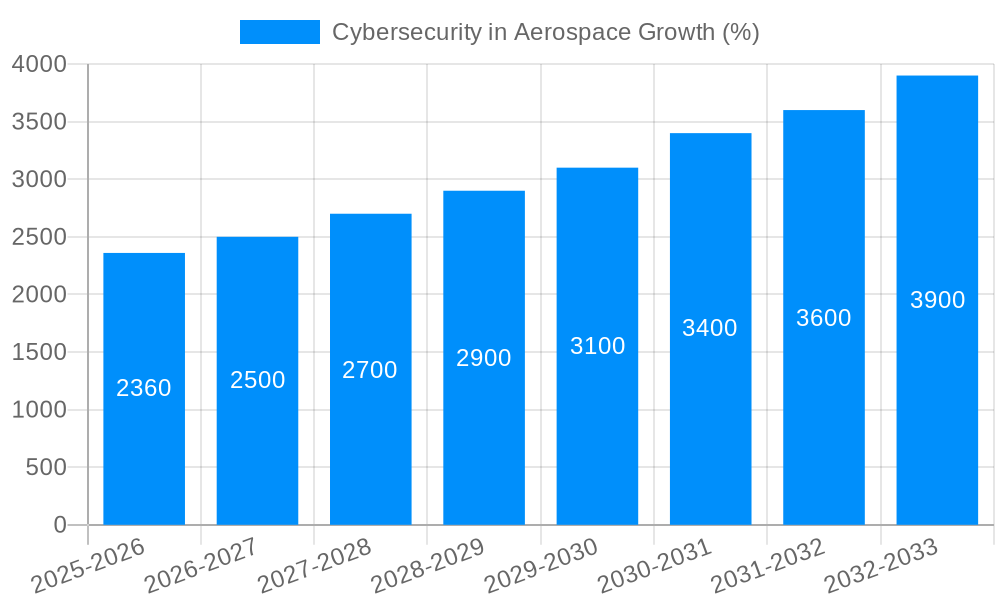

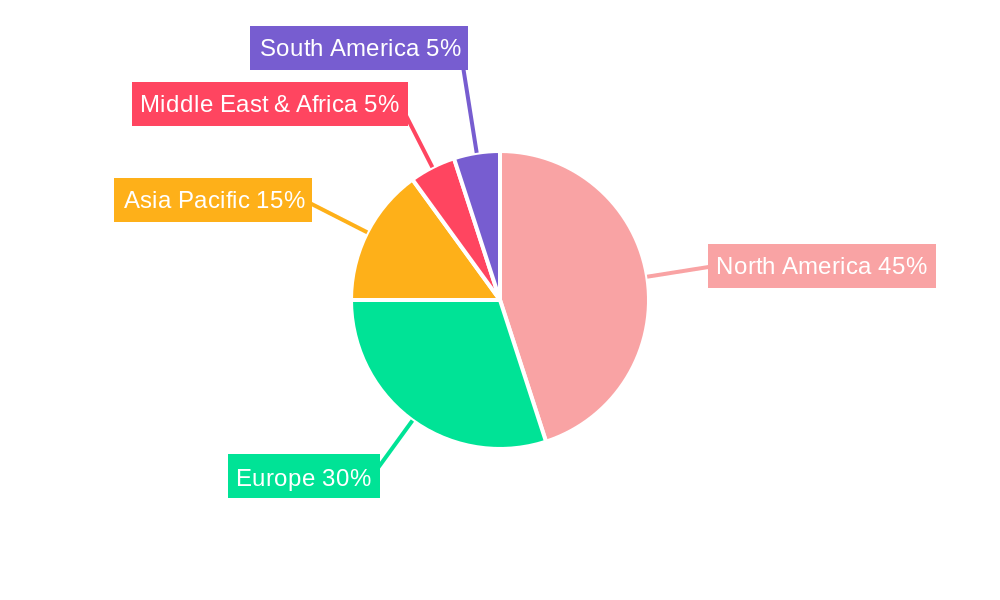

The aerospace cybersecurity market, currently valued at $51.04 billion (2025), is projected to experience robust growth with a compound annual growth rate (CAGR) of XX% during the forecast period (2025-2033). This expansion is fueled by several key drivers. The increasing reliance on interconnected systems within aircraft, from avionics and in-flight entertainment to air traffic management and maintenance systems, creates a vast attack surface vulnerable to cyber threats. The growing adoption of Internet of Things (IoT) devices within aerospace operations further exacerbates this vulnerability. Furthermore, stringent regulatory requirements concerning data security and operational safety, particularly from bodies like the FAA and EASA, are compelling companies to invest heavily in robust cybersecurity solutions. Key trends shaping the market include the rise of artificial intelligence (AI) and machine learning (ML) for threat detection and prevention, the increasing adoption of cloud-based security solutions for improved scalability and accessibility, and the growing focus on proactive threat intelligence and vulnerability management. However, the market faces certain restraints, including the high cost of implementation and maintenance of advanced cybersecurity systems, the complexity of integrating these systems into legacy infrastructure, and the skills gap in finding and retaining qualified cybersecurity professionals with specialized aerospace knowledge. Segmentation reveals a significant market across solutions (hardware, software) and services (consulting, managed security services), distributed across key application areas like avionics, in-flight entertainment, air traffic management, maintenance, supply chains, airport operations, and broader aerospace operations. Geographically, North America currently dominates the market, driven by advanced technological infrastructure and a strong regulatory framework. However, the Asia-Pacific region is expected to demonstrate significant growth in the coming years, fueled by rising air travel and investments in aerospace infrastructure.

Major players in this competitive market include established aerospace and defense companies like Boeing, Airbus, Lockheed Martin, Raytheon Technologies, and Northrop Grumman, alongside leading technology providers such as Cisco, IBM, Honeywell International, Thales Group, and Palo Alto Networks. These companies are engaged in strategic partnerships, mergers, and acquisitions to expand their market share and offer comprehensive cybersecurity solutions tailored to the unique needs of the aerospace industry. Smaller, specialized cybersecurity firms are also emerging, focusing on niche areas like threat intelligence, vulnerability assessment, and incident response. The competitive landscape is dynamic, characterized by continuous innovation in security technologies, evolving threat landscapes, and the need for adaptable and scalable solutions. The study period (2019-2033) and the base/estimated/forecast years provide a comprehensive view of market evolution, enabling informed strategic planning and investment decisions by stakeholders. Regional analysis, spanning North America, Europe, Asia-Pacific, and the Middle East & Africa, offers granular insights into market dynamics across various geographic locations. The ongoing integration of new technologies and the evolving threat environment will continue to shape the trajectory of the aerospace cybersecurity market over the long term.

The global cybersecurity in aerospace market is experiencing robust growth, projected to surpass $XX billion by 2030. This surge is driven by the increasing interconnectedness of aircraft systems, the proliferation of Internet of Things (IoT) devices within the aerospace ecosystem, and escalating concerns about cyberattacks targeting critical infrastructure. The market is witnessing a shift towards proactive security measures, moving beyond reactive incident response. This is evidenced by a significant increase in investments in advanced threat detection and prevention technologies, such as artificial intelligence (AI)-powered security analytics and blockchain-based solutions for secure data transmission. Furthermore, stringent regulatory compliance mandates, particularly within aviation safety standards, are compelling aerospace companies to prioritize cybersecurity investments. The market is also seeing a rise in the adoption of cloud-based security solutions to enhance scalability and cost-effectiveness. The integration of cybersecurity into the design phase of aircraft and related systems—a concept known as "security by design"—is gaining significant traction, ensuring robust protection from the outset. This trend is fueled by a growing understanding that mitigating cyber threats is not merely an operational cost but a strategic imperative for maintaining operational safety and upholding public trust. The market is also segmented into various service types, such as consulting, managed security services, and implementation services, each growing at a different pace depending on market demands. The adoption of these services varies greatly across different segments of the aerospace industry, with larger players typically investing more in comprehensive solutions. The development of new standards and protocols specifically designed for the aerospace industry further contributes to a more secure environment. This is crucial because legacy systems often lack the robust security features found in more modern technologies.

Several key factors are accelerating the growth of the cybersecurity in aerospace market. The increasing reliance on interconnected systems within modern aircraft, from avionics and in-flight entertainment to air traffic management, creates a larger attack surface, making robust cybersecurity essential. The growing sophistication of cyberattacks, ranging from data breaches to potentially catastrophic disruptions of flight operations, necessitates the adoption of advanced security measures. Stringent regulatory compliance requirements, imposed by organizations like the FAA and EASA, are pushing aerospace companies to invest heavily in cybersecurity solutions to meet compliance standards and avoid hefty penalties. The rising adoption of cloud-based services within the aerospace industry, while offering benefits in terms of scalability and cost-effectiveness, also presents new cybersecurity challenges that need to be addressed. The increasing use of IoT devices in aircraft and airports expands the attack surface and generates a massive volume of data that needs to be secured, requiring dedicated security solutions. Finally, the growing awareness among airlines and aerospace manufacturers of the potential financial and reputational damage from successful cyberattacks fuels a surge in investment in preventive measures. This overall increased focus on data privacy and security regulations globally further boosts demand for aerospace cybersecurity solutions.

Despite the significant growth potential, the cybersecurity in aerospace market faces several challenges. The legacy systems used in many aircraft and airport infrastructures often lack built-in security features, making them vulnerable to attacks. Upgrading these systems can be costly and complex, requiring significant investments and specialized expertise. The integration of various security solutions from different vendors can be difficult, leading to compatibility issues and potentially creating security gaps. Furthermore, the specialized nature of aerospace systems demands solutions tailored to the unique operational needs and safety standards of the industry. Finding skilled cybersecurity professionals with deep expertise in both aerospace systems and cybersecurity is a major hurdle, resulting in a talent shortage. The cost of implementing and maintaining advanced cybersecurity solutions can be substantial, especially for smaller airlines and aerospace companies. Maintaining regulatory compliance across diverse jurisdictions and evolving standards represents a significant operational challenge. Finally, the potential for disruption to air travel in the event of a successful cyberattack underlines the high stakes involved, making risk mitigation crucial. This complex ecosystem demands effective collaboration between stakeholders to achieve robust, holistic security.

The North American region currently holds a dominant position in the cybersecurity in aerospace market, driven by the presence of major aerospace manufacturers, a robust regulatory framework, and significant investments in cybersecurity infrastructure. Europe is another key market, characterized by a strong aerospace industry and stringent regulatory requirements. The Asia-Pacific region is witnessing rapid growth, fueled by increasing air travel and significant investments in airport modernization projects.

The aerospace sector faces unique cybersecurity challenges given its reliance on complex, interconnected systems, strict regulatory standards, and the potential for catastrophic consequences in case of a security breach. As such, investment in advanced solutions and services is crucial, with North America and Europe leading in terms of both adoption and innovation. The Asia-Pacific region is rapidly catching up, making it a crucial market to monitor. The focus is shifting toward proactive and preventive measures, integrated security solutions, and services that streamline compliance with ever-changing regulations.

Several factors are set to propel the growth of the cybersecurity in aerospace market. Increased adoption of cloud-based solutions in aircraft and airport operations will lead to an increased reliance on cloud security solutions. The growing number of Internet of Things (IoT) devices used in aircraft and airports will further stimulate growth in the industry. Expansion of the global aerospace industry, driven by the increasing demand for air travel, creates opportunities for companies providing cybersecurity services. Advancements in Artificial Intelligence (AI) and Machine Learning (ML) technologies offer enhanced capabilities for threat detection and prevention. Stringent government regulations regarding cybersecurity will drive companies to invest more in cybersecurity solutions to ensure compliance.

Recent significant developments include the increasing adoption of AI-powered threat detection systems, the rise of cloud-based security solutions, and a greater focus on "security by design" principles in the development of new aircraft and aerospace systems. Industry collaborations are also increasing, as companies recognize the importance of sharing threat intelligence and working together to develop better security standards. Several new regulations and compliance frameworks are also influencing the market, pushing companies to prioritize cybersecurity investments.

This report provides a comprehensive overview of the cybersecurity in aerospace market, analyzing key trends, driving forces, challenges, and growth opportunities. It profiles leading players in the industry, highlighting their strategic initiatives and market positions. The report also offers detailed insights into key market segments and geographical regions, providing valuable data-driven insights for companies operating in or seeking to enter this dynamic sector. The detailed analysis presented is crucial for stakeholders involved in understanding and mitigating cybersecurity risks within the aerospace industry, ensuring the continued safe and efficient operation of this critical sector.

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of XX% from 2019-2033 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately XX%.

Key companies in the market include Cisco, IBM, Raytheon Technologies, Northrop Grumman, Lockheed Martin Corp, Boeing, General Dynamics Corp, BAE Systems, Airbus, Leonardo S.p.A, Honeywell International, Thales Group, Collins Aerospace, Unisys, Palo Alto Networks, F-Secure, L3Harris Technologies, BluVector Inc, Qualys, Accenture, .

The market segments include Type, Application.

The market size is estimated to be USD 51040 million as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4480.00, USD 6720.00, and USD 8960.00 respectively.

The market size is provided in terms of value, measured in million.

Yes, the market keyword associated with the report is "Cybersecurity in Aerospace," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Cybersecurity in Aerospace, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.