1. What is the projected Compound Annual Growth Rate (CAGR) of the Cyber Security Technology in Telecom?

The projected CAGR is approximately XX%.

Cyber Security Technology in Telecom

Cyber Security Technology in TelecomCyber Security Technology in Telecom by Type (/> Device, Service, Sofware), by Application (/> SMEs, Large Enterprise), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2026-2034

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

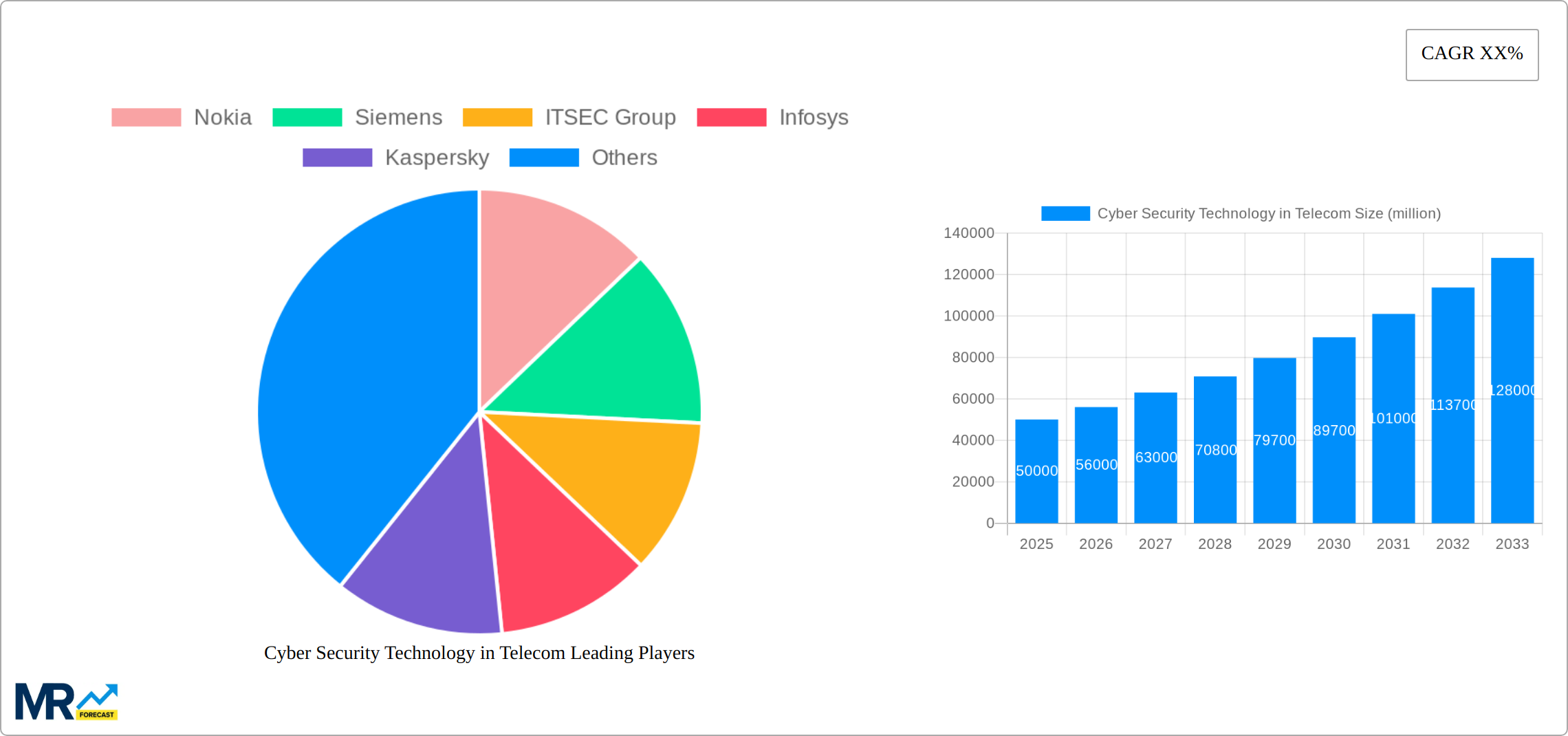

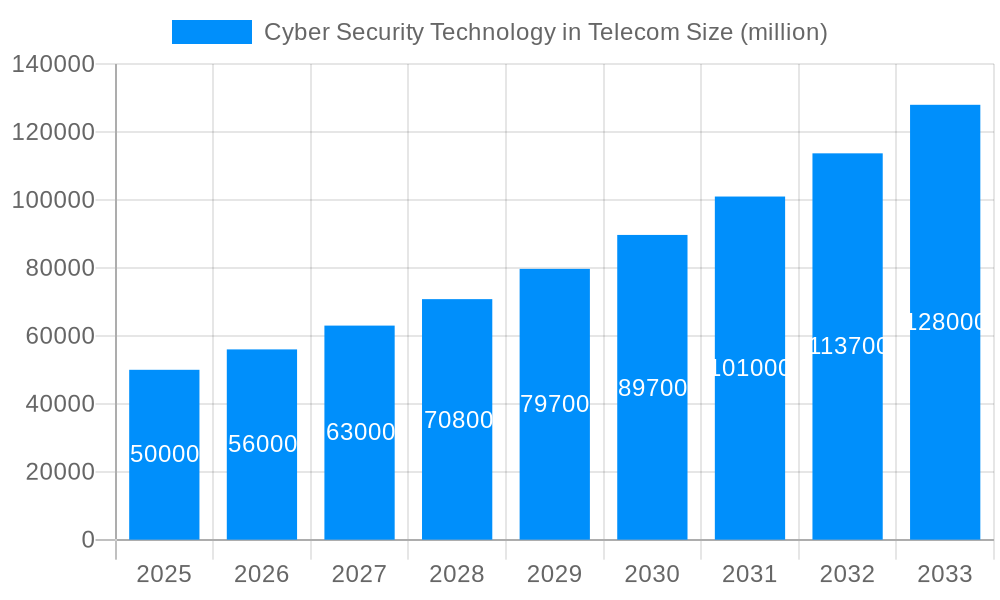

The global cybersecurity technology market within the telecom sector is experiencing robust growth, driven by the increasing reliance on digital infrastructure and the escalating sophistication of cyber threats targeting telecommunication networks. The market, estimated at $50 billion in 2025, is projected to exhibit a Compound Annual Growth Rate (CAGR) of 12% from 2025 to 2033, reaching approximately $150 billion by 2033. This expansion is fueled by several key factors: the surge in mobile data traffic and the Internet of Things (IoT) deployments, both significantly increasing the attack surface for telecom providers; the growing adoption of cloud-based services and network virtualization, which introduce new security challenges; and the rising regulatory pressure for enhanced data protection and compliance, necessitating significant investments in cybersecurity solutions. Major players like Nokia, Siemens, and Kaspersky are actively investing in research and development, and strategic partnerships are forming to enhance their offerings and cater to the growing demand.

The market segmentation reveals a strong focus on network security, data security, and endpoint security solutions. While North America and Europe currently hold the largest market share, Asia-Pacific is expected to experience the fastest growth due to increasing digitalization and infrastructure development. However, challenges remain, including the high cost of implementing advanced cybersecurity technologies, the shortage of skilled cybersecurity professionals, and the ever-evolving nature of cyber threats. The industry is navigating these complexities through advancements in artificial intelligence (AI) and machine learning (ML) to enhance threat detection and response capabilities, paving the way for more proactive and resilient security postures. Furthermore, collaborative efforts between telecom operators, cybersecurity vendors, and government agencies are becoming increasingly vital to effectively mitigate risks and safeguard critical telecommunications infrastructure.

The global cybersecurity technology market within the telecommunications sector is experiencing explosive growth, projected to reach hundreds of billions of dollars by 2033. The study period of 2019-2033 reveals a consistent upward trajectory, with the base year of 2025 serving as a pivotal point showcasing significant market maturation. The estimated market value for 2025 already indicates substantial investment and adoption of cybersecurity solutions across the telecom industry. This growth is fueled by the increasing reliance on interconnected networks, the proliferation of IoT devices, and the rising sophistication of cyber threats targeting telecom infrastructure. The forecast period (2025-2033) anticipates even more substantial growth driven by factors such as 5G deployment, cloud adoption, and the increasing regulatory pressure demanding robust cybersecurity measures. Analysis of the historical period (2019-2024) underscores the growing awareness of vulnerabilities and the resulting demand for advanced security solutions. This includes a shift towards proactive security measures, a move away from purely reactive responses to breaches, and a growing focus on AI-powered threat detection and response systems. Key market insights highlight a growing preference for comprehensive security solutions that offer a multi-layered approach to protection, encompassing network security, endpoint security, data security, and cloud security. The market is also witnessing a rise in managed security services, reflecting the increasing need for specialized expertise and ongoing security monitoring. Furthermore, the integration of cybersecurity solutions with network operations and orchestration platforms is becoming increasingly critical for efficient management and response. The convergence of IT and Operational Technology (OT) networks within the telecoms industry is driving demand for integrated security solutions that can effectively address the unique vulnerabilities of each environment. The total addressable market size is projected to exceed several hundred billion dollars by the end of the forecast period.

Several key factors are driving the rapid expansion of the cybersecurity technology market in the telecommunications sector. The widespread adoption of 5G networks significantly increases the attack surface, necessitating robust security measures to protect the expanded network infrastructure and the massive data volumes it handles. The exponential growth of the Internet of Things (IoT) introduces millions of new, often insecure, devices into telecom networks, creating vulnerabilities that need to be addressed by sophisticated security solutions. Cloud adoption, while offering scalability and flexibility, also presents new security challenges, requiring the implementation of advanced cloud security technologies to protect sensitive data and prevent breaches. Furthermore, stringent government regulations and industry standards, aimed at enhancing data protection and privacy, are compelling telecom operators to invest heavily in cybersecurity solutions to ensure compliance. The rising frequency and sophistication of cyberattacks targeting telecom infrastructure, resulting in substantial financial losses and reputational damage, are pushing companies to prioritize cybersecurity investments. Finally, the increasing reliance on data analytics and artificial intelligence (AI) for network optimization and security monitoring is driving the demand for advanced security solutions that can integrate with these technologies to enhance threat detection and response capabilities. The cumulative impact of these drivers creates a powerful impetus for substantial growth within the cybersecurity technology market within the telecommunications sector.

Despite the significant growth potential, the cybersecurity technology market in telecom faces certain challenges and restraints. The complexity of modern telecom networks makes implementing and managing comprehensive security solutions extremely difficult. The sheer scale and heterogeneity of these networks require highly specialized skills and expertise, leading to a shortage of qualified cybersecurity professionals. The high cost of deploying and maintaining advanced security solutions can be a significant barrier for smaller telecom operators, particularly in developing economies. Keeping up with the rapidly evolving threat landscape requires constant updates and upgrades to security systems, which can be expensive and time-consuming. Moreover, integrating new security solutions with existing legacy systems can be a complex and challenging process. The lack of interoperability between different security solutions from various vendors can also hinder effective security management. Concerns around data privacy and regulatory compliance add another layer of complexity to cybersecurity deployments. Finally, the increasing use of sophisticated cyberattacks employing AI and machine learning makes it more difficult for traditional security solutions to effectively mitigate threats. Overcoming these challenges requires collaborative efforts from industry stakeholders, governments, and regulatory bodies to develop effective strategies for enhancing cybersecurity in the telecommunications sector.

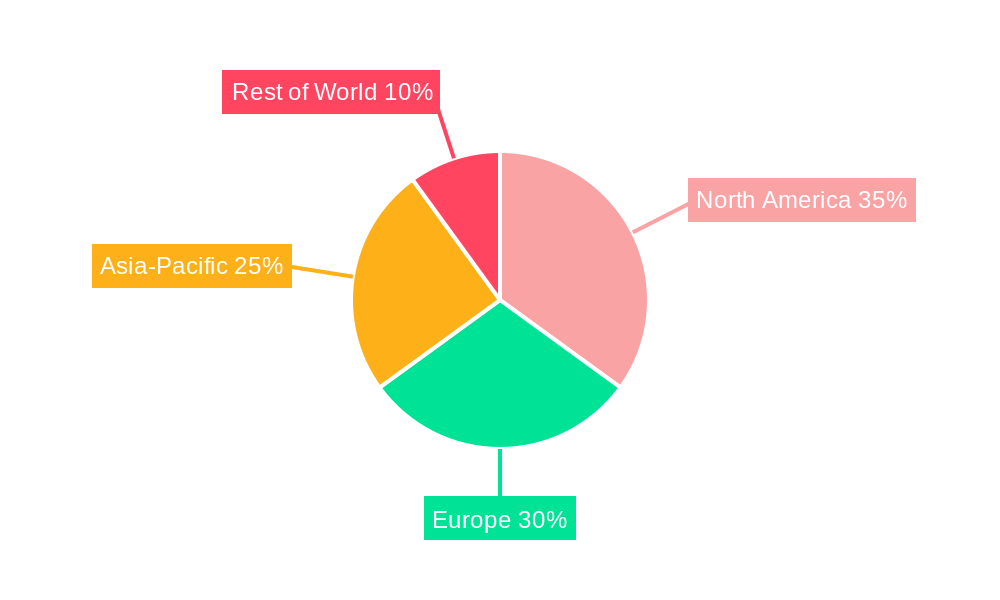

North America: The region is expected to hold a significant market share due to early adoption of advanced technologies, stringent regulatory environments driving security investments, and the presence of major telecom operators and technology companies. High levels of digitalization and robust technological infrastructure further propel market growth here. The significant presence of cybersecurity vendors in North America also fosters innovation and the development of advanced solutions.

Europe: Stringent data privacy regulations like GDPR are driving substantial investment in cybersecurity technologies within the European telecommunications sector. The region's well-established telecom infrastructure and a large number of telecom operators contribute to market growth. However, fragmentation of the market across different countries can pose challenges.

Asia-Pacific: Rapid technological advancements, a growing number of internet users, and significant investments in 5G infrastructure in countries like China, India, and Japan are expected to fuel strong market growth in this region. However, challenges related to cybersecurity awareness and skills gaps persist.

Segments: The managed security services segment is poised for significant growth, driven by the increasing need for specialized expertise and 24/7 monitoring of complex telecom networks. The network security segment is also a major contributor due to the critical importance of securing core network infrastructure against advanced threats. The cloud security segment will experience significant growth driven by the increasing adoption of cloud-based services by telecom operators. Furthermore, endpoint security solutions are gaining traction, reflecting the expanding ecosystem of endpoints within the telecom industry needing protection.

The overall market dominance will likely be shared among these regions, with North America and Europe potentially leading initially, followed by a rapid rise from the Asia-Pacific region due to its vast and rapidly expanding digital landscape. The specific segment dominance will depend on the pace of technological advancements and shifts in market priorities, with managed security services and network security expected to lead in the near term.

The increasing adoption of 5G, the expansion of IoT devices, and the growing use of cloud services are creating a massive demand for robust cybersecurity solutions. Government regulations mandating stronger data protection and privacy are also driving substantial investments in advanced security technologies. The rising sophistication of cyberattacks targeting telecom infrastructure further reinforces the need for enhanced security measures. These factors, combined with the continuous development of innovative security solutions, are creating a highly favorable environment for the growth of the cybersecurity technology market within the telecommunications sector.

This report provides a detailed analysis of the cybersecurity technology market in the telecom sector, covering market size, growth drivers, challenges, key players, and significant developments. It offers valuable insights for stakeholders, including telecom operators, cybersecurity vendors, investors, and regulatory bodies, enabling informed decision-making and strategic planning within this rapidly evolving market landscape. The analysis encompasses historical data, current market estimates, and future projections, offering a comprehensive perspective on the market's trajectory and opportunities.

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of XX% from 2020-2034 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately XX%.

Key companies in the market include Nokia, Siemens, ITSEC Group, Infosys, Kaspersky, Bitdefender, BAE Systems, GE Digital, Gamma, SecurityGen, Huntsman Security, Fortinet Security Fabric, Synopsys, .

The market segments include Type, Application.

The market size is estimated to be USD XXX million as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4480.00, USD 6720.00, and USD 8960.00 respectively.

The market size is provided in terms of value, measured in million.

Yes, the market keyword associated with the report is "Cyber Security Technology in Telecom," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Cyber Security Technology in Telecom, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.