1. What is the projected Compound Annual Growth Rate (CAGR) of the Cyber Risk Management Service?

The projected CAGR is approximately 8.3%.

Cyber Risk Management Service

Cyber Risk Management ServiceCyber Risk Management Service by Type (Human Error, Malicious Activity, System Vulnerabilities, Others), by Application (Large Enterprises, SMEs), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2026-2034

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

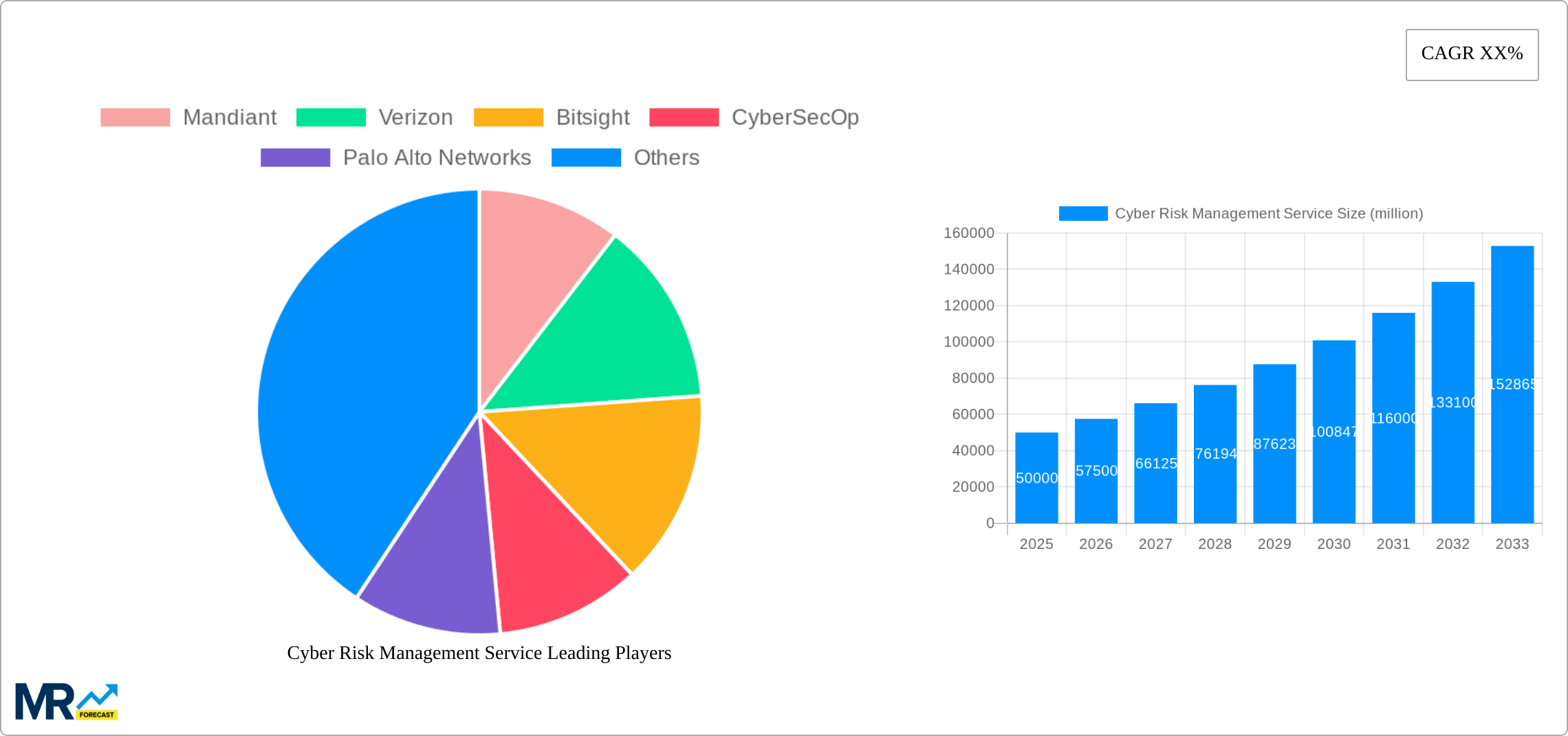

The global Cyber Risk Management (CRM) services market is experiencing robust growth, driven by the increasing frequency and sophistication of cyberattacks targeting both large enterprises and SMEs. The market, estimated at $20 billion in 2025, is projected to exhibit a Compound Annual Growth Rate (CAGR) of 15% from 2025 to 2033, reaching approximately $65 billion by 2033. This expansion is fueled by several key factors: the rising adoption of cloud computing and IoT devices, expanding regulatory compliance requirements (like GDPR and CCPA), and a growing awareness of the significant financial and reputational risks associated with cyber breaches. The market is segmented by the root cause of incidents (human error, malicious activity, system vulnerabilities, others) and by the size of the organizations served (large enterprises, SMEs). Large enterprises currently dominate the market due to their higher budgets and greater vulnerability to large-scale attacks, but the SME segment is showing significant growth potential as awareness increases and affordable solutions become more readily available. Key players in the market, including Mandiant, Verizon, and IBM Security, are actively innovating to provide comprehensive CRM services encompassing risk assessment, vulnerability management, incident response, and cybersecurity insurance.

The competitive landscape is characterized by a mix of established cybersecurity firms, specialized CRM providers, and consulting giants offering integrated services. While North America currently holds the largest market share due to early adoption and mature cybersecurity infrastructure, regions like Asia-Pacific and EMEA are exhibiting rapid growth, fueled by increasing digitalization and government initiatives to strengthen cybersecurity capabilities. However, restraints like skills shortages in cybersecurity professionals, the complexity of implementing effective CRM strategies, and the high cost of advanced security solutions pose challenges to market growth. Future market trends indicate an increasing focus on proactive risk mitigation, AI-powered security solutions, and the adoption of zero-trust security architectures. This will further shape the competitive landscape and fuel innovation in the years to come.

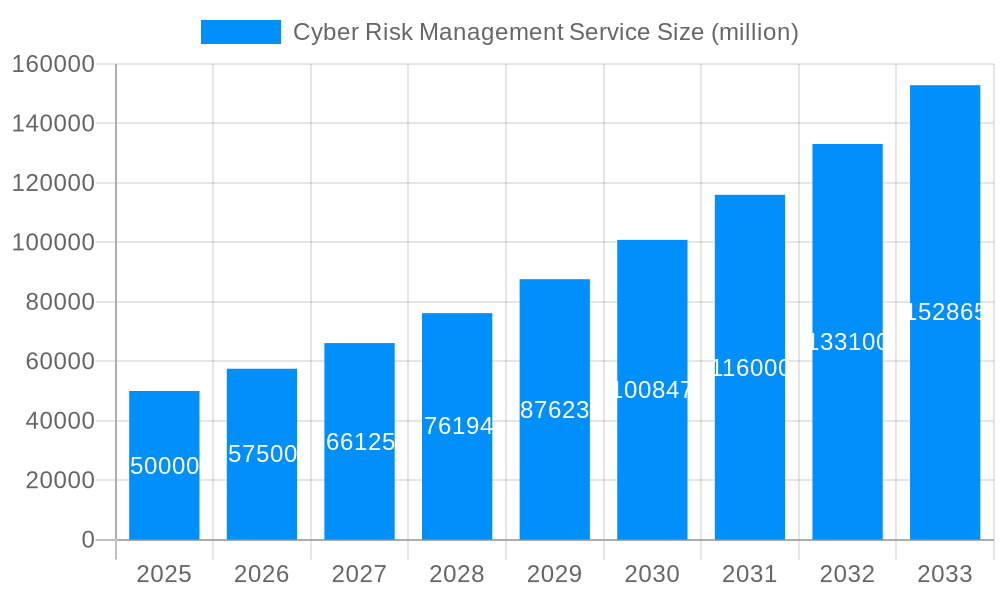

The global cyber risk management service market is experiencing explosive growth, projected to reach USD XXX million by 2033, up from USD XXX million in 2025. This represents a Compound Annual Growth Rate (CAGR) of X% during the forecast period (2025-2033). The historical period (2019-2024) witnessed a significant upswing driven by escalating cyber threats, stringent regulatory compliance mandates (like GDPR and CCPA), and the increasing reliance on digital infrastructure across all sectors. The market's expansion is fueled by several factors: the rising sophistication of cyberattacks, the increasing adoption of cloud computing and IoT devices (expanding attack surfaces), and a growing awareness among organizations of the potential financial and reputational damage from data breaches. Large enterprises are currently the primary drivers of market revenue, owing to their extensive IT infrastructure and higher vulnerability to large-scale attacks. However, SMEs are rapidly adopting cyber risk management solutions, recognizing the importance of protecting their sensitive data and operations. The market is witnessing a shift towards proactive and preventative strategies, with companies increasingly investing in threat intelligence, vulnerability management, and security awareness training. The rising adoption of AI and machine learning in cybersecurity solutions is also enhancing the effectiveness and efficiency of cyber risk management practices, further propelling market growth. Furthermore, the increasing demand for managed security service providers (MSSPs) is simplifying the complexities of cybersecurity for many businesses, allowing them to outsource these tasks to specialized companies. The market is segmented by type of threat (human error, malicious activity, system vulnerabilities, and others) and by application (large enterprises and SMEs), each exhibiting unique growth trajectories. Competition is intense, with a blend of established players and emerging niche providers vying for market share.

Several key factors are driving the expansion of the cyber risk management service market. The escalating frequency and severity of cyberattacks, ranging from ransomware attacks costing millions to sophisticated data breaches exposing sensitive customer information, are forcing organizations to prioritize cybersecurity investments. Government regulations and compliance mandates impose stringent requirements on data security, pushing organizations to implement robust cyber risk management programs to avoid hefty fines and reputational damage. The growing adoption of cloud computing and the Internet of Things (IoT) significantly expands the attack surface for organizations, demanding advanced cyber risk management solutions to mitigate these emerging vulnerabilities. Furthermore, the increasing interconnectedness of businesses and the reliance on third-party vendors necessitate comprehensive risk management strategies to address potential supply chain vulnerabilities. The rising awareness of cybersecurity risks among both businesses and consumers is leading to higher demand for security solutions and services. Organizations are increasingly recognizing that proactive cyber risk management is a cost-effective strategy compared to reactive incident response, resulting in heightened investment in preventive measures. Finally, the development and adoption of advanced technologies like AI and machine learning are providing more effective tools for threat detection and response, stimulating further market growth.

Despite the substantial growth potential, the cyber risk management service market faces several challenges. The ever-evolving nature of cyber threats necessitates continuous adaptation and innovation, requiring significant investment in research and development. The shortage of skilled cybersecurity professionals creates a bottleneck in the implementation and management of effective security solutions. This scarcity drives up labor costs and hinders the ability of some organizations to adequately address their cyber risk. Integrating various cybersecurity tools and technologies can be complex and time-consuming, creating challenges in establishing a cohesive and effective security posture. The cost of implementing and maintaining robust cyber risk management programs can be substantial, posing a significant barrier for smaller organizations with limited budgets. Furthermore, the difficulty in measuring the return on investment (ROI) for cybersecurity initiatives can make it challenging to justify spending to senior management. Finally, the lack of standardization in cyber risk management frameworks can lead to inconsistencies and inefficiencies across organizations. Addressing these challenges requires collaboration between industry stakeholders, government agencies, and educational institutions to develop and promote effective solutions.

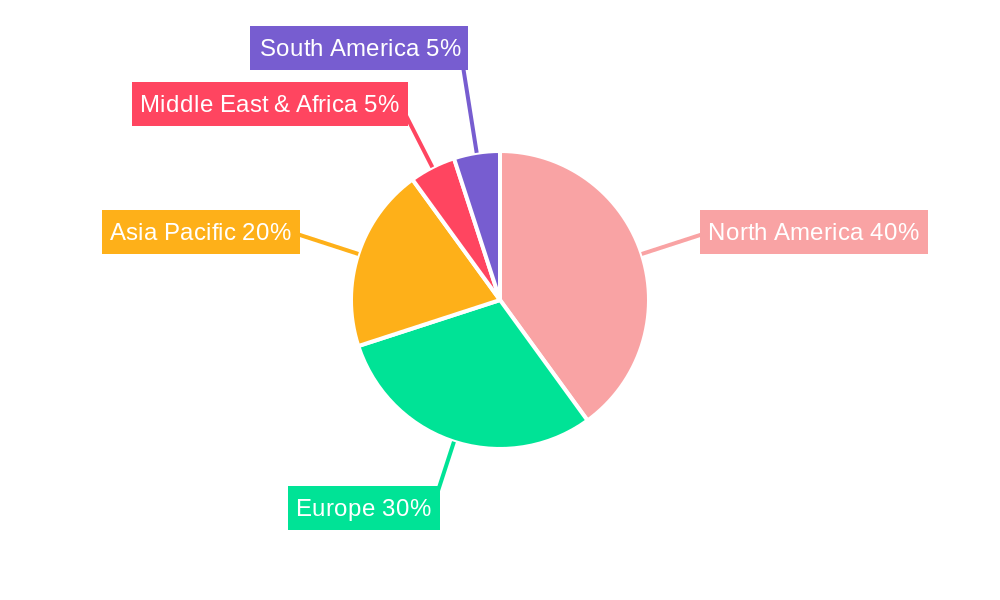

The North American market is projected to hold a significant share of the global cyber risk management services market during the forecast period. This dominance is largely attributable to the high concentration of technology companies, the early adoption of advanced security technologies, and the presence of stringent data protection regulations. The region is characterized by robust venture capital investment in cybersecurity startups and a mature market for cybersecurity services.

Large Enterprises: This segment is currently the major revenue contributor due to their extensive IT infrastructure and high vulnerability to sophisticated cyberattacks. Large enterprises have the financial resources to invest in comprehensive cyber risk management programs encompassing multiple layers of security. Their complex systems require sophisticated solutions for threat detection, incident response, and vulnerability management. The need for regulatory compliance further fuels the demand for these services within large enterprises.

Malicious Activity: This segment is expected to witness significant growth owing to the increasing sophistication and frequency of targeted attacks such as ransomware, phishing, and denial-of-service (DoS) attacks. Organizations are increasingly recognizing the need for proactive threat intelligence and incident response capabilities to mitigate the financial and reputational damage caused by malicious activities. The escalating costs associated with data breaches and recovery efforts further drive investment in this segment.

Europe, particularly Western Europe, is anticipated to exhibit substantial growth, driven by stricter data privacy regulations like GDPR and the rising adoption of cloud computing and IoT across various sectors. The Asia-Pacific region is also experiencing a rapid increase in demand, fueled by rapid economic growth and digital transformation, although it lags behind North America and Europe in terms of maturity. However, the growing awareness of cyber risks and increasing government investments in cybersecurity infrastructure are accelerating market expansion in this region.

The increasing adoption of cloud-based security solutions, the rising penetration of IoT devices, and the expansion of 5G networks are key catalysts for growth. Cloud-based solutions offer scalability and cost-effectiveness, while the proliferation of IoT devices necessitates robust security measures to protect against vulnerabilities. The advancements in AI and machine learning are significantly enhancing threat detection and response capabilities, leading to more effective cyber risk management. Stringent government regulations and compliance requirements are further driving demand for these services.

This report offers a comprehensive analysis of the cyber risk management service market, providing valuable insights into market trends, growth drivers, challenges, and key players. The detailed segmentation by threat type and application allows for a granular understanding of market dynamics. The forecast period projections provide a valuable tool for strategic decision-making, while the inclusion of key industry developments keeps readers informed of the latest advancements and trends in the sector. This report is essential for businesses, investors, and stakeholders seeking a deep understanding of this rapidly evolving market.

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 8.3% from 2020-2034 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately 8.3%.

Key companies in the market include Mandiant, Verizon, Bitsight, CyberSecOp, Palo Alto Networks, Gallagher, Imperva, IT Governance, Check Point, Marsh, IBM Security, ProWriters, Zurich, RiskLens, Aujas, LRQA Nettitude, Safe Security, Venable, Deloitte, WTW, NCC Group, Optiv, DXC, Zacco Digital Trust, EY, CyberClan, Night Lion Security, .

The market segments include Type, Application.

The market size is estimated to be USD XXX N/A as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3480.00, USD 5220.00, and USD 6960.00 respectively.

The market size is provided in terms of value, measured in N/A.

Yes, the market keyword associated with the report is "Cyber Risk Management Service," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Cyber Risk Management Service, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.