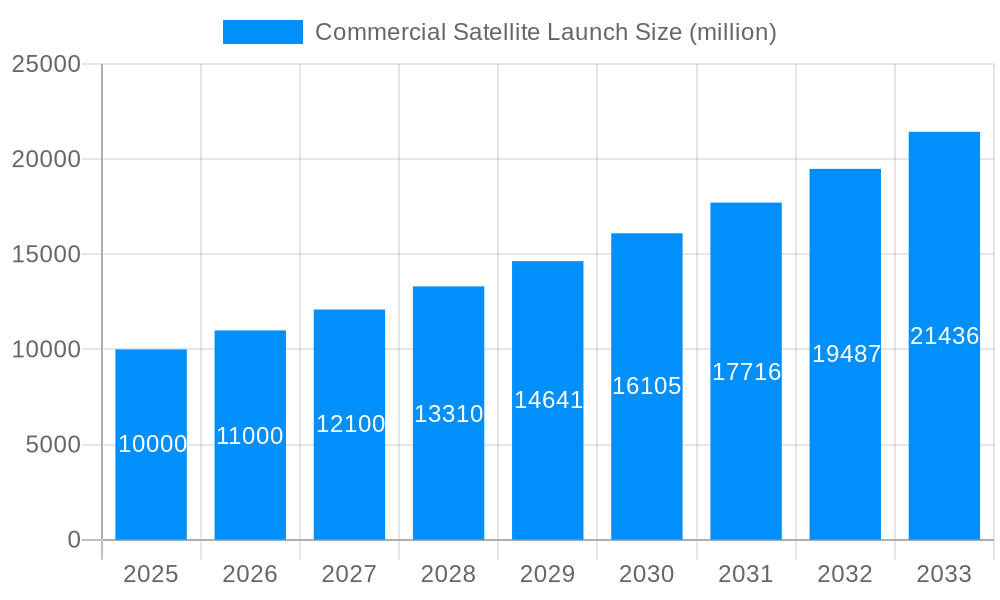

1. What is the projected Compound Annual Growth Rate (CAGR) of the Commercial Satellite Launch?

The projected CAGR is approximately 14.6%.

Commercial Satellite Launch

Commercial Satellite LaunchCommercial Satellite Launch by Type (/> GEO satellite, LEO satellite, Sun-synchronous satellite), by Application (/> Navigational satellite, Communication satellite, Reconnaissance satellite, Weather satellite, Remote sensing satellite), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2026-2034

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

The commercial satellite launch market is experiencing robust growth, driven by increasing demand for satellite-based services across various sectors. The miniaturization of satellites, coupled with the rise of constellations for applications like internet connectivity (e.g., Starlink), significantly contributes to this expansion. Furthermore, advancements in launch vehicle technology, including reusable rockets, are lowering launch costs and increasing launch frequency, making space more accessible. While regulatory hurdles and geopolitical factors can pose challenges, the overall market outlook remains positive, with a projected Compound Annual Growth Rate (CAGR) exceeding 10% (estimated based on typical growth in related technology sectors) through 2033. Key players like SpaceX, Lockheed Martin, Boeing, and Airbus are actively shaping the market landscape through innovation and strategic partnerships. The market is segmented by launch vehicle type (expendable vs. reusable), satellite type (communication, Earth observation, navigation), and geographic region.

North America currently holds a dominant market share, but Asia-Pacific is emerging as a significant growth area due to increasing government investments and private sector activity. The historical period (2019-2024) likely witnessed a gradual increase in market size, building momentum towards the stronger growth projected in the forecast period (2025-2033). This growth reflects a confluence of factors including decreasing launch costs, increased demand for various satellite applications (from Earth observation for environmental monitoring and agriculture to telecommunications for global connectivity), and the continued evolution of launch technologies. The competitive landscape is dynamic, with established aerospace giants and new entrants vying for market share. This competition further fuels innovation and drives down costs, benefiting the entire ecosystem.

The commercial satellite launch market experienced significant growth between 2019 and 2024, driven by increasing demand for satellite-based services across various sectors. The market's value soared, exceeding $XX billion in 2024, reflecting a Compound Annual Growth Rate (CAGR) of X%. This expansion is fueled by the burgeoning need for communication, navigation, Earth observation, and other applications reliant on satellite technology. The historical period (2019-2024) witnessed a rise in both the number of launches and the payload capacity deployed into orbit. Key market insights reveal a shift towards smaller, more frequent launches, driven by the increasing affordability and availability of smaller satellites. This trend is largely influenced by the advancements in miniaturization technology and the emergence of NewSpace companies. Furthermore, the rise of mega-constellations, such as SpaceX's Starlink, has had a profound impact, stimulating demand for launch services and reshaping the market landscape. Competition intensified during this period, with both established players and new entrants vying for market share. This competition has spurred innovation in launch vehicle technology, leading to more efficient and cost-effective launch solutions. The estimated market value for 2025 sits at $YY billion, indicating continued robust growth. The forecast period (2025-2033) anticipates a maintained CAGR of Y%, projecting a market valuation exceeding $ZZ billion by 2033. This projection underscores the market's sustained momentum and the increasing reliance on space-based technologies. The base year for this analysis is 2025. The study period covers 2019-2033, providing a comprehensive overview of the market’s evolution and future trajectory.

Several factors are accelerating the growth of the commercial satellite launch market. The increasing affordability of satellite technology is a primary driver, making it accessible to a broader range of users, including private companies and governments with smaller budgets. Simultaneously, the demand for high-bandwidth internet access, particularly in underserved regions, is fueling the development and deployment of massive satellite constellations, directly impacting the launch market. Advancements in launch vehicle technology, leading to increased reliability and reduced launch costs, are also significantly contributing to this growth. Furthermore, the burgeoning space tourism sector and the increasing interest in space exploration, beyond governmental initiatives, contribute to the rising demand for launch services. Governmental support and initiatives aimed at fostering innovation and competition within the space industry are instrumental in creating a conducive environment for growth. This includes both direct funding for space programs and policies that encourage private sector participation. Finally, the growing need for Earth observation data for applications such as environmental monitoring, agriculture, and disaster management further solidifies the market's expansion.

Despite the significant growth, the commercial satellite launch market faces considerable challenges. One major hurdle is the high initial investment required for developing and deploying new launch vehicles and infrastructure. This financial barrier often restricts entry for smaller companies and can lead to market consolidation. Regulatory complexities and international space law also present challenges, particularly regarding licensing, orbital debris management, and the allocation of orbital slots. The inherent risks associated with space launches, including potential launch failures and payload loss, pose significant financial and reputational risks for launch providers and their clients. Furthermore, competition is intense, with established players and innovative newcomers vying for market share. This competition necessitates continuous innovation and cost optimization to remain competitive. Finally, geopolitical factors and international relations can influence the market, potentially impacting launch site availability and access to key technologies.

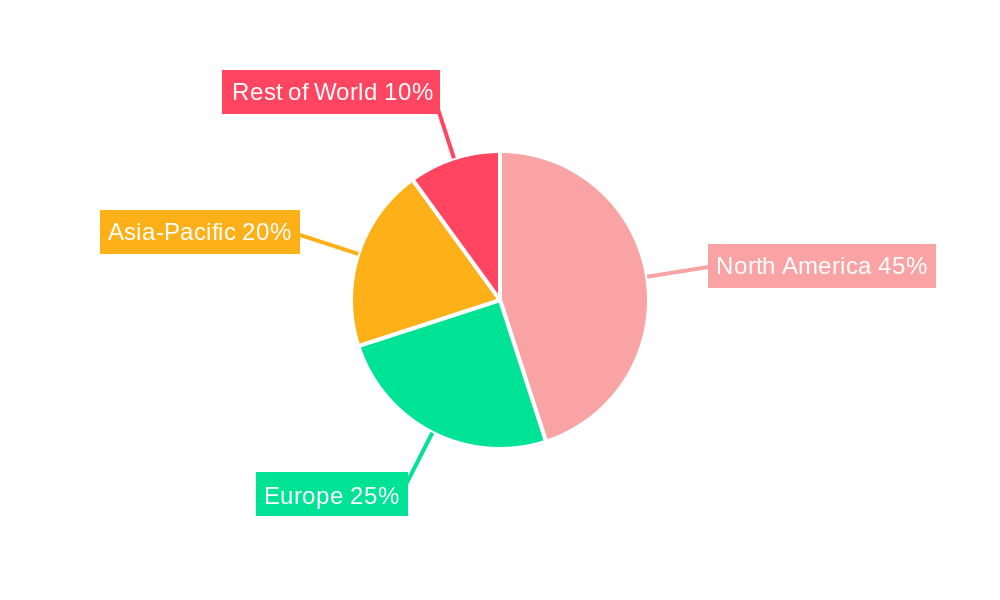

The commercial satellite launch market is geographically diverse, with significant contributions from several key regions and countries.

North America: The United States dominates this segment, holding a substantial share due to the presence of major players like SpaceX, Boeing, and Lockheed Martin, along with a robust and well-established space infrastructure. This region benefits from strong government support and a thriving private sector.

Europe: Europe, particularly through the efforts of Arianespace and Airbus, contributes significantly, offering a range of launch services and boasting expertise in satellite technology. The European Space Agency (ESA) also plays a crucial role in supporting and fostering growth within the region.

Asia: The Asia-Pacific region is witnessing rapid growth, with countries like China and India investing heavily in their space programs and developing indigenous launch capabilities. This region is poised for significant expansion in the coming years.

Segments:

Launch Vehicle Type: The market encompasses a diverse range of launch vehicles, from small-lift launchers suited for deploying small satellites to heavy-lift vehicles capable of carrying larger payloads. The trend towards smaller, more frequent launches is driving growth in the small-lift segment. The demand for heavy-lift vehicles remains substantial, however, particularly for large communication satellites and interplanetary missions.

Satellite Type: The market caters to various satellite types, including communication satellites, Earth observation satellites, navigation satellites, and scientific satellites. The growth of mega-constellations is significantly boosting the demand for launches accommodating multiple small satellites. The demand for high-resolution Earth observation satellites is also driving market growth.

The combined effect of these regional and segmental drivers indicates continued expansion for the foreseeable future, with North America maintaining a leading position while Asia-Pacific and other regions rapidly gain traction.

The convergence of several factors propels the commercial satellite launch industry's growth. The decreasing cost of launch services, coupled with miniaturization advancements in satellite technology, makes space-based solutions more accessible. This accessibility fuels the demand for diverse applications, from global internet connectivity to advanced Earth observation and environmental monitoring. Governmental policies promoting commercial space exploration further incentivize private investments and drive innovation within the sector. The increasing awareness of the importance of space-based technologies across various sectors, including agriculture, telecommunications, and defense, further stimulates market expansion.

This report offers a detailed analysis of the commercial satellite launch market, providing valuable insights into market trends, driving forces, challenges, key players, and future prospects. The comprehensive nature of this report makes it an invaluable resource for businesses, investors, and policymakers seeking to understand the dynamics and growth potential of this dynamic sector. The in-depth analysis of market segments, key players, and regional trends allows for informed decision-making and strategic planning. Furthermore, the report’s forecast offers a perspective on the future trajectory of the market, aiding in long-term strategic planning.

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 14.6% from 2020-2034 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately 14.6%.

Key companies in the market include Space Exploration Technologies Corp., Lockheed Martin Corporation, Boeing, Orbital ATK, Inc., Airbus S.A.S., Arianespace SA, Axelspace Corporation, .

The market segments include Type, Application.

The market size is estimated to be USD 8.2 billion as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4480.00, USD 6720.00, and USD 8960.00 respectively.

The market size is provided in terms of value, measured in billion.

Yes, the market keyword associated with the report is "Commercial Satellite Launch," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Commercial Satellite Launch, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.