1. What is the projected Compound Annual Growth Rate (CAGR) of the Commercial Launch Service?

The projected CAGR is approximately 16.41%.

Commercial Launch Service

Commercial Launch ServiceCommercial Launch Service by Type (Solid Launch Vehicle, Liquid Launch Vehicle, Solid-liquid Hybrid Launch Vehicle), by Application (Satellite Manufacturer, Satellite Operator, Others), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2026-2034

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

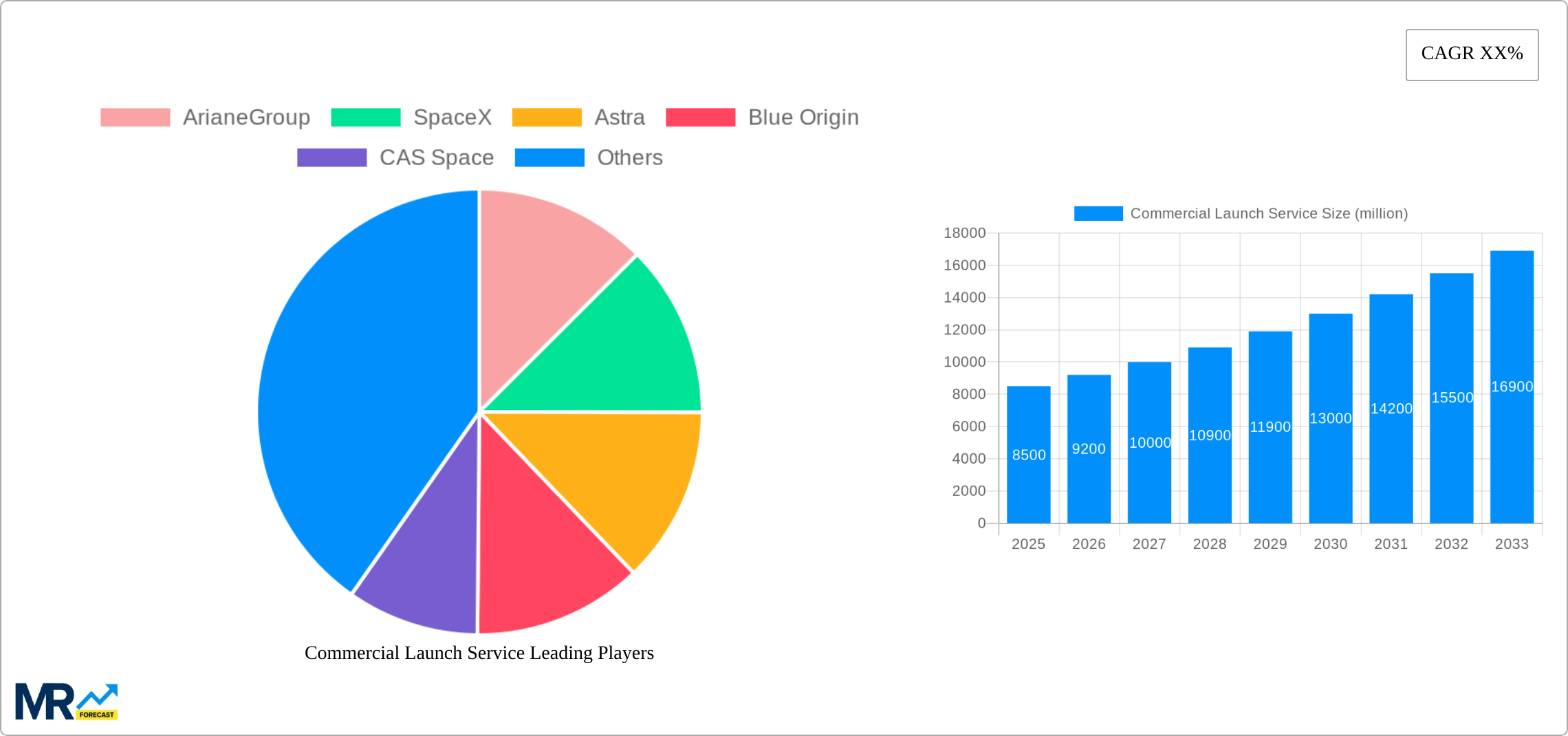

The commercial launch services market is experiencing robust growth, driven by increasing demand for satellite launches from both government and commercial entities. The miniaturization of satellites, coupled with the rise of constellations for various applications like Earth observation, communication, and navigation, is fueling this expansion. While solid launch vehicles currently dominate the market due to their lower cost and reliability for smaller payloads, liquid launch vehicles are gaining traction for heavier payloads and greater flexibility. The emergence of reusable launch systems from companies like SpaceX is significantly lowering launch costs, further stimulating market growth. Hybrid launch vehicles represent a promising technology blending the advantages of both solid and liquid propulsion systems, offering potential for improved performance and cost-effectiveness in the future. Competition is intense, with established players like ArianeGroup and United Launch Alliance facing pressure from innovative newcomers like SpaceX, Rocket Lab, and Relativity Space. This competitive landscape is pushing technological advancements and driving down prices, benefitting customers and accelerating market expansion. Geographical distribution reveals a strong presence in North America and Europe, but Asia-Pacific is witnessing rapid growth fueled by increasing domestic space programs in countries like China and India. Over the forecast period (2025-2033), continued technological innovation, falling launch costs, and burgeoning demand for satellite services will collectively contribute to sustained market expansion.

This growth, however, faces certain challenges. Regulatory hurdles, particularly concerning licensing and safety standards, can create complexities for launch providers. The inherent risks associated with space travel and the need for stringent safety protocols also represent a constraint. Furthermore, fluctuations in the global economy can impact investment in the space sector, potentially slowing down growth in certain periods. Despite these restraints, the long-term outlook for the commercial launch services market remains positive, with projections indicating considerable expansion over the next decade. The strategic partnerships forming between launch providers and satellite manufacturers/operators are expected to further enhance the market's trajectory. The ongoing quest for greater efficiency, sustainability, and cost reduction in launch operations will remain a key driver of market innovation and competitive advantage.

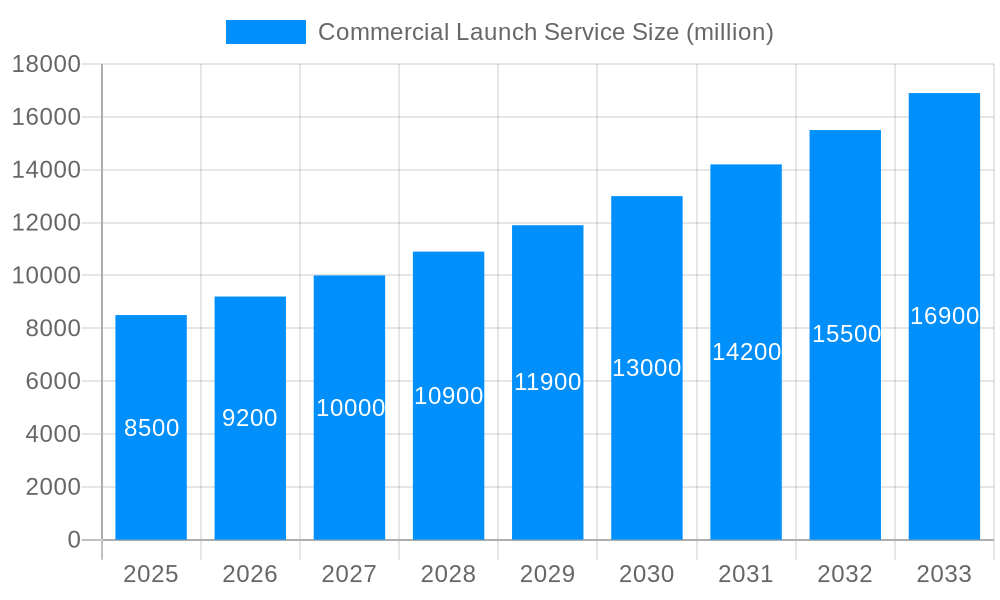

The global commercial launch service market is experiencing a period of unprecedented growth, driven by a confluence of factors including the burgeoning demand for satellite-based services, advancements in launch vehicle technology, and the emergence of new spacefaring nations. Over the study period (2019-2033), the market witnessed a significant expansion, with the estimated market value in 2025 exceeding $XX billion. This robust growth trajectory is projected to continue throughout the forecast period (2025-2033), exceeding $YY billion by 2033. Key market insights reveal a shift towards smaller, more frequent launches, catering to the increasing demand for constellations of small satellites. This trend is fueled by the rise of the NewSpace industry, characterized by agile, innovative companies disrupting the traditional space launch landscape. The market is also witnessing increasing competition, with both established players and new entrants vying for market share. This competitive environment is driving innovation and pushing down launch costs, making space access more affordable for a wider range of customers. Furthermore, the rising focus on sustainability and reusability is shaping the future of the industry, as companies strive to reduce environmental impact and enhance cost-effectiveness. The historical period (2019-2024) showcased significant advancements in launch technologies, paving the way for the rapid growth predicted in the coming years. The base year for this analysis is 2025, providing a robust foundation for future projections. Government support for space exploration and the increasing commercialization of space activities further contribute to this thriving ecosystem.

Several key factors are propelling the growth of the commercial launch service market. The increasing demand for satellite-based services, such as broadband internet, navigation, and Earth observation, is a primary driver. This demand fuels the need for more frequent and cost-effective satellite launches. Technological advancements in launch vehicle design, particularly the development of reusable rockets and smaller, more adaptable launch systems, are significantly reducing launch costs and increasing launch frequency. The emergence of NewSpace companies, characterized by their innovative approaches and agility, is disrupting the traditional market landscape, driving competition and innovation. Furthermore, government initiatives and supportive regulatory frameworks in various countries are encouraging private sector investment in space exploration and commercialization, further stimulating market growth. Finally, the decreasing cost of satellite technology itself makes deploying multiple small satellites more economically feasible, leading to a surge in demand for launch services. The overall effect of these converging trends is a dynamic and rapidly expanding market with significant potential for future growth.

Despite the significant growth opportunities, several challenges and restraints hinder the commercial launch service market. High launch costs, even with advancements in technology, remain a significant barrier for smaller companies and research institutions. The complexity and inherent risks associated with spaceflight, including potential launch failures, pose financial and reputational risks to launch providers and their clients. The competitive landscape, while driving innovation, also creates a challenging environment for new entrants to secure market share and achieve profitability. Regulatory hurdles and licensing requirements can add complexities and delays to launch operations. Furthermore, concerns related to space debris and the sustainability of launch activities are gaining importance, demanding a more responsible approach from industry players. Addressing these challenges requires collaboration among stakeholders, including governments, industry players, and international organizations, to foster a sustainable and commercially viable space launch sector. Finally, securing adequate funding for research and development remains crucial for sustaining innovation in this highly capital-intensive industry.

The Satellite Operator segment is poised for significant growth within the commercial launch service market. This segment's dominance is driven by the explosive growth of satellite constellations for various applications, including broadband internet, Earth observation, and navigation. The increasing reliance on satellite-based services across multiple sectors, from telecommunications to defense, fuels the demand for launch services specifically aimed at deploying operational satellites for these operators.

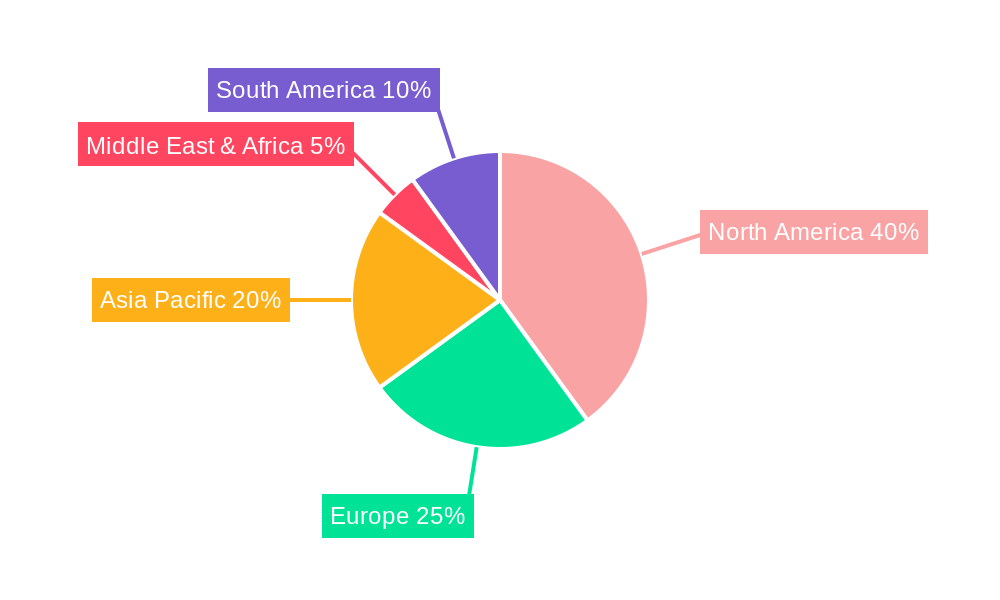

North America: The United States holds a strong position in the market, thanks to a robust private space sector and government support for space exploration. The presence of major players like SpaceX, Blue Origin, and United Launch Alliance, alongside a supportive regulatory environment, contributes significantly to North America's dominance.

Europe: While the European market is smaller compared to North America, it's characterized by strong government investment and established launch providers like ArianeGroup. This region is expected to see sustained growth, driven by government initiatives and participation in collaborative space programs.

Asia-Pacific: This region is emerging as a major player, with significant government investment driving development in launch capabilities. Companies like CASC and i-Space are contributing to growth in the region, albeit with a somewhat slower pace compared to North America. However, the rapid expansion of the satellite industry within Asia-Pacific promises substantial growth for this region in the future.

The liquid launch vehicle segment is also expected to retain a significant market share, driven by its versatility and ability to deliver heavier payloads to various orbits. While solid launch vehicles offer simplicity and cost-effectiveness for smaller payloads, the flexibility of liquid launch vehicles makes them indispensable for a large proportion of satellite deployments. The increasing need for precise orbit placement and larger payload capacity favors liquid launch vehicle usage. Hybrid launch vehicles are also gaining ground, showcasing a balance between cost-effectiveness and performance, attracting investors and customers seeking a balance between the two.

Several factors are catalyzing growth in the commercial launch service industry. The decreasing cost of satellite technology, coupled with the rising demand for satellite-based services, fuels the need for more frequent and cost-effective launches. Technological innovations in reusable rockets and smaller, more flexible launch vehicles are making space access more affordable and accessible. Government support and favorable regulatory environments are encouraging private sector investment and fostering a vibrant ecosystem. The growing interest in space exploration and commercial activities, along with the increase in private investment, further propels market growth.

This report provides a comprehensive overview of the commercial launch service market, analyzing historical trends, current market dynamics, and future growth prospects. It covers key players, technological advancements, and regional variations, offering valuable insights for businesses and investors in the space sector. The report's in-depth analysis of market segments, along with its detailed forecast, provides a solid foundation for strategic decision-making. This report effectively bridges the gap between current market dynamics and future projections, enabling informed investment decisions and strategic planning.

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 16.41% from 2020-2034 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately 16.41%.

Key companies in the market include ArianeGroup, SpaceX, Astra, Blue Origin, CAS Space, CASC, Evolution Space, Firefly Aerospace, GK Launch Services, International Launch Services, LANDSPACE, Mitsubishi Heavy Industries, Northrop Grumman, HyImpulse, SPACE ONE, PLD Space, Relativity Space, Rocket Factory Augsburg, Rocket Lab, Starsem, Stoke Space, United Launch Alliance, Up Aerospace, Virgin Galactic, OneSpace, i-Space, Galactic Energy, Beijing Space Trek, Deep Blue Aerospace, Antrix Corporation, .

The market segments include Type, Application.

The market size is estimated to be USD XXX N/A as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4480.00, USD 6720.00, and USD 8960.00 respectively.

The market size is provided in terms of value, measured in N/A.

Yes, the market keyword associated with the report is "Commercial Launch Service," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Commercial Launch Service, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.