1. What is the projected Compound Annual Growth Rate (CAGR) of the Clustering Software?

The projected CAGR is approximately 3.2%.

Clustering Software

Clustering SoftwareClustering Software by Type (Windows, Linux and Unix, Others), by Application (Small & Medium businesses, Enterprises), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2026-2034

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

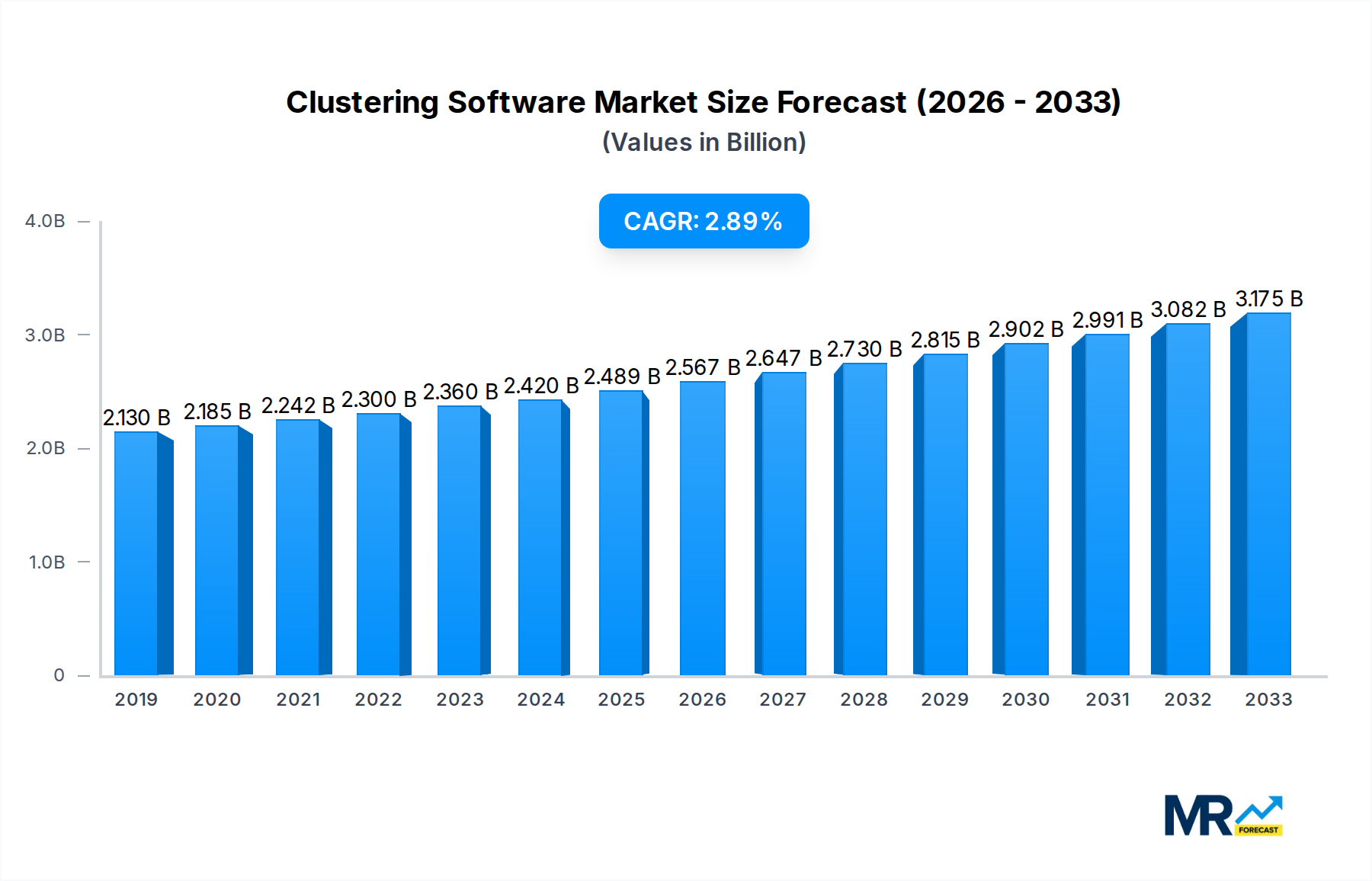

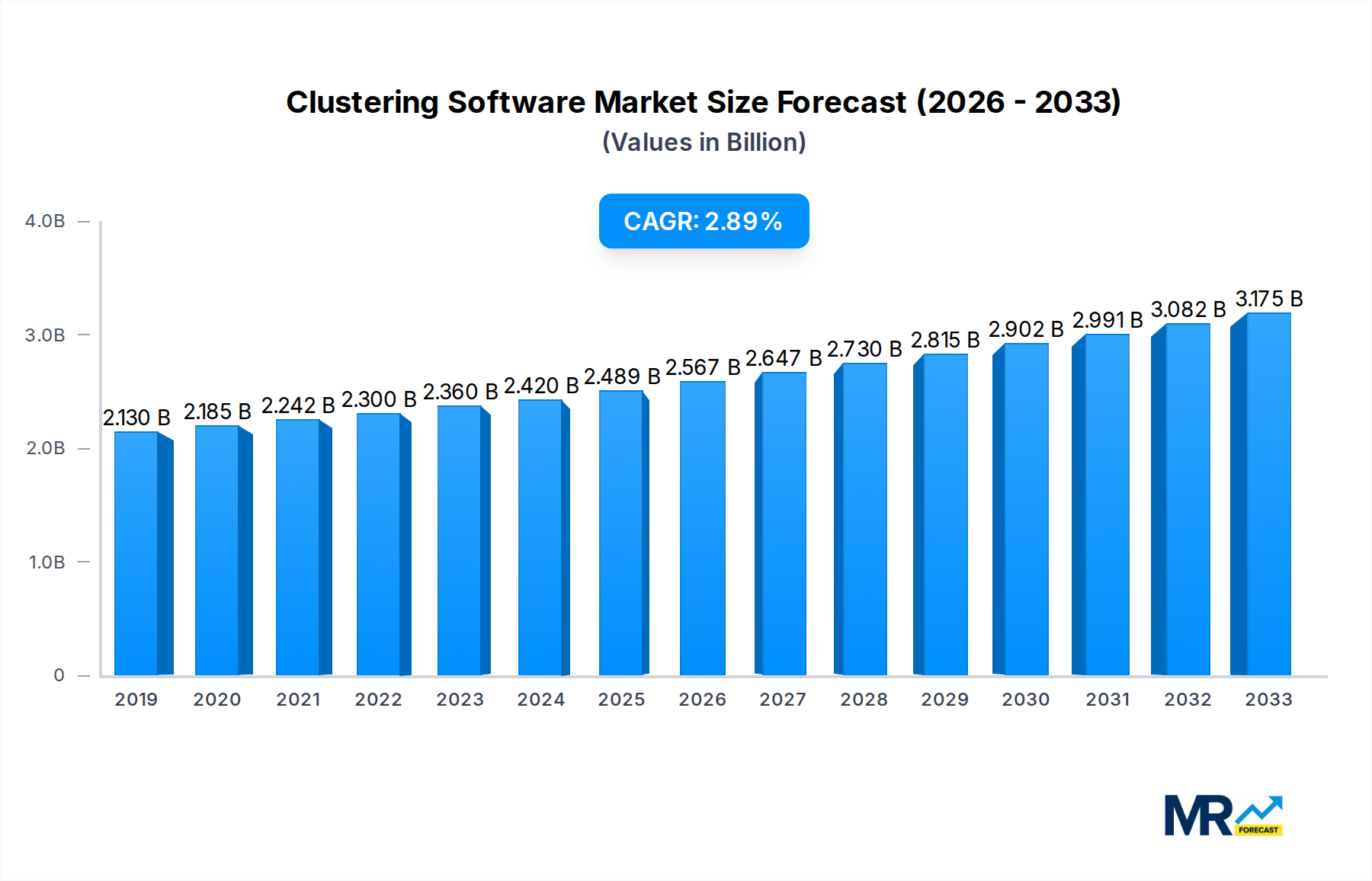

The global Clustering Software market is poised for steady growth, with an estimated market size of USD 2488.7 million in 2025 and a projected Compound Annual Growth Rate (CAGR) of 3.2% extending through 2033. This robust expansion is underpinned by the increasing demand for high availability, improved performance, and enhanced scalability across various industries. Organizations are increasingly adopting clustering solutions to ensure continuous operation of critical applications and to manage large volumes of data efficiently. The trend towards big data analytics, artificial intelligence, and machine learning further fuels this demand, as these technologies often require significant computational power that can be effectively distributed and managed through clustering. Furthermore, the growing adoption of cloud computing and hybrid cloud environments is creating new opportunities for clustering software, enabling seamless resource management and application deployment across distributed infrastructures.

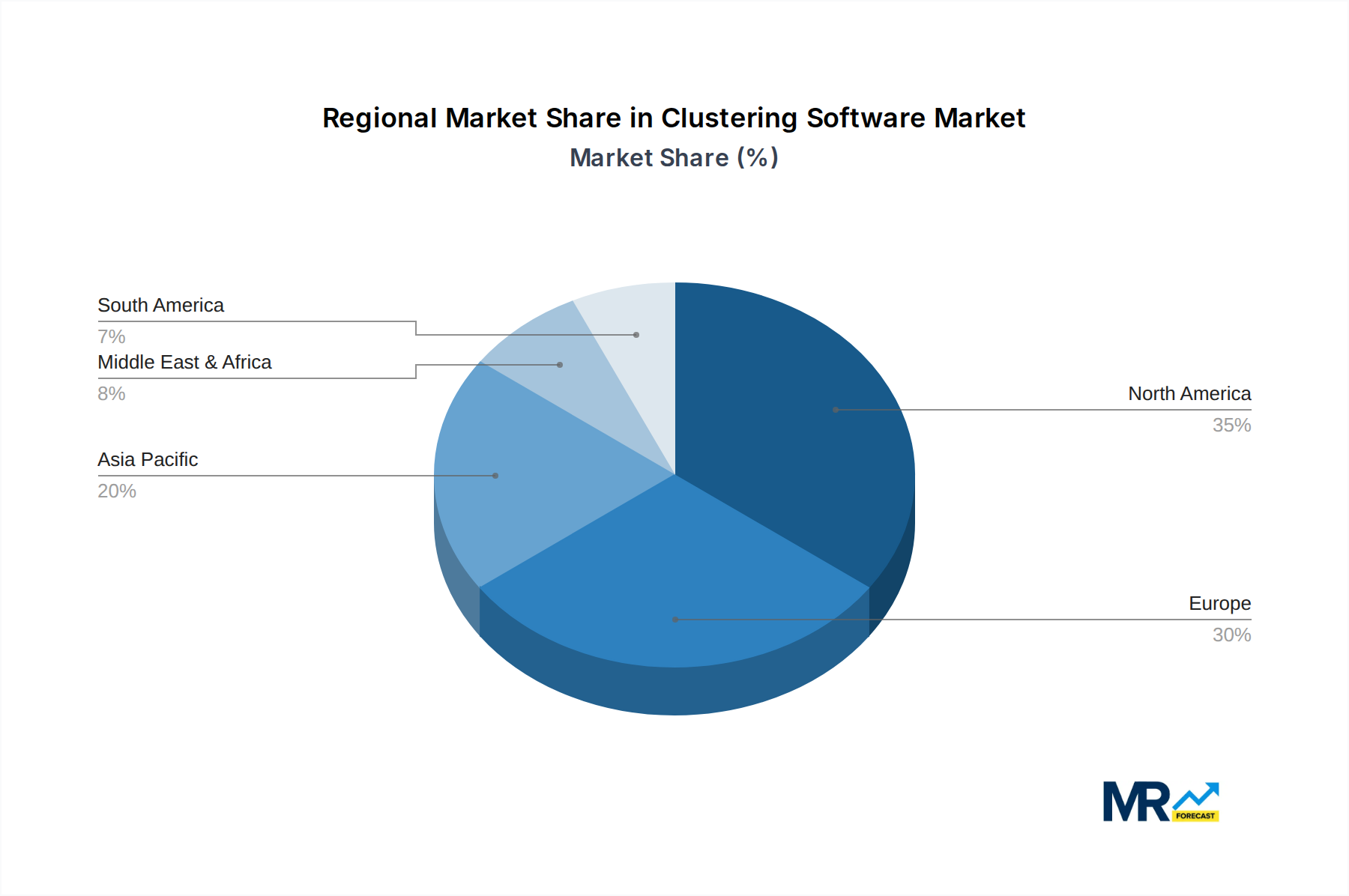

The market is segmented by type and application, with "Linux and Unix" and "Windows" expected to dominate the type segment due to their widespread adoption in enterprise environments. In terms of applications, both "Small & Medium businesses" and "Enterprises" are significant contributors, with enterprises, in particular, driving demand for advanced clustering features to support complex workloads and mission-critical operations. Key players such as Microsoft, IBM, Oracle, and Red Hat are actively innovating, introducing advanced features like enhanced fault tolerance, simplified management, and tighter integration with cloud platforms. Geographical analysis indicates that North America and Europe are leading markets, driven by early adoption of advanced technologies and a strong presence of IT infrastructure. However, the Asia Pacific region is anticipated to witness the fastest growth, fueled by rapid digital transformation initiatives and increasing investments in IT infrastructure by businesses of all sizes.

This report delves into the multifaceted world of clustering software, a critical technology underpinning modern IT infrastructure. We offer an in-depth analysis of market trends, driving forces, challenges, and future projections within this dynamic sector. Our comprehensive research spans the Historical Period (2019-2024), utilizing 2025 as the Base Year and Estimated Year, and projecting growth through the Forecast Period (2025-2033), all within a detailed Study Period of 2019-2033. Expect granular insights into the market's evolution, valued in the millions of USD.

The global clustering software market is experiencing a period of robust expansion, driven by the increasing demand for high availability, fault tolerance, and enhanced performance across diverse business applications. The market size, estimated at USD 18,500 million in 2025, is poised for significant growth, projected to reach an impressive USD 42,000 million by 2033, exhibiting a compound annual growth rate (CAGR) of approximately 10.5% during the Forecast Period (2025-2033). This upward trajectory is largely attributed to the pervasive adoption of cloud computing, big data analytics, and mission-critical applications that necessitate uninterrupted operation. As businesses across all scales increasingly recognize the strategic importance of resilient IT systems, the investment in sophisticated clustering solutions is accelerating. The evolution of clustering technologies, moving from basic failover mechanisms to advanced active-active configurations and hyper-converged infrastructure, further fuels this market. The growing complexity of IT environments, coupled with the ever-present threat of downtime, compels organizations to seek out solutions that can ensure business continuity and minimize operational disruptions. Furthermore, the rise of containerization and microservices architectures, while presenting new avenues for distributed computing, also amplifies the need for robust orchestration and clustering capabilities to manage these dynamic workloads effectively. The market is witnessing a shift towards software-defined clustering, offering greater flexibility and cost-efficiency compared to traditional hardware-centric approaches. This trend is particularly evident in the Linux and Unix segment, which is projected to hold a substantial market share throughout the forecast period, owing to its open-source nature, scalability, and cost-effectiveness for enterprise deployments. Similarly, the Enterprises segment represents a major revenue contributor, as large organizations invest heavily in high-performance computing and disaster recovery solutions. The increasing sophistication of cyber threats also drives the demand for clustered systems that can maintain operational integrity even under duress. Innovations in areas such as distributed databases, high-performance computing (HPC) clusters, and web server load balancing are continuously expanding the application landscape for clustering software, ensuring its continued relevance and growth.

The clustering software market is experiencing a significant surge, propelled by an undeniable need for enhanced IT resilience and operational efficiency. The increasing reliance on digital infrastructure for core business functions, from e-commerce platforms and financial transactions to scientific research and critical healthcare services, has made downtime an unacceptable risk. Consequently, businesses are investing heavily in clustering software to ensure high availability and fault tolerance, guaranteeing uninterrupted access to essential applications and data. This drive for continuous operation is further amplified by the burgeoning adoption of cloud computing and hybrid cloud environments, where distributed workloads and the management of multiple interconnected resources necessitate sophisticated clustering solutions. Big data analytics and the ever-growing volume of data generated by businesses also demand powerful processing capabilities, which can be effectively achieved through distributed computing environments facilitated by clustering software. The pursuit of improved performance and scalability to handle fluctuating workloads is another critical driver. As organizations expand their operations and customer base, their IT infrastructure must be able to scale seamlessly without compromising performance. Clustering software provides the framework for distributing workloads across multiple servers, thereby enhancing processing power and responsiveness. Furthermore, the increasing prevalence of complex IT architectures, including microservices and containerized applications, requires advanced orchestration and management capabilities, which clustering software inherently provides by enabling the coordination and availability of these distributed components. The economic benefits of minimizing downtime, such as preventing lost revenue and reputational damage, also play a crucial role in encouraging investment in this technology.

Despite the strong growth trajectory, the clustering software market is not without its hurdles. A primary challenge revolves around the complexity of implementation and management. Setting up and maintaining clustered environments often requires specialized expertise, leading to a shortage of skilled IT professionals capable of handling these intricate systems. This complexity can translate into significant upfront investment in training and personnel, acting as a restraint for some organizations, particularly Small & Medium businesses. Another significant concern is the cost of implementation and ongoing maintenance. While the long-term benefits of high availability are undeniable, the initial acquisition of clustering software, coupled with the necessary hardware infrastructure, can represent a substantial financial outlay. This cost factor can deter smaller enterprises from adopting robust clustering solutions, limiting their market penetration in this segment. Compatibility issues between different hardware, operating systems, and application software can also pose a significant challenge. Ensuring seamless interoperability within a clustered environment requires careful planning and thorough testing, adding to the implementation time and complexity. Moreover, the evolving threat landscape presents a continuous challenge, as clustering solutions must be continually updated and secured against sophisticated cyberattacks that could compromise the integrity of the entire cluster. The dependency on network infrastructure is another critical factor; the performance and reliability of a clustered system are heavily reliant on the underlying network's stability and speed, making network outages or bottlenecks a direct threat to the cluster's availability. Finally, the integration with existing legacy systems can be a complex and time-consuming undertaking, requiring extensive customization and potentially disrupting established workflows.

The clustering software market is characterized by regional and segment-specific dominance, with several key players and areas poised to lead the charge in the coming years.

North America: This region is expected to maintain a leading position in the global clustering software market throughout the Forecast Period (2025-2033). Several factors contribute to this dominance. Firstly, the presence of a highly developed IT infrastructure, coupled with a strong concentration of large enterprises and technology giants, fuels a substantial demand for advanced clustering solutions. The region is a hub for innovation, with significant investments in research and development for high-performance computing, big data analytics, and cloud technologies, all of which heavily rely on clustering. Furthermore, stringent regulatory requirements and a strong emphasis on business continuity and disaster recovery in sectors like finance and healthcare compel organizations in North America to adopt robust clustering software. The Enterprise segment within North America is particularly dominant, as these organizations possess the financial resources and the critical need for uninterrupted operations to justify significant investments in clustering technologies. The United States, in particular, represents a substantial portion of this regional market share.

Europe: Following closely behind North America, Europe is anticipated to be another significant contributor to the clustering software market. The region benefits from a mature IT landscape, a growing adoption of cloud services, and a strong presence of industries such as manufacturing, automotive, and telecommunications that are increasingly reliant on highly available IT systems. Regulatory compliance, such as GDPR, also indirectly drives the need for data resilience and availability, which clustering software provides. Similar to North America, the Enterprise segment in Europe is a primary driver of growth.

Asia Pacific: This region is projected to witness the fastest growth rate in the clustering software market during the Forecast Period (2025-2033). Rapid digitalization, the burgeoning adoption of cloud technologies, and the increasing demand for high-performance computing from emerging economies are key catalysts. Countries like China, India, and South Korea are making substantial investments in their IT infrastructure, leading to a surge in demand for clustering solutions. The growth of the Small & Medium businesses segment in this region is also noteworthy, as these businesses are increasingly recognizing the value of affordable and scalable clustering solutions to remain competitive. The increasing focus on digital transformation initiatives across various industries in the Asia Pacific region will further bolster the adoption of clustering software.

Segment Dominance - Enterprises: Across all regions, the Enterprise segment is unequivocally the dominant force in the clustering software market. Large corporations have the most critical applications and the most significant exposure to financial and reputational risks associated with IT downtime. This necessitates substantial investments in high-availability, fault-tolerant, and disaster recovery solutions, which are core functionalities of clustering software. Enterprises leverage clustering for a wide array of applications, including:

The clustering software industry is experiencing robust growth fueled by several key catalysts. The pervasive adoption of cloud computing and hybrid environments necessitates sophisticated solutions for managing distributed workloads and ensuring high availability. The escalating demand for big data analytics and high-performance computing (HPC) requires robust, scalable processing power, which clustering software effectively delivers by enabling distributed computation. Furthermore, the increasing sophistication of cyber threats and the critical need for business continuity and disaster recovery are compelling organizations of all sizes to invest in resilient IT infrastructures, with clustering software playing a pivotal role in achieving this objective.

The clustering software market is characterized by the presence of several key players, each contributing significantly to its growth and innovation. These companies offer a diverse range of solutions catering to various operating systems and application needs.

The clustering software sector has witnessed several key developments that have shaped its evolution and market dynamics.

This report provides an exhaustive analysis of the clustering software market, offering deep insights into its current state and future trajectory. We meticulously examine market size, segmentation by type (Windows, Linux and Unix, Others) and application (Small & Medium businesses, Enterprises), and regional dynamics. Our study highlights key trends, growth drivers, and challenges, painting a comprehensive picture of the competitive landscape. The report includes detailed company profiles of leading players and significant developments, providing actionable intelligence for stakeholders, investors, and businesses seeking to leverage the power of clustering technology. With a Study Period spanning 2019-2033, a Base Year of 2025, and a Forecast Period from 2025-2033, this report offers unparalleled depth and foresight into this critical IT sector.

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 3.2% from 2020-2034 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately 3.2%.

Key companies in the market include HP, IBM, Microsoft, Oracle, Symantec, Fujitsu, Nec Corporation, Red Hat, Silicon Graphics International Corp. (SGI), VMware, .

The market segments include Type, Application.

The market size is estimated to be USD 2488.7 million as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3480.00, USD 5220.00, and USD 6960.00 respectively.

The market size is provided in terms of value, measured in million.

Yes, the market keyword associated with the report is "Clustering Software," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Clustering Software, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.