1. What is the projected Compound Annual Growth Rate (CAGR) of the Cloud Game Service Platform?

The projected CAGR is approximately 43.31%.

Cloud Game Service Platform

Cloud Game Service PlatformCloud Game Service Platform by Application (Mobile, Consoles), by Type (<$10/Month, $10-20/Month, >$20/Month), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2026-2034

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

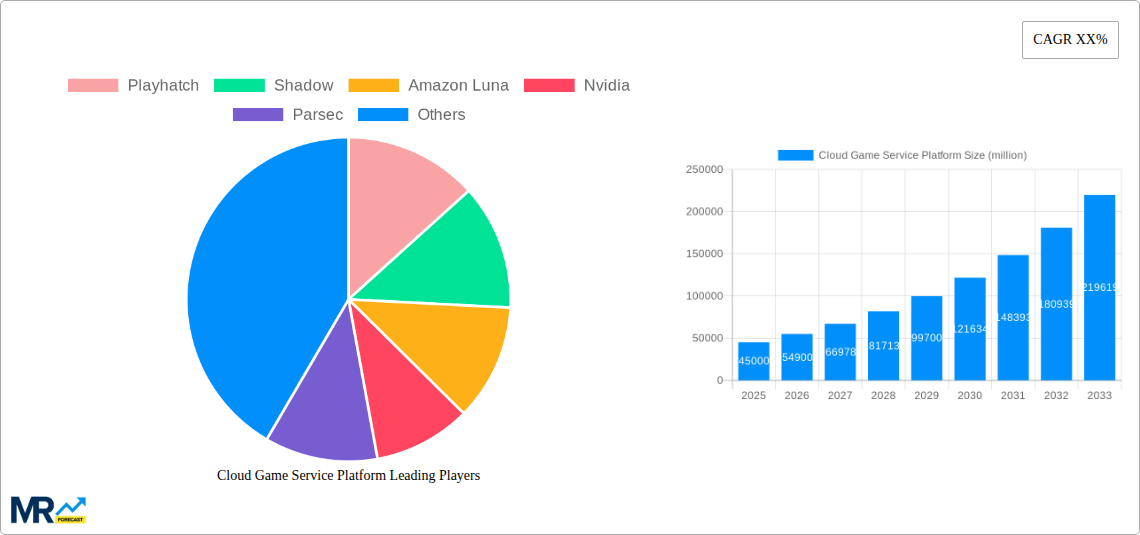

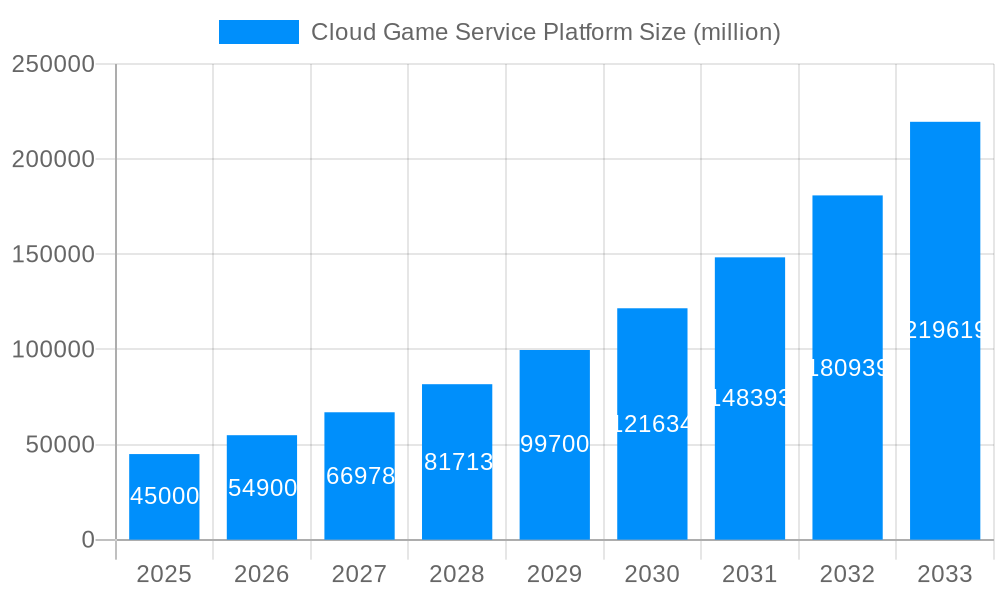

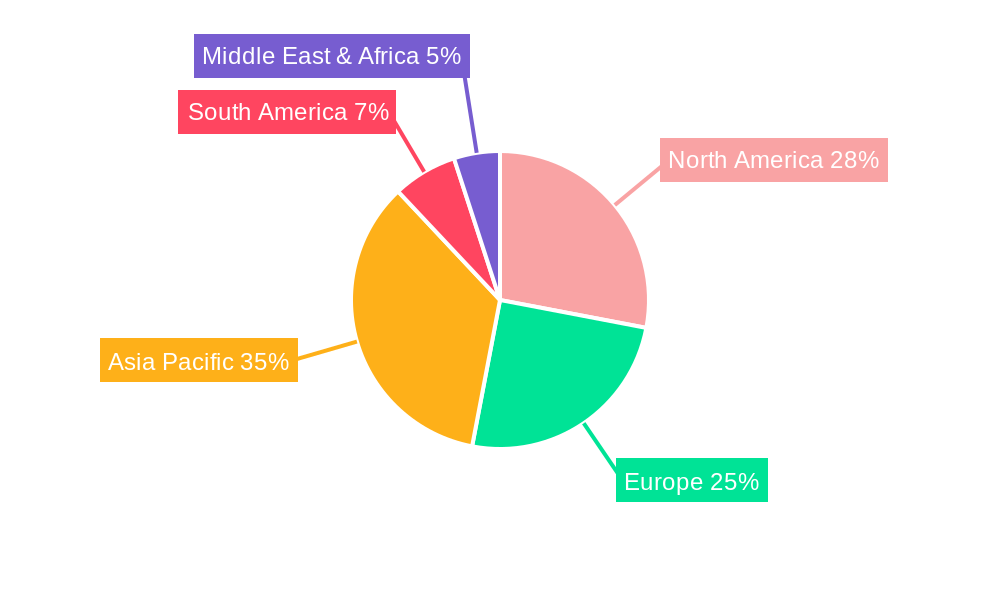

The cloud gaming service platform market is experiencing robust growth, driven by increasing internet penetration, the proliferation of high-speed mobile networks, and the rising demand for convenient and accessible gaming experiences. The market, estimated at $5 billion in 2025, is projected to achieve a Compound Annual Growth Rate (CAGR) of 25% from 2025 to 2033, reaching approximately $25 billion by 2033. This expansion is fueled by several key trends: the increasing popularity of subscription-based gaming models, advancements in cloud computing infrastructure enabling higher fidelity streaming, and the growing adoption of cloud gaming across diverse platforms, including mobile devices, consoles, and PCs. The market is segmented by pricing tiers ($10/month, $10-20/month, >$20/month) and application (mobile, consoles, PC). While the sub-$10/month tier currently dominates market share due to affordability, the higher-tier segments are witnessing rapid growth, driven by increased demand for higher-quality streaming and exclusive game libraries. Competition is intense, with established tech giants like Microsoft, Google, Amazon, and Nvidia alongside specialized cloud gaming providers such as Playhatch, Shadow, Parsec, and Blacknut vying for market share. Geographic growth is particularly strong in North America and Europe, but Asia-Pacific represents a significant opportunity for future expansion, driven by growing smartphone adoption and increasing internet access. However, challenges remain, including concerns around latency and bandwidth requirements, the need for consistent high-speed internet connectivity, and the ongoing development of more robust security measures to prevent piracy and data breaches.

The competitive landscape is shaping the future of cloud gaming. Major players are investing heavily in content acquisition and technological advancements to enhance the user experience and differentiate their services. Strategic partnerships and mergers and acquisitions are also expected to play a crucial role in reshaping the market. The success of individual platforms will depend on their ability to attract and retain subscribers by offering compelling game libraries, seamless user interfaces, affordable pricing models, and a reliable streaming infrastructure. This underscores the importance of continuous innovation and strategic positioning to thrive in this dynamic and evolving market. Future growth will also hinge on addressing technological limitations and overcoming the adoption barriers related to internet infrastructure in developing markets.

The cloud game service platform market is experiencing explosive growth, projected to reach multi-billion dollar valuations by 2033. Driven by advancements in internet infrastructure, processing power, and consumer demand for convenient and accessible gaming, the industry is witnessing a significant shift from traditional gaming models. The historical period (2019-2024) saw foundational development with key players establishing their platforms and a gradual increase in user adoption. The base year of 2025 marks a pivotal point, representing a period of market consolidation and significant expansion. The forecast period (2025-2033) anticipates continued substantial growth fueled by the increasing affordability of high-speed internet, the proliferation of 5G networks, and the continuous improvement in streaming technology resulting in higher-quality gameplay experiences. Key market insights indicate that the under-$10/month subscription tier shows the greatest growth potential, driven by price sensitivity among a broad user base. Furthermore, mobile application adoption is accelerating rapidly due to the convenience and ubiquity of smartphones. Competitive dynamics are shaping the market, with established tech giants like Microsoft and Google vying for market share alongside specialized cloud gaming platforms such as Shadow and Playkey. The industry is also witnessing strategic partnerships and mergers, aimed at expanding reach and enhancing service offerings. The overall trend demonstrates a maturing yet dynamically evolving market with immense growth potential across various segments. The adoption of cloud gaming is further accelerated by the ever-increasing need for high-end gaming experiences without requiring expensive hardware investments, paving the way for broader market penetration. This accessibility democratizes gaming, expanding the potential player base to millions.

Several factors are propelling the rapid growth of the cloud game service platform market. Firstly, the ever-improving internet infrastructure globally, particularly the widespread availability of high-speed broadband and the rollout of 5G networks, eliminates the latency issues that previously hampered the experience. This ensures smoother, more responsive gameplay, critical for attracting a mainstream audience. Secondly, the increasing affordability of cloud gaming subscriptions, especially the sub-$10/month plans, makes it a financially accessible option for a wider range of consumers compared to purchasing expensive consoles and high-end PCs. Thirdly, the convenience factor is undeniable; users can play their favorite games on various devices without being tied to a specific machine. This accessibility extends to different locations and is particularly appealing to a mobile generation. Furthermore, the constant innovation in game streaming technology has significantly improved visual quality and reduced input lag, further enhancing the user experience and driving adoption. Lastly, the market is boosted by strategic partnerships between game developers, platform providers, and hardware manufacturers, leading to a more comprehensive and integrated ecosystem. The combined effect of these factors positions the cloud gaming market for sustained and significant growth in the coming years.

Despite the promising outlook, several challenges and restraints hinder the widespread adoption of cloud gaming services. A persistent hurdle remains the dependency on a stable and high-speed internet connection. In regions with limited or unreliable internet infrastructure, the cloud gaming experience is severely compromised, limiting market penetration. Furthermore, data caps and variable internet costs can make cloud gaming expensive for some users, potentially offsetting the cost savings compared to traditional gaming. The issue of latency remains a concern, even with technological advancements, impacting the responsiveness of gameplay, especially in competitive scenarios. Concerns surrounding data security and privacy, particularly regarding sensitive user information and game progress, may also deter some potential users. Competition from established console and PC gaming industries poses a significant challenge, with these platforms benefitting from a large and loyal user base built over decades. Finally, the ongoing costs associated with maintaining robust server infrastructure and managing intellectual property rights for game libraries represent substantial financial investments for platform providers. Overcoming these challenges is crucial for achieving the full potential of the cloud game service platform market.

The <$10/month subscription tier is poised to dominate the market. This segment's affordability appeals to a massive user base, including casual gamers and those new to gaming. The high demand for this tier drives competitive pricing strategies and promotes market penetration. This is in line with the overall global trend towards more accessible entertainment options.

In summary, the sub-$10/month segment, fueled by mobile application adoption and driven by growth in both established and developing markets, will likely lead the market. The combined effect of affordability, accessibility, and strategic partnerships creates a powerful impetus for this segment's continued dominance.

The cloud game service platform industry is experiencing rapid growth due to several key factors. Firstly, improvements in internet speed and availability are making high-quality streaming possible for a wider audience. Secondly, the rising popularity of mobile gaming and the convenience of accessing games on diverse devices fuels demand. Thirdly, competitive pricing strategies, particularly in the budget-friendly subscription tiers, are attracting a wider range of consumers. Finally, technological advancements continue to improve the streaming experience, reducing latency and enhancing visual fidelity, which further drives market expansion.

This report provides a comprehensive analysis of the cloud game service platform market, examining its current state, future trends, and key players. It includes detailed insights into market segmentation, growth drivers, challenges, and competitive dynamics, allowing businesses to make data-driven decisions. The forecast period extends to 2033, providing a long-term perspective on market evolution and opportunities. The report’s comprehensive approach offers valuable information for stakeholders seeking a detailed understanding of this rapidly expanding sector.

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 43.31% from 2020-2034 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately 43.31%.

Key companies in the market include Playhatch, Shadow, Amazon Luna, Nvidia, Parsec, Playkey, Blacknut, Microsoft, Google, Steam, .

The market segments include Application, Type.

The market size is estimated to be USD 3.3 billion as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4480.00, USD 6720.00, and USD 8960.00 respectively.

The market size is provided in terms of value, measured in billion.

Yes, the market keyword associated with the report is "Cloud Game Service Platform," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Cloud Game Service Platform, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.