1. What is the projected Compound Annual Growth Rate (CAGR) of the Chiplet Packaging Technology?

The projected CAGR is approximately 15.61%.

Chiplet Packaging Technology

Chiplet Packaging TechnologyChiplet Packaging Technology by Type (2D, 2.5D, 3D), by Application (Artificial Intelligence, Automotive Electronics, High performance Computing Devices, 5G Applications, Other), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2026-2034

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

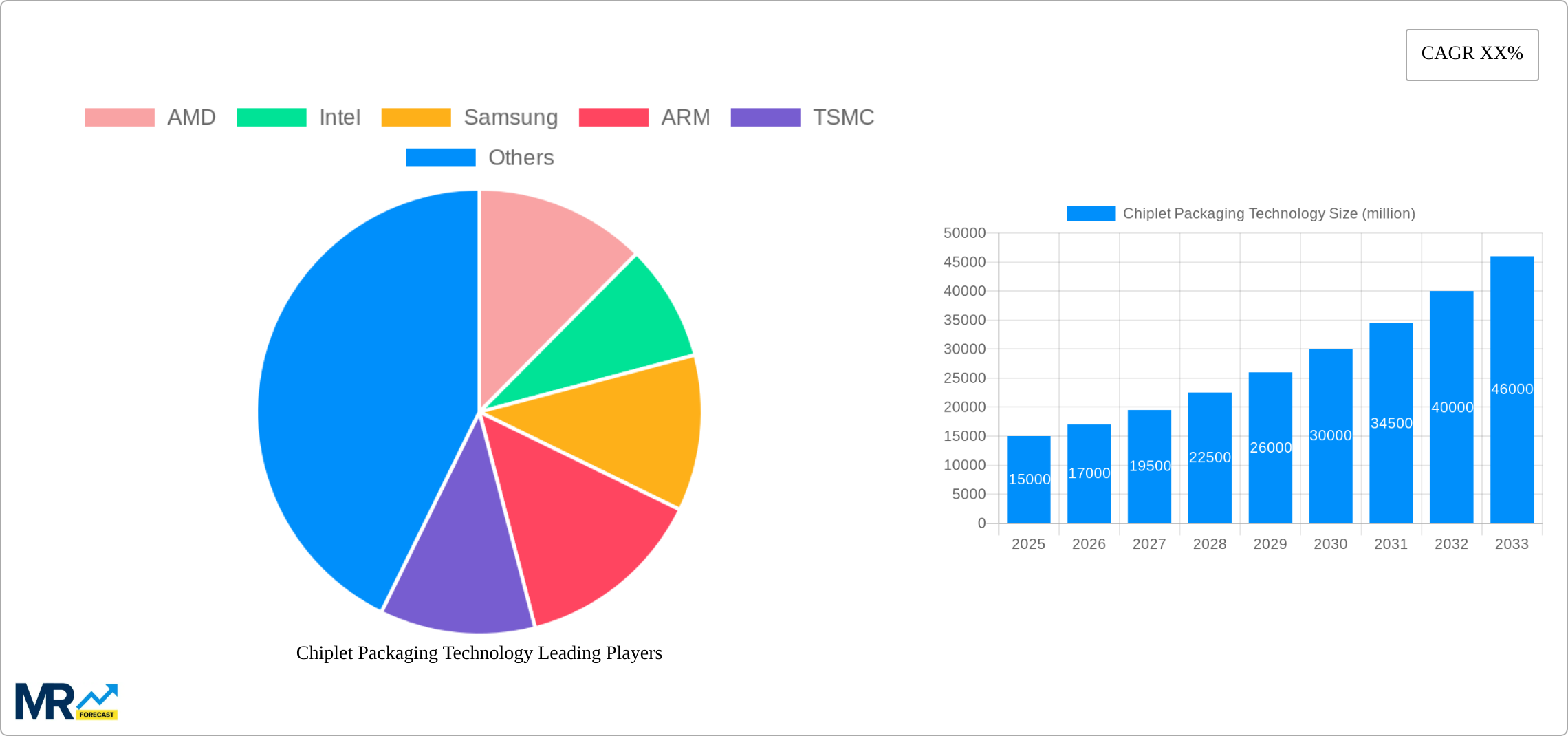

The chiplet packaging technology market is poised for significant expansion, driven by escalating demand for high-performance computing (HPC) and sophisticated semiconductor applications. This growth is fueled by the imperative for enhanced chip density, superior power efficiency, and optimized manufacturing economics. The capacity to integrate specialized chiplets from diverse manufacturers into a unified package enables superior performance and scalability, addressing the multifaceted needs of numerous industries. Key sectors such as artificial intelligence (AI), automotive electronics, and 5G are pivotal contributors, with AI notably demanding advanced processing capabilities. While 2.5D and 3D packaging currently dominate, the 2D segment retains a considerable share due to its cost-effectiveness for specific applications. However, a discernible trend towards advanced 2.5D and 3D solutions is evident as technological innovations overcome manufacturing challenges and improve affordability. Leading entities including AMD, Intel, and Nvidia are making substantial investments in research and development, reinforcing their market standing and fostering innovation. North America and Asia-Pacific currently lead market penetration, with emerging economies projected for robust growth through infrastructure development and accelerated technological adoption. Interoperability and standardization challenges persist but are being addressed through ongoing industry collaborations to facilitate broader adoption and seamless integration.

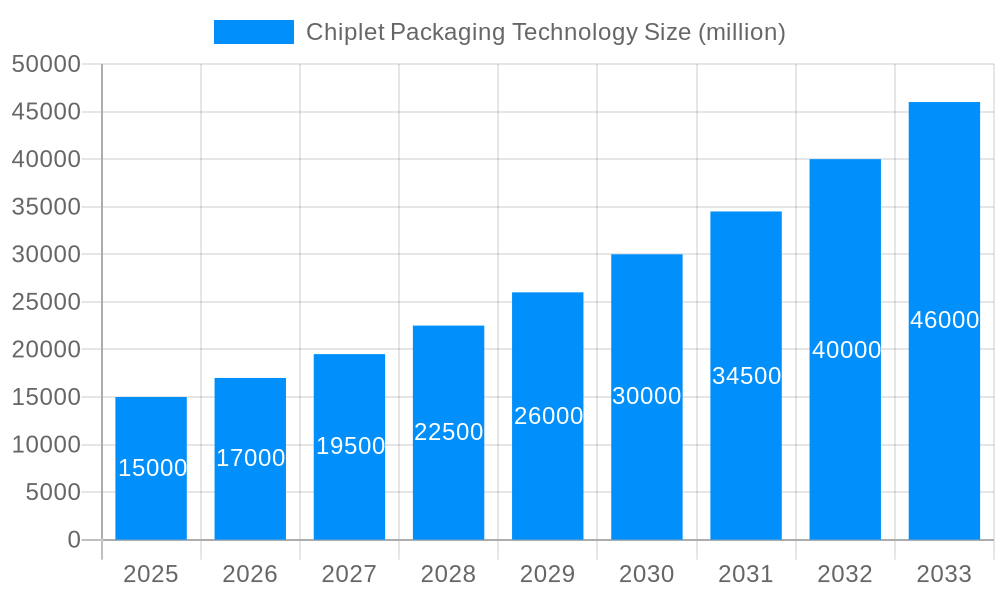

The chiplet packaging technology market is projected to achieve a compound annual growth rate (CAGR) of 15.61%. The current market size stands at 54.62 billion in the base year 2025, with robust growth anticipated through the forecast period (2025-2033). This expansion is propelled by continuous advancements in semiconductor technology and a burgeoning demand for high-performance computing. Market segmentation reveals a dynamic interplay between packaging types (2D, 2.5D, 3D) and applications. The 3D segment offers the highest growth potential due to its superior performance, while the 2.5D segment is expected to maintain a substantial market share by balancing performance and cost. The increasing complexity of electronic devices and the need for tailored solutions are driving demand for customized chiplet packaging. The competitive landscape is characterized by intensive R&D and strategic alliances among leading chip manufacturers, packaging firms, and equipment providers, crucial for overcoming technical hurdles and accelerating market adoption.

The chiplet packaging technology market is experiencing explosive growth, driven by the relentless demand for higher performance and power efficiency in computing. The global market, valued at USD XX million in 2024, is projected to reach USD YY million by 2033, exhibiting a robust CAGR of ZZ% during the forecast period (2025-2033). This remarkable expansion is fueled by several key factors. Firstly, the limitations of monolithic chip design in terms of cost, yield, and power consumption are becoming increasingly apparent, particularly in high-performance computing applications. Chiplet technology, by enabling the integration of specialized dies into a single system, elegantly addresses these challenges. Secondly, the increasing adoption of advanced nodes (e.g., 3nm, 5nm) further necessitates chiplet integration, as the cost and complexity of producing large monolithic chips at these advanced nodes become prohibitive. This trend is particularly visible in the high-growth segments like AI, HPC, and 5G, where the need for high computational power and low latency is paramount. Furthermore, the continuous innovation in packaging technologies, including 2.5D and 3D packaging, is further enhancing the performance and density of chiplet-based systems. Companies such as AMD, Intel, and TSMC are aggressively investing in research and development to improve chiplet packaging techniques, leading to advancements in inter-die communication and thermal management. This continuous improvement in technology is attracting more players into the ecosystem, broadening the potential applications and further driving market expansion. The market’s growth is also supported by the rising demand for high-performance computing in various sectors including automotive, cloud computing, and consumer electronics, which pushes the limits of traditional monolithic chip designs. Finally, collaborations across the industry chain, including packaging companies, chip designers, and equipment manufacturers, are streamlining the process and reducing the barriers to entry for adopting chiplet technology. The combined effect of these trends paints a picture of a consistently expanding market with significant potential for future growth.

Several key factors are driving the rapid growth of the chiplet packaging technology market. Firstly, the escalating demand for higher computing performance in diverse applications, particularly in high-performance computing (HPC), artificial intelligence (AI), and 5G infrastructure, is a primary catalyst. Traditional monolithic chip designs are struggling to keep pace with these demands, facing limitations in terms of cost, power consumption, and design complexity. Chiplet technology offers a compelling solution by enabling the integration of multiple specialized dies, each optimized for a specific function, into a single system. This modular approach allows for greater design flexibility, improved yield, and reduced development costs. Secondly, the advancements in packaging technologies, such as 2.5D and 3D stacking, are facilitating the creation of increasingly complex and powerful chiplet-based systems. These advanced packaging techniques enable higher bandwidth interconnects between chiplets, reducing communication latency and improving overall system performance. Thirdly, the industry’s growing adoption of heterogeneous integration, which involves combining different types of dies (e.g., CPUs, GPUs, memory) within a single package, is further boosting the market's growth. This allows for optimized system-level design and enhanced functionality, enabling the creation of more powerful and energy-efficient devices. Finally, increasing investment in R&D by major players like AMD, Intel, and TSMC is fostering innovation in chiplet technology, leading to continuous improvements in performance, reliability, and cost-effectiveness. These collaborative efforts are essential to the wider adoption of chiplet packaging solutions across various industries.

Despite its considerable potential, the widespread adoption of chiplet packaging technology faces several challenges. Firstly, the complexity of designing and manufacturing chiplet-based systems is significantly higher compared to monolithic chips. This increased complexity necessitates advanced design tools, sophisticated manufacturing processes, and specialized expertise, all of which add to the overall cost and time-to-market. Secondly, ensuring reliable and high-bandwidth interconnections between chiplets is crucial for optimal system performance. The development and implementation of robust interconnects, capable of handling the high data transfer rates required by high-performance applications, presents a significant technical hurdle. Moreover, effective thermal management is a critical concern in chiplet-based systems, as the high power density generated by multiple dies can lead to overheating and performance degradation. Efficient heat dissipation strategies are essential to ensure the reliable and stable operation of such systems. Thirdly, standardization and interoperability across different chiplet platforms remain an ongoing challenge. The lack of widely adopted standards could hinder the seamless integration of chiplets from different vendors and create compatibility issues. Finally, testing and verification of chiplet-based systems pose additional challenges due to the increased complexity of the system architecture. Rigorous testing protocols are necessary to ensure the reliability and functionality of these intricate systems, thereby adding further complexity and expense.

The High-Performance Computing (HPC) segment is poised to dominate the chiplet packaging technology market throughout the forecast period. This segment's demand is fuelled by the insatiable need for greater computational power in fields such as AI, machine learning, scientific simulations, and data analytics. The ability of chiplets to combine specialized processing units (CPUs, GPUs, memory) into a single package offers a significant advantage, enabling unparalleled performance levels while addressing constraints in power consumption and cost.

High-Performance Computing (HPC) applications: This segment is expected to witness significant growth due to the increasing demand for high computational power in various sectors, including data centers, cloud computing, and scientific research. The use of chiplet technology allows for the creation of more powerful and energy-efficient HPC systems. The projected market size for HPC applications using chiplet packaging is expected to reach USD XX million by 2033.

Artificial Intelligence (AI) applications: The AI sector is another major driver of chiplet adoption. The high computational demands of AI algorithms and the need for specialized hardware accelerators make chiplet technology a natural fit. The flexibility offered by chiplet designs makes it easy to incorporate specialized AI accelerators alongside other processing units for optimal performance. This market segment is expected to reach USD YY million by 2033.

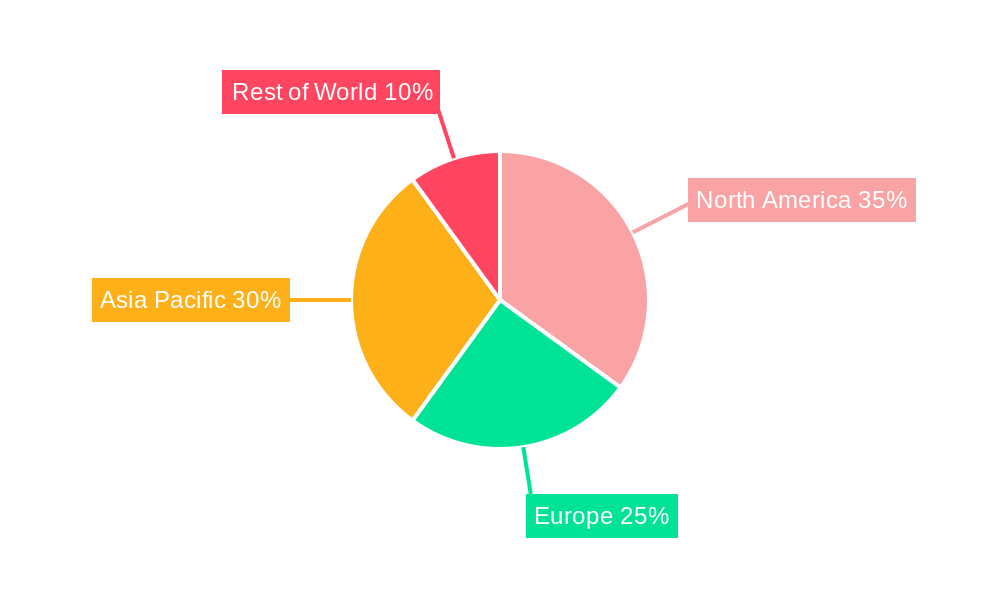

Geographical Dominance: North America is predicted to maintain its position as a leading market for chiplet technology, driven by the concentration of major technology companies and research institutions in the region. However, Asia Pacific (specifically regions like Taiwan, South Korea, and China) is expected to experience significant growth, fuelled by the rapid expansion of the semiconductor industry and substantial government investments in advanced technologies.

The 3D packaging type is anticipated to gain considerable traction, offering superior performance improvements compared to its 2D and 2.5D counterparts. The ability to stack multiple dies vertically allows for higher interconnect density and reduced signal latency, leading to enhanced system performance, reduced power consumption, and a smaller footprint. While 3D packaging presents greater manufacturing complexities, its performance advantages will drive adoption in high-performance applications.

In summary, the convergence of increasing demand from high-growth segments like HPC and AI, coupled with the performance advantages of 3D packaging, creates a powerful synergy that ensures the dominance of this specific market segment. The continuous development of advanced packaging techniques and increasing industry collaborations will only amplify this trend in the years to come.

The chiplet packaging technology industry's growth is fueled by several key factors: The increasing demand for higher performance and energy efficiency in computing, especially in high-growth markets like AI and HPC, drives the need for more advanced packaging solutions. Advancements in packaging technologies, such as 2.5D and 3D stacking, offer significant performance and density improvements. Furthermore, the growing adoption of heterogeneous integration, combining different types of dies within a single package, enhances system-level optimization and functionality. Finally, significant investments in research and development by key players continuously improve the technology, making it more accessible and cost-effective.

This report provides a comprehensive analysis of the chiplet packaging technology market, offering valuable insights into market trends, driving forces, challenges, and key players. It covers various aspects of the market, including different packaging types (2D, 2.5D, 3D), key applications (HPC, AI, Automotive), leading companies, and significant industry developments. The report provides detailed market forecasts for the period 2025-2033, offering a valuable resource for stakeholders in the semiconductor and related industries. The data-driven projections and insights are crucial for informed decision-making regarding investments, product development strategies, and market positioning.

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 15.61% from 2020-2034 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately 15.61%.

Key companies in the market include AMD, Intel, Samsung, ARM, TSMC, ASE Group, Qualcomm, NVIDIA Corporation, Tongfu Microelectronics, VeriSilicon Holdings, Akrostar Technology, Xpeedic, JCET Group, Tianshui Huatian Technology, Forehope Electronic, Empyrean Technology, Tongling Trinity Technology, .

The market segments include Type, Application.

The market size is estimated to be USD 54.62 billion as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4480.00, USD 6720.00, and USD 8960.00 respectively.

The market size is provided in terms of value, measured in billion.

Yes, the market keyword associated with the report is "Chiplet Packaging Technology," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Chiplet Packaging Technology, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.