1. What is the projected Compound Annual Growth Rate (CAGR) of the Cell Phone Insurance?

The projected CAGR is approximately XX%.

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

Cell Phone Insurance

Cell Phone InsuranceCell Phone Insurance by Type (/> Wireless Carrier, Mobile Phone Operators & Retailers, Other Channels), by Application (/> Physical Damage, Theft & Loss, Others), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2025-2033

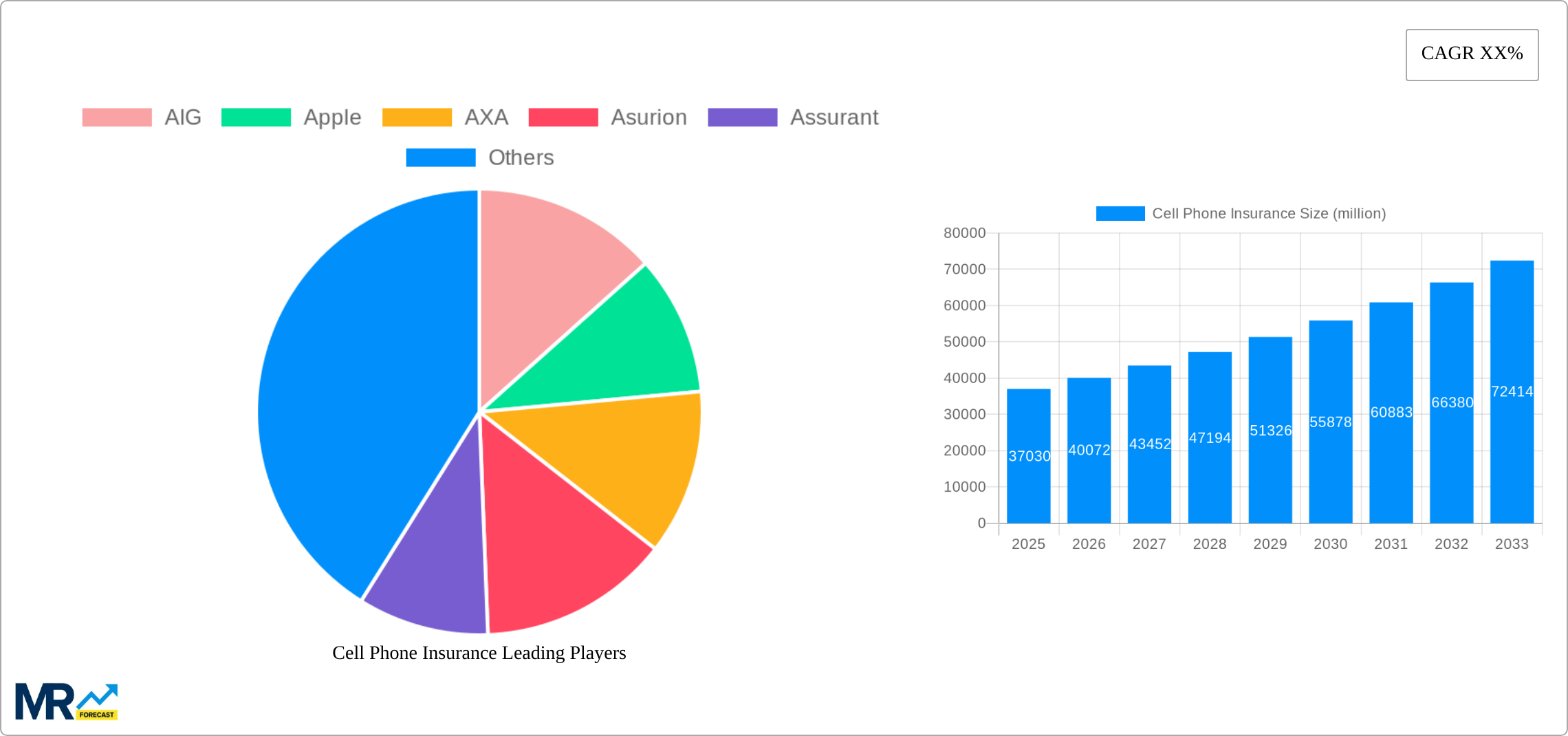

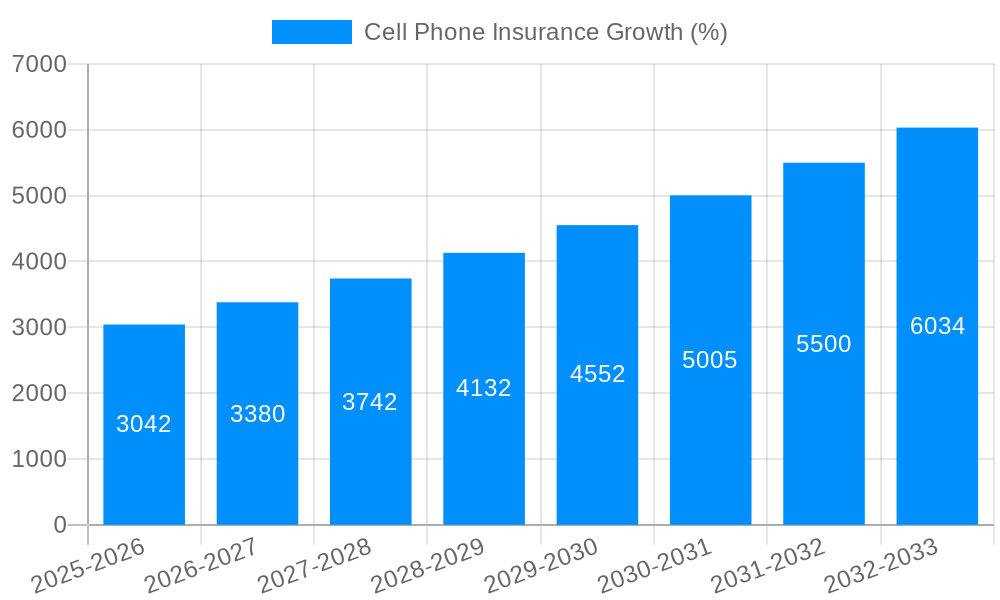

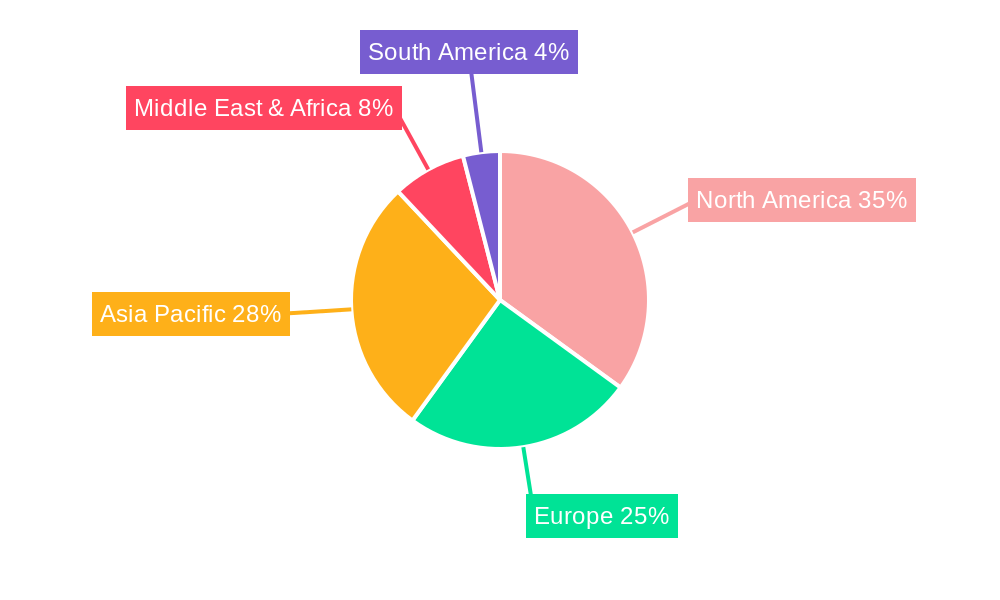

The global cell phone insurance market, valued at $37.03 billion in 2025, is poised for substantial growth. Driven by increasing smartphone ownership, escalating device costs, and a growing awareness of the risks associated with phone damage and theft, this market is expected to experience a considerable Compound Annual Growth Rate (CAGR). While precise CAGR figures are unavailable, considering the market drivers and the prevalence of insurance products in related tech sectors, a conservative estimate would place the CAGR between 8% and 12% for the forecast period of 2025-2033. Key market segments include wireless carriers, mobile phone operators & retailers, and other channels, with significant demand driven by coverage for physical damage and theft & loss. Major players like AIG, Apple, AXA, Asurion, and Assurant are actively competing, offering diverse coverage plans and distribution channels. Geographic growth will vary, with North America and Asia Pacific expected to dominate the market share due to high smartphone penetration and consumer spending on insurance products. The market will continue to evolve with technological advancements in device protection and the expansion of digital insurance platforms.

Further growth will be fueled by several factors including the increasing adoption of premium smartphones with higher repair costs, the growing popularity of mobile payment services increasing the risk of financial loss in case of theft, and the development of innovative insurance products like bundled packages that combine phone insurance with other services, like extended warranties or subscription services. The competitive landscape is likely to see further consolidation, with larger players potentially acquiring smaller companies to expand their market reach and service offerings. Regulatory changes and evolving consumer preferences will also impact market dynamics, necessitating adaptation from players to maintain their competitive edge. Regional variations in consumer behavior and insurance penetration rates will also influence the market's growth trajectory.

The global cell phone insurance market, valued at XXX million units in 2024, is projected to experience robust growth, reaching XXX million units by 2033. This signifies a Compound Annual Growth Rate (CAGR) of X% during the forecast period (2025-2033). The historical period (2019-2024) witnessed a steady increase driven by rising smartphone adoption, increasing device costs, and consumer awareness of the financial risks associated with phone damage or loss. The market is highly fragmented, with a mix of large multinational insurers like AIG, AXA, and Allianz, alongside specialized providers like Asurion and Assurant, and increasingly, mobile carriers themselves offering bundled insurance plans. The shift towards premium smartphones with advanced features has further fueled demand, as consumers are more hesitant to absorb the high replacement costs. This report analyzes market trends across various distribution channels—wireless carriers, mobile phone operators & retailers, and other channels—and application types: physical damage, theft & loss, and other miscellaneous coverages. The increasing adoption of online channels and the use of embedded insurance within the purchasing process also contributes to market growth. Furthermore, technological advancements in claims processing and fraud detection are optimizing the industry's efficiency. The rising popularity of extended warranty programs further adds to the market's overall growth. Data analysis from the period 2019-2024 indicates a consistent upward trajectory, setting the stage for a significant expansion over the coming decade. The base year for this report is 2025, and its insights are crucial for stakeholders across the insurance and mobile technology industries.

Several key factors are driving the expansion of the cell phone insurance market. The escalating cost of smartphones is a primary driver, making consumers more receptive to insurance options that mitigate the financial burden of repair or replacement. Moreover, the increasing prevalence of smartphones in daily life, coupled with their susceptibility to damage, theft, and loss, fuels the demand for protective coverage. The rise of bundled insurance plans offered directly by mobile carriers and retailers simplifies the purchasing process and enhances accessibility for consumers. The convenience of integrated insurance offerings within the smartphone purchase itself further contributes to the market’s growth. This seamless integration removes a barrier to entry and makes insurance a more attractive proposition to the average consumer. Marketing efforts emphasizing the value proposition of cell phone insurance, highlighting the cost savings associated with claims versus outright replacement costs, play a significant role. Furthermore, the growing sophistication of insurance products, offering tailored coverage options to meet varied consumer needs, drives market expansion. Innovative features, such as immediate online claims filing and faster processing times, enhance customer satisfaction and fuel demand. Finally, the continued growth in smartphone penetration, particularly in emerging economies, promises sustained market expansion in the coming years.

Despite the positive growth trajectory, several challenges hinder the cell phone insurance market. High claims rates, particularly for theft and loss, can significantly impact profitability for insurers. This necessitates robust fraud detection mechanisms and potentially higher premiums. Furthermore, competition among providers, including those directly integrated with mobile carriers, leads to price pressures and necessitates efficient cost management for sustained profitability. Another key challenge is ensuring accurate valuation of devices, especially given the rapid pace of technological advancements and fluctuations in market values. Managing customer expectations, particularly regarding claims processing speed and efficiency, is also paramount to maintaining positive brand perception. Regulatory complexities, varying across different jurisdictions, also impact market operations and require insurers to adapt to diverse legal frameworks. The challenge of accurately assessing the risk associated with specific phone models and usage patterns is another barrier to efficient risk management. Finally, maintaining customer trust and transparency in claims processes is vital, as negative experiences can negatively impact the market's reputation.

Segments Dominating the Market:

Application: Physical Damage: This segment consistently accounts for the largest share of the market due to the inherent fragility of smartphones and their susceptibility to accidental damage, such as screen cracks or water damage. The high repair costs associated with these types of damages directly translate to a higher demand for this specific coverage type. Consumer behavior shows a clear preference for protecting against the most common and costly repair needs.

Distribution Channel: Wireless Carriers: Wireless carriers are increasingly becoming a dominant distribution channel. Bundled insurance offerings directly through carriers offer unmatched convenience and simplify the purchasing process. This strategic integration results in high adoption rates and strong market penetration for this distribution channel, often exceeding that of independent insurance providers or retailers.

Key Regions:

North America: North America consistently leads the global market due to high smartphone penetration, high average device prices, and a well-developed insurance infrastructure. The mature insurance market and advanced technological capabilities also contribute to the region's dominance.

Europe: Europe's considerable smartphone user base and growing awareness of the benefits of mobile insurance contribute to its position as a significant market. The region's diverse insurance landscape, encompassing both established players and new entrants, fosters healthy competition and innovation.

Asia-Pacific: The Asia-Pacific region exhibits significant growth potential, driven by rapid smartphone adoption and expanding middle-class populations. While initially lagging in insurance penetration compared to North America and Europe, the region is demonstrating impressive growth rates.

The strategic focus on these specific segments and regions offers significant opportunities for market players to capture significant shares of the expanding cell phone insurance market. The combined impact of these factors ensures a strong outlook for this market segment's growth through 2033 and beyond.

The confluence of rising smartphone prices, increasing consumer reliance on mobile devices, and streamlined insurance distribution models significantly fuels growth in the cell phone insurance industry. The ease of integrating insurance into existing mobile phone purchase plans and bundled services further propels growth. Innovative features like faster claims processing and broader coverage options enhance consumer appeal and trust. Finally, the evolving technological landscape, constantly demanding higher-end phone replacements, continually increases the market's overall potential.

This report provides a comprehensive overview of the cell phone insurance market, analyzing current trends, driving forces, challenges, and growth catalysts. The study includes detailed market segmentation, regional analysis, and profiles of key market players, offering valuable insights for businesses and stakeholders in the industry. Its forecasts for 2025-2033 provide a robust foundation for strategic decision-making, covering a range of factors vital for understanding the industry's trajectory. The report's meticulous analysis enables effective planning and investment strategies for navigating this dynamic market successfully.

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of XX% from 2019-2033 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately XX%.

Key companies in the market include AIG, Apple, AXA, Asurion, Assurant, Hollard Group, Chubb (ACE), SoftBank, Allianz Insurance, AmTrust, Aviva.

The market segments include Type, Application.

The market size is estimated to be USD 37030 million as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4480.00, USD 6720.00, and USD 8960.00 respectively.

The market size is provided in terms of value, measured in million.

Yes, the market keyword associated with the report is "Cell Phone Insurance," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Cell Phone Insurance, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.