1. What is the projected Compound Annual Growth Rate (CAGR) of the Automotive Usage-based Insurance?

The projected CAGR is approximately 24.8%.

Automotive Usage-based Insurance

Automotive Usage-based InsuranceAutomotive Usage-based Insurance by UBI Model Type (Pay-How-You-Drive (PHYD), Pay-As-You-Drive (PAYD), Manage-How-You-Drive (MHYD), Distance-Based Insurance), by Distribution Channel (Direct-to-Consumer (DTC) Sales, Brokers & Agents, OEM Partnerships), by End-User (Private Individuals, Fleet Operators & Logistics Companies, Ride-Sharing & Mobility Service Providers, Corporate & Employee Vehicle Programs), by Vehicle Type (Passenger Vehicles, Commercial Vehicles), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2026-2034

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

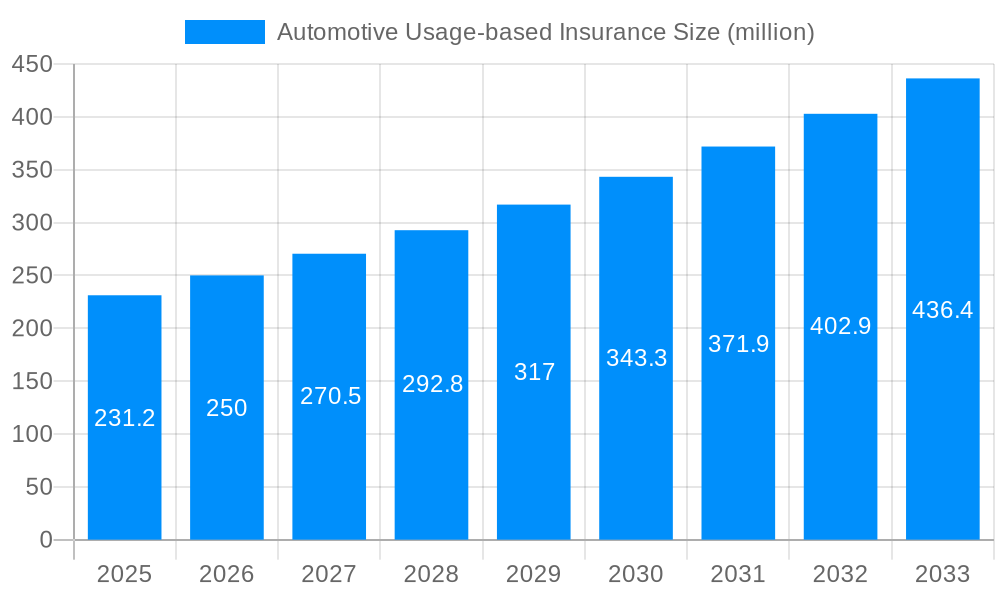

The Global Automotive Usage-based Insurance Market is poised for an exponential growth trajectory, demonstrating its transformative potential within the broader Automotive Insurance Market. Valued at an estimated $62.6 billion in 2025, the market is projected to expand significantly, driven by a robust Compound Annual Growth Rate (CAGR) of 24.8% over the forecast period. This impressive growth is anticipated to propel the market valuation to approximately $380.4 billion by 2033. This surge is fundamentally fueled by the convergence of advanced telematics, sophisticated data analytics, and a growing consumer appetite for personalized insurance products.

The demand for Automotive Usage-based Insurance Market solutions is primarily driven by several critical factors. Consumers are increasingly seeking lower premiums, personalized risk assessments, and incentivized safer driving behaviors. Insurers, on the other hand, benefit from improved risk segmentation, reduced claims fraud, and enhanced customer engagement. Macroeconomic tailwinds, including rapid digital transformation across industries, the proliferation of IoT Devices Market, and increasing penetration of the Connected Car Market, further bolster this expansion. The continuous evolution in sensor technology, artificial intelligence, and real-time data processing capabilities, underpinning the Data Analytics Market, allows for more accurate and dynamic pricing models, moving away from traditional demographic-based underwriting.

The forward-looking outlook for the Automotive Usage-based Insurance Market indicates a shift towards more sophisticated models, integrating predictive analytics, gamification elements, and multi-modal data inputs. Strategic partnerships between insurance providers, automotive OEMs, and technology firms are accelerating the adoption of embedded UBI solutions, making it a seamless part of vehicle ownership. Regulatory frameworks, while still nascent in some regions, are gradually adapting to support data-driven insurance models, fostering an environment conducive to innovation and growth. The market's robust CAGR underscores a fundamental restructuring of the automotive insurance paradigm, moving towards a fairer, more data-informed, and highly personalized approach to risk management.

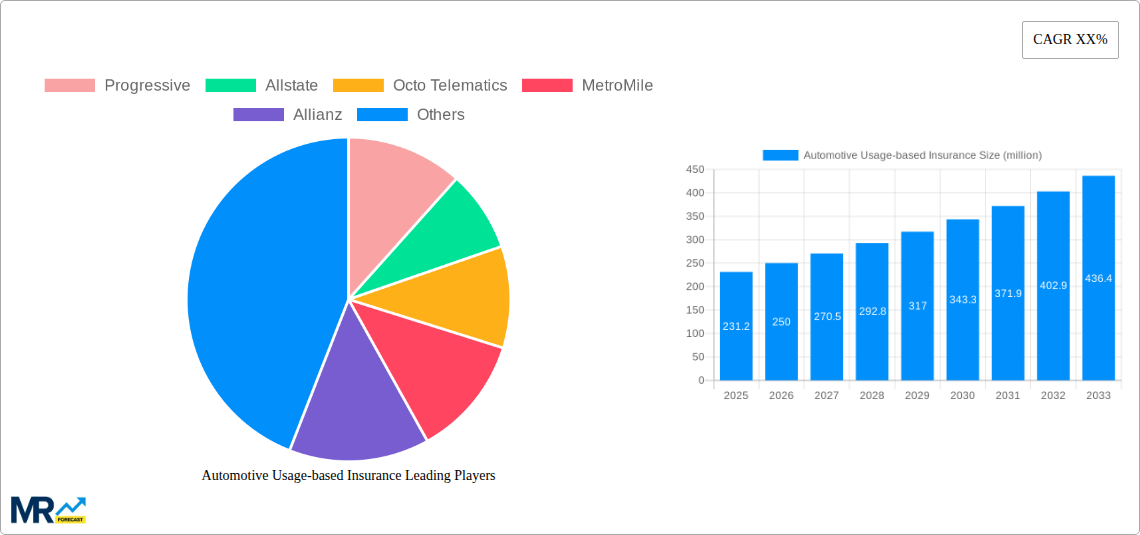

Within the Automotive Usage-based Insurance Market, the Pay-How-You-Drive (PHYD) model stands as the dominant segment by revenue share, largely due to its direct and transparent correlation between driving behavior and insurance premiums. This model meticulously assesses driving habits such as speed, braking, acceleration, cornering, and time of day, thereby empowering policyholders to directly influence their premium costs through safer driving. The fundamental appeal of PHYD lies in its fairness, offering tangible financial incentives for low-risk drivers and promoting improved road safety across the board. This contrasts with traditional models where premiums are largely based on broader demographic statistics rather than individual performance. The widespread adoption of telematics technology, a key enabler for the Telematics Market, has significantly enhanced the efficacy and precision of PHYD programs, allowing for real-time data collection and analysis.

Key players in the Automotive Usage-based Insurance Market, such as Progressive, Allstate, and Octo Telematics, have heavily invested in and popularized PHYD programs. Progressive's 'Snapshot' and Allstate's 'Drivewise' are prime examples of successful PHYD initiatives that have captured significant market share by demonstrating clear value propositions to consumers. These programs leverage advanced sensors and GPS data collected via smartphone apps or dedicated in-vehicle devices to build comprehensive driver profiles. The growing sophistication of data analytics, a crucial component of the Data Analytics Market, allows insurers to refine their risk algorithms, making PHYD models increasingly accurate and appealing.

While PHYD currently dominates, other UBI models like Pay-As-You-Drive (PAYD), Manage-How-You-Drive (MHYD), and Distance-Based Insurance also hold significant niches. PAYD primarily focuses on mileage driven, appealing to low-mileage drivers. MHYD, an evolving model, offers proactive coaching and feedback to drivers to improve behavior. Distance-Based Insurance, a simpler form of PAYD, charges based on total miles. The market share of PHYD is expected to continue its growth trajectory, driven by consumer preference for personalized pricing and the increasing availability of sophisticated and user-friendly telematics solutions. The continuous innovation in the Automotive Telematics Market, coupled with the integration of AI and machine learning for predictive analysis, is further cementing PHYD's leadership. As the Connected Car Market expands, embedded telematics solutions from OEMs are also making PHYD adoption more seamless and pervasive, suggesting a consolidation of its dominance rather than a shift towards alternative models, although hybrid models integrating elements of all types are likely to emerge.

The Automotive Usage-based Insurance Market is shaped by a dynamic interplay of factors that both accelerate its adoption and pose significant challenges. A primary driver is the rising penetration of telematics technology. The rapid expansion of the Telematics Market means more vehicles are equipped with communication and data capture capabilities, whether through embedded systems, smartphone apps, or aftermarket devices. This pervasive data collection infrastructure is fundamental to UBI's operational model, enabling real-time monitoring of driving behavior. For instance, the global automotive telematics subscriber base is projected to grow substantially, directly fueling the availability of data essential for UBI policies.

Another significant driver is the increasing consumer demand for personalized and fair insurance premiums. Traditional insurance models often penalize good drivers due to broad risk pools. UBI, particularly the Pay-How-You-Drive model, offers a compelling alternative by directly linking premiums to individual driving behavior. This appeal is amplified by a cost-conscious consumer base seeking to reduce expenses, especially those with lower risk profiles. Furthermore, technological advancements in data analytics and artificial intelligence are transforming the efficiency and accuracy of UBI. The evolution of the Data Analytics Market allows insurers to process vast quantities of driving data, identify nuanced risk patterns, and offer highly granular pricing. This capability also extends to fraud detection and claims processing, improving operational efficiency for providers.

Conversely, the market faces several notable constraints. Data privacy and security concerns represent a significant hurdle. Consumers are often reluctant to share personal driving data due to fears of misuse, breaches, or surveillance, directly impacting the adoption rate. Insurers must invest heavily in robust data protection measures to build trust. Additionally, the high initial investment required for telematics infrastructure and advanced analytical platforms can be a barrier for smaller insurance providers entering the Automotive Usage-based Insurance Market. The cost of developing, deploying, and maintaining the necessary hardware, software, and data management systems can be substantial. Lastly, regulatory fragmentation and varying legal frameworks across different regions can complicate market expansion. Divergent regulations regarding data collection, storage, and usage create operational complexities and compliance challenges for global insurers, slowing down the standardized rollout of UBI products and hindering the seamless growth of the Digital Insurance Market.

The Automotive Usage-based Insurance Market is characterized by a mix of established insurance giants, specialized telematics providers, and innovative startups. Competition is intensifying as companies vie for market share through technological differentiation, strategic partnerships, and tailored product offerings.

February 2024: A leading European insurer announced a partnership with a major automotive OEM to integrate embedded telematics systems into new vehicle models, offering seamless opt-in UBI policies at the point of sale, aiming to grow its market share in the Automotive Usage-based Insurance Market. December 2023: A prominent U.S. based telematics provider secured Series C funding to expand its AI-driven risk assessment platform, enhancing its predictive capabilities for the Automotive Insurance Market and targeting more granular pricing models. October 2023: Regulatory authorities in a key Asia-Pacific nation unveiled new guidelines for data privacy and security specific to usage-based insurance, aiming to boost consumer confidence and accelerate adoption in the region. August 2023: Several insurers launched pilot programs for multi-modal UBI, incorporating data from not just vehicle usage but also public transport and ride-sharing activities, reflecting an evolving understanding of mobility risks. June 2023: A specialized startup introduced an edge computing solution for telematics data processing, aiming to reduce latency and improve the efficiency of real-time UBI feedback for drivers, leveraging advancements in the IoT Devices Market. April 2023: A global automotive manufacturer announced the acquisition of a telematics software company, signaling a strategic move to offer its own branded UBI services directly to customers, strengthening its position in the Connected Car Market. February 2023: A consortium of insurers and technology firms initiated a cybersecurity task force focused on protecting sensitive driving data, addressing growing concerns around data breaches in the Automotive Usage-based Insurance Market.

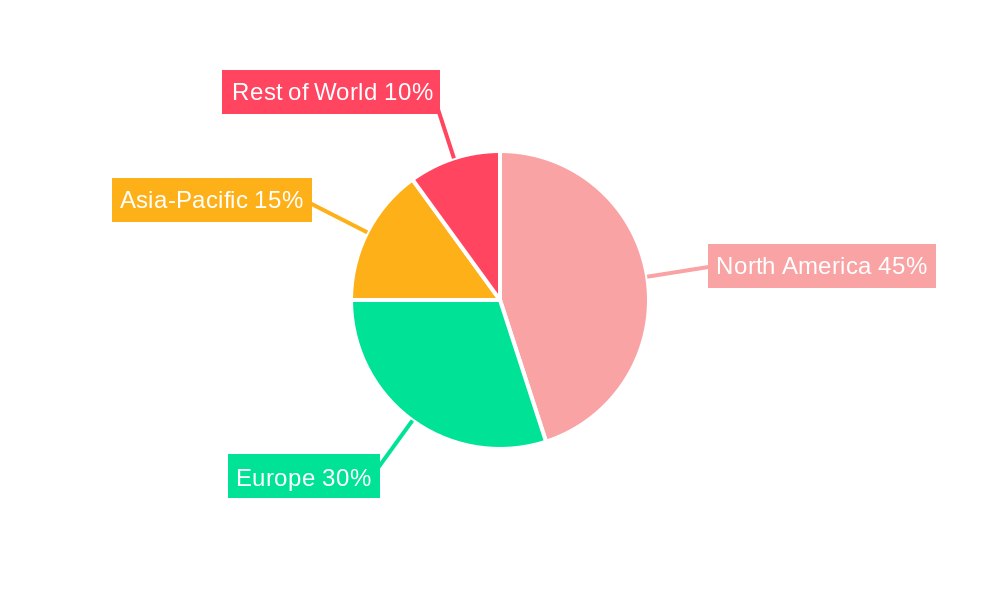

The global Automotive Usage-based Insurance Market exhibits diverse growth patterns and adoption rates across its key geographical segments. North America and Europe currently represent the most mature markets, having been early adopters of UBI technologies. In North America, particularly the United States, high consumer awareness, favorable regulatory environments in some states, and the presence of major UBI pioneers like Progressive and Allstate have fueled consistent growth. The region benefits from a high penetration of the Connected Car Market and a sophisticated Automotive Telematics Market infrastructure. Key demand drivers include competitive insurance markets, a strong focus on risk mitigation, and consumer demand for lower premiums based on individual driving behavior. Europe, similarly, has seen robust adoption, particularly in countries like the UK and Italy, where early regulatory support and a proactive insurance sector fostered innovation. Demand in Europe is driven by increasing smartphone penetration, the push for road safety, and competitive pricing strategies among insurers.

Asia Pacific (APAC) is rapidly emerging as the fastest-growing region in the Automotive Usage-based Insurance Market. Countries such as China, India, and Japan are witnessing a surge in vehicle ownership, coupled with rapid digitalization and technological advancements. The vast population and burgeoning middle class present an immense untapped potential for UBI solutions. Demand drivers in APAC include increasing digital literacy, government initiatives promoting smart cities and connected infrastructure, and a growing recognition of UBI's role in reducing accident rates and insurance fraud. The expanding IoT Devices Market in the region also plays a crucial role in providing the necessary hardware for telematics data collection. While starting from a smaller base, the region's growth rate is expected to outpace that of more mature markets.

Latin America and the Middle East & Africa (MEA) regions are considered emerging markets for Automotive Usage-based Insurance. Growth in these areas is slower but steadily progressing, driven by increasing smartphone adoption, rising vehicle penetration, and the potential for UBI to address high accident rates and insurance fraud. In Latin America, countries like Brazil and Argentina are gradually embracing UBI, motivated by the desire to reduce the cost of insurance and improve driver safety. The MEA region is also showing nascent interest, with GCC countries and South Africa leading the way. The primary demand drivers here revolve around the need for more efficient risk management, technological leapfrogging in digital services, and a young, digitally-native population open to innovative insurance products. The long-term potential for the Digital Insurance Market in these regions is significant as infrastructure develops and consumer awareness grows, alongside the burgeoning Commercial Vehicles Market adoption of telematics.

The Automotive Usage-based Insurance Market caters to a diverse range of end-users, each with distinct purchasing criteria, price sensitivities, and procurement channels. Private Individuals constitute the largest segment. Their buying behavior is heavily influenced by price sensitivity, primarily seeking lower premiums through demonstrated safe driving. Convenience of participation, ease of data sharing, and perceived fairness are crucial. Many private individuals procure UBI policies through direct-to-consumer (DTC) channels via insurer websites or mobile apps, valuing digital interactions. However, traditional brokers and agents still play a role, particularly for those seeking personalized advice or bundling options. Privacy concerns remain a significant hurdle for this segment, requiring transparent data usage policies from insurers.

Fleet Operators & Logistics Companies represent a high-value segment within the Automotive Usage-based Insurance Market. Their purchasing criteria extend beyond mere premium reduction to encompass operational efficiency, driver safety improvements, and asset utilization. They seek UBI solutions that integrate with broader Fleet Management Market systems, providing data on vehicle tracking, fuel efficiency, maintenance alerts, and driver coaching. Price sensitivity exists, but the emphasis shifts to return on investment (ROI) derived from reduced accidents, lower fuel costs, and optimized logistics. Procurement is typically through specialized commercial insurance brokers or direct enterprise sales, often involving custom solutions and long-term contracts. The integration with existing telematics systems for Commercial Vehicles Market is a key consideration.

Ride-Sharing & Mobility Service Providers form a rapidly growing, specialized segment. Their unique risk profiles, characterized by high mileage and multiple drivers per vehicle, necessitate bespoke UBI solutions. These providers prioritize flexibility, scalability, and seamless integration with their operational platforms. Cost-effectiveness is vital, but so is the ability to adapt to dynamic usage patterns. Procurement often involves strategic partnerships with insurers or direct engagement for white-label solutions, sometimes facilitated by automotive OEMs that integrate UBI capabilities into their vehicles for these services. Data insights from the Automotive Telematics Market are critical for managing the unique risks of this segment.

Corporate & Employee Vehicle Programs seek UBI for risk management, employee safety, and cost control for company-owned or leased vehicles. Purchasing decisions are driven by compliance, duty of care, and overall cost reduction through reduced claims and improved driver behavior. Procurement involves corporate insurance departments working with brokers or directly with insurers to implement fleet-wide UBI solutions. Notable shifts in buyer preference include an increasing demand for integrated digital platforms that offer real-time feedback, gamification to incentivize safer driving, and clear, concise data privacy assurances across all segments, reflecting the broader Digital Insurance Market trends.

The Automotive Usage-based Insurance Market has attracted substantial investment and funding activity over the past two to three years, driven by its high growth potential and the ongoing digital transformation within the Automotive Insurance Market. Mergers and acquisitions (M&A) have been a prominent feature, with established insurers often acquiring specialized telematics providers or technology startups to bolster their UBI capabilities. This strategy allows traditional players to rapidly integrate advanced data analytics platforms and proprietary telematics hardware/software, thereby accelerating their time to market for innovative UBI products. For example, several large insurance groups have strategically acquired smaller companies focusing on the Data Analytics Market or specific Telematics Market niches to gain a competitive edge in behavioral risk assessment.

Venture funding rounds have seen significant capital flowing into startups that are innovating across the UBI value chain. Companies specializing in AI and machine learning for predictive risk modeling, real-time feedback mechanisms, and sophisticated driver scoring algorithms have been particularly attractive to venture capitalists. These startups are often focused on enhancing the precision and personalization of UBI offerings, leveraging advancements in the IoT Devices Market and cloud computing. Furthermore, new entrants focusing on novel data sources or alternative telematics capture methods (e.g., smartphone-only solutions) have also secured considerable funding, indicating a diverse range of technological approaches being explored.

Strategic partnerships represent another critical aspect of investment activity. Collaborations between automotive OEMs, technology companies, and insurers are becoming increasingly common. These partnerships aim to embed UBI solutions directly into new vehicles, creating a seamless experience for consumers and a new distribution channel for insurers. Such alliances also facilitate the sharing of data and expertise, accelerating the development of next-generation UBI products. Sub-segments attracting the most capital include AI/ML-driven risk assessment platforms, real-time telematics data processing solutions, and innovative digital distribution channels. These areas are seen as crucial for unlocking further efficiencies, improving customer engagement, and expanding the reach of the Automotive Usage-based Insurance Market globally, especially as the Connected Car Market continues its expansion. The focus on enhancing the digital customer journey and leveraging advanced analytics indicates a strong push towards solidifying the broader Digital Insurance Market.

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 24.8% from 2020-2034 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately 24.8%.

Key companies in the market include Progressive, Allstate, Octo Telematics, MetroMile, Allianz, AXA, Liberty Mutual, Verizon, Movitrack Viasat, Nationwide, Esurance, Safeco, Travellers, Liberty Mutual Insurance, AIOI, QBE, Modus Group, Intelligent Mechatronic Systems, Inseego, Truemotion, Cambridge Mobile Telematics.

The market segments include UBI Model Type, Distribution Channel, End-User, Vehicle Type.

The market size is estimated to be USD 62.6 billion as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4480.00, USD 6720.00, and USD 8960.00 respectively.

The market size is provided in terms of value, measured in billion.

Yes, the market keyword associated with the report is "Automotive Usage-based Insurance," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Automotive Usage-based Insurance, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.