1. What is the projected Compound Annual Growth Rate (CAGR) of the Advanced Distribution Management Systems Software?

The projected CAGR is approximately 32.2%.

Advanced Distribution Management Systems Software

Advanced Distribution Management Systems SoftwareAdvanced Distribution Management Systems Software by Type (Cloud-Based, On-Premises), by Application (Buildings and Facilities, Electric and Gas Utilities, Government, Mapping and Surveying, Mining, Rail and Transit, Roads and Highways), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2026-2034

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

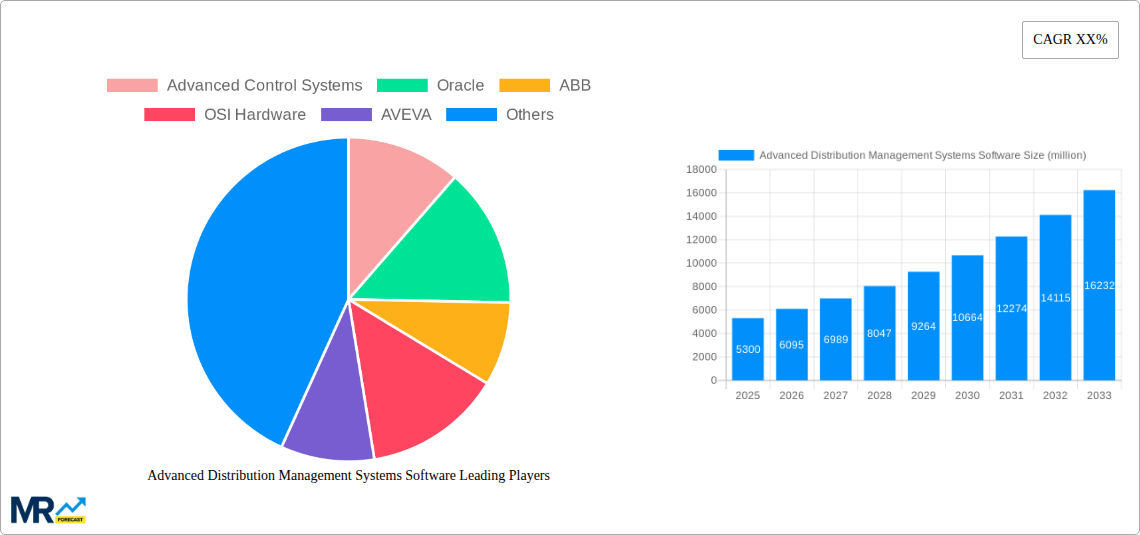

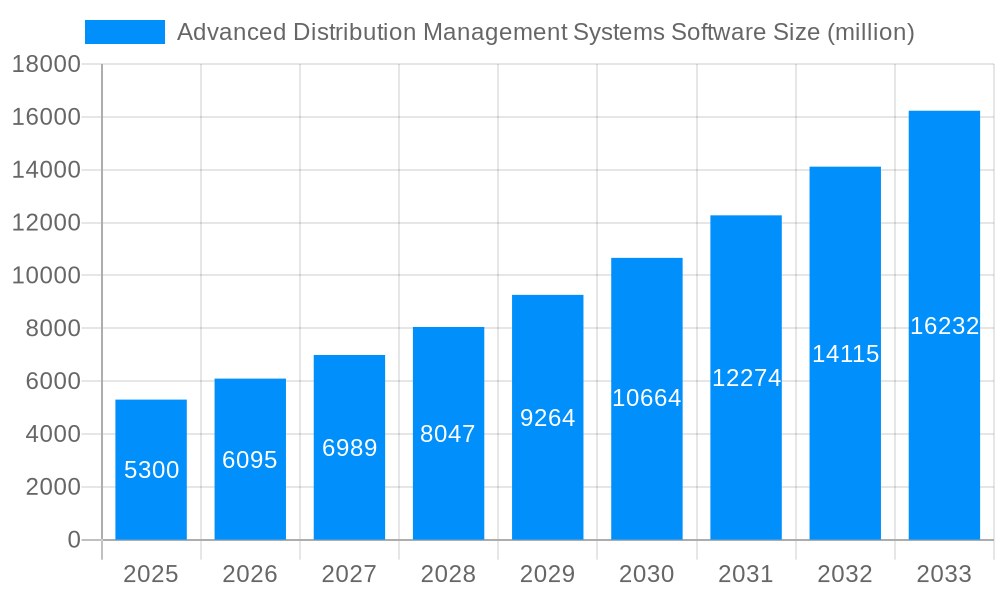

The Advanced Distribution Management Systems (ADMS) Software market is poised for significant expansion, projected to reach an estimated market size of $5,300 million in 2025, with a robust Compound Annual Growth Rate (CAGR) of 15.0% throughout the forecast period of 2025-2033. This upward trajectory is primarily fueled by the escalating need for enhanced grid reliability, operational efficiency, and the integration of renewable energy sources across utility sectors. As power grids become more complex with distributed energy resources (DERs) and smart grid technologies, ADMS software plays a crucial role in enabling real-time monitoring, control, and optimization of electricity distribution networks. The increasing focus on reducing energy losses, improving outage management, and ensuring grid resilience against cyber threats and extreme weather events are also key drivers propelling market growth. Furthermore, government initiatives promoting smart grid development and investments in modernizing aging infrastructure are creating substantial opportunities for ADMS providers.

The market is experiencing a pronounced shift towards cloud-based solutions, driven by their scalability, cost-effectiveness, and ease of deployment compared to traditional on-premises systems. While cloud adoption is rapidly gaining traction, on-premises solutions continue to hold relevance for entities with specific data security concerns or existing infrastructure investments. The application landscape is diverse, with significant adoption observed in Electric and Gas Utilities, where ADMS is integral to managing complex distribution operations. The Buildings and Facilities sector is also emerging as a key growth area, driven by the demand for smart building management and energy optimization. Other notable segments include Government, Mapping and Surveying, Mining, Rail and Transit, and Roads and Highways, all of which benefit from the enhanced operational visibility and control offered by ADMS. Leading companies such as Siemens, Oracle, GE, and AVEVA are at the forefront, innovating and expanding their offerings to meet the evolving demands of this dynamic market.

This report offers a comprehensive analysis of the global Advanced Distribution Management Systems (ADMS) Software market, projecting its trajectory through 2033. The study delves into the intricate dynamics that are reshaping how utilities and other industries manage their complex distribution networks. From optimizing energy flow and enhancing grid reliability to integrating renewable energy sources and driving operational efficiency, ADMS software is at the forefront of modern infrastructure management.

Our research encompasses a rigorous examination of market trends, drivers, challenges, and the competitive landscape, providing stakeholders with actionable insights. The report leverages data from the Historical Period (2019-2024) to establish a baseline, with the Base Year (2025) serving as a pivotal point for projections. The Study Period (2019-2033) allows for a nuanced understanding of long-term market evolution, while the Forecast Period (2025-2033) offers a clear outlook on future growth. We have meticulously analyzed the market in millions of units, providing quantitative data to support our qualitative assessments.

The global Advanced Distribution Management Systems (ADMS) Software market is currently experiencing a transformative surge, driven by an increasing demand for enhanced grid reliability, operational efficiency, and the integration of distributed energy resources (DERs). A significant trend observed is the accelerating adoption of Cloud-Based ADMS solutions. This shift away from traditional on-premises deployments is primarily motivated by the inherent scalability, flexibility, and cost-effectiveness offered by cloud infrastructure. Companies are increasingly recognizing the benefits of reduced upfront capital expenditure and the ability to rapidly deploy updates and new functionalities without the burden of extensive hardware management. This trend is particularly pronounced in the Electric and Gas Utilities segment, where the need to manage increasingly complex and dynamic power grids necessitates agile and responsive systems. The projected market growth in millions of units for cloud-based solutions is substantial, reflecting this paradigm shift.

Furthermore, the growing imperative to incorporate renewable energy sources such as solar and wind power into the existing grid infrastructure is acting as a powerful catalyst for ADMS adoption. These intermittent energy sources require sophisticated management capabilities to ensure grid stability and prevent disruptions. ADMS software, with its advanced forecasting, load balancing, and outage management features, is proving indispensable in this regard. We anticipate a significant increase in the deployment of ADMS across Electric and Gas Utilities to accommodate these evolving energy landscapes. The market's growth is also being fueled by government initiatives and regulatory mandates aimed at modernizing grid infrastructure and promoting energy efficiency. These policies are encouraging utilities to invest in advanced technologies like ADMS to meet compliance requirements and improve service delivery. The increasing complexity of urban infrastructure, particularly in Buildings and Facilities and Roads and Highways segments, also presents a growing avenue for ADMS application, as these areas demand sophisticated control and monitoring for optimal resource allocation and safety. The evolution of ADMS also encompasses enhanced functionalities like predictive analytics for equipment maintenance and real-time operational intelligence, moving beyond basic management to proactive optimization. The sheer volume of data generated by modern grids and connected devices is pushing ADMS solutions to become more data-intensive and analytical, a trend that will continue to define the market's evolution.

The market for Advanced Distribution Management Systems (ADMS) software is experiencing robust growth, propelled by a confluence of critical factors. Foremost among these is the escalating need for enhanced grid reliability and resilience in the face of increasingly frequent and severe weather events. Utilities worldwide are investing heavily in ADMS to proactively identify and mitigate potential outages, minimize downtime, and ensure the continuous delivery of essential services. This focus on grid modernization is directly supported by significant investments in new ADMS deployments, with projections indicating a substantial increase in the number of units implemented across the Electric and Gas Utilities sector.

Another key driver is the global push towards the integration of renewable energy sources. The decentralized nature of solar and wind power presents unique challenges for grid management, requiring sophisticated software to balance supply and demand, manage voltage fluctuations, and ensure grid stability. ADMS software, with its advanced forecasting and control capabilities, is crucial in enabling the seamless incorporation of these intermittent resources. Furthermore, the growing adoption of electric vehicles (EVs) and the subsequent increase in electricity demand are compelling utilities to optimize their distribution networks. ADMS plays a vital role in managing EV charging loads, preventing grid overload, and ensuring efficient energy distribution. The drive for operational efficiency and cost reduction within utility organizations also significantly contributes to ADMS market expansion. By automating processes, optimizing resource allocation, and providing real-time insights, ADMS helps utilities streamline operations, reduce manual intervention, and ultimately lower their operating expenses. The increasing regulatory pressure to improve grid performance, reduce carbon emissions, and meet sustainability targets further incentivizes the adoption of advanced ADMS solutions.

Despite the robust growth trajectory, the Advanced Distribution Management Systems (ADMS) Software market faces several significant challenges and restraints that could temper its expansion. A primary hurdle is the substantial upfront investment required for the implementation of comprehensive ADMS solutions. While cloud-based options are becoming more prevalent, many utilities, especially smaller ones or those in developing regions, may find the initial capital expenditure for hardware, software licenses, and system integration to be a significant deterrent. This is particularly true for organizations still reliant on legacy systems, where a complete overhaul can be a complex and costly undertaking. The On-Premises deployment model, while still relevant for some organizations with specific security or control requirements, often entails higher initial costs and ongoing maintenance expenses, further contributing to this restraint.

The complexity of integrating new ADMS software with existing, often disparate, legacy systems poses another considerable challenge. Utilities typically operate with a patchwork of older technologies, and ensuring seamless interoperability between these systems and a modern ADMS can be a time-consuming and technically demanding process, potentially leading to project delays and cost overruns. Furthermore, the shortage of skilled personnel capable of implementing, operating, and maintaining advanced ADMS platforms is a growing concern. The intricate nature of these systems requires specialized expertise in areas such as data analytics, cybersecurity, and grid operations, and a lack of qualified professionals can hinder widespread adoption and efficient utilization. Cybersecurity threats represent a persistent and evolving challenge. As ADMS systems become more interconnected and reliant on data, they become potential targets for cyberattacks, which could disrupt critical infrastructure and compromise sensitive information. Ensuring robust cybersecurity measures and continuous vigilance is paramount but also adds to the complexity and cost of implementation and operation. Finally, the resistance to change within established utility organizations can also act as a restraint. Shifting to new technologies and workflows often requires a cultural transformation, which can be met with internal inertia and a preference for familiar, albeit less efficient, processes.

The Electric and Gas Utilities segment is undeniably poised to dominate the global Advanced Distribution Management Systems (ADMS) Software market throughout the study period. This dominance stems from the inherent and critical need for sophisticated grid management within this sector. Utilities are grappling with an unprecedented transformation of their operational landscapes, driven by several interconnected forces.

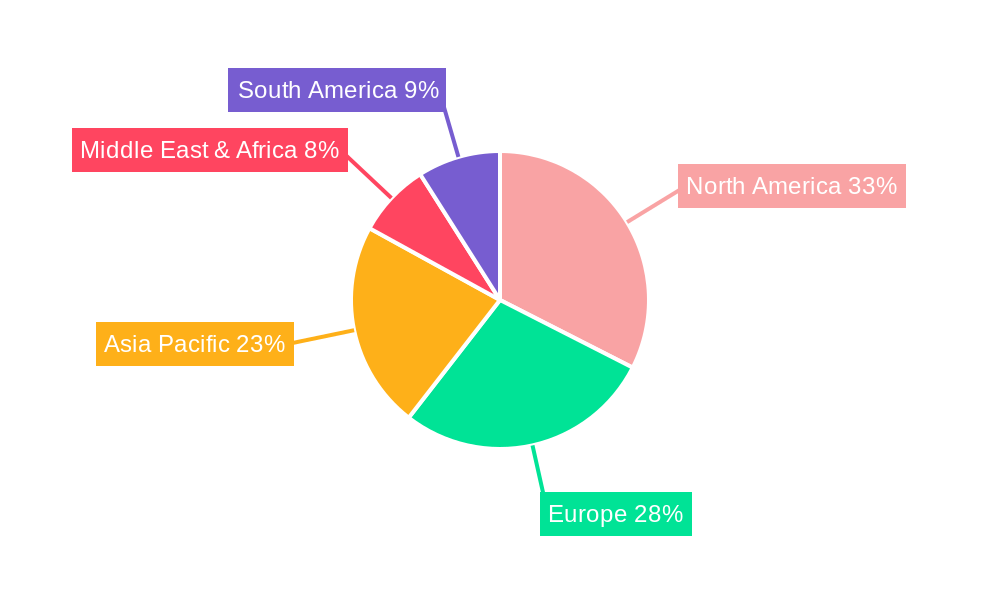

The North America region, particularly the United States, is expected to be a leading market for ADMS software within the Electric and Gas Utilities segment. This is attributed to several factors:

While North America is projected to lead, other regions such as Europe and Asia-Pacific are also expected to witness significant growth, driven by similar trends of grid modernization, renewable energy integration, and increasing electricity demand. The market in these regions is dynamic, with specific countries exhibiting strong growth potential based on their individual energy policies and infrastructure development plans. The application of ADMS in segments like Buildings and Facilities and Roads and Highways will also see a steady rise, but the sheer scale of operations and the critical nature of power supply will ensure that Electric and Gas Utilities remain the dominant force in the ADMS software market. The sheer volume of millions of units of electricity and gas distributed daily underscores the indispensable role of ADMS in this segment.

The growth of the Advanced Distribution Management Systems (ADMS) Software industry is being significantly accelerated by several key catalysts. The global drive towards a cleaner energy future, characterized by the increasing integration of renewable energy sources like solar and wind power, necessitates sophisticated grid management capabilities that ADMS provides. Furthermore, the accelerating adoption of electric vehicles (EVs) and the resulting surge in electricity demand are compelling utilities to optimize their distribution networks, a task where ADMS plays a crucial role. Government mandates and initiatives focused on grid modernization, reliability enhancement, and decarbonization are also acting as powerful growth drivers, encouraging significant investment in ADMS solutions. The continuous advancement in IoT (Internet of Things) technology, enabling greater data collection and real-time monitoring, fuels the demand for intelligent ADMS platforms capable of processing and analyzing this vast amount of information for improved decision-making.

The global Advanced Distribution Management Systems (ADMS) Software market is characterized by the presence of several prominent players, each contributing significantly to the innovation and adoption of these critical systems. The following companies are at the forefront:

The Advanced Distribution Management Systems (ADMS) Software sector has witnessed several pivotal developments that have shaped its evolution and continue to influence its future trajectory:

This report provides an exhaustive analysis of the Advanced Distribution Management Systems (ADMS) Software market, offering a deep dive into its current state and future projections. It meticulously examines market size in millions of units, historical trends from 2019-2024, and forecasts up to 2033, with 2025 serving as the base year. The study breaks down the market by deployment types (Cloud-Based, On-Premises) and application segments (Buildings and Facilities, Electric and Gas Utilities, Government, Mapping and Surveying, Mining, Rail and Transit, Roads and Highways), identifying key growth drivers and potential restraints. It highlights the dominant regions and segments, while also profiling leading market players and their contributions. The report's comprehensive coverage ensures that stakeholders are equipped with the necessary insights to navigate this dynamic and rapidly evolving market, enabling informed strategic decision-making.

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 32.2% from 2020-2034 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately 32.2%.

Key companies in the market include Advanced Control Systems, Oracle, ABB, OSI Hardware, AVEVA, GE, Survalent Technology, Axxiom, Siemens, Indra, Hewlett Packard Enterprise (HPE), .

The market segments include Type, Application.

The market size is estimated to be USD 3.83 billion as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3480.00, USD 5220.00, and USD 6960.00 respectively.

The market size is provided in terms of value, measured in billion.

Yes, the market keyword associated with the report is "Advanced Distribution Management Systems Software," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Advanced Distribution Management Systems Software, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.