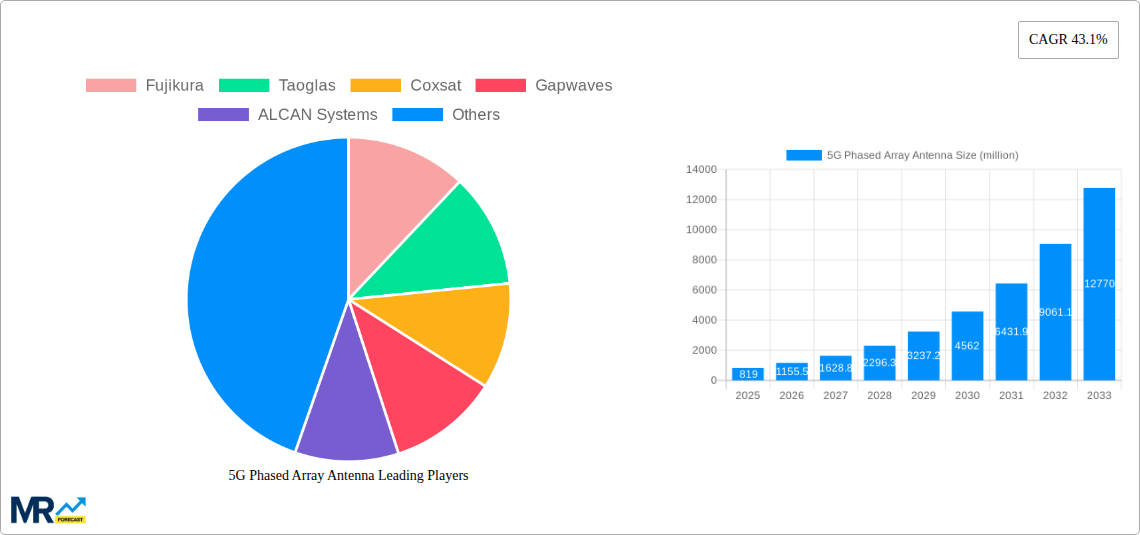

1. What is the projected Compound Annual Growth Rate (CAGR) of the 5G Phased Array Antenna?

The projected CAGR is approximately 43.1%.

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

5G Phased Array Antenna

5G Phased Array Antenna5G Phased Array Antenna by Type (24-30 GHz, Others), by Application (5G Infrastructure, Others), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2025-2033

The global 5G Phased Array Antenna market is experiencing explosive growth, projected to reach $819 million by 2025, driven by an unprecedented Compound Annual Growth Rate (CAGR) of 43.1%. This remarkable expansion is fundamentally fueled by the relentless global rollout of 5G infrastructure. As telecommunication companies invest heavily in upgrading their networks to support higher speeds, lower latency, and increased connectivity, the demand for advanced phased array antennas, crucial for beamforming and efficient signal management, is surging. The 24-30 GHz frequency band is a primary driver, offering significant bandwidth for enhanced 5G services. This surge in demand is further amplified by the increasing adoption of 5G in various applications beyond traditional mobile communication, including enterprise networks, the Internet of Things (IoT), and advanced automotive systems. The market's trajectory is characterized by rapid technological advancements, with ongoing innovation in antenna design and material science enhancing performance and reducing costs, thereby accelerating market penetration.

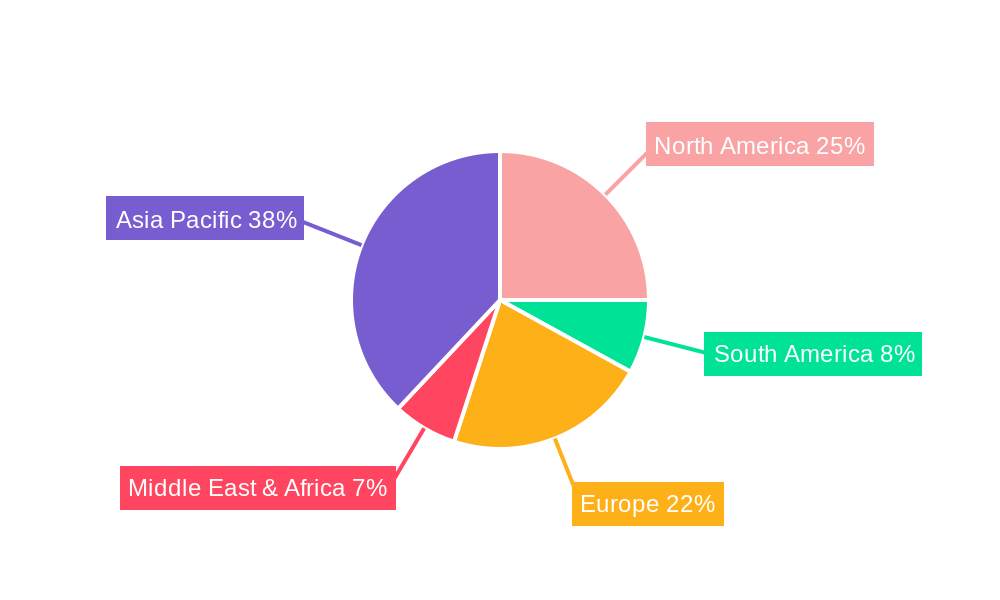

The market is poised for sustained expansion, with key players like Fujikura, Taoglas, and Coxsat actively innovating and expanding their product portfolios to cater to the diverse needs of the 5G ecosystem. While the adoption of 5G infrastructure is the dominant growth driver, other applications are also contributing to the market's momentum. However, certain factors could present challenges. The high initial cost of advanced phased array antennas, coupled with the complex integration process into existing networks, might pose some restraints to immediate widespread adoption in certain budget-constrained regions or for smaller-scale deployments. Geographically, Asia Pacific, led by China, is expected to dominate the market, owing to its aggressive 5G deployment strategies and manufacturing capabilities. North America and Europe are also significant markets, driven by substantial investments in 5G infrastructure and a growing demand for high-performance wireless solutions. The study period from 2019-2033, with a base year of 2025, indicates a long-term outlook for robust growth, reflecting the enduring transformative impact of 5G technology.

This comprehensive report delves into the dynamic landscape of the 5G phased array antenna market, offering an in-depth analysis of trends, driving forces, challenges, and future growth opportunities. Spanning a study period from 2019 to 2033, with a Base Year and Estimated Year of 2025, and a detailed Forecast Period of 2025-2033, this report leverages historical data from 2019-2024 to provide robust projections and actionable insights. We examine the market across key segments, including antenna Type (24-30 GHz and Others) and Application (5G Infrastructure and Others), with a specific focus on the burgeoning millimeter-wave frequencies crucial for advanced 5G deployments. The report quantifies market estimations in the millions of units, providing a clear picture of the scale and potential of this critical technology.

The global 5G phased array antenna market is experiencing a transformative surge, driven by the relentless pursuit of enhanced mobile broadband, ultra-reliable low-latency communication, and massive machine-type communication. The transition from sub-6 GHz to millimeter-wave (mmWave) frequencies, particularly in the 24-30 GHz spectrum, is a defining trend. This shift is necessitated by the need for wider bandwidths to support the exponentially increasing data demands of 5G services. Phased array antennas are the cornerstone of these mmWave deployments, enabling beamforming capabilities that precisely direct radio signals, thereby overcoming the inherent propagation challenges of higher frequencies. The market is witnessing a significant increase in the deployment of small cells and base stations equipped with these advanced antennas. Furthermore, the integration of artificial intelligence (AI) and machine learning (ML) within antenna systems for adaptive beam management and interference mitigation is becoming increasingly prevalent. This intelligent approach promises to optimize network performance and user experience, paving the way for more efficient and responsive 5G networks. The demand for miniaturization and cost-effectiveness in phased array antenna designs is also a key trend, as manufacturers strive to integrate these sophisticated components into a wider range of devices and infrastructure elements. The evolving regulatory landscape and spectrum allocation strategies globally are also shaping deployment patterns and antenna technology advancements. As the 5G ecosystem matures, the focus is shifting towards enabling more immersive applications like augmented reality (AR), virtual reality (VR), and advanced industrial automation, all of which heavily rely on the high-performance capabilities offered by phased array antennas. The market is expected to see a substantial increase in the adoption of these antennas beyond traditional telecommunications infrastructure, including enterprise networks, private 5G deployments, and even in emerging IoT applications demanding robust connectivity.

The exponential growth of the 5G phased array antenna market is underpinned by a confluence of powerful driving forces. Foremost among these is the escalating demand for higher data speeds and increased network capacity to support the burgeoning ecosystem of connected devices and data-intensive applications. The widespread adoption of smartphones, IoT devices, and the increasing reliance on cloud-based services are placing unprecedented pressure on existing network infrastructure, making the capabilities of 5G, and by extension, phased array antennas, indispensable. Governments worldwide are actively promoting 5G deployment through favorable policies and spectrum auctions, recognizing its strategic importance for economic growth and digital transformation. This proactive regulatory support acts as a significant catalyst, accelerating the rollout of 5G networks and consequently, the demand for phased array antennas. The ongoing evolution of applications such as augmented reality (AR), virtual reality (VR), autonomous vehicles, and smart cities necessitates the low latency and high bandwidth that 5G, enabled by phased array technology, can deliver. These transformative applications are not merely incremental improvements but represent paradigm shifts in how we interact with technology and the world around us, directly fueling the need for advanced antenna solutions. Furthermore, the continuous innovation in semiconductor technology and antenna design is leading to more compact, power-efficient, and cost-effective phased array antennas, making their integration into diverse infrastructure and devices more feasible. The strategic investments made by telecommunications operators and technology providers in 5G research and development are also crucial in driving the adoption and advancement of phased array antenna technology.

Despite the robust growth trajectory, the 5G phased array antenna market is not without its hurdles. One of the primary challenges is the significant cost of advanced phased array antenna components, particularly those designed for mmWave frequencies. The intricate manufacturing processes and the need for specialized materials contribute to higher unit costs, which can be a deterrent for widespread adoption, especially in price-sensitive markets. Furthermore, the complexity of integrating phased array antennas into existing infrastructure and devices poses technical challenges. Beamforming algorithms require sophisticated control and calibration, demanding specialized expertise and potentially leading to longer deployment cycles. The propagation characteristics of millimeter-wave frequencies, while offering high bandwidth, are also a significant restraint. These frequencies are susceptible to blockage by obstacles such as buildings, foliage, and even rain, necessitating a denser deployment of base stations and advanced beam management techniques to ensure reliable connectivity. Power consumption associated with active phased array antennas, especially when operating at higher frequencies and with numerous elements, can also be a concern, requiring efficient power management solutions. The short supply chain for critical components and the reliance on a limited number of specialized manufacturers can create bottlenecks and impact production volumes. Finally, spectrum interference and regulatory hurdles related to the allocation and utilization of specific frequency bands for 5G services can also pose challenges to market expansion.

The 5G Infrastructure segment, particularly within the 24-30 GHz frequency band, is poised to dominate the 5G phased array antenna market. This dominance is largely attributed to the fundamental requirements of current and future 5G network deployments. As telecommunication operators globally race to roll out their 5G networks, the demand for robust and high-performance infrastructure components, including phased array antennas, is paramount. The 24-30 GHz spectrum is critically important for delivering the ultra-high speeds and low latency promised by 5G, especially for dense urban areas and enterprise applications. These frequencies offer substantial bandwidth, enabling technologies like Fixed Wireless Access (FWA), enhanced mobile broadband, and the foundation for advanced IoT applications.

Key Regions Dominating the Market:

The 5G Infrastructure application segment is projected to account for the largest market share due to the ongoing build-out of macro base stations, small cells, and other network elements essential for widespread 5G coverage. The 24-30 GHz type segment is gaining significant traction as it is crucial for unlocking the full potential of 5G, especially for higher capacity and lower latency services, directly influencing the demand for the sophisticated beamforming capabilities offered by phased array antennas. The sustained investment in network densification and the need to support evolving 5G use cases will ensure the continued dominance of these segments throughout the forecast period.

Several factors are acting as potent growth catalysts for the 5G phased array antenna industry. The relentless expansion of 5G networks globally, fueled by government support and operator investments, is the primary driver. The increasing demand for high-speed data and low-latency applications, such as AR, VR, and autonomous systems, necessitates the advanced capabilities of phased array antennas. Furthermore, the development of more compact, energy-efficient, and cost-effective antenna designs is expanding their applicability across a wider range of devices and infrastructure. The growing adoption of private 5G networks for industrial and enterprise use cases also presents a significant new avenue for growth.

This report provides a comprehensive analysis of the 5G phased array antenna market, offering invaluable insights for stakeholders. It meticulously covers market size estimations in millions of units, forecasts market growth across key segments including 24-30 GHz type and 5G Infrastructure application, and analyzes the competitive landscape. The report details driving forces, challenges, regional market dynamics, and significant industry developments. With data spanning from 2019 to 2033, including a detailed Base Year (2025) and Forecast Period (2025-2033), it equips businesses with the knowledge to strategize effectively, identify opportunities, and navigate the evolving market.

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

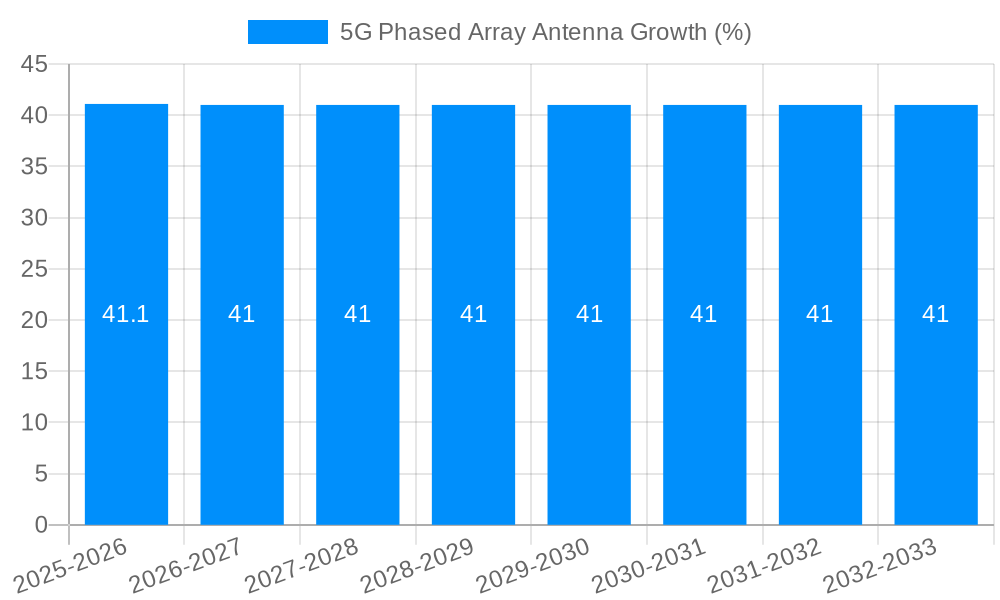

| Growth Rate | CAGR of 43.1% from 2019-2033 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately 43.1%.

Key companies in the market include Fujikura, Taoglas, Coxsat, Gapwaves, ALCAN Systems, T-Ray, Movandi Corporation, Doosan.

The market segments include Type, Application.

The market size is estimated to be USD 819 million as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3480.00, USD 5220.00, and USD 6960.00 respectively.

The market size is provided in terms of value, measured in million and volume, measured in K.

Yes, the market keyword associated with the report is "5G Phased Array Antenna," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the 5G Phased Array Antenna, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.