1. What is the projected Compound Annual Growth Rate (CAGR) of the 3D Printing in Industrial?

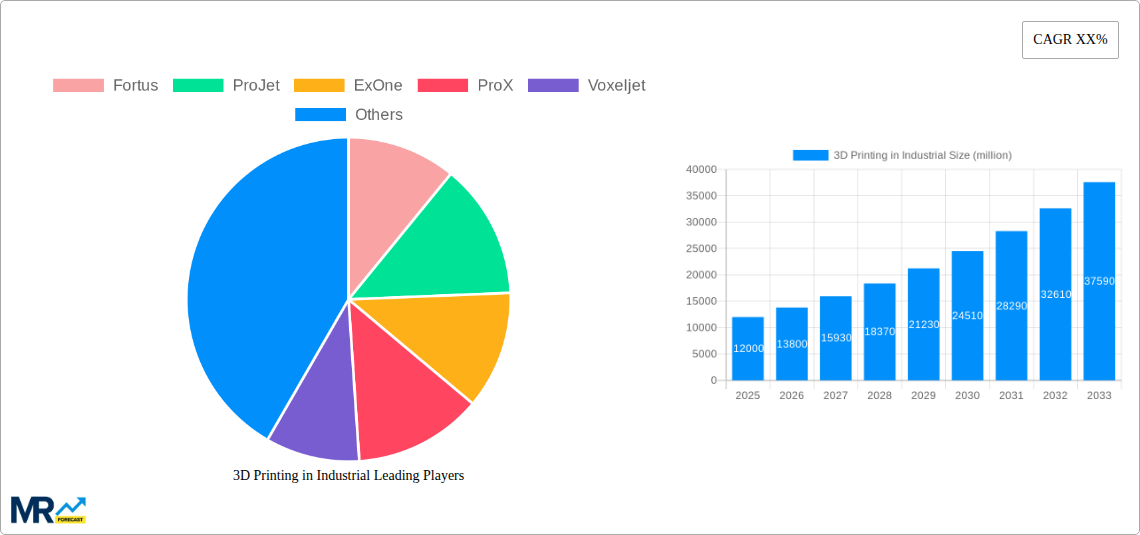

The projected CAGR is approximately 20.8%.

3D Printing in Industrial

3D Printing in Industrial3D Printing in Industrial by Type (Stereolithography (SLA), Fused Deposition Modeling (FDM), Selective Laser Sintering (SLS), Direct Metal Laser Sintering (DMLS), PolyJet Printing (MJP), Inkjet Printing, Electron Beam Melting (EBM), Laser Metal Deposition (LMD), Direct Light Projection (DLP), Laminated Object Manufacturing (LOM)), by Application (Automotive, Aerospace & Defense, Healthcare, Printed Electronics, Foundry & Forging, Food & Culinary, Jewelry, Other), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2026-2034

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

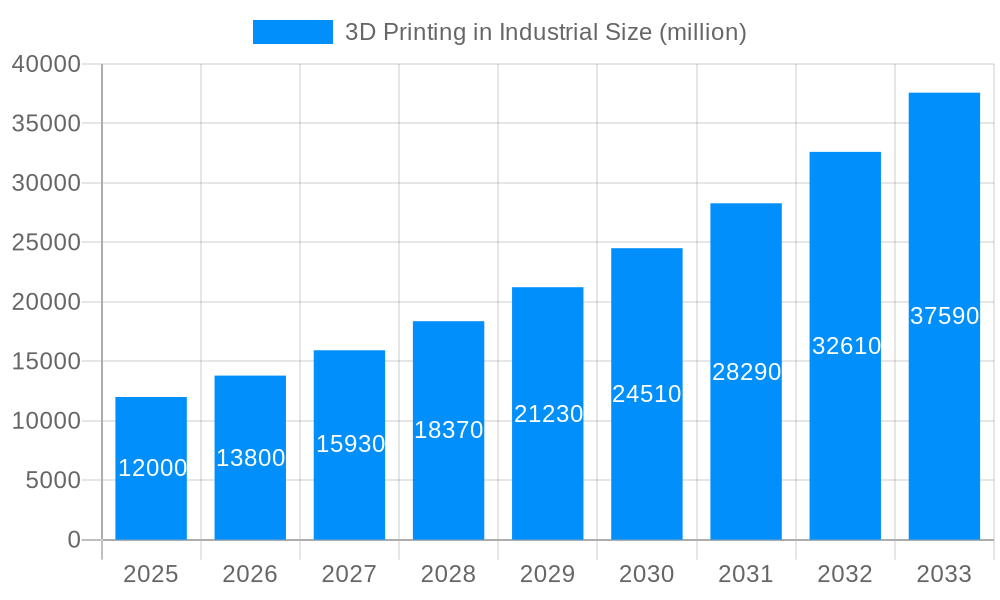

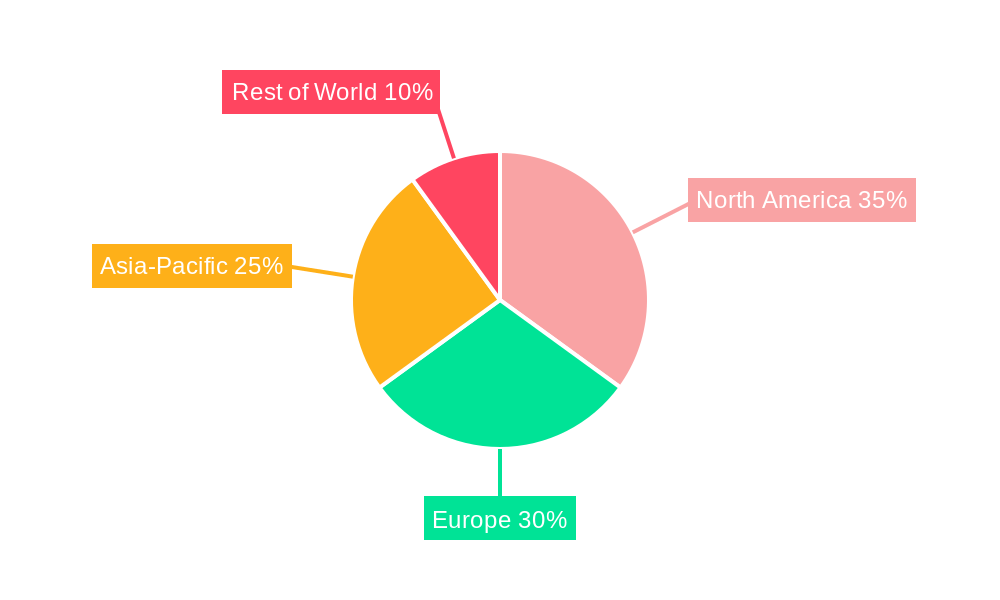

The industrial 3D printing market is experiencing robust growth, driven by increasing adoption across diverse sectors. The market, estimated at $15 billion in 2025, is projected to witness a Compound Annual Growth Rate (CAGR) of 18% from 2025 to 2033, reaching an estimated $45 billion by 2033. This expansion is fueled by several key factors: the rising need for customized and lightweight components in automotive and aerospace applications, the growing demand for personalized medical devices and prosthetics in healthcare, and the increasing use of 3D printing in rapid prototyping and tooling across various industries. Furthermore, advancements in additive manufacturing technologies, such as improved material properties and faster printing speeds, are significantly contributing to market growth. The dominance of Stereolithography (SLA) and Fused Deposition Modeling (FDM) technologies is expected to continue, although the adoption of metal-based technologies like Direct Metal Laser Sintering (DMLS) and Electron Beam Melting (EBM) is poised for significant expansion due to their use in high-value applications. Geographic distribution shows North America and Europe currently holding the largest market share, but the Asia-Pacific region is anticipated to demonstrate the fastest growth, fueled by increasing industrialization and technological advancements in countries like China and India.

Despite the positive outlook, certain restraints impact the market's trajectory. High initial investment costs associated with 3D printing equipment and materials can be a barrier for entry for smaller businesses. Furthermore, the need for skilled operators and the potential for inconsistencies in print quality remain challenges that need to be addressed. However, ongoing technological advancements, coupled with increasing awareness of the benefits of additive manufacturing, are gradually mitigating these challenges. The ongoing development of new materials with enhanced properties, alongside the increasing availability of user-friendly software and improved post-processing techniques, will continue to drive market adoption and propel growth throughout the forecast period. Specific segments like aerospace & defense and healthcare are demonstrating particularly strong growth, driven by the unique advantages 3D printing offers in creating complex geometries and highly customized parts.

The industrial 3D printing market is experiencing explosive growth, projected to reach tens of billions of dollars by 2033. From 2019 to 2024, the historical period showed significant advancements in technology and adoption across diverse sectors. The estimated market value in 2025 is already in the multi-billion-dollar range, indicating a substantial acceleration in the forecast period (2025-2033). This expansion is driven by several factors, including the increasing demand for customized products, the need for faster prototyping, and the desire to reduce production costs. The market is characterized by continuous innovation in printing technologies, materials, and software, leading to a wider range of applications and improved efficiency. Key trends include the rise of additive manufacturing for high-value parts in aerospace and medical applications, the integration of 3D printing into existing production lines, and the growing importance of sustainable and biocompatible materials. Furthermore, the development of hybrid manufacturing processes, combining additive and subtractive techniques, is optimizing production workflows and enhancing final product quality. The shift towards digitalization and Industry 4.0 is further bolstering the adoption of 3D printing, facilitating greater connectivity and data-driven optimization within industrial settings. This interconnectedness enables real-time monitoring, predictive maintenance, and enhanced overall productivity. The increasing availability of affordable and user-friendly 3D printing solutions is further democratizing access to this transformative technology, expanding its reach beyond large corporations to SMEs and individual innovators. This expansion fuels competition and innovation across the industry value chain.

Several key factors are accelerating the adoption of 3D printing in industrial settings. Firstly, the ability to produce highly customized and complex parts on demand is a game-changer. This eliminates the need for expensive tooling and allows for rapid iteration of designs, shortening lead times and accelerating product development cycles. Secondly, the increasing efficiency and cost-effectiveness of 3D printing technologies are making them increasingly competitive with traditional manufacturing processes, especially for smaller production runs and specialized components. The potential for reduced material waste and energy consumption further enhances the economic viability of 3D printing. Thirdly, the expanding range of materials compatible with 3D printing is broadening the scope of applications. From metals and polymers to ceramics and composites, manufacturers can now choose the optimal material for specific performance requirements. This material diversity unlocks new possibilities across various industries. Fourthly, growing technological advancements, including improved software and automation, contribute to the increased speed, precision, and reliability of 3D printing processes. Lastly, government initiatives and investments in additive manufacturing research and development are further fostering innovation and adoption in the industrial sector.

Despite its immense potential, the widespread adoption of 3D printing in industrial settings still faces several challenges. The relatively high initial investment cost of 3D printing equipment can be a barrier for smaller companies with limited budgets. The need for skilled operators and technicians to manage the complex processes is another hurdle. Furthermore, the relatively slower production speed compared to traditional mass production methods can limit its suitability for high-volume manufacturing needs. The scalability of 3D printing for large-scale production remains a challenge, especially for some technologies. Quality control and consistency can also be more difficult to maintain compared to established manufacturing techniques, necessitating robust quality assurance processes. Concerns about intellectual property protection and the potential for counterfeiting also require careful consideration. Finally, the availability of suitable materials and the need for continuous material development limit the application range of certain 3D printing technologies. Addressing these challenges requires continued innovation in technology, cost reduction strategies, and the development of standardized quality control protocols.

The industrial 3D printing market is witnessing strong growth across various regions, with North America and Europe currently leading the way due to established manufacturing industries and early adoption of the technology. However, Asia-Pacific is expected to experience the fastest growth in the coming years, driven by rapid industrialization and increasing investments in advanced manufacturing technologies. Within specific segments, the aerospace and defense sector is a major driver, demanding high-precision and lightweight components often uniquely suited to additive manufacturing. The medical industry is another significant adopter, utilizing 3D printing for customized implants, prosthetics, and surgical tools. The automotive sector is increasingly using 3D printing for prototyping and the production of specialized parts.

The paragraph above explains the dominance of certain geographical areas and sectors. The high precision and functionality offered by DMLS, SLS, and SLA make them ideal for the high-stakes applications in aerospace and medical industries, driving their market dominance. The cost-effectiveness of FDM makes it popular for prototyping and smaller-scale production. The versatility of PolyJet is a key factor in its rising popularity.

The industrial 3D printing market is fueled by several significant growth catalysts. The ongoing miniaturization and enhancement of 3D printing technology, combined with reductions in manufacturing costs, make the technology increasingly accessible. The growing demand for customized products across various industries, including automotive, aerospace, and healthcare, further propels the adoption of additive manufacturing. Government initiatives promoting research and development in 3D printing, coupled with increasing private investments, are fostering innovation and driving market growth. The integration of 3D printing into smart factories and Industry 4.0 environments also enhances efficiency and productivity, further contributing to its widespread adoption.

This report offers a comprehensive overview of the 3D printing in industrial market, providing detailed analysis of market trends, growth drivers, challenges, and leading players. It examines various printing technologies and their applications across different industries, offering valuable insights for businesses seeking to leverage the transformative potential of additive manufacturing. The report also provides market forecasts, enabling informed decision-making and strategic planning for the future. Detailed regional and segment analysis provides a granular perspective, enabling a deeper understanding of market dynamics.

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 20.8% from 2020-2034 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately 20.8%.

Key companies in the market include Fortus, ProJet, ExOne, ProX, Voxeljet, Magicfirm, 3D Systems Corporation, Stratasys, EOS, Materialise NV, EnvisionTEC, Arcam AB, Concept Laser, Optomec, SLM Solutions Group, Groupe Gorge, Renishaw, Koninklijke, Hoganas, ARC Group Worldwide, Markforged, Cookson Precious Metals, Sculpteo, .

The market segments include Type, Application.

The market size is estimated to be USD 16.75 billion as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3480.00, USD 5220.00, and USD 6960.00 respectively.

The market size is provided in terms of value, measured in billion.

Yes, the market keyword associated with the report is "3D Printing in Industrial," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the 3D Printing in Industrial, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.