1. What is the projected Compound Annual Growth Rate (CAGR) of the Zero Trust SDP?

The projected CAGR is approximately XX%.

Zero Trust SDP

Zero Trust SDPZero Trust SDP by Type (Cloud Based, On-premise), by Application (Finance, Government, Education, Healthcare, Others), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2026-2034

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

The Zero Trust Software Defined Perimeter (SDP) market is experiencing robust growth, driven by the escalating need for enhanced cybersecurity in a distributed and increasingly cloud-based work environment. The market's expansion is fueled by several key factors: the rising adoption of cloud computing, the increasing frequency and sophistication of cyberattacks targeting enterprise networks, and the growing awareness of the limitations of traditional perimeter-based security models. Businesses across various sectors, including finance, government, healthcare, and education, are actively seeking robust solutions to protect sensitive data and applications from unauthorized access, regardless of location or device. The shift towards remote work, accelerated by recent global events, has further intensified this demand. While on-premise deployments still hold a significant share, cloud-based SDP solutions are experiencing faster growth rates due to their scalability, flexibility, and cost-effectiveness. Competition among vendors is fierce, with established players and innovative startups vying for market share. This competitive landscape fosters innovation and drives down costs, making Zero Trust SDP solutions accessible to a broader range of organizations.

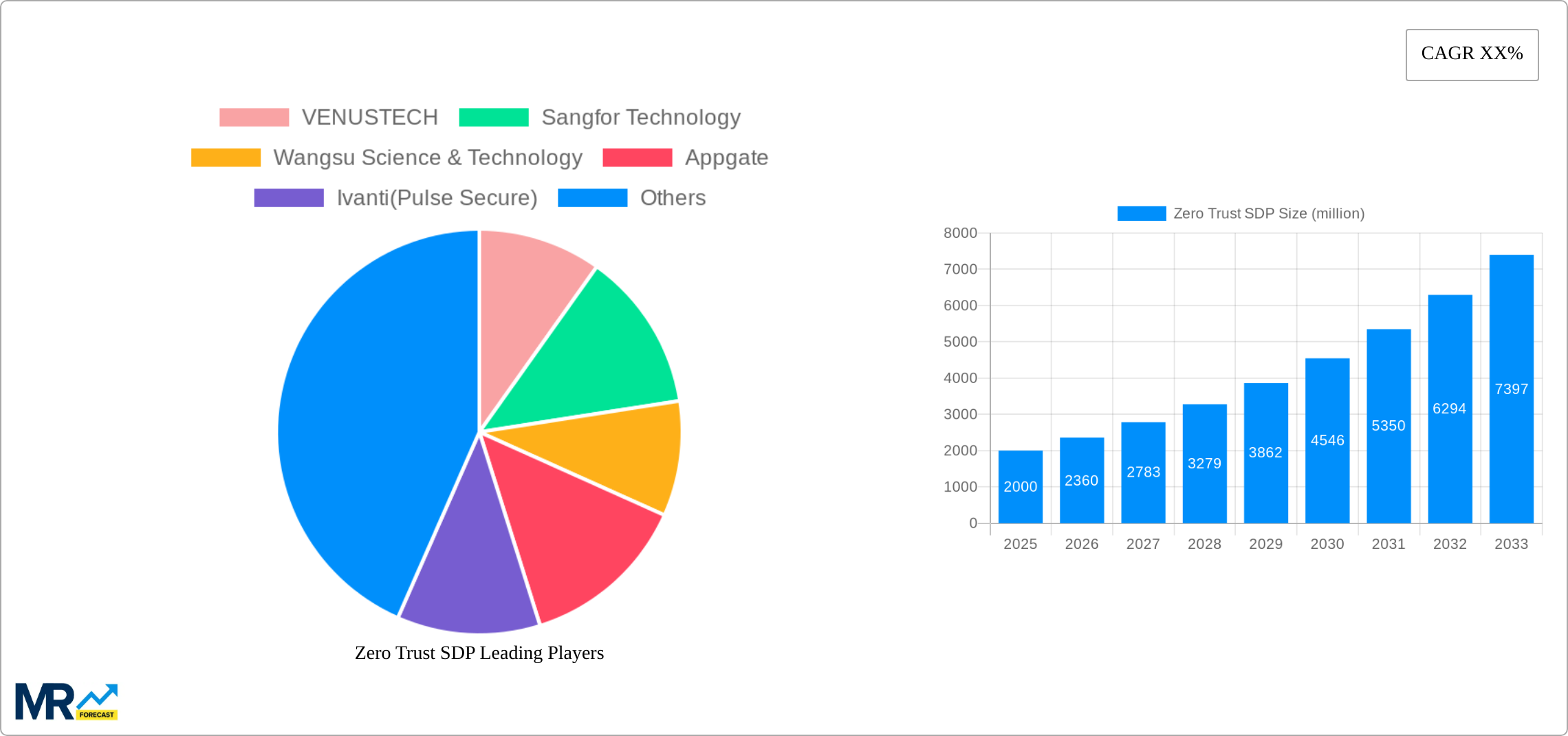

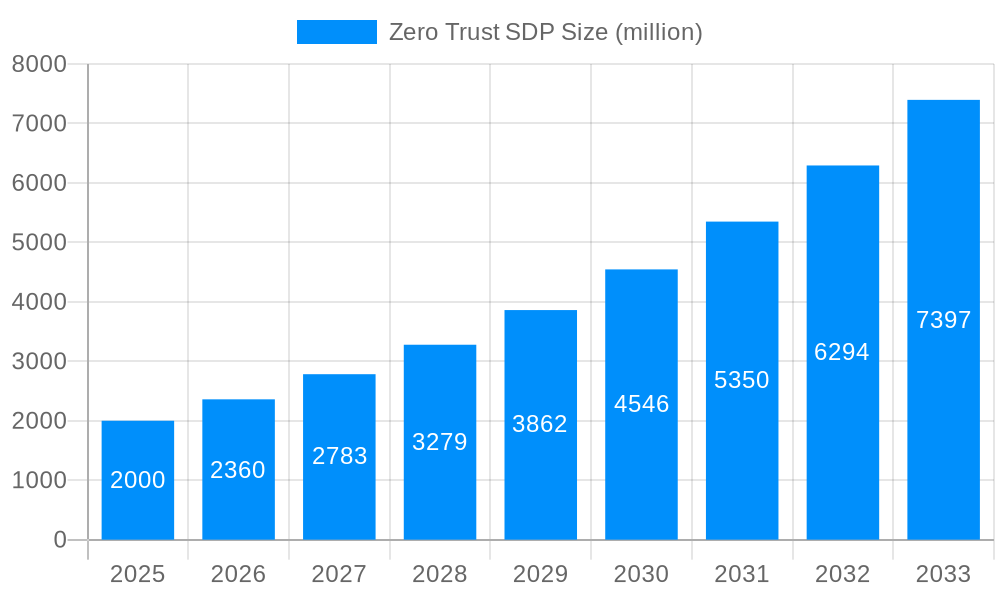

A conservative estimate places the 2025 Zero Trust SDP market size at $2 billion, projecting a Compound Annual Growth Rate (CAGR) of 18% over the forecast period (2025-2033). This growth is expected to be particularly strong in regions like North America and Asia Pacific, driven by high technology adoption rates and stringent data privacy regulations. However, factors such as the complexity of implementation and the need for skilled professionals to manage these systems could pose challenges to broader adoption. Nevertheless, the long-term outlook for the Zero Trust SDP market remains positive, with continuous innovation and evolving market needs driving further expansion. The diverse range of applications across different sectors suggests continued high demand.

The Zero Trust Software Defined Perimeter (SDP) market is experiencing explosive growth, projected to reach multi-billion dollar valuations by 2033. Our comprehensive report, covering the period from 2019 to 2033, reveals a significant upswing in adoption driven by escalating cyber threats and the increasing need for robust network security across diverse sectors. The historical period (2019-2024) saw a steady rise in awareness and initial deployments, largely concentrated within the finance and government sectors. However, the estimated year (2025) marks a turning point, with substantial growth projected throughout the forecast period (2025-2033). This expansion is fueled by several factors: the maturation of cloud-based SDP solutions, increasing regulatory pressure mandating enhanced security protocols, and a growing understanding of the limitations of traditional perimeter-based security models. Key market insights indicate a preference for cloud-based solutions due to their scalability and ease of deployment, especially amongst smaller organizations. Simultaneously, larger enterprises, particularly in finance and government, are heavily investing in on-premise solutions for greater control and compliance. The market is witnessing innovation in various application segments, with healthcare showing impressive growth potential due to increasingly stringent data privacy regulations and the sensitive nature of patient information. The competitive landscape is dynamic, with both established players and emerging startups vying for market share through strategic partnerships, product innovation, and aggressive marketing campaigns. This report provides detailed analysis of market size, segmentation by type (cloud-based, on-premise), application (finance, government, education, healthcare, others), and geographical distribution, providing crucial insights for stakeholders considering investments or strategic partnerships within this rapidly evolving market. Millions of devices are projected to be secured under Zero Trust SDP architectures by the end of the forecast period.

The surge in adoption of Zero Trust SDP is primarily driven by a confluence of factors. The increasing sophistication and frequency of cyberattacks, including ransomware and data breaches, have forced organizations to re-evaluate their security postures. Traditional perimeter-based security models, which rely on a trusted network, are proving inadequate in the face of modern threats. Zero Trust SDP offers a significant upgrade, focusing on verification and authorization of every access request regardless of location, thus mitigating the risk of lateral movement within a compromised network. The rise of remote work and cloud adoption further accelerates this trend. Employees accessing corporate resources from diverse locations and devices necessitate a security framework that transcends geographical boundaries and device types. Zero Trust SDP fits this need perfectly. Moreover, regulatory mandates and compliance requirements, particularly in highly regulated industries like finance and healthcare, mandate enhanced data protection measures. Zero Trust SDP aligns with these regulations, providing organizations with a verifiable path to compliance and reducing the risk of penalties. The continuous evolution of technology itself plays a role; improved automation capabilities, easier integration with existing security systems, and reduced complexity in deployment and management are driving wider adoption. Furthermore, the increasing awareness amongst organizations about the financial and reputational damage associated with data breaches encourages proactive investment in robust security measures like Zero Trust SDP.

Despite the significant advantages, the widespread adoption of Zero Trust SDP faces several challenges. The initial investment costs associated with implementation, including hardware, software, and professional services, can be substantial, particularly for smaller organizations. This can act as a barrier to entry, limiting adoption in certain market segments. Furthermore, the complexity involved in integrating Zero Trust SDP with existing network infrastructure and security systems presents a significant hurdle. Organizations may require specialized expertise and resources for seamless integration, potentially leading to delays and increased costs. Concerns around potential performance impacts and latency issues due to the increased authentication and authorization checks can also hinder adoption. Organizations need to carefully plan their implementation to minimize the impact on user experience. A lack of skilled professionals proficient in deploying and managing Zero Trust SDP solutions poses another constraint. The demand for skilled cybersecurity professionals far exceeds the supply, creating a talent gap that can limit the market's growth. Finally, the continuous evolution of cyber threats requires ongoing investment in updates, patches, and new security technologies to maintain effectiveness. This ongoing operational cost can be a deterrent for some organizations.

The Finance sector is poised to dominate the Zero Trust SDP market, fueled by stringent regulatory compliance requirements and the high value of sensitive financial data. The sector's robust financial capabilities also contribute to faster adoption of cutting-edge technologies like Zero Trust SDP.

High Value of Data: The finance industry handles highly sensitive and valuable data, making it a prime target for cyberattacks. Zero Trust's granular access control significantly reduces the risk of data breaches and resulting financial losses, driving high adoption rates.

Stringent Regulatory Compliance: Financial institutions operate under strict regulatory scrutiny, with mandates to ensure data privacy and security. Zero Trust SDP directly supports compliance with regulations like GDPR, CCPA, and others, making its implementation a necessity.

High Investment Capacity: Financial institutions possess the resources to invest in sophisticated security solutions like Zero Trust SDP, making them early adopters and key drivers of market growth.

Increased Threat Landscape: The finance industry experiences an extremely high volume of sophisticated and persistent cyberattacks, significantly raising their awareness and need for robust security measures. Zero Trust SDP is viewed as a critical tool in this high-risk environment.

Focus on Risk Mitigation: Financial institutions prioritize risk mitigation and loss prevention. Zero Trust's inherent ability to minimize exposure by verifying every access request aligns perfectly with this priority.

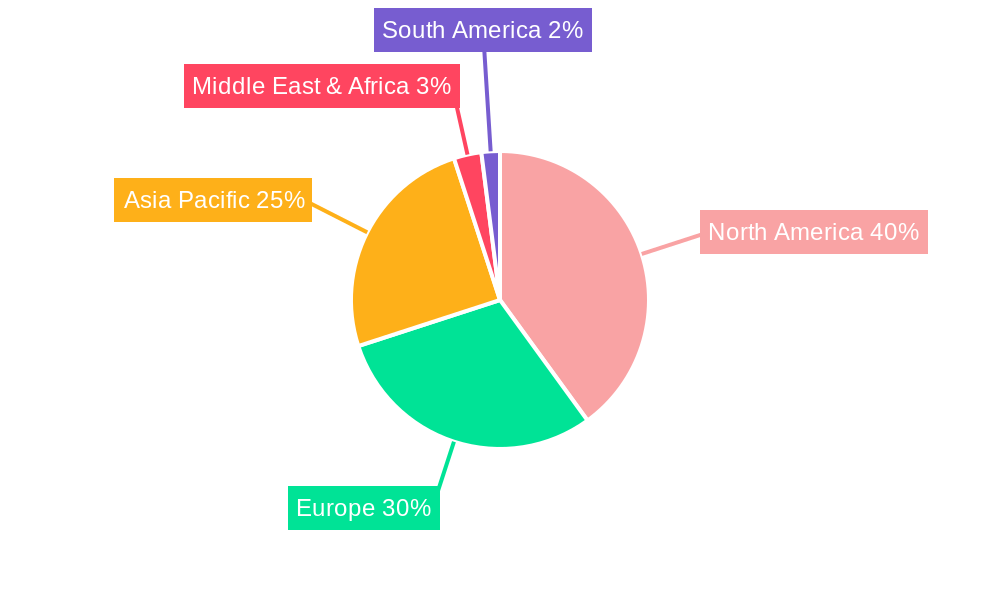

Furthermore, the North American region is anticipated to lead the global market in terms of adoption and revenue. This is attributable to its high concentration of financial institutions, mature technology infrastructure, and proactive regulatory landscape driving demand for advanced security solutions. Early adoption by large financial organizations in North America is paving the way for wider adoption across various segments within the region. European countries are also projected to show substantial growth due to the influence of GDPR and other data privacy regulations. Asia Pacific follows, with rapidly developing economies and rising digitalization creating increasing demand for robust cybersecurity measures.

The Zero Trust SDP industry’s growth is fueled by increasing cyber threats, the adoption of cloud and remote work models, tightening regulations requiring enhanced security protocols, and improved integration capabilities with existing infrastructure. These factors combine to create a powerful market driver, pushing organizations to adopt more advanced and secure access solutions.

This report provides in-depth analysis of the Zero Trust SDP market, encompassing historical data, current market trends, and future projections. It offers valuable insights into market size, segmentation, key players, growth catalysts, challenges, and regional dynamics, enabling informed decision-making for businesses and investors within this rapidly growing sector. The extensive market data and forecasts are based on rigorous research and analysis, presenting a comprehensive overview of the Zero Trust SDP landscape.

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of XX% from 2020-2034 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately XX%.

Key companies in the market include VENUSTECH, Sangfor Technology, Wangsu Science & Technology, Appgate, Ivanti(Pulse Secure), macmon secure GmbH, Nanjing Minyu Shuxing Information Technology, Jiangsu Yi Anlian Network Technology(Enlink Cloud), Shanghai Angeek Technology, .

The market segments include Type, Application.

The market size is estimated to be USD XXX million as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4480.00, USD 6720.00, and USD 8960.00 respectively.

The market size is provided in terms of value, measured in million.

Yes, the market keyword associated with the report is "Zero Trust SDP," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Zero Trust SDP, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.