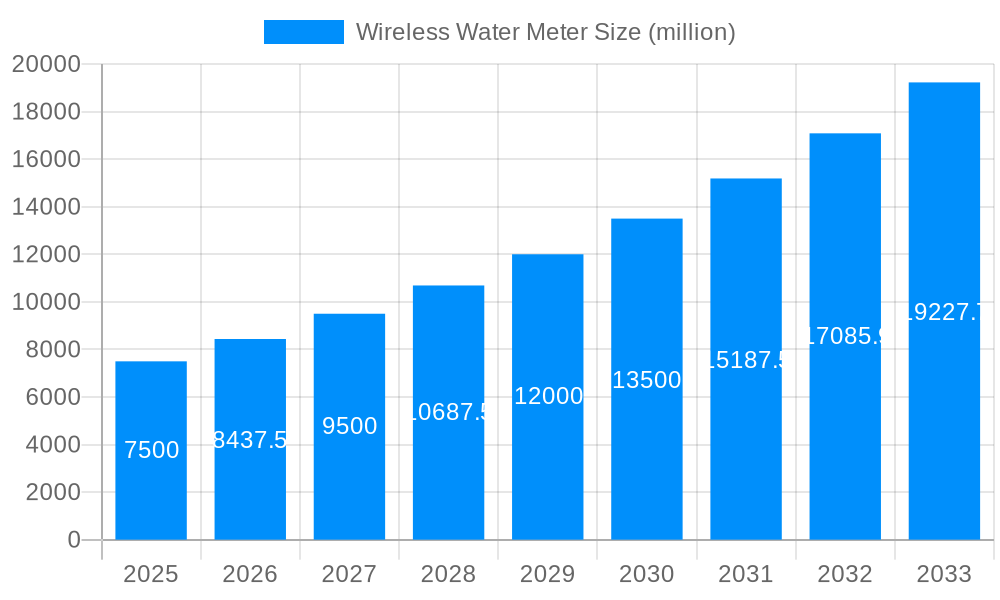

1. What is the projected Compound Annual Growth Rate (CAGR) of the Wireless Water Meter?

The projected CAGR is approximately 11.9%.

Wireless Water Meter

Wireless Water MeterWireless Water Meter by Type (Ultrasonic Water Meter, Electromagnetic Water Meter, World Wireless Water Meter Production ), by Application (Residential, Industrial, Commercial, World Wireless Water Meter Production ), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2026-2034

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

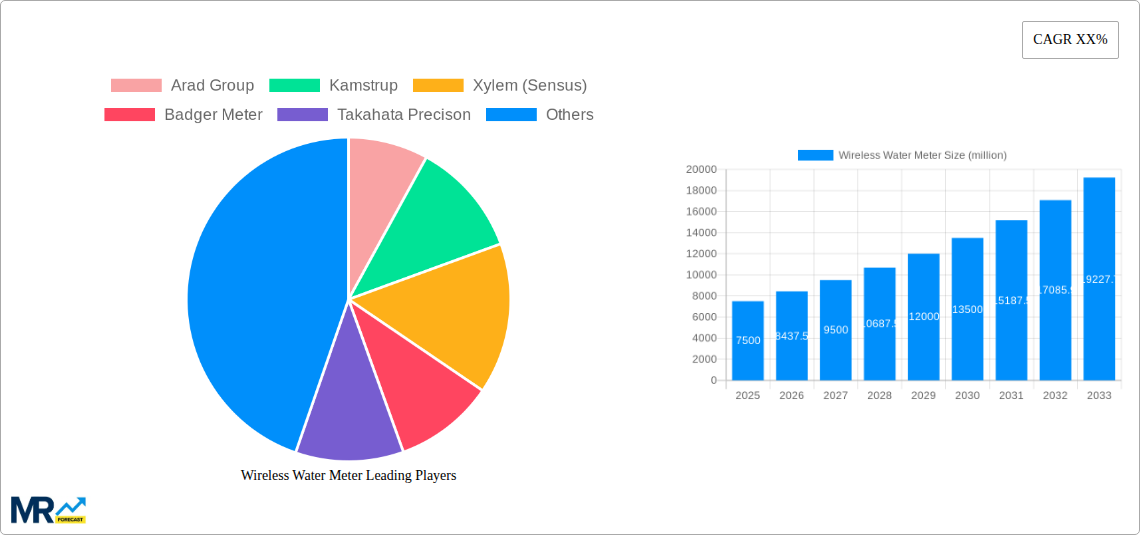

The global wireless water meter market is experiencing robust growth, driven by increasing urbanization, the need for efficient water resource management, and the rising adoption of smart city initiatives. The market's expansion is fueled by the advantages offered by wireless technology, including remote monitoring, reduced operational costs, and improved accuracy in water consumption measurement. Ultrasonic and electromagnetic technologies dominate the market, catering to residential, commercial, and industrial applications. While North America and Europe currently hold significant market shares, the Asia-Pacific region is projected to witness the fastest growth due to substantial infrastructure development and rising government investments in water management systems. Key players like Itron, Kamstrup, and Xylem (Sensus) are leading the market through technological innovation and strategic partnerships. However, high initial investment costs and concerns about data security and network reliability pose challenges to market penetration. The market is expected to witness continued consolidation with mergers and acquisitions as companies strive for a larger market share. Furthermore, the emergence of advanced analytics and the integration of wireless water meters with other smart city infrastructure will further drive market expansion in the coming years.

The forecast period (2025-2033) anticipates a steady rise in market value, driven primarily by increasing demand for accurate water metering and the potential for cost savings associated with reduced water loss and improved operational efficiency. The continued development of low-power wide-area networks (LPWAN) technologies will facilitate broader deployment of wireless water meters, particularly in remote areas. Competitive pressures are expected to intensify, prompting manufacturers to focus on developing more cost-effective and feature-rich solutions. Governments worldwide are increasingly implementing water conservation policies, which is creating a favorable regulatory environment for the growth of the wireless water meter market. The adoption of advanced data analytics platforms will enable utilities to gain valuable insights into water consumption patterns, allowing for better resource allocation and improved infrastructure management. This will further accelerate the market's expansion throughout the forecast period.

The global wireless water meter market is experiencing robust growth, driven by the increasing demand for efficient water management and the need to reduce water loss. The market, valued at several billion dollars in 2024, is projected to reach tens of billions by 2033, exhibiting a significant Compound Annual Growth Rate (CAGR). This surge is fueled by several factors, including the increasing adoption of smart city initiatives, advancements in sensor technology, and the growing awareness of water scarcity. The shift towards advanced metering infrastructure (AMI) is a key trend, allowing for real-time data monitoring and improved billing accuracy. This minimizes revenue loss from non-revenue water and enhances operational efficiency for utilities. Furthermore, the integration of wireless water meters with IoT platforms facilitates data analytics, leading to better decision-making regarding water resource allocation and infrastructure maintenance. The rising adoption of ultrasonic and electromagnetic water meters, due to their accuracy and longevity, is also significantly impacting market growth. Geographically, North America and Europe are currently leading the market adoption, while Asia-Pacific is poised for significant expansion in the coming years due to increasing urbanization and government initiatives promoting water conservation. Competition in the market is intense, with both established players and emerging companies vying for market share through innovation in technology and business models. The market is seeing a growing trend towards advanced functionalities, such as leak detection, remote meter reading, and predictive maintenance, which are further contributing to its growth. Finally, the increasing focus on sustainability and the need for improved water resource management are strong tailwinds supporting the continued expansion of the wireless water meter market.

Several key factors are driving the exponential growth of the wireless water meter market. Firstly, the increasing need for efficient water management is paramount. Water scarcity and aging water infrastructure are forcing utilities to adopt smart metering solutions to minimize water loss and improve operational efficiency. Wireless meters, with their ability to provide real-time data on water consumption, enable proactive leak detection and efficient resource allocation. Secondly, advancements in technology, specifically in sensor technology and communication protocols (like LoRaWAN and NB-IoT), are leading to more reliable, cost-effective, and feature-rich wireless water meters. Thirdly, government regulations and incentives aimed at promoting water conservation and efficient resource management are encouraging the widespread adoption of these meters. Many regions are mandating the installation of smart meters to improve water billing accuracy and reduce water theft. Moreover, the increasing adoption of smart city initiatives, which often include the deployment of smart water management systems, is fueling the demand for wireless water meters. Finally, the cost benefits associated with remote meter reading, reduced labor costs, and improved billing accuracy are making wireless meters a financially attractive option for water utilities. The confluence of these factors contributes to a highly favorable market environment for the continued expansion of the wireless water meter industry.

Despite the significant growth potential, the wireless water meter market faces certain challenges and restraints. One key hurdle is the high initial investment cost associated with deploying a complete AMI system. Replacing existing water meters with wireless counterparts requires substantial upfront capital expenditure, which can be a deterrent for some utilities, particularly smaller ones with limited budgets. Furthermore, concerns about data security and privacy are growing, necessitating robust security measures to protect sensitive consumer data. The complexity of integrating wireless meters with existing billing and management systems can also pose challenges during the implementation process. In addition, the need for reliable and robust communication networks in all deployment areas, especially in remote or geographically challenging regions, is crucial for the effective operation of wireless meters. Interoperability issues between different wireless technologies and communication protocols can also impede the seamless integration of systems from various vendors. Finally, the longevity and potential need for replacement of battery-powered meters could pose a concern for the long-term sustainability of these systems. Addressing these challenges through technological advancements, strategic partnerships, and government support will be crucial for the continued and sustainable growth of the wireless water meter market.

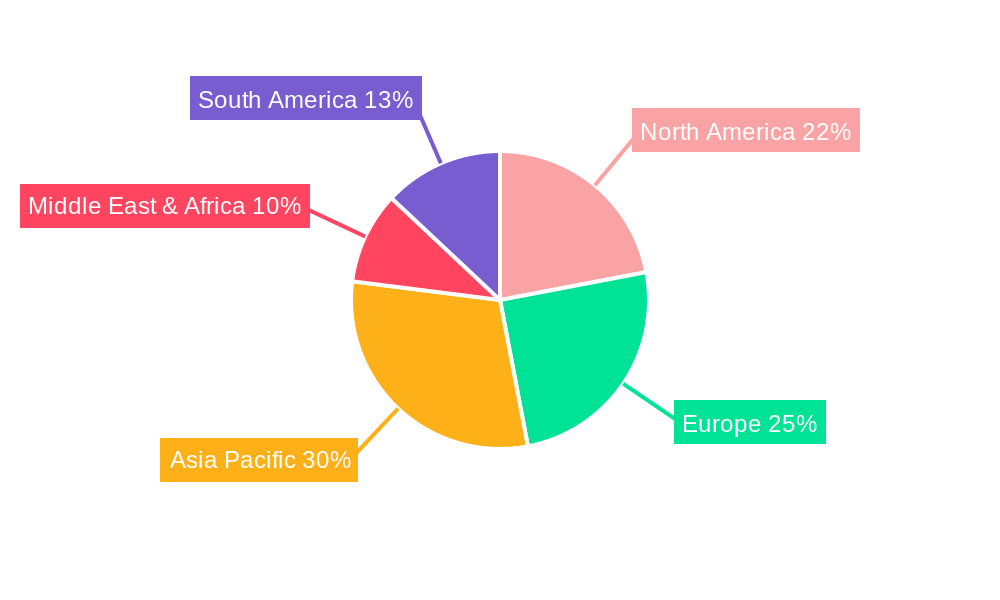

The global wireless water meter market is characterized by diverse regional and segmental growth patterns. North America and Europe currently hold significant market share due to early adoption of smart metering technologies and well-established water infrastructure. However, the Asia-Pacific region is predicted to witness the fastest growth rate over the forecast period, driven by rapid urbanization, increasing investments in water infrastructure, and government initiatives focused on water conservation and efficient water management.

Ultrasonic Water Meters: This segment is projected to dominate the market due to their high accuracy, long lifespan, and non-invasive nature. Ultrasonic meters use sound waves to measure water flow, making them particularly suitable for various applications.

Residential Applications: This segment accounts for a substantial portion of the market. The growing awareness of water conservation among residential users and the increasing implementation of smart home technologies are driving the demand for wireless residential water meters.

Commercial and Industrial Applications: While residential accounts for a larger volume, commercial and industrial applications often involve larger scale deployments, potentially resulting in higher revenue generation for manufacturers. These applications benefit significantly from remote monitoring and leak detection offered by wireless systems.

In summary, while North America and Europe currently dominate, the Asia-Pacific region’s rapid growth and the prevalent use of ultrasonic meters in both residential and commercial/industrial settings highlight the key segments and regions expected to lead the market's expansion in the coming years. The sheer volume of residential installations contributes significantly to overall market size, while the larger-scale deployments in commercial and industrial sectors translate to substantial revenue contributions.

The wireless water meter industry is experiencing strong growth propelled by several key factors. Increased government regulations mandating smart water metering are driving significant adoption. Simultaneously, advancements in IoT technology, particularly low-power wide-area networks (LPWANs), enable reliable and cost-effective data transmission. The increasing need to conserve water resources due to growing water scarcity and drought conditions further emphasizes the necessity of accurate and efficient water metering systems.

This report provides a comprehensive overview of the global wireless water meter market, covering market trends, driving forces, challenges, regional analysis, key players, and significant developments. The report offers detailed insights into various market segments, including ultrasonic, electromagnetic meters, and application-based breakdowns (residential, commercial, industrial). It also includes detailed forecasts for market growth, providing valuable insights for stakeholders across the wireless water meter industry. The information presented is intended to support informed decision-making regarding investments, market positioning, and future growth strategies within this dynamic sector.

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 11.9% from 2020-2034 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately 11.9%.

Key companies in the market include Arad Group, Kamstrup, Xylem (Sensus), Badger Meter, Takahata Precison, Diehl Metering, Itron, Neptune Technology Group, Honeywell (Elster), B METERS, Sanchuan, Suntront, iESLab, Chongqing Intelligence, Ningbo Water Meter, Wasion Group, Shenzhen Huaxu, Hunan Changde, .

The market segments include Type, Application.

The market size is estimated to be USD XXX N/A as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4480.00, USD 6720.00, and USD 8960.00 respectively.

The market size is provided in terms of value, measured in N/A and volume, measured in K.

Yes, the market keyword associated with the report is "Wireless Water Meter," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Wireless Water Meter, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.