1. What is the projected Compound Annual Growth Rate (CAGR) of the Wind Turbine Installation Vessel?

The projected CAGR is approximately XX%.

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

Wind Turbine Installation Vessel

Wind Turbine Installation VesselWind Turbine Installation Vessel by Type (Self-propelled Jack-up Vessel, Normal Jack-up Vessel, Heavy Lift Vessel, World Wind Turbine Installation Vessel Production ), by Application (Offshore, Others, World Wind Turbine Installation Vessel Production ), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2025-2033

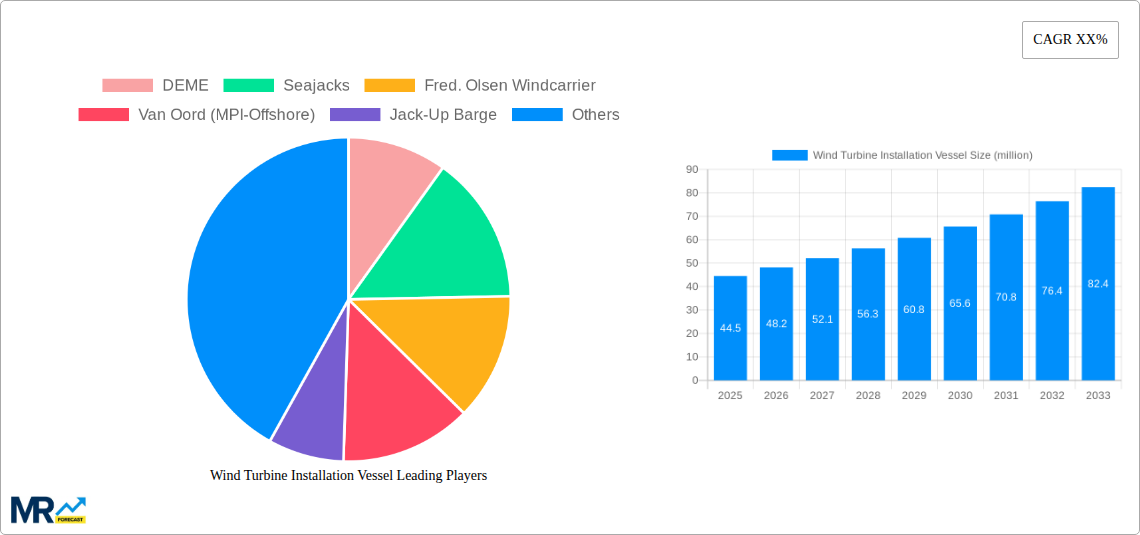

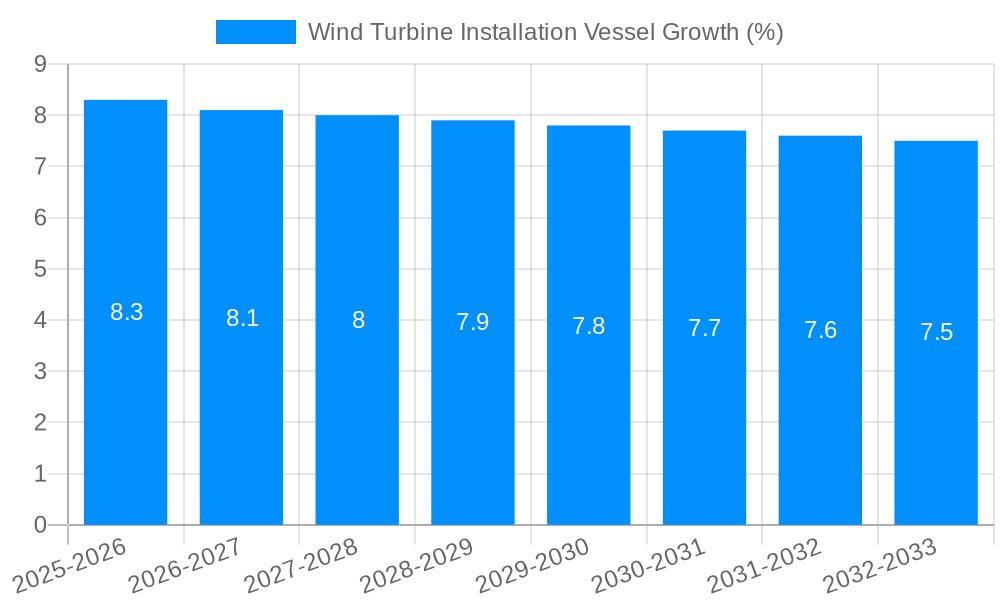

The global Wind Turbine Installation Vessel (WTIV) market is poised for significant expansion, driven by the accelerating transition to renewable energy sources and ambitious offshore wind power targets worldwide. With a current market size of approximately USD 42 million, the industry is projected to witness robust growth, exhibiting a compound annual growth rate (CAGR) of approximately 8.5% over the forecast period of 2025-2033. This upward trajectory is primarily fueled by increasing investments in large-scale offshore wind farms, demanding specialized and larger vessels for efficient turbine erection. Emerging economies in Asia Pacific, particularly China and its burgeoning offshore wind sector, are becoming increasingly influential drivers, alongside established markets in Europe, such as the United Kingdom and Germany, which continue to invest heavily in expanding their offshore wind capacities. Technological advancements in vessel design, including the development of self-propelled jack-up vessels with enhanced lifting capacities and greater operational stability, are also contributing to market expansion by enabling the installation of larger and more complex wind turbines.

The market is segmented by vessel type, with Self-propelled Jack-up Vessels leading the demand due to their operational efficiency and suitability for diverse offshore conditions. Normal Jack-up Vessels and Heavy Lift Vessels also play crucial roles in specific project requirements. In terms of application, the offshore segment is overwhelmingly dominant, reflecting the industry's focus on expanding wind power generation beyond coastal areas. Key players like DEME, Seajacks, Fred. Olsen Windcarrier, and Van Oord are actively investing in fleet expansion and technological innovation to cater to the growing demand. However, the market faces certain restraints, including the high capital expenditure associated with building and maintaining these specialized vessels, potential logistical challenges in certain regions, and the impact of fluctuating government policies and subsidies that can influence project timelines and investment decisions. Despite these challenges, the overarching global commitment to decarbonization and energy security will continue to propel the demand for WTIVs, ensuring a dynamic and growing market landscape.

The global wind turbine installation vessel (WTIV) market is on a trajectory of robust expansion, driven by the escalating demand for renewable energy and the ambitious decarbonization targets set by nations worldwide. The report delves into the intricate trends shaping this vital sector from 2019 to 2033, with a comprehensive analysis focusing on the base year of 2025 and a detailed forecast period extending to 2033. During the historical period of 2019-2024, the market witnessed significant advancements in vessel design and capacity, a trend that is set to accelerate. A key insight is the increasing specialization of WTIVs, moving beyond generic heavy-lift capabilities to bespoke designs tailored for specific turbine sizes and installation techniques. The sheer scale of next-generation wind turbines, with rotor diameters exceeding 250 meters and hub heights reaching over 150 meters, necessitates vessels with colossal deck space, immense lifting capacities exceeding 2,000 metric tons, and advanced jacking systems capable of operating in deeper waters and harsher offshore environments.

The market is characterized by a discernible shift towards larger and more sophisticated self-propelled jack-up vessels. These vessels, often costing upwards of \$300 million to \$500 million to construct, offer enhanced operational efficiency, reduced installation times, and improved safety. The "World Wind Turbine Installation Vessel Production" segment, encompassing the manufacturing and deployment of these specialized assets, is projected to see substantial growth. Furthermore, the "Offshore" application segment, by far the dominant force, is expected to continue its reign, fueled by the rapid development of offshore wind farms globally, particularly in Europe, Asia, and North America. The strategic investments by leading companies in expanding their WTIV fleets underscore the industry's confidence in the long-term viability of offshore wind. This includes the development of newbuilds and the retrofitting of existing vessels to meet the evolving demands of the industry, thereby driving innovation and competitive differentiation. The overall market value is expected to reach several tens of millions of dollars by the end of the forecast period, demonstrating a significant CAGR driven by these overarching trends. The increasing complexity of offshore wind farm projects, including floating wind technologies, also presents a nascent but significant trend, pushing the boundaries of WTIV capabilities and deployment strategies.

The inexorable rise of the wind turbine installation vessel market is propelled by a confluence of powerful global forces, all converging to accelerate the adoption of renewable energy. Foremost among these is the urgent global imperative to combat climate change and achieve net-zero emission targets. Governments worldwide are implementing ambitious policies, including subsidies, tax incentives, and renewable energy mandates, which directly translate into significant investment in offshore wind projects. This creates a sustained demand for the specialized vessels required to construct these farms. Secondly, the declining levelized cost of energy (LCOE) for offshore wind power is making it increasingly competitive with traditional fossil fuels. Technological advancements in turbine efficiency and manufacturing, coupled with economies of scale, have significantly reduced the cost per megawatt-hour, making offshore wind an attractive investment for utilities and energy companies. The sheer size and power output of modern wind turbines are also a major driver. As turbines grow larger, the need for installation vessels with commensurately larger lifting capacities and deck space becomes critical, spurring the development of next-generation WTIVs. This constant evolution in turbine technology necessitates continuous innovation and investment in specialized maritime assets, creating a cyclical growth pattern within the WTIV sector. The increasing maturity of the offshore wind industry, coupled with a supportive regulatory environment, further solidifies the market's expansion.

Despite the buoyant outlook, the wind turbine installation vessel sector is not without its formidable challenges and restraints. One of the most significant is the substantial capital expenditure required for both new vessel construction and the maintenance of existing fleets. The cost of a state-of-the-art WTIV can easily run into hundreds of millions of dollars, representing a considerable financial commitment that can be a barrier to entry for smaller players and a risk for established companies. The long lead times associated with vessel construction, often spanning several years, also present a planning challenge, requiring accurate long-term market forecasting. Furthermore, the availability of skilled labor, both for vessel operation and for the construction and maintenance of the vessels themselves, is a growing concern. The specialized nature of WTIV operations demands highly trained engineers, deck crews, and project managers, and a shortage of such talent can impede project timelines and increase operational costs. Environmental regulations, while a driving force for offshore wind, also impose stringent compliance requirements on vessel operations, including emissions standards and waste management protocols, which can add to operational complexity and cost. Additionally, the intermittent nature of wind resource and the dependence on favorable weather conditions can lead to project delays and scheduling disruptions, impacting the overall efficiency and profitability of WTIV operations. The potential for supply chain disruptions, particularly for specialized components and materials, can also pose a significant risk to timely vessel delivery and ongoing operations.

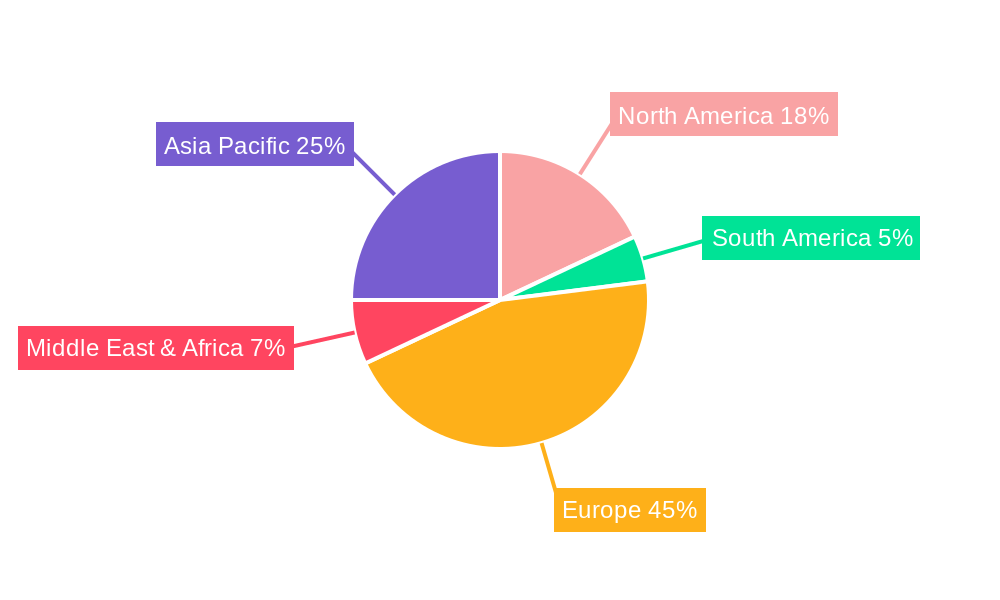

The global wind turbine installation vessel market is poised for significant dominance by specific regions and certain vessel segments, driven by the concentration of offshore wind development and the specific technological requirements of these projects. Europe stands out as a pivotal region, and is projected to continue its leadership in the offshore wind market throughout the study period (2019-2033). This dominance is underpinned by a mature regulatory framework, substantial government support, and a long-standing commitment to renewable energy development. Countries like the United Kingdom, Germany, the Netherlands, and Denmark have been at the forefront of offshore wind farm installations, necessitating a robust fleet of WTIVs to service their extensive and ambitious projects. The North Sea, in particular, represents a mature and highly active offshore wind development zone, requiring a high density of specialized installation vessels.

Within this dominant region, the Self-propelled Jack-up Vessel segment is expected to be the primary driver of market growth and demand. These advanced vessels, capable of independently navigating to offshore sites and then jacking up their hulls to provide a stable platform for heavy lifting operations, are indispensable for the installation of the increasingly large and complex wind turbines. Their self-propelled nature reduces reliance on tugboats, enhancing operational efficiency and cost-effectiveness. The sheer lifting capacity and working height of modern self-propelled jack-up vessels, often exceeding 2,000 metric tons and capable of reaching over 150 meters, are crucial for handling the massive components of next-generation offshore turbines. Companies like DEME and Seajacks have been heavily investing in and operating these types of vessels, demonstrating their critical role. The "World Wind Turbine Installation Vessel Production" within this segment refers to the manufacturing and deployment of these specialized assets, which is a significant indicator of market health.

Furthermore, the Offshore application segment is, by definition, the undisputed leader, as the vast majority of wind turbine installations occur in marine environments. The growth of offshore wind farms, both in shallower waters and the emerging deep-water floating wind sector, directly fuels the demand for WTIVs. The ongoing expansion of offshore wind capacity globally, with new projects emerging in Asia-Pacific and North America, will further solidify the offshore application's dominance, creating a consistent and growing need for specialized installation vessels. The report's forecast for the Estimated Year: 2025 and the Forecast Period: 2025-2033 indicates a sustained and increasing reliance on these specialized assets for the successful deployment of global renewable energy infrastructure. The capacity of these vessels to handle turbine weights in the hundreds of tons and heights of over 200 meters is a key factor in their market dominance.

The wind turbine installation vessel industry is experiencing a surge in growth, primarily catalyzed by the accelerating global transition to renewable energy. Supportive government policies, including tax incentives and renewable energy targets, are a significant driver, stimulating substantial investment in offshore wind projects. The continuous innovation in wind turbine technology, leading to larger and more powerful turbines, directly necessitates the development of more capable WTIVs, creating a positive feedback loop for the industry. Furthermore, the increasing cost-competitiveness of offshore wind power compared to traditional energy sources makes it an attractive investment for utilities and corporations, thereby boosting demand for installation services.

This comprehensive report offers an in-depth analysis of the global wind turbine installation vessel market, providing critical insights for stakeholders. The study meticulously covers the market dynamics from 2019 to 2033, with a detailed examination of the base year 2025 and a thorough forecast period from 2025 to 2033. It delves into the prevailing trends, identifying the increasing demand for larger, more specialized vessels like self-propelled jack-up units. The report also dissects the key driving forces, including the global push for renewable energy and the declining cost of offshore wind. Furthermore, it addresses the significant challenges and restraints facing the industry, such as high capital expenditures and labor shortages. The analysis highlights the dominant regions and key segments expected to lead market growth, with a particular focus on Europe and the self-propelled jack-up vessel category. This extensive coverage ensures a holistic understanding of the market's current state and future trajectory.

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of XX% from 2019-2033 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately XX%.

Key companies in the market include DEME, Seajacks, Fred. Olsen Windcarrier, Van Oord (MPI-Offshore), Jack-Up Barge, SEAFOX, Swire Blue Ocean, Longyuan Zhenhua, CCCC Third Harbor Engineering, .

The market segments include Type, Application.

The market size is estimated to be USD 42 million as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4480.00, USD 6720.00, and USD 8960.00 respectively.

The market size is provided in terms of value, measured in million and volume, measured in K.

Yes, the market keyword associated with the report is "Wind Turbine Installation Vessel," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Wind Turbine Installation Vessel, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.