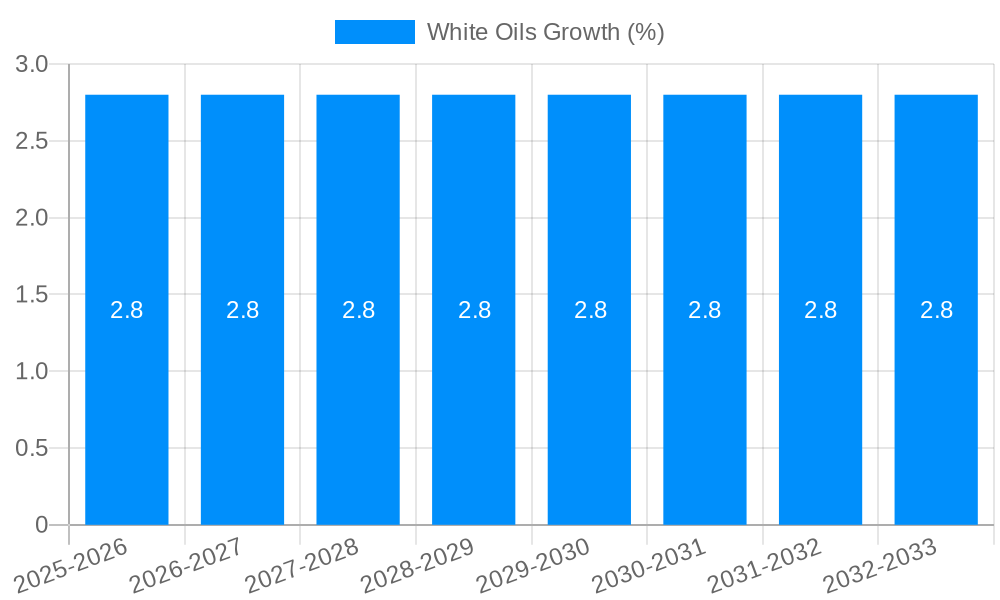

1. What is the projected Compound Annual Growth Rate (CAGR) of the White Oils?

The projected CAGR is approximately 2.8%.

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

White Oils

White OilsWhite Oils by Type (Industrial Grade, Cosmetic Grade, Food Grade, Pharmaceutical Grade), by Application (Textile, Solvent Oil, Lubricants, Polystyrene and Other Polymers, Adhesive, Other), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2025-2033

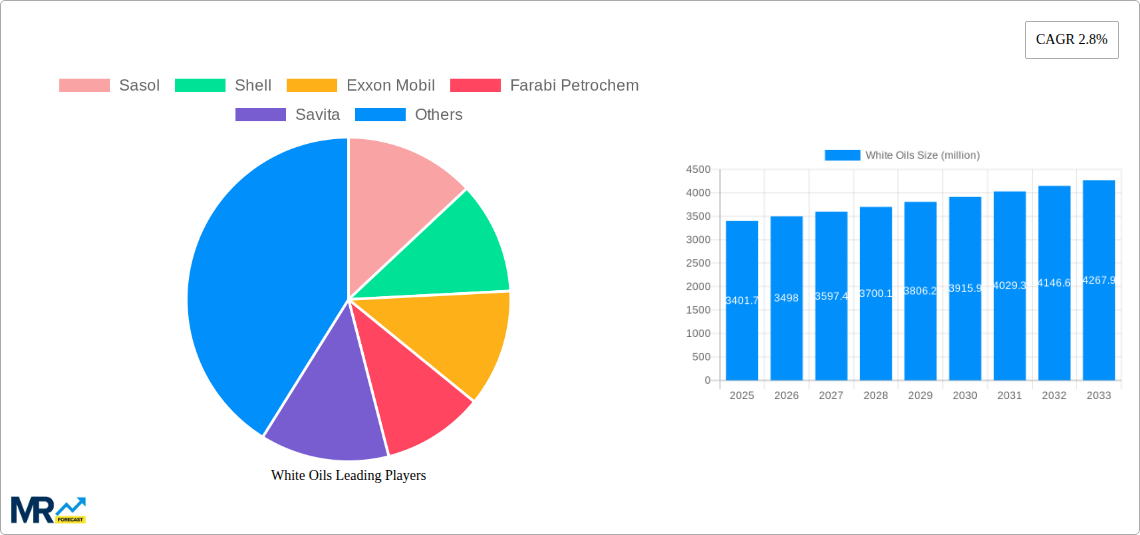

The global White Oils market is poised for steady growth, projected to reach approximately USD 3401.7 million by 2025, driven by a compound annual growth rate (CAGR) of 2.8%. This expansion is primarily fueled by the increasing demand for high-purity and versatile petroleum distillates across a wide array of industrial and consumer applications. The robust performance in sectors such as pharmaceuticals, where white oils serve as key excipients and active ingredients, and cosmetics, as emollients and bases for personal care products, are significant contributors. Furthermore, the burgeoning food industry's need for food-grade white oils for processing and packaging is also playing a crucial role in market upliftment. The expanding manufacturing capabilities in emerging economies, coupled with stringent quality standards for end-use products, are creating a favorable environment for market participants.

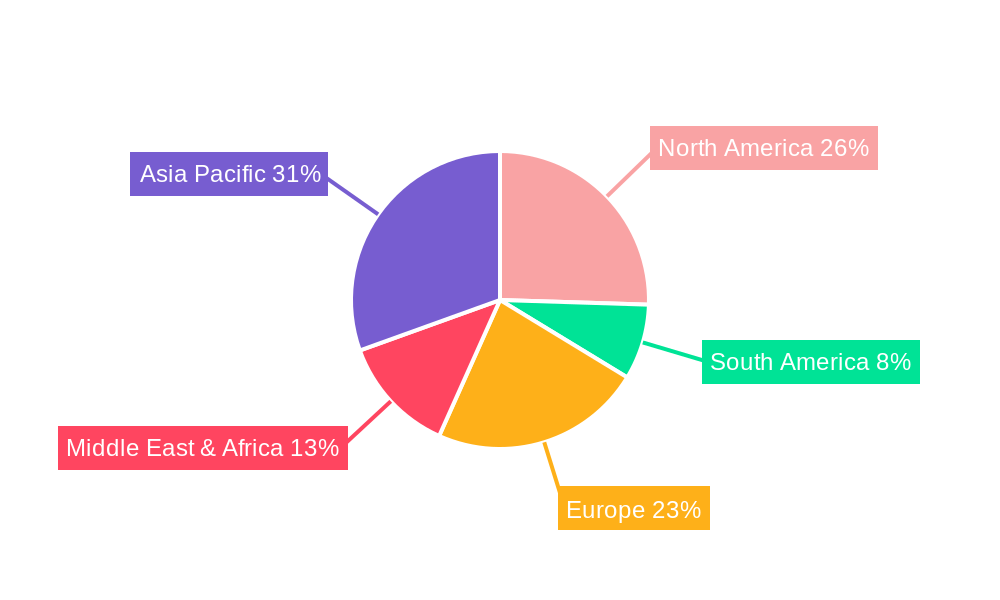

The market is characterized by a diverse segmentation, with Industrial Grade, Cosmetic Grade, Food Grade, and Pharmaceutical Grade white oils catering to specific industry requirements. Applications are equally varied, ranging from textile processing and solvent oil formulations to advanced lubricants, polystyrene and other polymer production, and adhesives. Geographically, Asia Pacific is expected to lead market growth due to rapid industrialization and a growing consumer base, particularly in China and India. North America and Europe, while mature markets, continue to exhibit sustained demand driven by specialized applications and technological advancements. Key players like Sasol, Shell, and Exxon Mobil are actively investing in research and development to innovate and meet evolving regulatory landscapes, ensuring product quality and sustainability. Navigating the challenges posed by fluctuating raw material prices and the increasing adoption of sustainable alternatives will be critical for sustained success in this dynamic market.

Here's a comprehensive report description on White Oils, incorporating your specified requirements:

The global white oils market is poised for robust expansion, demonstrating a compound annual growth rate (CAGR) of approximately XXX% between 2019 and 2033. The study period, encompassing the historical phase from 2019-2024 and the forecast period of 2025-2033 with a base and estimated year of 2025, reveals significant underlying dynamics. A key market insight is the escalating demand for high-purity white oils across diverse applications, driven by increasingly stringent regulatory standards and a growing consumer preference for products manufactured using safe and inert ingredients. Specifically, the Pharmaceutical Grade segment is projected to witness an accelerated growth trajectory, attributed to the expanding pharmaceutical industry and the critical role of white oils as excipients, emollients, and lubricants in drug formulations. Similarly, the Cosmetic Grade segment is experiencing substantial uplift due to the burgeoning beauty and personal care industry, with consumers actively seeking out natural and hypoallergenic ingredients. This trend is further amplified by innovations in product formulations that leverage the unique properties of white oils, such as their excellent stability, low volatility, and non-comedogenic characteristics.

The Industrial Grade segment, while mature, continues to be a cornerstone of the market, with applications in textiles, lubricants, and polymers forming a substantial volume. However, growth in this segment is increasingly tied to the development of specialized grades and the adoption of more sustainable manufacturing processes by key players like Sasol, Shell, and Exxon Mobil. The market is also characterized by a geographical shift, with Asia Pacific emerging as a dominant region, fueled by its rapidly industrializing economies and a burgeoning middle class that drives demand across all grades. The report will delve into granular market insights, such as the price sensitivity of certain industrial grades versus the premium pricing attainable for pharmaceutical and cosmetic grades. Furthermore, the impact of technological advancements in refining processes, leading to enhanced purity and customized functionalities, will be a critical focus. The interplay between raw material availability, primarily from crude oil refining, and the increasing emphasis on sustainability will also be thoroughly analyzed, offering a nuanced perspective on the market's trajectory.

Several powerful forces are propelling the growth of the global white oils market, painting a picture of consistent and substantial expansion throughout the study period. Foremost among these drivers is the relentless pursuit of enhanced product safety and quality across a multitude of end-user industries. Stringent regulatory frameworks globally, particularly concerning food contact materials, pharmaceuticals, and cosmetics, are mandating the use of highly purified and inert substances like white oils. This regulatory push directly translates into increased demand for Pharmaceutical Grade and Food Grade white oils, where purity is paramount to prevent contamination and ensure consumer well-being. The growth of the pharmaceutical sector, marked by an aging global population and advancements in medical treatments, further amplifies this demand, as white oils are indispensable in formulations for topical medications, laxatives, and drug delivery systems.

Beyond regulatory mandates, evolving consumer preferences are playing a pivotal role. There's a discernible shift towards products perceived as safer, cleaner, and more natural. In the cosmetics and personal care sector, white oils are lauded for their emollient, moisturizing, and protective properties, making them a favored ingredient in skincare, haircare, and baby care products. This trend is particularly pronounced in emerging economies where a rising disposable income empowers consumers to opt for premium and high-quality personal care items. Furthermore, the versatility of white oils extends to industrial applications. Their excellent solvency, lubricating, and insulating properties make them vital in the manufacturing of plastics, textiles, and a wide array of industrial lubricants. The increasing complexity of manufacturing processes and the demand for higher performance in these sectors are continuously driving the need for specialized white oil grades, thereby contributing significantly to market growth.

Despite the robust growth trajectory, the white oils market is not without its hurdles, which could temper the pace of expansion or necessitate strategic adaptation by market participants. A primary challenge stems from the inherent price volatility of its key raw material: crude oil. As white oils are refined petroleum distillates, fluctuations in crude oil prices directly impact their production costs, leading to unpredictable pricing for end-users. This can create hesitation in procurement decisions, particularly for large-volume industrial applications where cost-effectiveness is a critical factor. Moreover, growing environmental concerns and the global push towards sustainability are putting pressure on industries reliant on petroleum-based products. While white oils themselves are often inert and considered safe, their origin from fossil fuels might lead to increasing scrutiny and a potential preference for bio-based or synthetic alternatives in some niche applications.

Furthermore, the market faces the challenge of intense competition, with a multitude of established players and emerging regional manufacturers vying for market share. This competitive landscape can lead to price wars, particularly in more commoditized segments like Industrial Grade white oils, squeezing profit margins. The development and adoption of stringent quality control measures and certifications, while a positive development for product integrity, can also represent a barrier to entry for smaller players and increase operational costs for all. In some regions, specific regulatory changes or the introduction of alternative materials that offer comparable performance at a lower cost or with a better environmental profile could pose a threat to established applications. For instance, in the lubricant sector, the development of high-performance synthetic lubricants or bio-lubricants might gradually erode the market share of certain white oil-based formulations.

The global white oils market is characterized by the dominant influence of Asia Pacific as a key region, driven by a confluence of robust industrialization, a burgeoning middle class, and increasing disposable incomes. Within this dynamic region, China stands out as a pivotal country, acting as both a major producer and a colossal consumer of white oils across all grades. The sheer scale of its manufacturing sector, encompassing textiles, plastics, and pharmaceuticals, coupled with its rapidly expanding domestic market for cosmetics and personal care products, fuels an insatiable demand. Countries like India, South Korea, and Southeast Asian nations also contribute significantly to the region's dominance, driven by similar, albeit on a smaller scale, industrial and consumer growth patterns. The robust infrastructure development and favorable government policies in many of these countries further facilitate market expansion.

When considering segment dominance within the broader market, the Industrial Grade segment, while extensive, is witnessing a steady, albeit more moderate, growth compared to its more specialized counterparts. However, the sheer volume and consistent demand from sectors like Textiles and Lubricants ensure its continued significance. The Polystyrene and Other Polymers application within the Industrial Grade segment is particularly noteworthy, as white oils are crucial processing aids and additives in the production of a vast array of plastic products that are ubiquitous in modern life. The report anticipates that the demand for Industrial Grade white oils will remain substantial throughout the forecast period, driven by the continued expansion of manufacturing capabilities in emerging economies.

However, a closer examination of growth potential and value, rather than just volume, points towards the Cosmetic Grade and Pharmaceutical Grade segments as areas poised for exceptional growth and increasing market share. The increasing consumer awareness regarding product safety, coupled with the global rise in healthcare expenditure and the growth of the wellness industry, directly translates to a heightened demand for high-purity white oils in these premium segments. In the Cosmetic Grade segment, applications in skincare, haircare, and makeup are expanding rapidly, driven by a global trend towards natural-looking, safe, and effective beauty products. Consumers are actively seeking out ingredients that are gentle, hypoallergenic, and derived from reliable sources, characteristics that white oils in these grades possess.

Similarly, the Pharmaceutical Grade segment is experiencing a significant uplift. The increasing prevalence of chronic diseases, the growing demand for over-the-counter (OTC) medications, and advancements in drug formulation technologies all contribute to this surge. White oils serve as critical excipients, emollients, and laxatives in a wide range of pharmaceutical products. The strict regulatory requirements for pharmaceutical ingredients further ensure the premium pricing and consistent demand for high-quality pharmaceutical grade white oils. Companies like Sonneborn, H&R Group, and Savita are key players in these high-value segments, focusing on R&D to meet evolving purity and performance standards. While Asia Pacific leads in overall volume, North America and Europe remain significant markets for Cosmetic and Pharmaceutical Grade white oils due to higher per capita spending on healthcare and personal care, and more mature regulatory environments that favor high-purity ingredients.

The white oils industry is experiencing several key growth catalysts that are shaping its future trajectory. A primary catalyst is the increasing global emphasis on product purity and safety across diverse end-user industries. This is driving demand for high-quality Cosmetic Grade and Pharmaceutical Grade white oils, where stringent regulatory requirements necessitate their use. Furthermore, the expanding pharmaceutical sector, fueled by an aging global population and advancements in medical treatments, provides a consistent demand for white oils as essential excipients and lubricants. In the industrial realm, the growing manufacturing base in emerging economies, particularly in Asia Pacific, coupled with the continuous development of new polymers and specialized applications, fuels the demand for Industrial Grade white oils.

The global white oils market is characterized by the presence of several key global and regional players who are driving innovation and catering to diverse market needs. These companies are instrumental in shaping the market's landscape through their production capabilities, product portfolios, and strategic initiatives.

The white oils sector has witnessed several key developments over the study period, reflecting industry trends and strategic moves by market participants:

This comprehensive report on the White Oils market offers an in-depth analysis of market dynamics, trends, and future projections. Spanning the study period of 2019-2033, with a Base Year of 2025, it provides crucial insights into the growth drivers, challenges, and opportunities within this vital sector. The report meticulously dissects the market by Type (Industrial Grade, Cosmetic Grade, Food Grade, Pharmaceutical Grade) and Application (Textile, Solvent Oil, Lubricants, Polystyrene and Other Polymers, Adhesive, Other), offering granular data and forecasts for each. It highlights the burgeoning demand for high-purity grades in the pharmaceutical and cosmetic industries, propelled by stringent regulations and evolving consumer preferences for safe and high-quality products. The report also examines the significant role of the Asia Pacific region, particularly China, as a dominant force in both production and consumption. Furthermore, it identifies key growth catalysts, such as technological advancements in refining and the increasing adoption of sustainable practices. With detailed profiles of leading global players like Sasol, Shell, and Exxon Mobil, and an analysis of significant industry developments, this report serves as an indispensable resource for stakeholders seeking to navigate and capitalize on the evolving white oils market.

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 2.8% from 2019-2033 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately 2.8%.

Key companies in the market include Sasol, Shell, Exxon Mobil, Farabi Petrochem, Savita, Nippon Oil, CEPSA, Eni, H&R Group, SEOJIN CHEM, Sonneborn, MORESCO, KDOC, Atlas Setayesh Mehr, Gandhar Oil, FPCC, CNPC, Sinopec, ChemChina, Yitai Petro, .

The market segments include Type, Application.

The market size is estimated to be USD 3401.7 million as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3480.00, USD 5220.00, and USD 6960.00 respectively.

The market size is provided in terms of value, measured in million and volume, measured in K.

Yes, the market keyword associated with the report is "White Oils," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the White Oils, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.