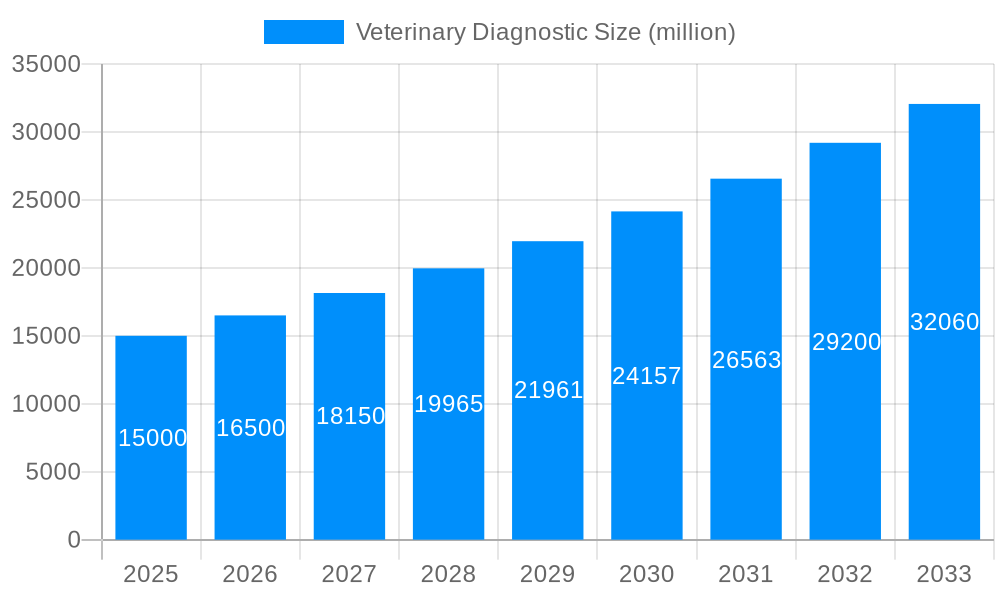

1. What is the projected Compound Annual Growth Rate (CAGR) of the Veterinary Diagnostic?

The projected CAGR is approximately 10.5%.

Veterinary Diagnostic

Veterinary DiagnosticVeterinary Diagnostic by Type (Immunodiagnostic Tests, Molecular Diagnostics, Diagnostic Imaging, Hematology Analyzers, Clinical Chemistry, Others), by Application (Farm Animals, Companion Animals, Others), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2026-2034

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

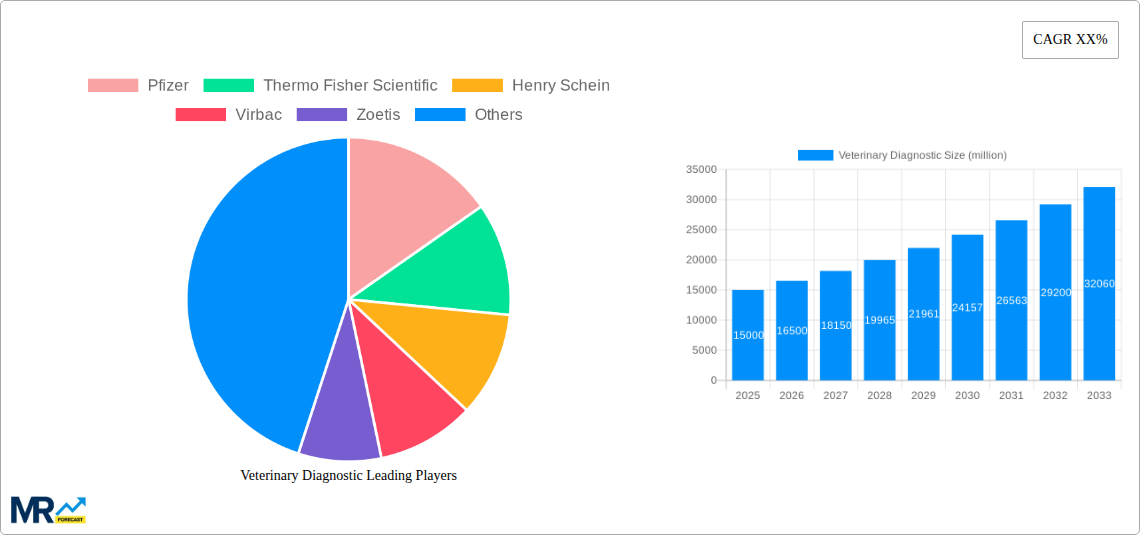

The global veterinary diagnostics market is poised for significant expansion, propelled by escalating pet ownership, the growing trend of pet humanization, and continuous advancements in diagnostic technology. This dynamic market offers a comprehensive suite of diagnostic solutions, including clinical pathology, microbiology, immunology, molecular diagnostics, and imaging. Key industry leaders such as Pfizer, Thermo Fisher Scientific, and IDEXX Laboratories are strategically capitalizing on technological innovation and acquisitions to broaden their market reach and deliver integrated diagnostic capabilities. The rising incidence of zoonotic diseases further underscores the critical need for advanced diagnostic tools for prompt detection and effective management.

Technological breakthroughs, particularly in point-of-care diagnostics and sophisticated molecular techniques, are enhancing the efficiency and precision of veterinary testing, ultimately improving animal health outcomes and optimizing veterinary workflows. Despite these advancements, market accessibility can be constrained by the high cost of advanced equipment and testing, especially in emerging economies. Navigating diverse regulatory landscapes and varying reimbursement policies presents additional challenges. The competitive environment necessitates ongoing innovation and strategic collaborations for sustained market leadership. Looking ahead, the market is projected to maintain a robust growth trajectory, driven by sustained demand for cutting-edge diagnostic solutions across all veterinary sectors. The integration of artificial intelligence and machine learning in veterinary diagnostics is expected to further elevate accuracy, speed, and cost-efficiency.

The global veterinary diagnostic market is experiencing robust growth, projected to reach multi-billion dollar valuations by 2033. Driven by factors such as increasing pet ownership, rising pet healthcare expenditure, and advancements in diagnostic technologies, the market exhibits a positive trajectory. The historical period (2019-2024) witnessed a steady expansion, laying the groundwork for the impressive forecast period (2025-2033). Our analysis, with the base year set at 2025 and the estimated year also at 2025, reveals a significant market opportunity across various segments. The increasing prevalence of zoonotic diseases, emphasizing the interconnectedness of animal and human health, further underscores the importance of accurate and timely veterinary diagnostics. This is fueling demand for sophisticated diagnostic tools and services, leading to substantial investments in research and development by major players like Idexx and Zoetis. The shift towards preventative healthcare for animals, coupled with the growing adoption of point-of-care diagnostics, contributes to the market's upward trend. Furthermore, the increasing availability of advanced diagnostic techniques, such as molecular diagnostics and imaging technologies, allows for earlier disease detection and improved treatment outcomes. This trend is particularly pronounced in developed economies, where pet owners are more likely to invest in comprehensive healthcare for their animals, yet developing economies show significant growth potential given increasing pet ownership and rising disposable incomes. The market is also witnessing a consolidation trend, with larger players acquiring smaller companies to expand their product portfolio and market share. This competitive landscape is further intensified by the continuous innovation in diagnostic technology, ensuring that the veterinary diagnostic market remains dynamic and rapidly evolving.

Several factors are driving the expansion of the veterinary diagnostic market. The escalating prevalence of chronic diseases in companion animals, such as diabetes, cancer, and kidney disease, necessitates advanced diagnostic tools for early detection and management. The increasing humanization of pets, leading to higher veterinary care spending, further fuels market growth. Pet owners are increasingly willing to invest in sophisticated diagnostic tests to ensure their pets receive the best possible care, leading to a surge in demand for high-quality diagnostic services. Technological advancements, such as the development of faster, more accurate, and cost-effective diagnostic tests (e.g., PCR, ELISA), are also contributing significantly to market expansion. The development of point-of-care testing devices is particularly impactful, allowing veterinarians to provide faster results and improve patient care efficiency. Moreover, the rising demand for personalized medicine in veterinary care, tailored to the specific needs of individual animals, underscores the need for advanced diagnostic capabilities. Government initiatives promoting animal welfare and disease surveillance also play a crucial role, encouraging investment in veterinary diagnostic infrastructure and research. Finally, the increasing integration of data analytics and artificial intelligence (AI) into veterinary diagnostics is improving diagnostic accuracy and facilitating better disease management strategies.

Despite the positive growth trajectory, the veterinary diagnostic market faces several challenges. The high cost of advanced diagnostic equipment and technologies can be a barrier to entry for smaller veterinary clinics, particularly in developing countries. The need for specialized personnel to operate and interpret complex diagnostic tests also presents a challenge, requiring investment in training and education. Regulatory hurdles and stringent approval processes for new diagnostic products can slow down market penetration. Furthermore, reimbursement policies for veterinary diagnostic services can vary significantly across different regions, impacting the affordability and accessibility of advanced testing. The competitive landscape, with established players like Idexx and Zoetis alongside emerging innovative companies, presents challenges in terms of maintaining market share and profitability. The accuracy and reliability of diagnostic tests are crucial, as inaccurate results can lead to misdiagnosis and inappropriate treatment, which can pose both ethical and financial implications for veterinary practices. Finally, the market is also subject to fluctuations influenced by economic conditions and changes in pet ownership trends.

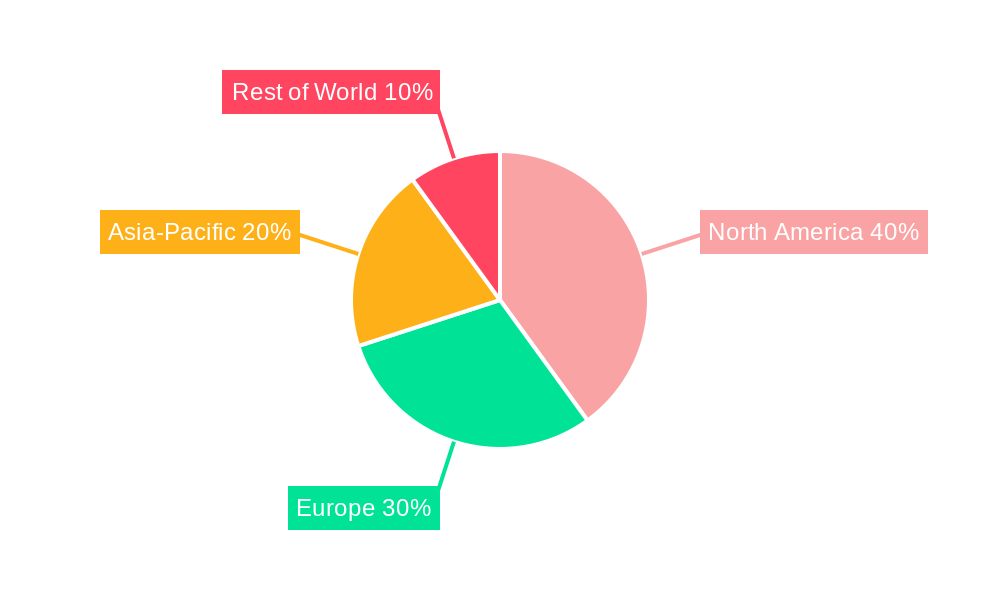

North America (USA & Canada): This region is projected to maintain its dominant position, fueled by high pet ownership rates, significant spending on pet healthcare, and the presence of major diagnostic companies. The advanced healthcare infrastructure and widespread adoption of advanced diagnostic technologies contribute to this dominance. The high disposable incomes of pet owners in this region further drive demand for premium diagnostic services.

Europe (Western Europe & Rest of Europe): Significant growth is anticipated in Europe, driven by rising pet ownership and increasing awareness of animal health. However, stricter regulatory frameworks may pose some challenges for market penetration. The segment in Europe that is likely to exhibit fastest growth will be the molecular diagnostics segment.

Asia Pacific (Japan, China, India, Australia, and Rest of Asia Pacific): This region presents a substantial growth opportunity, albeit with varying levels of market maturity across different countries. Rapid economic growth, increasing pet ownership (particularly in China and India), and rising disposable incomes are key drivers. However, infrastructure limitations and regulatory differences may need to be addressed. This region would see high growth in point-of-care testing, due to growing veterinary clinics.

Segments: The molecular diagnostics segment (PCR, ELISA) is experiencing the most rapid growth due to its ability to detect a wider range of diseases earlier and more accurately. Imaging technologies (radiography, ultrasound) also represent a significant segment, while point-of-care testing is rapidly gaining traction due to its convenience and speed.

The overall market is segmented by product type (reagents, instruments, software), by animal type (companion animals, livestock, poultry), by technology, by end-user (veterinary clinics, veterinary hospitals, research institutions). Within these segments, the high-growth areas are driven by factors such as increased prevalence of certain diseases, advancements in specific technologies, and expanding access to healthcare in emerging markets. The overall market is projected to reach several billion dollars in the next few years, representing an enormous opportunity for investors and players in the sector.

The convergence of several factors is propelling the growth of the veterinary diagnostic industry. These include a growing awareness of preventative healthcare for animals, leading to increased diagnostic testing; significant technological advancements yielding more efficient, accurate, and affordable diagnostic tools; and expanding veterinary service provision, particularly in emerging economies. Government regulations promoting animal health and disease control also play a significant role, coupled with the rising adoption of point-of-care diagnostics in veterinary settings.

This report offers a detailed analysis of the veterinary diagnostic market, providing insights into market trends, growth drivers, challenges, and key players. The comprehensive coverage includes historical data, current market estimates, and future projections, segmented by region, product type, animal type, and end-user. The report also assesses the competitive landscape, providing company profiles, competitive strategies, and market share data. This analysis is crucial for understanding the market's dynamics and opportunities for growth and investment.

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 10.5% from 2020-2034 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately 10.5%.

Key companies in the market include Pfizer, Thermo Fisher Scientific, Henry Schein, Virbac, Zoetis, IDVet, Abaxis, Heska Corporation, Idexx, Biochek, VCA Antech.

The market segments include Type, Application.

The market size is estimated to be USD 8.78 billion as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3480.00, USD 5220.00, and USD 6960.00 respectively.

The market size is provided in terms of value, measured in billion and volume, measured in K.

Yes, the market keyword associated with the report is "Veterinary Diagnostic," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Veterinary Diagnostic, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.