1. What is the projected Compound Annual Growth Rate (CAGR) of the Thin Wafers Temporary Bonding Equipment?

The projected CAGR is approximately 5.7%.

Thin Wafers Temporary Bonding Equipment

Thin Wafers Temporary Bonding EquipmentThin Wafers Temporary Bonding Equipment by Type (Semi-Automatic Bonding Equipment, Fully Automatic Bonding Equipment), by Application (MEMS, Advanced Packaging, CIS, Others), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2026-2034

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

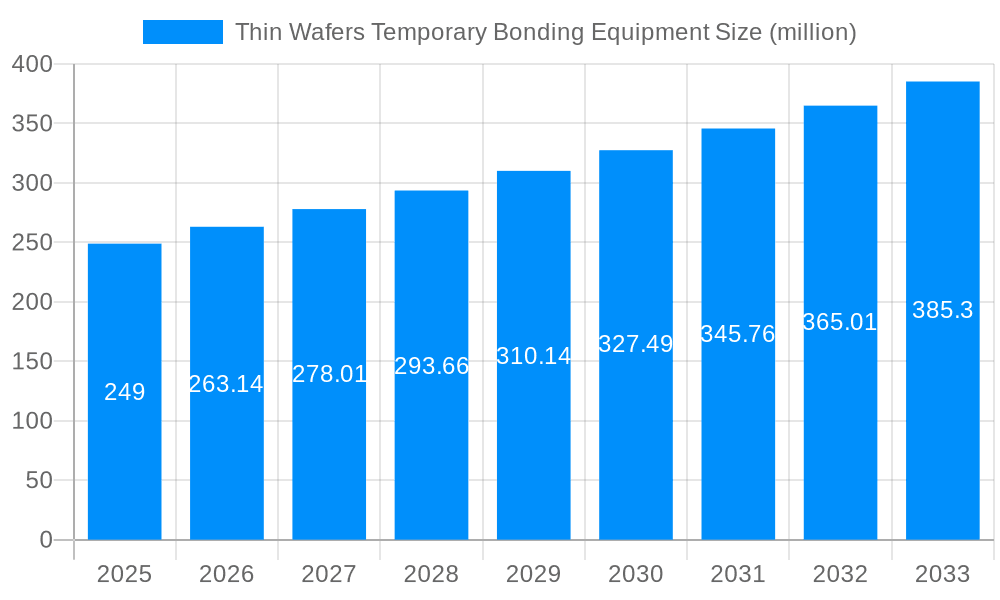

The global Thin Wafers Temporary Bonding Equipment market is poised for robust expansion, projected to reach approximately USD 249 million in 2025, with a significant Compound Annual Growth Rate (CAGR) of 5.7% anticipated over the forecast period of 2025-2033. This growth trajectory is primarily fueled by the escalating demand for advanced semiconductor packaging solutions, particularly within the burgeoning MEMS, Advanced Packaging, and CIS (Contact Image Sensor) sectors. The increasing miniaturization of electronic devices, coupled with the growing complexity of integrated circuits, necessitates sophisticated wafer thinning and temporary bonding processes to maintain wafer integrity and enable the fabrication of high-performance components. Furthermore, the widespread adoption of these technologies in consumer electronics, automotive applications (especially for advanced driver-assistance systems and infotainment), and the Internet of Things (IoT) devices underscores the critical role of thin wafers and the equipment used to handle them. This sustained demand is expected to drive innovation and investment in more efficient and precise bonding equipment.

Several key trends are shaping the Thin Wafers Temporary Bonding Equipment landscape. The shift towards fully automatic bonding equipment is accelerating, offering enhanced throughput, reduced human error, and improved process control, which are crucial for high-volume manufacturing. Innovations in temporary bonding materials, such as advanced polymer-based adhesives that allow for easier debonding without damaging the wafer or die, are also gaining traction. While the market presents significant opportunities, certain restraints could temper its growth. The high initial capital investment required for state-of-the-art bonding equipment, coupled with the stringent quality control and process validation protocols inherent in semiconductor manufacturing, can pose challenges for smaller players. Additionally, fluctuations in the supply chain for raw materials and the skilled labor required to operate and maintain these sophisticated machines could present intermittent hurdles. Despite these constraints, the overarching technological advancements and the insatiable demand for thinner, more powerful semiconductor devices paint a promising picture for the market.

This report provides a comprehensive analysis of the global Thin Wafers Temporary Bonding Equipment market, with a deep dive into trends, driving forces, challenges, and future prospects. The study covers the historical period from 2019 to 2024, establishing a strong foundation for the base year analysis of 2025 and extending into an extensive forecast period from 2025 to 2033. We aim to equip stakeholders with critical insights into a market projected to reach multi-million dollar valuations, driven by the increasing demand for advanced semiconductor manufacturing technologies. The report leverages detailed market segmentation, including equipment types like Semi-Automatic Bonding Equipment and Fully Automatic Bonding Equipment, and key application areas such as MEMS, Advanced Packaging, CIS, and Others. Furthermore, it meticulously examines industry developments and profiles leading players to offer a holistic view of the competitive landscape.

The global Thin Wafers Temporary Bonding Equipment market is poised for significant expansion over the study period (2019-2033), with the base year (2025) serving as a pivotal point for projected growth. A key trend defining this market is the relentless pursuit of miniaturization and increased performance in semiconductor devices. As wafer thicknesses continue to shrink, often reaching sub-50 micron levels, the need for highly precise and reliable temporary bonding solutions becomes paramount. This trend is directly fueled by the burgeoning demand for advanced semiconductor packaging technologies, which enable the stacking of multiple dies and the integration of complex functionalities within smaller footprints. The report will highlight how the market is shifting towards higher throughput and increased automation to meet the escalating production volumes required by sectors like consumer electronics, automotive, and healthcare. We will observe a discernible move from semi-automatic to fully automatic bonding equipment, driven by the desire to minimize human error, enhance yield, and reduce operational costs, especially as production scales into the millions of units annually. The growing adoption of 3D integration techniques, including through-silicon vias (TSVs) and advanced wafer-level packaging (WLP), is a significant market influencer, necessitating equipment capable of handling extremely thin and fragile wafers with utmost care. The report will detail how innovation in bonding materials and processes, such as the utilization of advanced polymers and UV-curable adhesives, is shaping the equipment requirements. Furthermore, the increasing complexity of device architectures, particularly in the MEMS and CIS (CMOS Image Sensor) sectors, demands specialized temporary bonding solutions that can accommodate intricate designs and maintain wafer integrity throughout subsequent processing steps. The market's trajectory indicates a substantial growth in the value of equipment sold, likely reaching tens of millions of dollars annually by the end of the forecast period, reflecting both increased unit sales and the adoption of higher-priced, advanced systems. The interplay between technological advancements in wafer thinning, dicing, and bonding is creating a synergistic ecosystem where advancements in one area directly stimulate demand in others, solidifying the critical role of temporary bonding equipment in the semiconductor value chain.

The burgeoning demand for advanced semiconductor devices, particularly those requiring intricate 3D integration and higher densities, is the primary engine driving the growth of the thin wafers temporary bonding equipment market. As manufacturers push the boundaries of miniaturization and performance, the ability to process increasingly thin wafers – often down to a few tens of microns – becomes indispensable. This capability is essential for applications like stacked memory, heterogeneous integration, and advanced MEMS devices, where wafer thinning is a critical step in achieving desired form factors and functionalities. The rapid evolution of the Internet of Things (IoT) ecosystem, with its proliferation of smart devices, sensors, and wearable technology, further amplifies this demand. Each of these applications relies on increasingly sophisticated semiconductor components, many of which necessitate the processing of ultra-thin wafers. Moreover, the ongoing advancements in artificial intelligence (AI) and high-performance computing (HPC) are creating a surge in demand for powerful processors and specialized chips that benefit from advanced packaging techniques facilitated by temporary bonding. The automotive sector's transition towards electric vehicles and autonomous driving systems, with their increasing reliance on advanced sensors and computing power, also represents a significant growth catalyst. This necessitates the production of high-reliability, high-density semiconductor components processed on thin wafers. Consequently, the market for thin wafers temporary bonding equipment is projected to experience robust growth, with sales potentially reaching tens of millions of dollars annually, reflecting the industry's commitment to investing in the enabling technologies for next-generation semiconductor manufacturing.

Despite the promising growth trajectory, the thin wafers temporary bonding equipment market faces several significant challenges and restraints that could temper its expansion. The inherent fragility of ultra-thin wafers is a primary concern. These wafers are highly susceptible to breakage, chipping, and warpage during handling, bonding, and debonding processes. This necessitates highly specialized and extremely precise equipment, leading to higher capital investment costs for manufacturers. Developing and implementing robust quality control measures to ensure consistent bonding and debonding without damaging these delicate wafers is a complex technical hurdle. Furthermore, the specialized nature of temporary bonding materials, often proprietary formulations, can create supply chain vulnerabilities and compatibility issues between different equipment vendors and material suppliers. Achieving high throughput while maintaining the required level of precision for millions of units is another considerable challenge. The transition to fully automated systems, while desirable for efficiency, requires substantial upfront investment in R&D, automation integration, and skilled personnel, which can be a barrier for smaller players. The stringent quality requirements and low defect tolerance in advanced semiconductor applications mean that any failure in the temporary bonding process can lead to significant yield losses, impacting profitability. The high cost of advanced temporary bonding equipment itself, often running into the millions of dollars per unit for high-end systems, can also be a restraint, particularly for emerging markets or companies with limited capital. Moreover, evolving industry standards and the need for continuous technological upgrades to keep pace with rapid advancements in semiconductor device design present ongoing investment pressures.

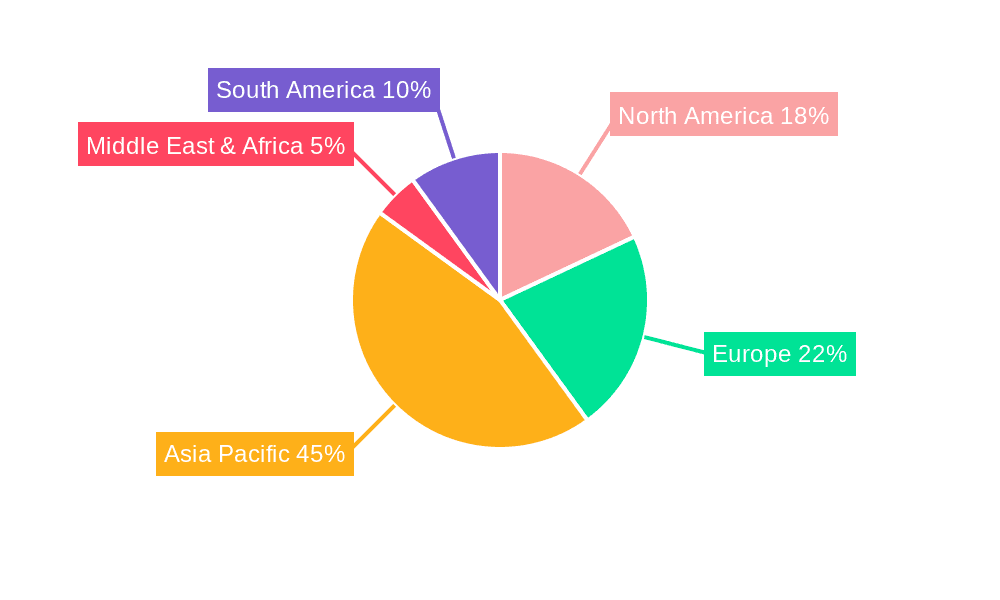

The global Thin Wafers Temporary Bonding Equipment market is characterized by distinct regional strengths and dominant application segments, with the Advanced Packaging segment and the Asia Pacific region poised to lead the market in terms of value and volume.

Advanced Packaging Segment Dominance:

The Advanced Packaging segment is expected to be the primary driver of growth and market share within the thin wafers temporary bonding equipment landscape. This dominance is attributed to several interconnected factors:

Asia Pacific Region as a Dominant Hub:

The Asia Pacific region, particularly countries like Taiwan, South Korea, China, and Japan, is set to dominate the thin wafers temporary bonding equipment market. This regional dominance is underpinned by:

Other Key Segments and Regions:

While Advanced Packaging and Asia Pacific are projected to lead, other segments and regions also contribute significantly. The MEMS and CIS application segments are critical, particularly in their demand for specialized wafer handling and bonding for sensor technologies. In terms of geography, North America remains a significant market due to the presence of leading R&D centers and fabless semiconductor companies, while Europe also shows steady growth driven by its strong automotive and industrial sectors. Fully Automatic Bonding Equipment will witness higher growth than Semi-Automatic Bonding Equipment due to the increasing need for high-volume, high-yield manufacturing.

The industry is propelled by the insatiable demand for advanced semiconductor packaging solutions, which are essential for miniaturization, increased performance, and heterogeneous integration. The rapid proliferation of IoT devices, 5G technology, AI, and autonomous vehicles is creating an unprecedented need for sophisticated semiconductor components, directly stimulating the market for thin wafer processing. Furthermore, ongoing innovation in wafer thinning technologies and materials continues to lower the barriers to entry for ultra-thin wafer processing, making these solutions more accessible.

This report offers an exhaustive examination of the Thin Wafers Temporary Bonding Equipment market, encompassing crucial segments like Semi-Automatic Bonding Equipment and Fully Automatic Bonding Equipment, and delving into key applications such as MEMS, Advanced Packaging, CIS, and Others. It meticulously analyzes market dynamics across regions, identifying dominant areas and potential growth hotspots. The report provides critical insights into industry developments from 2019 to 2033, with a detailed base year analysis for 2025 and an extended forecast period. Stakeholders will gain a comprehensive understanding of the growth catalysts, challenges, and the competitive landscape populated by leading players like EV Group, SUSS MicroTec, Tokyo Electron, and others.

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 5.7% from 2020-2034 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately 5.7%.

Key companies in the market include EV Group, SUSS MicroTec, Tokyo Electron, AML, Mitsubishi, Ayumi Industry, SMEE.

The market segments include Type, Application.

The market size is estimated to be USD 249 million as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3480.00, USD 5220.00, and USD 6960.00 respectively.

The market size is provided in terms of value, measured in million and volume, measured in K.

Yes, the market keyword associated with the report is "Thin Wafers Temporary Bonding Equipment," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Thin Wafers Temporary Bonding Equipment, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.