1. What is the projected Compound Annual Growth Rate (CAGR) of the Thermal Insulation Decorative Integrated Board?

The projected CAGR is approximately XX%.

Thermal Insulation Decorative Integrated Board

Thermal Insulation Decorative Integrated BoardThermal Insulation Decorative Integrated Board by Type (Below 20mm, 20 to 50mm, Over 50mm, World Thermal Insulation Decorative Integrated Board Production ), by Application (Residential Roofs, Walls, Ceilings, Others, World Thermal Insulation Decorative Integrated Board Production ), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2026-2034

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

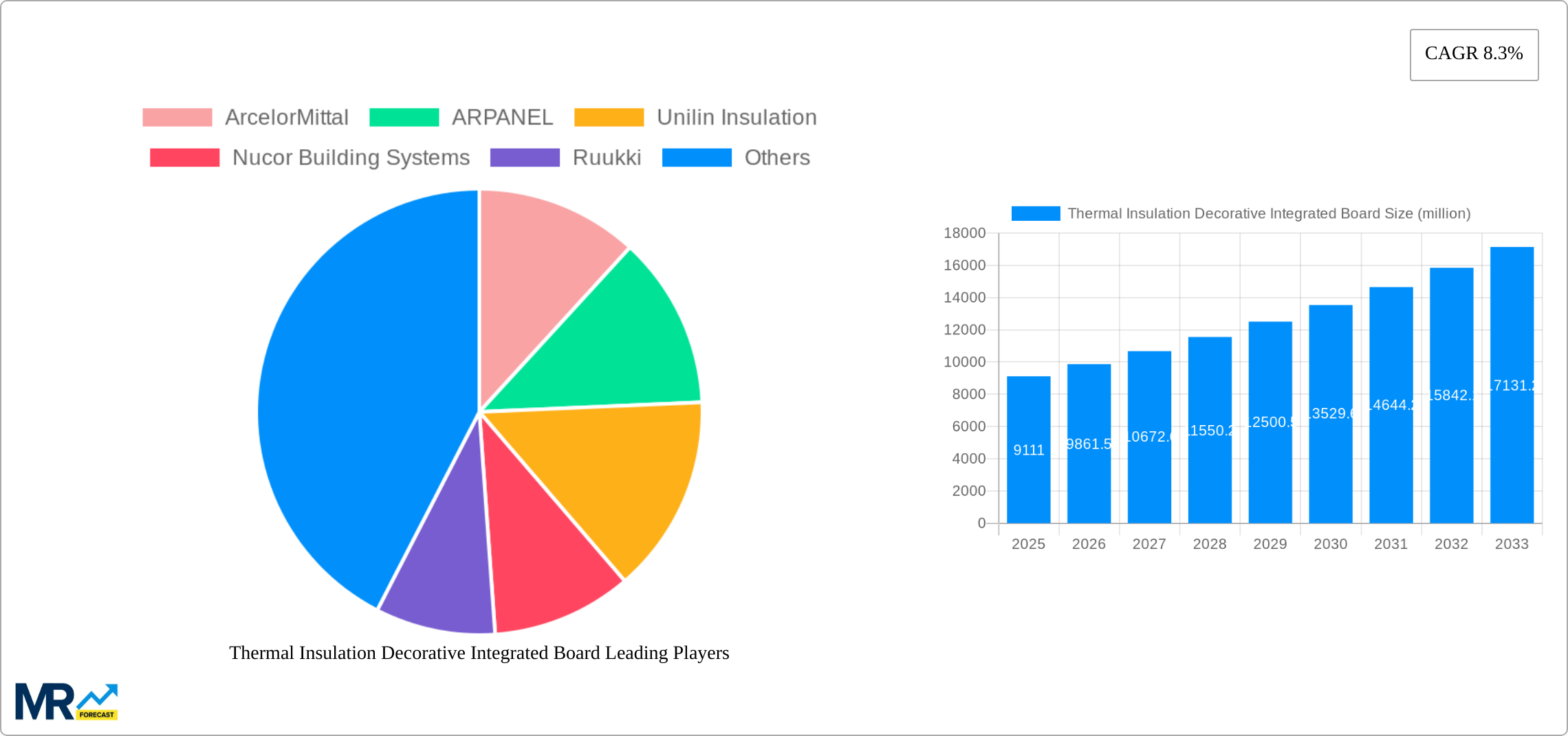

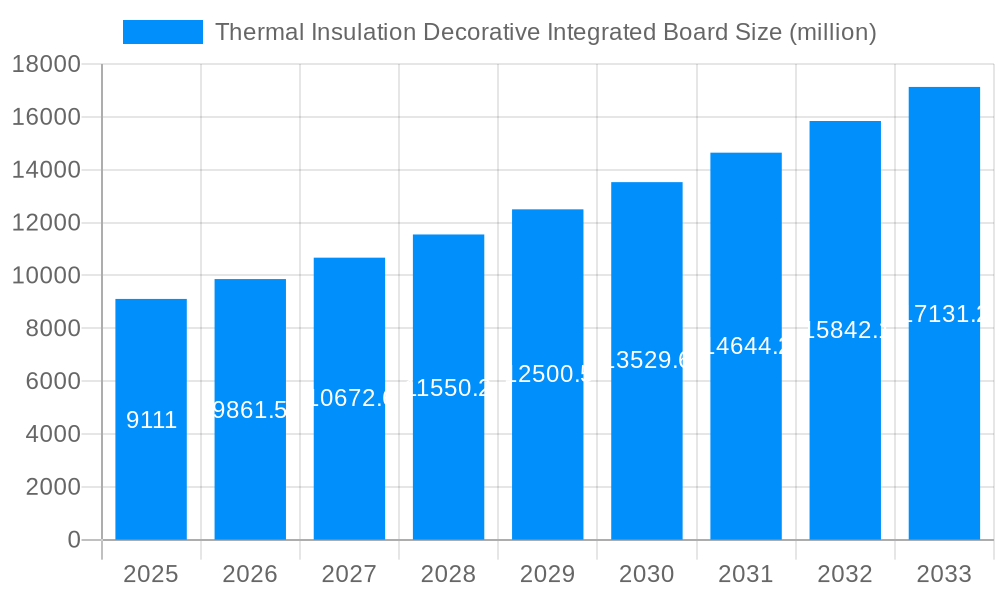

The global thermal insulation decorative integrated board market, valued at $9.111 billion in 2025, is poised for significant growth. Driven by increasing demand for energy-efficient buildings and aesthetically pleasing architectural solutions, the market is projected to experience substantial expansion throughout the forecast period (2025-2033). The rising construction activity in developing economies, coupled with stringent building codes promoting energy conservation, are key drivers. Furthermore, the growing preference for prefabricated and modular construction methods, which often incorporate these boards, is fueling market expansion. Segmentation reveals strong demand across residential applications (roofs, walls, and ceilings), showcasing the board's versatility. Thickness segmentation indicates a high demand for boards in the 20-50mm range, reflecting a balance between insulation efficiency and cost-effectiveness. Major players like ArcelorMittal, Kingspan, and others are actively investing in research and development to introduce innovative products with enhanced insulation properties and design aesthetics. This competitive landscape is fostering innovation and driving down costs, further stimulating market growth. While potential supply chain disruptions and raw material price fluctuations pose some restraints, the overall market outlook remains positive, driven by long-term trends toward sustainable and energy-efficient construction.

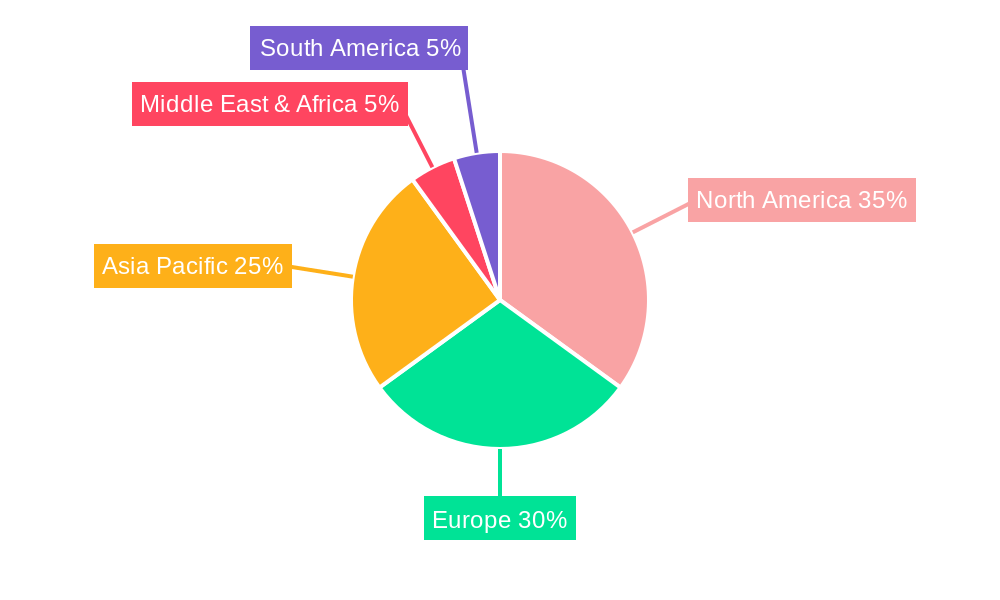

The market's regional distribution reflects the global construction landscape. North America and Europe currently hold substantial market shares, driven by mature construction sectors and high adoption of energy-efficient building technologies. However, rapidly developing economies in Asia-Pacific (specifically China and India) are expected to witness the fastest growth rates during the forecast period, fueled by rapid urbanization and infrastructure development. The Middle East and Africa region also presents promising opportunities due to significant investments in infrastructure projects. Considering the continuous advancements in material science and increasing awareness of sustainable building practices, the market's future trajectory indicates strong and sustained expansion, presenting lucrative investment and growth opportunities for industry stakeholders. To achieve higher profitability, players are focusing on offering a wide range of products in diverse sizes and aesthetics and are also focusing on strategic partnerships to strengthen their market presence.

The global thermal insulation decorative integrated board market is experiencing robust growth, projected to reach several million units by 2033. Driven by increasing awareness of energy efficiency and sustainable building practices, the demand for aesthetically pleasing and energy-saving building materials is surging. This report, covering the period 2019-2033, with a base year of 2025, reveals significant market shifts. The historical period (2019-2024) shows steady growth, while the forecast period (2025-2033) anticipates an accelerated expansion fueled by technological advancements and government initiatives promoting green building technologies. The market is witnessing a transition towards thinner, more efficient boards, particularly in the below 20mm segment, driven by the need for space optimization in modern construction. Simultaneously, the demand for thicker boards (over 50mm) remains strong in regions with extreme climates, highlighting the diverse application needs across different geographical locations. The residential sector, particularly for roofs, walls, and ceilings, constitutes a significant portion of the market, reflecting the growing emphasis on improving home energy performance and comfort. However, the "Others" application segment, encompassing commercial and industrial projects, is also witnessing notable growth, indicating a wider adoption of these integrated boards across various building types. Key players are strategically focusing on innovation, creating products with improved insulation properties, enhanced aesthetics, and simplified installation processes to gain a competitive edge. The market is also seeing increased integration of smart technologies, leading to the emergence of “smart” insulation panels with built-in sensors and monitoring capabilities, further enhancing energy efficiency and building management. The estimated value for 2025 reveals a significant market size, underscoring the potential for future expansion.

Several factors are driving the expansion of the thermal insulation decorative integrated board market. Stringent building codes and regulations aimed at enhancing energy efficiency are a primary driver. Governments worldwide are increasingly implementing policies that mandate higher energy performance standards for new constructions and renovations, thereby boosting the demand for high-performance insulation materials. Furthermore, rising energy costs are compelling homeowners and businesses to seek cost-effective solutions to reduce energy consumption. The integrated nature of these boards, combining insulation and decorative finishes in a single product, offers significant advantages in terms of time and cost savings during construction, further fueling market growth. Growing environmental awareness is also playing a crucial role. Consumers and builders are increasingly seeking eco-friendly building materials with low environmental impact. Manufacturers are responding by developing boards using recycled materials and employing sustainable production processes. The increasing preference for aesthetically appealing building solutions is another critical factor, as these boards offer a variety of finishes and textures, allowing for greater design flexibility and enhanced visual appeal. Finally, advancements in material science and manufacturing technologies are enabling the creation of lighter, stronger, and more efficient boards, further improving their market appeal.

Despite the promising growth outlook, the thermal insulation decorative integrated board market faces certain challenges. High initial costs compared to traditional insulation methods can be a barrier to adoption, especially for budget-conscious consumers and builders. The availability and cost of raw materials fluctuate significantly, impacting production costs and profitability. Furthermore, the durability and longevity of these boards are crucial factors influencing consumer choices. Concerns about the potential for moisture damage or degradation over time can hinder market penetration. Competition from established players in the insulation and building materials industries is intense, requiring manufacturers to constantly innovate and offer superior products at competitive prices. Ensuring consistent quality and performance across different batches is also critical for maintaining consumer trust and building a strong brand reputation. Finally, logistical challenges related to transportation and storage of these relatively large and bulky boards can impact overall market efficiency and cost. Addressing these challenges through continuous improvement in manufacturing processes, material sourcing strategies, and innovative product development is essential for long-term market success.

The market's dominance is distributed across several key regions and segments. Analyzing the data, several stand out:

Europe: Stringent energy efficiency regulations and a high awareness of sustainable construction practices make Europe a leading market for thermal insulation decorative integrated boards. Countries like Germany, France, and the UK show consistently strong demand.

North America: This region exhibits significant growth potential driven by expanding construction activities and increasing focus on energy efficiency improvements.

Asia-Pacific: This rapidly developing region is witnessing a surge in construction projects, particularly in emerging economies like China and India. The growing middle class and increased disposable incomes are further boosting market demand.

Segment: 20 to 50mm: This thickness range finds a balance between insulation performance and ease of installation, making it the most widely adopted segment across diverse applications. This versatility is key to its market leadership.

Application: Residential Walls: Home renovations and new construction are major drivers of demand for this segment. The aesthetic appeal and energy-saving benefits of integrated boards contribute to their popularity in wall applications.

The above regions and segments represent significant market share, though other areas and segments are experiencing growth. The 20 to 50mm thickness range provides an optimal balance between insulation effectiveness and cost, making it a dominant segment. Residential wall applications benefit significantly from the combined insulation and aesthetic properties of these boards. The continued growth in these sectors is anticipated to strengthen their market position in the coming years.

Several factors will catalyze the growth of the thermal insulation decorative integrated board industry. Continued advancements in material science will lead to the development of lighter, stronger, and more energy-efficient boards. Government incentives and subsidies for energy-efficient building materials will significantly boost adoption. Growing awareness of climate change and the importance of sustainable building practices will further drive market demand. The increasing preference for aesthetically pleasing, easy-to-install solutions will make these integrated boards attractive to both consumers and contractors.

This report offers a comprehensive analysis of the thermal insulation decorative integrated board market, providing valuable insights into market trends, growth drivers, challenges, and key players. The report's detailed segmentation, regional analysis, and forecast projections equip stakeholders with the necessary information for strategic decision-making and informed investment strategies. The study's focus on recent developments and future prospects provides a clear roadmap for navigating this rapidly evolving market landscape.

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of XX% from 2020-2034 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately XX%.

Key companies in the market include ArcelorMittal, ARPANEL, Unilin Insulation, Nucor Building Systems, Ruukki, Johns Manville, SOPREMA, Kingspan, Metecno, BCOMS, Mannok Build, Assan Panel, BMI Group UK Ltd, Romakowski, Italpannelli, Lattonedil, TENAX PANEL, Brianza Plastica SpA, Alubel, ProfHolod, Zhejiang Zhenshen, Suzhou Maize, Hebei Salable, Hunan Sanhemei, TOPOLO.

The market segments include Type, Application.

The market size is estimated to be USD 9111 million as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4480.00, USD 6720.00, and USD 8960.00 respectively.

The market size is provided in terms of value, measured in million and volume, measured in K.

Yes, the market keyword associated with the report is "Thermal Insulation Decorative Integrated Board," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Thermal Insulation Decorative Integrated Board, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.