1. What is the projected Compound Annual Growth Rate (CAGR) of the Superalloy for Oil & Gas?

The projected CAGR is approximately 9.07%.

Superalloy for Oil & Gas

Superalloy for Oil & GasSuperalloy for Oil & Gas by Type (Fe based, Ni based, Co based, World Superalloy for Oil & Gas Production ), by Application (Crude Oil, Natrual Gas, World Superalloy for Oil & Gas Production ), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2026-2034

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

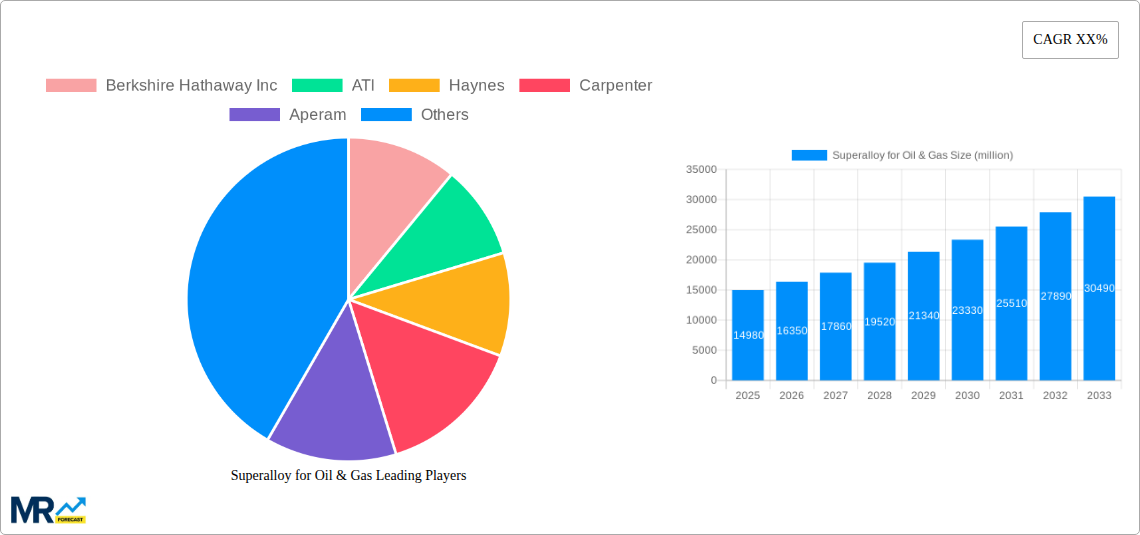

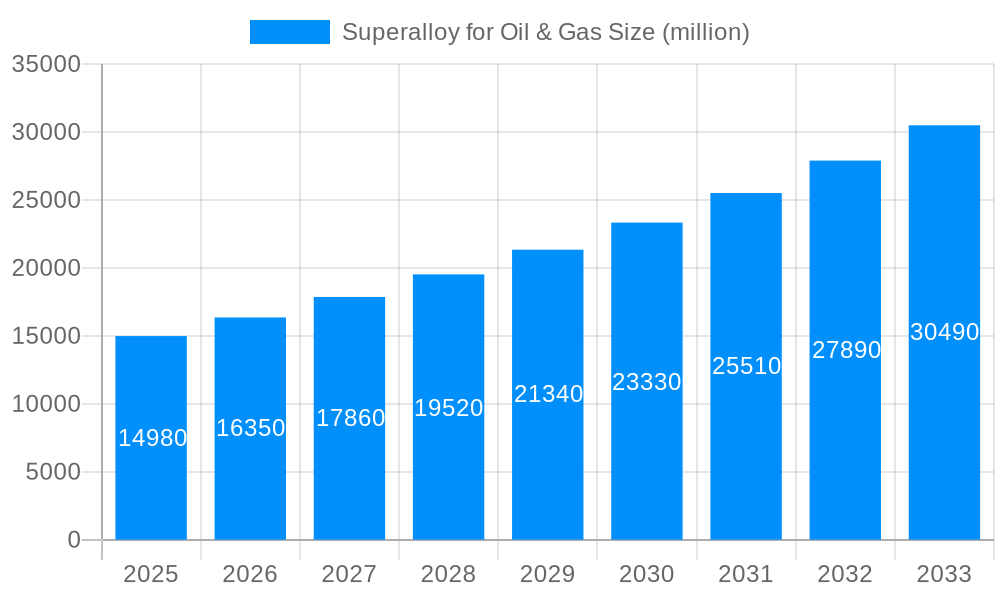

The global Superalloy for Oil & Gas market is poised for significant expansion, projected to reach a substantial value of approximately USD 14.98 billion by 2025. This robust growth is underpinned by a compelling Compound Annual Growth Rate (CAGR) of 9.07% expected between 2025 and 2033. The escalating demand for energy resources, particularly from nascent and developing economies, is a primary catalyst for this upward trajectory. As the exploration and production activities in the oil and gas sector become increasingly complex and challenging, requiring operations in harsh environments such as deep-sea wells and high-pressure, high-temperature formations, the demand for high-performance materials like superalloys is set to surge. These alloys, renowned for their exceptional resistance to corrosion, oxidation, creep, and fatigue, are indispensable for ensuring the integrity and longevity of critical oil and gas infrastructure, including pipelines, wellheads, and processing equipment. Furthermore, technological advancements in refining processes and the need for enhanced operational efficiency are further propelling the adoption of advanced superalloy solutions across the value chain.

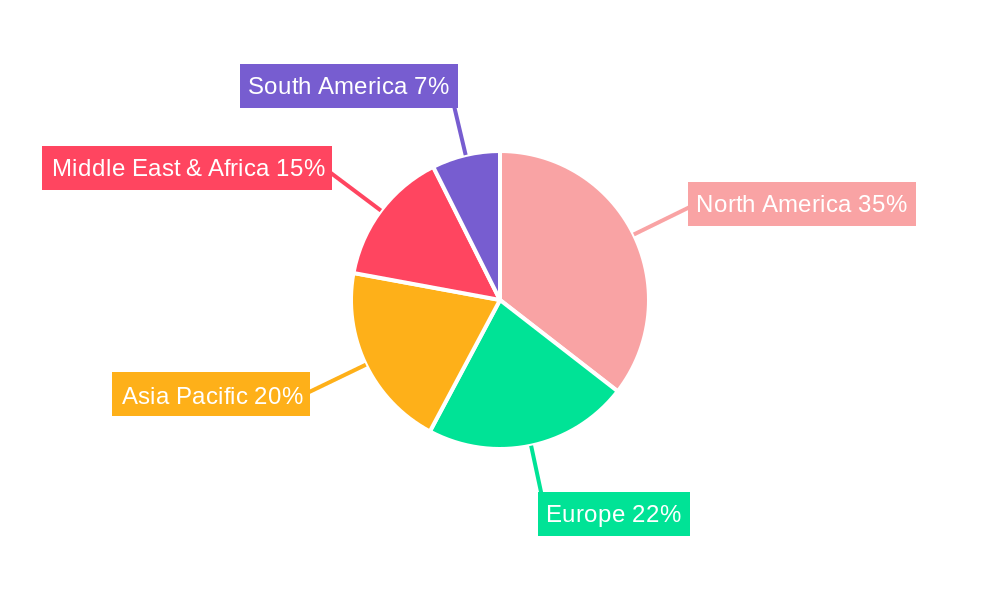

The market segmentation reveals a dynamic landscape, with Fe-based superalloys currently holding a dominant position due to their cost-effectiveness and widespread applicability in less extreme conditions. However, Ni-based and Co-based superalloys are expected to witness significant growth, driven by their superior performance characteristics in highly corrosive and high-temperature environments, which are becoming increasingly prevalent in advanced oil and gas extraction techniques. The application segment for crude oil and natural gas production is the primary revenue generator, reflecting the core demand drivers of the industry. Geographically, North America, particularly the United States, is anticipated to lead the market owing to its extensive and mature oil and gas industry, coupled with significant investments in technological upgrades. Asia Pacific, with its rapidly growing energy consumption and increasing exploration activities, is poised to be the fastest-growing region, presenting substantial opportunities for market players. Key industry players such as Berkshire Hathaway Inc., ATI, Haynes, and Carpenter are actively investing in research and development to innovate and cater to the evolving needs of the oil and gas sector, further shaping the market's future.

This comprehensive report offers an in-depth analysis of the global Superalloy for Oil & Gas market, providing valuable insights for stakeholders navigating this complex and evolving industry. Spanning a study period from 2019 to 2033, with a base year of 2025, the report meticulously examines historical trends, current market dynamics, and future projections. The estimated market value, particularly for the year 2025, is projected to reach several tens of billions of dollars globally, underscoring the significant economic footprint of superalloys in oil and gas exploration and production. The forecast period, from 2025 to 2033, anticipates sustained growth, driven by a confluence of technological advancements, increasing energy demands, and the persistent need for robust materials capable of withstanding extreme operational conditions. The historical period (2019-2024) has laid the groundwork for this trajectory, showcasing the resilience and adaptability of superalloys in the face of fluctuating energy prices and geopolitical shifts.

The global Superalloy for Oil & Gas market is characterized by a distinct set of trends that are shaping its trajectory and influencing investment decisions. A primary trend is the escalating demand for Nickel-based superalloys, which are increasingly favored due to their superior performance in high-temperature and corrosive environments encountered in deep-sea exploration and sour gas fields. These alloys offer unparalleled resistance to stress corrosion cracking and oxidation, crucial for the longevity and safety of critical infrastructure such as subsea pipelines, offshore platforms, and downhole drilling equipment. The market is also witnessing a steady rise in the adoption of advanced alloy compositions, moving beyond traditional formulations to incorporate novel elements and microstructures that further enhance mechanical properties, such as creep strength and fatigue resistance. This innovation is driven by the relentless pursuit of efficiency and safety in more challenging extraction scenarios. Furthermore, there's a noticeable trend towards specialized alloys tailored for specific applications, moving away from a one-size-fits-all approach. For instance, alloys optimized for hydrogen sulfide environments differ significantly from those designed for high-pressure steam applications. The increasing complexity of oil and gas extraction, pushing the boundaries of depth and environmental conditions, necessitates these highly specialized solutions. The market is also experiencing a growing emphasis on sustainability and recyclability, with manufacturers exploring ways to reduce the environmental impact of superalloy production and promote the use of recycled materials. This aligns with broader industry initiatives aimed at achieving net-zero emissions and responsible resource management. The growing adoption of advanced manufacturing techniques, such as additive manufacturing (3D printing) for superalloy components, is another significant trend. This allows for the creation of intricate geometries and customized parts, reducing material waste and lead times. The report estimates the total market value for superalloys in oil and gas, encompassing all types and applications, to be in the tens of billions of dollars in 2025, with a projected CAGR during the forecast period that signifies a healthy and robust market expansion. The segmentation by application, particularly the substantial contribution of Crude Oil and Natural Gas extraction to overall demand, highlights the critical role these superalloys play in securing global energy supplies. The ongoing exploration in frontier regions and the need to maintain existing infrastructure in challenging conditions will continue to fuel this demand, placing the market firmly in the tens of billions of dollars bracket for the foreseeable future.

The global Superalloy for Oil & Gas market is experiencing robust growth, propelled by a confluence of powerful driving forces. Foremost among these is the ever-increasing global demand for energy, a fundamental driver that underpins the entire oil and gas industry. As populations grow and economies develop, the need for reliable energy sources, primarily from crude oil and natural gas, continues to escalate, necessitating advanced materials that can facilitate efficient and safe extraction. Coupled with this is the increasing complexity and harshness of exploration environments. The easily accessible reserves are dwindling, pushing exploration activities into deeper waters, more remote locations, and challenging geological formations characterized by extreme temperatures, pressures, and corrosive substances. Superalloys, with their inherent resistance to these conditions, are indispensable for the functionality and longevity of critical equipment in such environments, from subsea pipelines to downhole tools. Furthermore, stringent safety regulations and environmental standards are also playing a significant role. The oil and gas industry operates under intense scrutiny, demanding materials that can guarantee operational integrity and prevent failures that could lead to environmental disasters or safety hazards. Superalloys provide the necessary reliability and durability to meet these demanding requirements. Technological advancements in exploration and production techniques, such as enhanced oil recovery (EOR) and the exploitation of unconventional resources, often require specialized alloys capable of withstanding novel operational parameters. This continuous innovation in upstream technology indirectly fuels the demand for advanced superalloy solutions, contributing to market growth estimated in the tens of billions of dollars by 2025. The economic imperative to maximize resource recovery and minimize downtime also drives the adoption of high-performance superalloys, as their longevity and resistance to degradation translate into reduced maintenance costs and extended operational life for oil and gas infrastructure.

Despite the strong growth trajectory, the Superalloy for Oil & Gas market faces several significant challenges and restraints that temper its expansion. A primary concern is the volatility of crude oil and natural gas prices. Fluctuations in global energy markets directly impact the capital expenditure budgets of oil and gas companies. When prices are low, exploration and production activities tend to slow down, leading to a reduced demand for new superalloy components and a postponement of critical infrastructure upgrades. This economic uncertainty can significantly influence market growth, potentially impacting the projected tens of billions of dollars valuation. Another considerable restraint is the high cost of superalloys. These advanced materials are inherently expensive to produce due to their complex compositions and specialized manufacturing processes. This high price point can make them prohibitive for certain projects, especially in scenarios where cost optimization is a paramount consideration. Companies may opt for less expensive, though less durable, alternatives for less critical applications. The complex and lengthy qualification and certification processes for new superalloy materials and components also pose a challenge. Given the high-stakes nature of the oil and gas industry, any new material must undergo rigorous testing and validation to ensure its safety and reliability in extreme conditions. This can add significant time and cost to the adoption of innovative alloys, slowing down market penetration. Furthermore, the availability of skilled labor and specialized manufacturing capabilities can be a bottleneck. Producing and fabricating superalloys requires highly specialized expertise and advanced equipment, and a shortage of such resources can limit the overall production capacity and supply chain efficiency, impacting the market's ability to meet demand, especially as it is projected to reach tens of billions of dollars. Finally, environmental regulations and the push towards renewable energy sources present a long-term restraint. As the world transitions towards cleaner energy alternatives, the long-term demand for fossil fuels, and consequently for the superalloys used in their extraction, may face downward pressure in the distant future, although the immediate demand remains robust.

The global Superalloy for Oil & Gas market exhibits distinct regional dominance and segment leadership, with several key players poised to capture substantial market share, projected to be in the tens of billions of dollars globally.

Dominant Regions/Countries:

Dominant Segments:

Nickel-Based Superalloys: This segment is unequivocally the dominant force within the Superalloy for Oil & Gas market, contributing significantly to the projected tens of billions of dollars valuation.

Crude Oil Application: Within the application segment, the extraction and processing of crude oil represent the largest consumer of superalloys. The immense global demand for crude oil, coupled with the ongoing need to access reserves in increasingly difficult locations, ensures a continuous requirement for superalloy components in exploration rigs, production platforms, pipelines, and refining processes. The scale of crude oil operations globally means that even small improvements in material performance can translate into significant economic benefits, further driving the adoption of high-end superalloys. This application segment alone is anticipated to account for a substantial portion of the tens of billions of dollars market value.

The Superalloy for Oil & Gas industry is propelled by several key growth catalysts. The relentless global demand for energy, particularly from crude oil and natural gas, remains a fundamental driver. As conventional reserves deplete, exploration is pushing into more challenging and remote environments, necessitating the use of high-performance superalloys capable of withstanding extreme temperatures, pressures, and corrosive conditions. Technological advancements in drilling and extraction techniques, such as deep-sea exploration and unconventional resource development, further amplify the need for specialized, robust materials. Additionally, stringent safety regulations and the industry's commitment to operational integrity and environmental protection mandate the use of reliable alloys that minimize failure risks.

The Superalloy for Oil & Gas market is characterized by the presence of several prominent and established players, including:

The Superalloy for Oil & Gas sector has witnessed numerous significant developments that have shaped its current landscape and future potential. These advancements have been driven by the need for enhanced performance, cost-effectiveness, and sustainability in oil and gas operations.

This report offers a comprehensive overview of the Superalloy for Oil & Gas market, delving into its intricate dynamics and future prospects. It meticulously analyzes market size and growth projections, with the base year 2025 estimated to see a global market value in the tens of billions of dollars. The study encompasses a detailed examination of key market drivers, including the insatiable global demand for energy and the increasingly challenging environments of oil and gas exploration. It also addresses significant restraints, such as price volatility and the high cost of advanced materials. The report provides in-depth regional analysis, highlighting the dominance of North America and the Middle East, and segment analysis, underscoring the critical role of Nickel-based superalloys in applications like crude oil and natural gas extraction. Furthermore, it identifies leading players and tracks significant industry developments, offering a forward-looking perspective on growth catalysts and emerging trends, making it an indispensable resource for informed decision-making within this vital sector.

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 9.07% from 2020-2034 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately 9.07%.

Key companies in the market include Berkshire Hathaway Inc, ATI, Haynes, Carpenter, Aperam, Eramet Group, AMG, Hitachi Metals, CMK Group, VDM, .

The market segments include Type, Application.

The market size is estimated to be USD XXX N/A as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4480.00, USD 6720.00, and USD 8960.00 respectively.

The market size is provided in terms of value, measured in N/A and volume, measured in K.

Yes, the market keyword associated with the report is "Superalloy for Oil & Gas," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Superalloy for Oil & Gas, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.