1. What is the projected Compound Annual Growth Rate (CAGR) of the Submarine Pipeline?

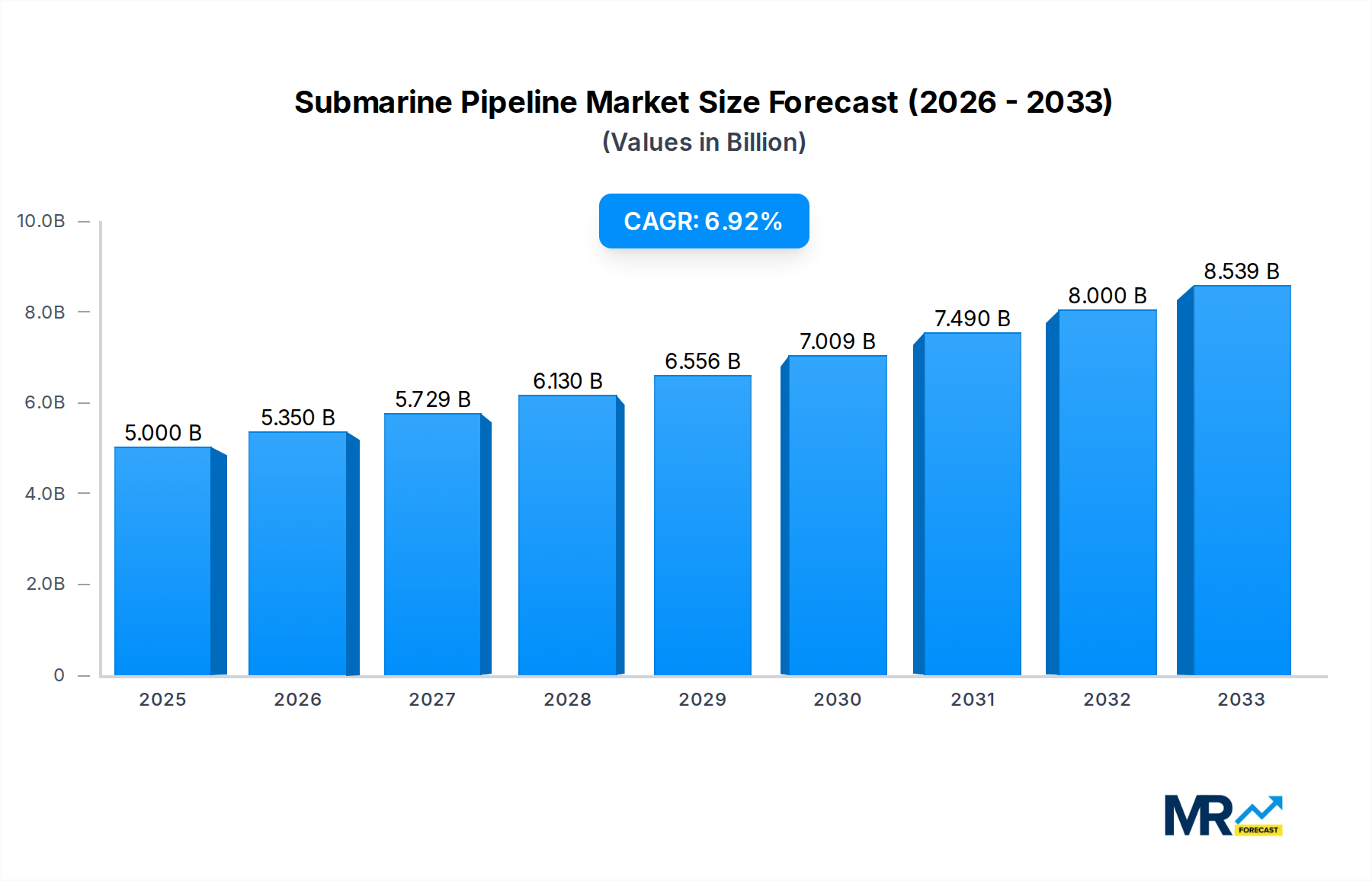

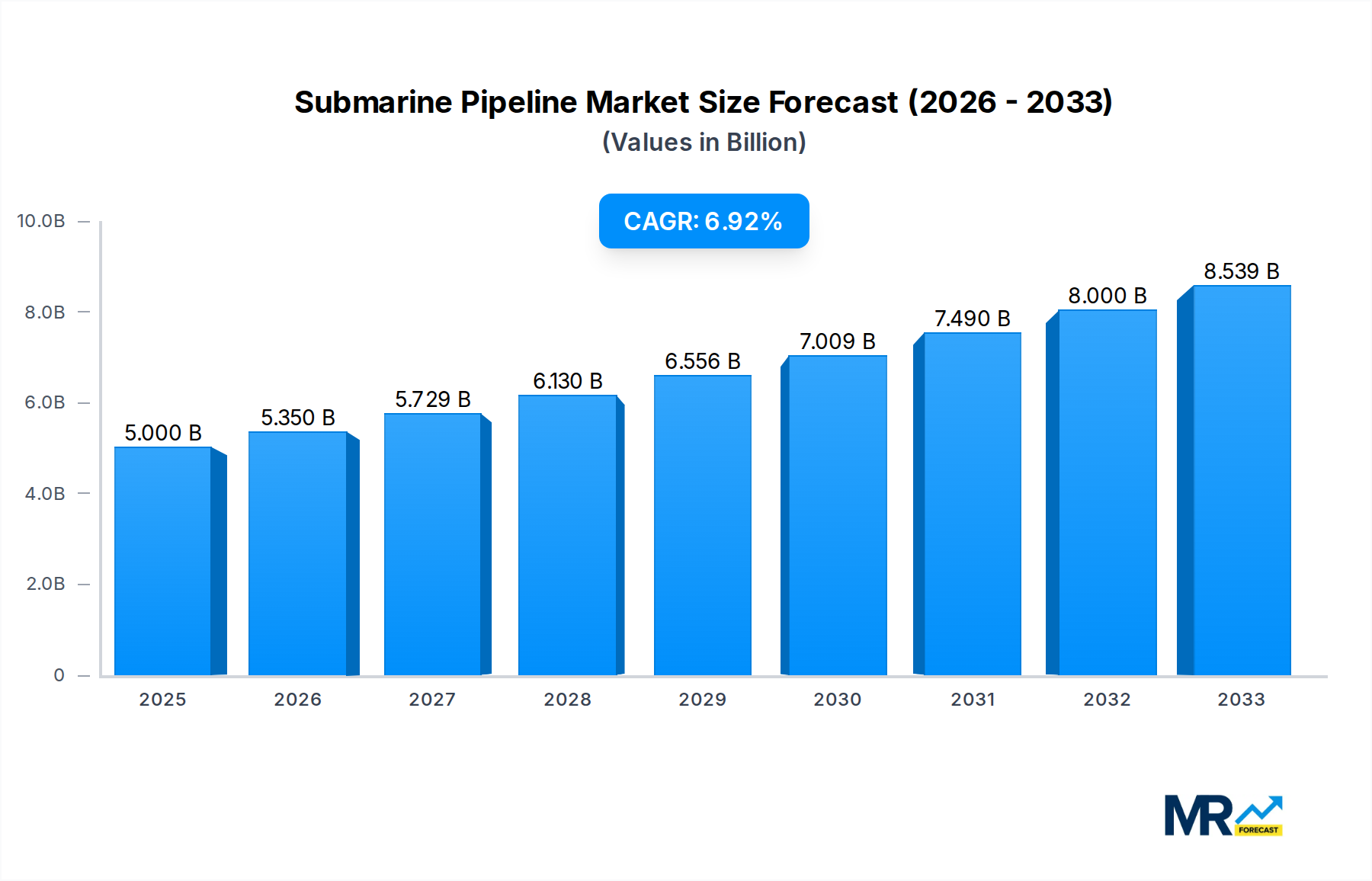

The projected CAGR is approximately 7%.

Submarine Pipeline

Submarine PipelineSubmarine Pipeline by Type (ERW Pipes, LSAW Pipes, SSAW Pipes), by Application (Crude Oil Transmission, Natural Gas Transmission, Other), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2026-2034

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

The global Submarine Pipeline market is poised for substantial growth, projected to reach approximately USD 5 billion by 2025, with an estimated Compound Annual Growth Rate (CAGR) of 7% from 2025 to 2033. This expansion is primarily driven by the escalating global demand for energy resources, particularly crude oil and natural gas, necessitating robust and extensive transportation networks. The increasing investments in offshore exploration and production activities worldwide are key enablers, pushing the need for advanced submarine pipeline infrastructure to facilitate efficient and safe transfer of these commodities from offshore fields to onshore processing facilities. Furthermore, the ongoing modernization of existing offshore energy infrastructure and the development of new deep-sea reserves will continue to fuel market expansion. The market's growth is also bolstered by technological advancements in pipeline manufacturing and installation, enabling operations in more challenging environments and at greater depths.

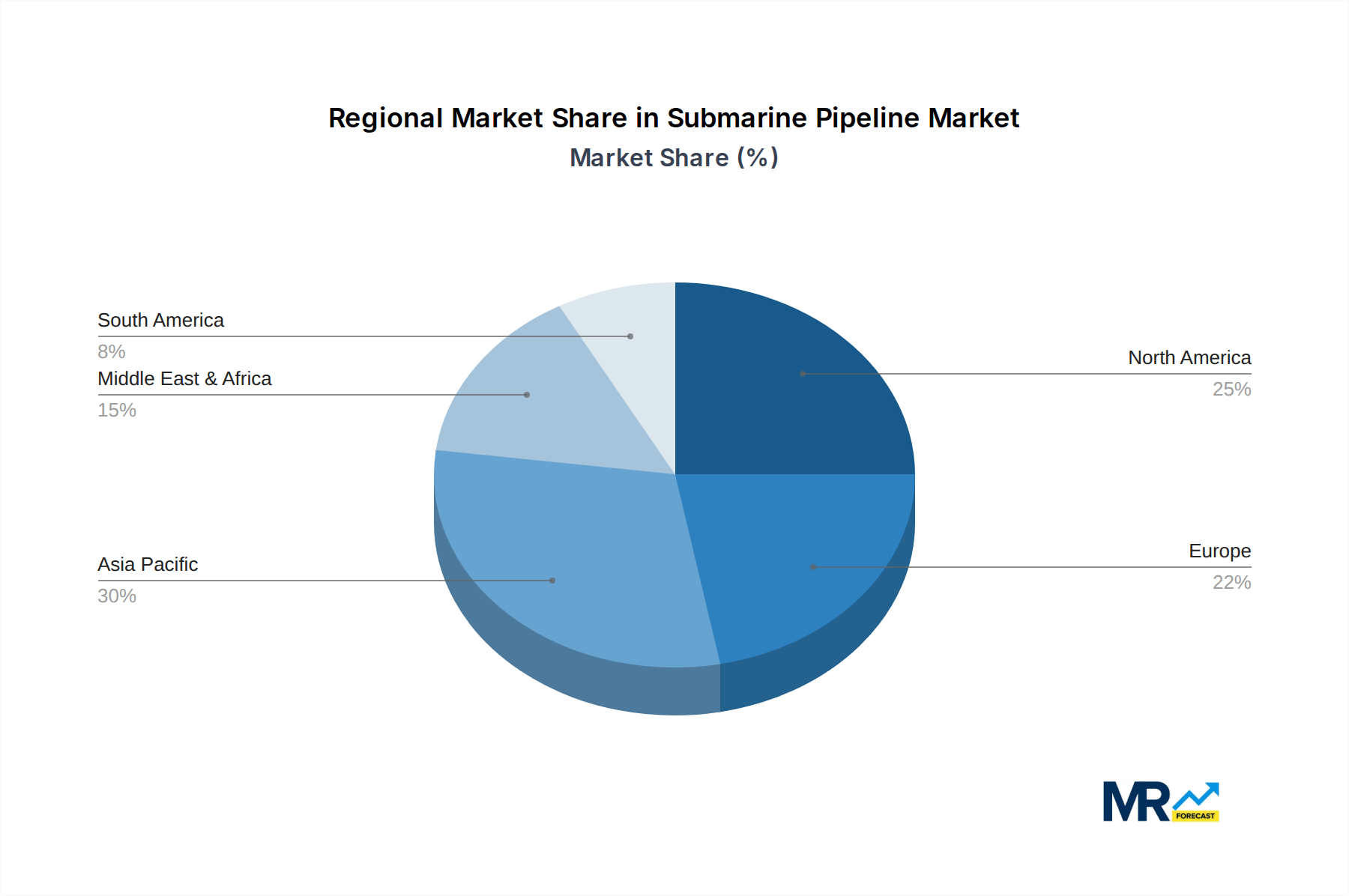

The submarine pipeline market is segmented by Type into ERW Pipes, LSAW Pipes, and SSAW Pipes, with LSAW and SSAW pipes expected to dominate due to their suitability for high-pressure applications and larger diameters required in offshore settings. In terms of Application, Crude Oil Transmission and Natural Gas Transmission represent the largest segments, reflecting the critical role of submarine pipelines in the global energy supply chain. The market is witnessing significant investments from major players like Tenaris, Baosteel, and JFE, who are innovating in materials science and welding technologies to enhance pipeline durability and corrosion resistance. Geographically, the Asia Pacific region, led by China and India, is anticipated to exhibit the fastest growth, fueled by expanding energy consumption and significant investments in offshore infrastructure. North America and Europe remain key markets due to their established offshore oil and gas industries. However, challenges such as stringent environmental regulations and high capital expenditure for offshore projects could pose restraints, emphasizing the need for sustainable and cost-effective solutions.

The global submarine pipeline market is poised for robust expansion, projected to witness a significant leap in value from an estimated $XX billion in 2025 to $XX billion by 2033, exhibiting a compound annual growth rate (CAGR) of XX% during the 2025-2033 forecast period. This impressive growth trajectory is underpinned by the escalating global demand for energy resources, particularly crude oil and natural gas, which are increasingly being extracted from offshore reserves. The historical period between 2019-2024 saw steady advancements, laying the groundwork for the anticipated surge. The 2019-2033 study period encapsulates this dynamic evolution, with 2025 serving as the critical base and estimated year for current market valuation and immediate future projections. The industry is witnessing a pronounced shift towards larger diameter pipelines and advanced materials to accommodate the immense volumes of hydrocarbons being transported. Technological innovations in welding, coating, and installation techniques are also playing a pivotal role, enabling the laying of pipelines in increasingly challenging deep-sea environments. Furthermore, the growing emphasis on offshore wind farm development, while not directly transporting hydrocarbons, requires extensive subsea cabling and infrastructure, indirectly contributing to the overall growth and technological advancements within the subsea construction and pipeline sector. This burgeoning market is characterized by substantial investments, with companies channeling billions into research and development to enhance efficiency, safety, and environmental sustainability of offshore energy transportation. The ongoing exploration and production activities in frontier offshore regions, coupled with the strategic need to connect these resources to onshore processing facilities and consumption hubs, are the primary drivers fueling this multi-billion dollar industry. The increasing complexity of offshore projects, demanding higher operational pressures and longer transmission distances, necessitates continuous innovation and a commitment to high-quality, resilient pipeline solutions.

Several powerful forces are collectively propelling the submarine pipeline market into a new era of expansion. The insatiable global appetite for energy, fueled by industrialization, urbanization, and a growing global population, is the paramount driver. As easily accessible onshore reserves dwindle, exploration and production activities are increasingly shifting towards offshore locations, necessitating the deployment of extensive submarine pipeline networks to transport these valuable resources. This reliance on offshore hydrocarbon extraction directly translates into a greater demand for the pipes and associated infrastructure required for their safe and efficient transmission. Moreover, governments worldwide are investing heavily in energy security and diversification, often prioritizing the development of offshore resources to reduce dependence on volatile geopolitical regions. This strategic imperative translates into significant project pipelines and a sustained demand for submarine pipeline solutions. The ongoing technological advancements in drilling, extraction, and pipeline laying are also crucial enablers. Innovations in materials science have led to the development of stronger, more corrosion-resistant pipes capable of withstanding the harsh subsea environment and high pressures. Simultaneously, advancements in subsea construction vessels and trenching technologies have made it feasible and economically viable to lay pipelines in deeper waters and more challenging terrains, opening up previously inaccessible reserves. The increasing focus on natural gas as a transition fuel also contributes significantly, as many new offshore gas fields require extensive subsea pipeline infrastructure for their development.

Despite the promising growth outlook, the submarine pipeline sector faces a unique set of challenges and restraints that can temper its expansion. The sheer complexity and inherent risks associated with offshore operations are significant. Extreme environmental conditions, including strong currents, seismic activity, and the corrosive nature of seawater, pose constant threats to pipeline integrity and necessitate robust engineering and maintenance strategies. The high capital expenditure required for submarine pipeline projects is a major hurdle. The design, manufacturing, transportation, installation, and ongoing monitoring of subsea pipelines involve substantial investments, often running into billions of dollars per project. This high cost can deter smaller players and make financing a critical factor. Regulatory hurdles and environmental concerns also play a crucial role. Stringent environmental regulations aimed at minimizing the impact of offshore activities on marine ecosystems can lead to delays in project approvals and increase operational costs. The risk of accidental leaks or spills, however remote, carries severe environmental and economic consequences, leading to intense scrutiny and demanding comprehensive risk mitigation measures. Furthermore, the long lead times associated with planning, permitting, and executing large-scale submarine pipeline projects can create market volatility and impact investment decisions. Geopolitical uncertainties and fluctuating commodity prices can also affect project viability and investment flows into the sector.

Within the global submarine pipeline market, several key regions and specific segments are poised to dominate, driven by a confluence of resource availability, investment, and technological adoption.

Dominant Regions/Countries:

Dominant Segments:

Several key factors are acting as catalysts, accelerating the growth of the submarine pipeline industry. The continuous exploration and development of new offshore hydrocarbon reserves, particularly in deepwater and frontier regions, are a primary catalyst. As traditional onshore fields mature, the focus shifts offshore, creating immediate demand for subsea infrastructure. Furthermore, governmental policies promoting energy security, diversification, and the development of domestic resources are significant growth enablers. Investments in renewable energy infrastructure, such as offshore wind farms, also indirectly foster growth by driving innovation in subsea cable laying and offshore construction technologies, which can be leveraged for pipeline projects.

The submarine pipeline sector is characterized by a landscape of highly specialized and technologically advanced companies, many of whom operate on a global scale and manage projects worth billions of dollars. These include:

The submarine pipeline sector has seen a consistent stream of significant developments aimed at enhancing efficiency, safety, and operational capabilities. These advancements often represent investments in the hundreds of millions to billions of dollars and are crucial for tackling increasingly complex offshore projects.

This comprehensive report offers an in-depth analysis of the global submarine pipeline market, providing critical insights for stakeholders. Covering the study period from 2019-2033, with 2025 as the base and estimated year, it meticulously analyzes the market's evolution. The report delves into the projected market value, estimated to reach $XX billion by 2033, and forecasts a robust CAGR of XX% during the 2025-2033 forecast period. It meticulously examines the driving forces, challenges, and growth catalysts shaping the industry, offering a nuanced understanding of its dynamics. Furthermore, it identifies key regions and segments poised for dominance, providing valuable strategic intelligence. The report also features an exhaustive list of leading players, alongside significant developments and technological advancements within the sector, offering a holistic view of this multi-billion dollar industry.

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 7% from 2020-2034 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately 7%.

Key companies in the market include Baoji Petroleum Steel Pipe, JFE, Jindal SAW Ltd, EUROPIPE Group, Essar Steel, Jiangsu Yulong Steel Pipe, American SpiralWeld Pipe Company, LLC, Zhejiang Kingland, Tenaris, Shengli Oil & Gas Pipe, CNPC Bohai Equipment Manufacturing, CHU KONG PIPE, Baosteel, Borusan Mannesmann, .

The market segments include Type, Application.

The market size is estimated to be USD XXX N/A as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3480.00, USD 5220.00, and USD 6960.00 respectively.

The market size is provided in terms of value, measured in N/A and volume, measured in K.

Yes, the market keyword associated with the report is "Submarine Pipeline," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Submarine Pipeline, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.