1. What is the projected Compound Annual Growth Rate (CAGR) of the Structural Adhesives and Sealants for EV Batteries?

The projected CAGR is approximately 35.9%.

Structural Adhesives and Sealants for EV Batteries

Structural Adhesives and Sealants for EV BatteriesStructural Adhesives and Sealants for EV Batteries by Type (Epoxy, Polyurethane, Silicone, Acrylate, Others, World Structural Adhesives and Sealants for EV Batteries Production ), by Application (Passenger Vehicle, Commercial Vehicle, World Structural Adhesives and Sealants for EV Batteries Production ), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2026-2034

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

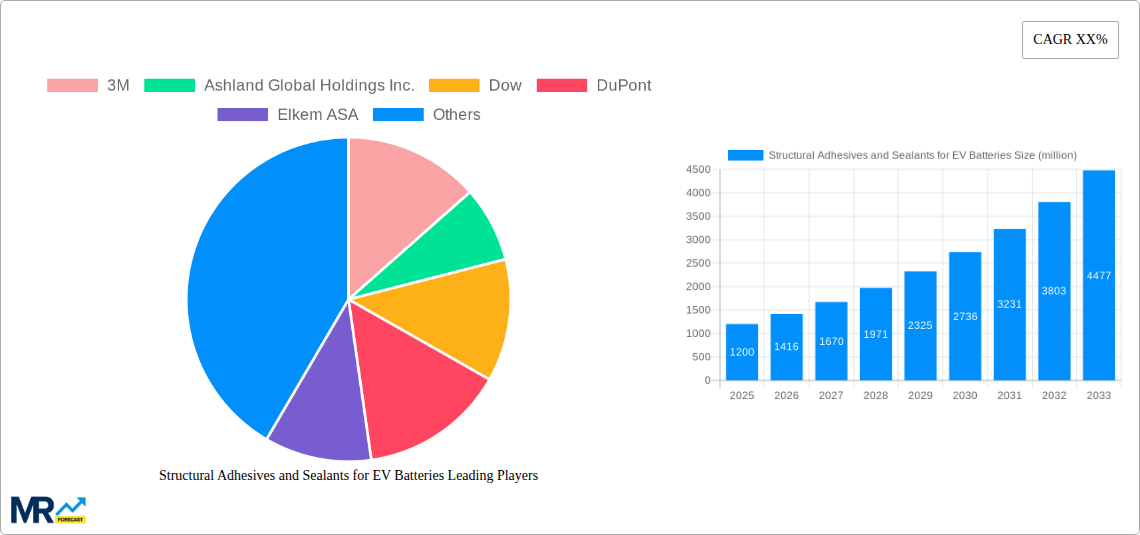

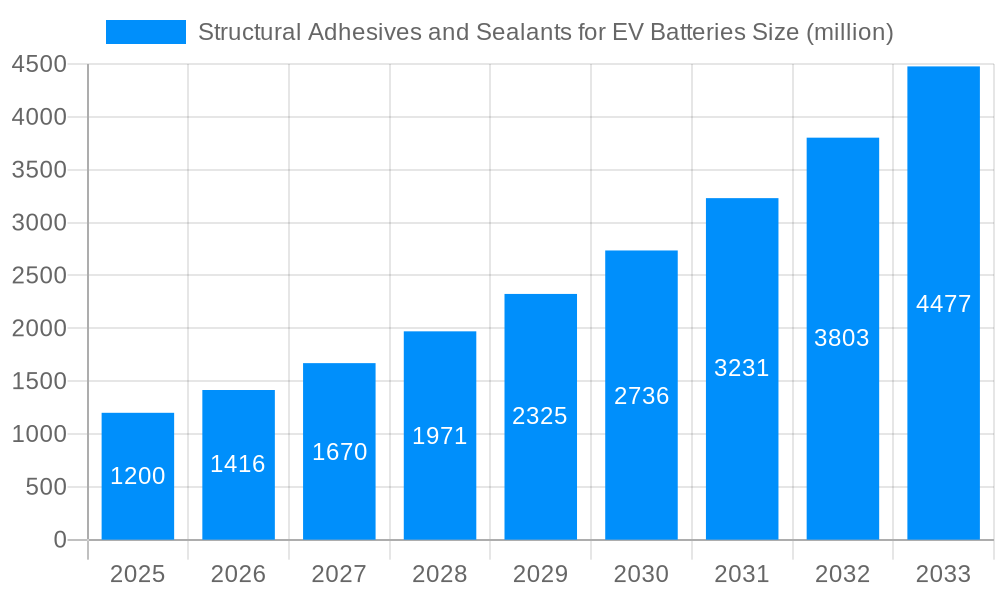

The global market for structural adhesives and sealants in electric vehicle (EV) battery production is poised for significant expansion, driven by the escalating demand for electric mobility and the critical role these materials play in ensuring battery safety, performance, and longevity. Valued at an estimated $1,200 million in 2025, the market is projected to witness a robust Compound Annual Growth Rate (CAGR) of 18% over the forecast period of 2025-2033. This growth is fundamentally underpinned by the increasing production volumes of EVs globally, necessitating advanced bonding and sealing solutions that can withstand the stringent demands of battery packs, including thermal management, vibration resistance, and electrical insulation. Key market drivers include government initiatives promoting EV adoption, advancements in battery technology leading to higher energy densities and more complex battery architectures, and the continuous pursuit of lighter, more efficient vehicle designs, where structural adhesives offer a compelling alternative to traditional mechanical fasteners. The emphasis on enhanced safety features and extended battery lifespan further fuels the adoption of high-performance adhesives and sealants.

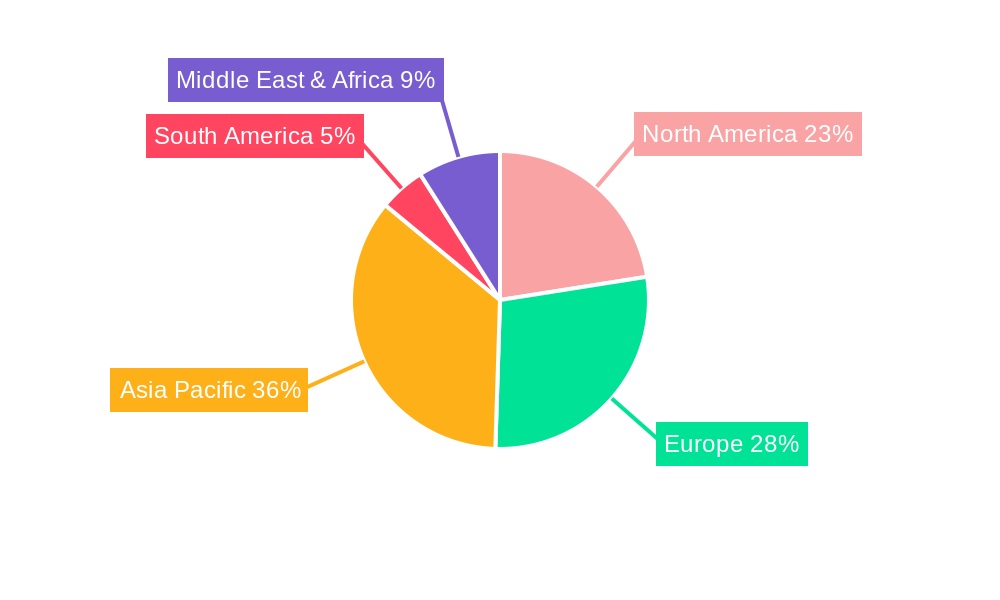

The market is segmented by type, with Epoxy, Polyurethane, and Silicone adhesives and sealants holding substantial shares due to their versatile properties, including strong adhesion, excellent thermal conductivity, and chemical resistance. Acrylate-based solutions are also gaining traction for their rapid curing times and good adhesion to a variety of substrates. In terms of application, the Passenger Vehicle segment dominates, reflecting the larger production volumes of electric passenger cars. However, the Commercial Vehicle segment is expected to witness faster growth as electrification expands into trucks, buses, and vans, demanding robust and durable battery solutions. Geographically, Asia Pacific, led by China, is the largest market, owing to its dominant position in EV manufacturing. North America and Europe are also significant markets, driven by strong regulatory support and growing consumer demand for EVs. Major industry players like 3M, Dow, DuPont, and Henkel are at the forefront of innovation, developing specialized formulations to meet the evolving needs of the EV battery industry.

The global market for structural adhesives and sealants in Electric Vehicle (EV) batteries is experiencing a significant surge, driven by the relentless expansion of the EV sector. This burgeoning demand is reshaping manufacturing processes and material science, making these specialized chemicals indispensable components. The market, which was valued in the hundreds of millions of USD in the historical period (2019-2024), is projected to witness robust growth throughout the forecast period (2025-2033). The base year (2025) serves as a pivotal point for understanding the current landscape, with estimations for this year suggesting a sustained upward trajectory. The primary driver behind this trend is the increasing adoption of EVs globally, fueled by government incentives, growing environmental consciousness, and advancements in battery technology that enhance range and performance.

Structural adhesives and sealants play a critical role in EV battery pack assembly, contributing to enhanced safety, durability, thermal management, and overall structural integrity. They are instrumental in bonding battery cells to modules, modules to packs, and sealing battery enclosures against environmental ingress such as moisture and dust. The need for lightweight yet robust materials to improve vehicle efficiency also bolsters the demand for these advanced bonding solutions. The study period (2019-2033) encompasses a dynamic phase of EV development, from early adoption to mass market penetration, during which the requirements for battery materials, including adhesives and sealants, have become increasingly sophisticated. As battery chemistries evolve and energy densities increase, the performance demands on adhesives and sealants will only intensify, necessitating continuous innovation in product development. The market's expansion is not merely about volume but also about the increasing sophistication of the solutions being offered, with a focus on high-performance, specialized formulations designed to meet the unique challenges of EV battery architectures. The ongoing research and development efforts are focused on achieving improved adhesion to diverse battery materials, enhanced thermal conductivity for efficient heat dissipation, and superior fire retardancy to ensure passenger safety. This evolution signifies a fundamental shift in how EV battery packs are constructed, moving towards integrated and bonded structures that offer significant advantages over traditional mechanical fastening methods.

The remarkable growth of the structural adhesives and sealants market for EV batteries is underpinned by a confluence of powerful driving forces. Foremost among these is the unprecedented global acceleration in electric vehicle adoption. Governments worldwide are implementing stringent emission regulations and offering substantial incentives for EV purchases, directly translating into higher production volumes for electric cars, vans, and trucks. This surge in EV manufacturing necessitates a proportional increase in the consumption of essential battery components, including specialized adhesives and sealants.

Furthermore, advancements in battery technology are acting as a significant catalyst. As EV manufacturers strive to increase battery energy density, improve charging speeds, and enhance overall battery lifespan, the design and assembly of battery packs are becoming more complex. Structural adhesives and sealants are crucial for achieving the intricate bonding and sealing required for these next-generation battery architectures, ensuring structural integrity, thermal management, and protection against harsh operating conditions. The drive for lightweighting in the automotive industry to improve fuel efficiency (or electric range) also favors the use of adhesives over heavier mechanical fasteners, further boosting the demand for these versatile bonding solutions. The inherent ability of adhesives to distribute stress more evenly across bonded surfaces also contributes to improved battery pack durability and longevity.

Despite the robust growth trajectory, the structural adhesives and sealants market for EV batteries is not without its challenges. One of the primary restraints is the stringent regulatory landscape and evolving safety standards surrounding EV batteries. Manufacturers must adhere to rigorous guidelines for fire safety, thermal runaway prevention, and environmental impact, which necessitates the development and validation of adhesives and sealants that meet these demanding specifications. This can lead to longer development cycles and increased R&D costs.

Another significant challenge lies in the complex material compatibility and processing requirements. EV battery packs utilize a diverse range of materials, including various metals, plastics, and composite materials, each with unique surface properties. Developing adhesives and sealants that can reliably bond to these disparate substrates while maintaining long-term performance under extreme temperatures and vibration is a continuous technical hurdle. The cost-effectiveness of these specialized materials also remains a consideration, especially as EV manufacturers aim to reduce the overall cost of electric vehicles to achieve wider market penetration. Balancing high performance with competitive pricing is a delicate act for adhesive and sealant suppliers. Furthermore, the supply chain volatility for certain raw materials used in adhesive formulations can pose risks to production continuity and pricing stability, impacting market dynamics.

Key Regions & Countries Dominating the Market:

Asia-Pacific: This region is poised to be the dominant force in the structural adhesives and sealants for EV batteries market. This dominance stems from:

Europe: Europe represents another critical and rapidly growing market for these materials, driven by:

North America: The North American market is also experiencing substantial growth, propelled by:

Key Segments Dominating the Market:

Type: Epoxy:

Application: Passenger Vehicle:

The structural adhesives and sealants industry for EV batteries is experiencing accelerated growth due to several key catalysts. The ever-increasing global demand for electric vehicles, driven by environmental concerns and government mandates, is the primary growth engine. As EV production volumes climb, so does the need for these essential battery assembly materials. Innovations in battery technology, leading to higher energy densities and more complex pack designs, necessitate advanced bonding and sealing solutions, thereby spurring demand for specialized formulations. Furthermore, the continuous push for lightweighting vehicles to improve energy efficiency favors adhesives over traditional mechanical fasteners, offering a lightweight yet robust assembly solution. Finally, the development of new adhesive chemistries with enhanced thermal conductivity, fire retardancy, and adhesion capabilities is expanding their application scope and driving market penetration.

This comprehensive report delves deep into the dynamic global market for structural adhesives and sealants used in electric vehicle (EV) batteries. It meticulously analyzes market trends, key drivers, and prevailing challenges from the historical period (2019-2024) through the study period (2019-2033), with a specific focus on the base year (2025) and forecast period (2025-2033). The report provides granular insights into production volumes, estimated at hundreds of millions of units, and examines the market's segmentation by product type (Epoxy, Polyurethane, Silicone, Acrylate, Others) and application (Passenger Vehicle, Commercial Vehicle). Geographical market landscapes, technological innovations, and the competitive strategies of leading players are thoroughly investigated. The report aims to equip stakeholders with actionable intelligence for strategic decision-making in this rapidly evolving and critical sector of the automotive industry.

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 35.9% from 2020-2034 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately 35.9%.

Key companies in the market include 3M, Ashland Global Holdings Inc., Dow, DuPont, Elkem ASA, HB Fuller Company, Henkel AG & Co. KGaA, Huntsman Corporation, Sika AG, Wacker Chemie AG, Dymax Corporation, Jowat SE, LORD Corporation, Permabond LLC, Polytec PT GmbH, .

The market segments include Type, Application.

The market size is estimated to be USD XXX N/A as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4480.00, USD 6720.00, and USD 8960.00 respectively.

The market size is provided in terms of value, measured in N/A and volume, measured in K.

Yes, the market keyword associated with the report is "Structural Adhesives and Sealants for EV Batteries," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Structural Adhesives and Sealants for EV Batteries, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.