1. What is the projected Compound Annual Growth Rate (CAGR) of the Steel Canned Food Packaging?

The projected CAGR is approximately 7.3%.

Steel Canned Food Packaging

Steel Canned Food PackagingSteel Canned Food Packaging by Type (Pressurized Food Packaging Cans, Vacuum Food Packaging Cans, World Steel Canned Food Packaging Production ), by Application (Readymade Meals, Meat, Sea Food, Others, World Steel Canned Food Packaging Production ), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2026-2034

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

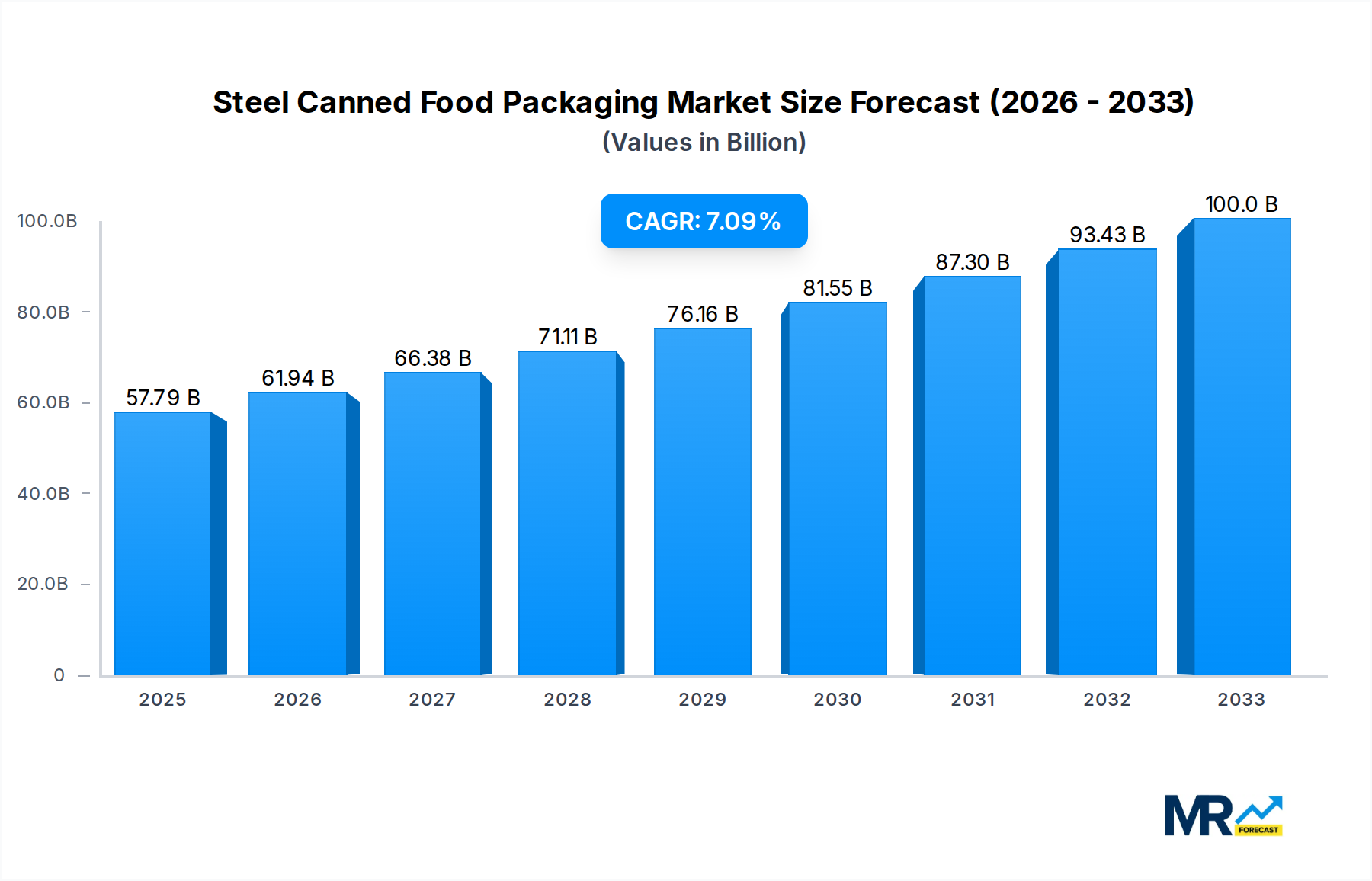

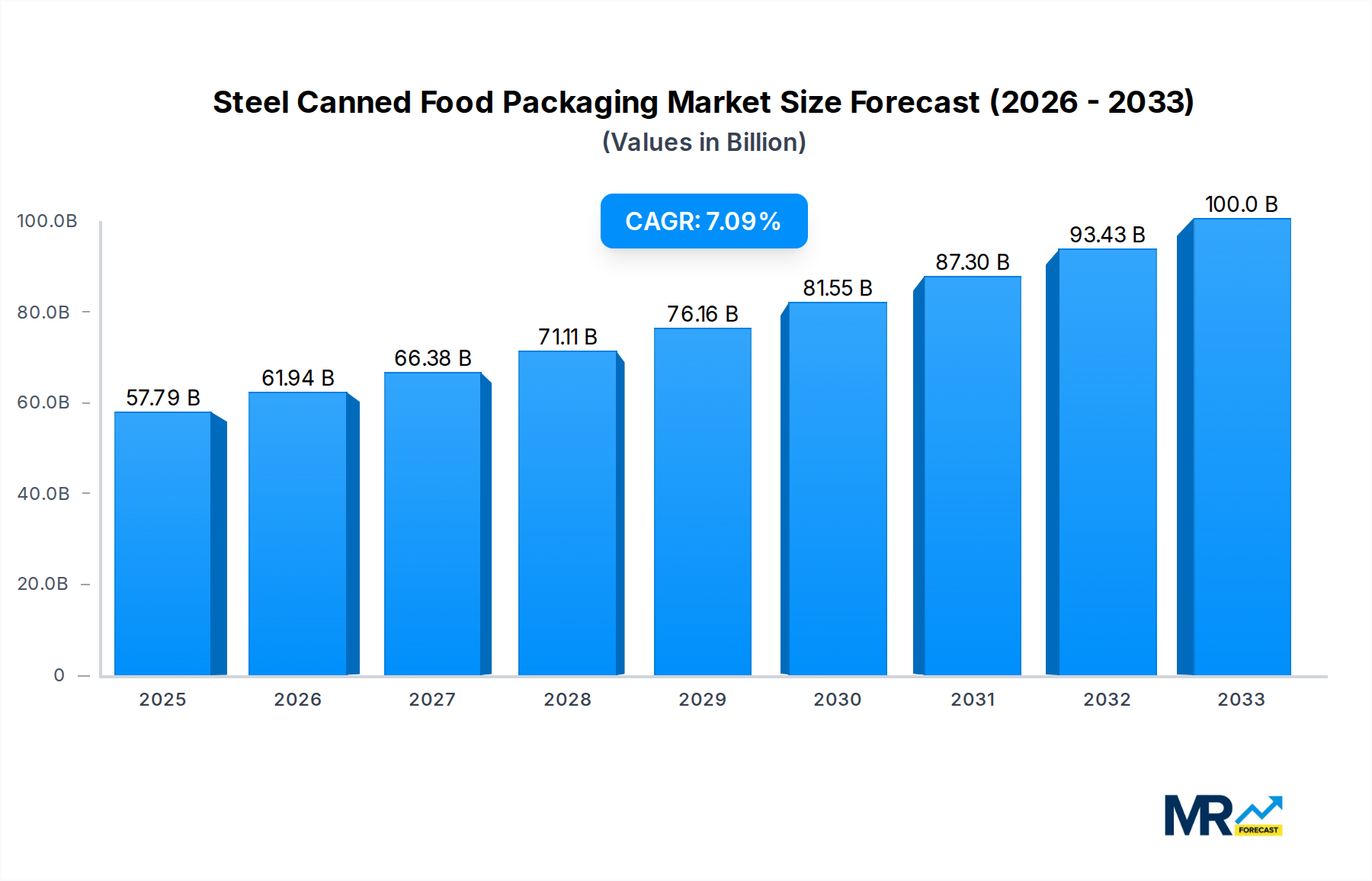

The global steel canned food packaging market is poised for significant expansion, projected to reach 57.79 billion by 2025, with a Compound Annual Growth Rate (CAGR) of 7.3% from the base year 2025. This growth is primarily fueled by increasing consumer preference for convenient, shelf-stable food solutions, including ready-to-eat meals. Steel cans offer superior product protection, extending shelf life and minimizing food waste, thereby supporting sustainability initiatives. Advancements in manufacturing, such as lightweighting and enhanced coatings, are improving efficiency and the environmental profile of steel packaging, making it a preferred choice for food producers.

While challenges such as raw material price volatility and the environmental impact of steel production exist, industry players are actively pursuing innovative solutions and sustainable sourcing strategies. The market is segmented by packaging type (pressurized and vacuum) and application (ready-made meals, meat, seafood, etc.). Ready-to-eat meals and meat products represent the largest application segments. Leading companies such as Ball Corporation, Crown Holdings, and Amcor Limited are investing in research and development and expanding their global presence, particularly in emerging economies.

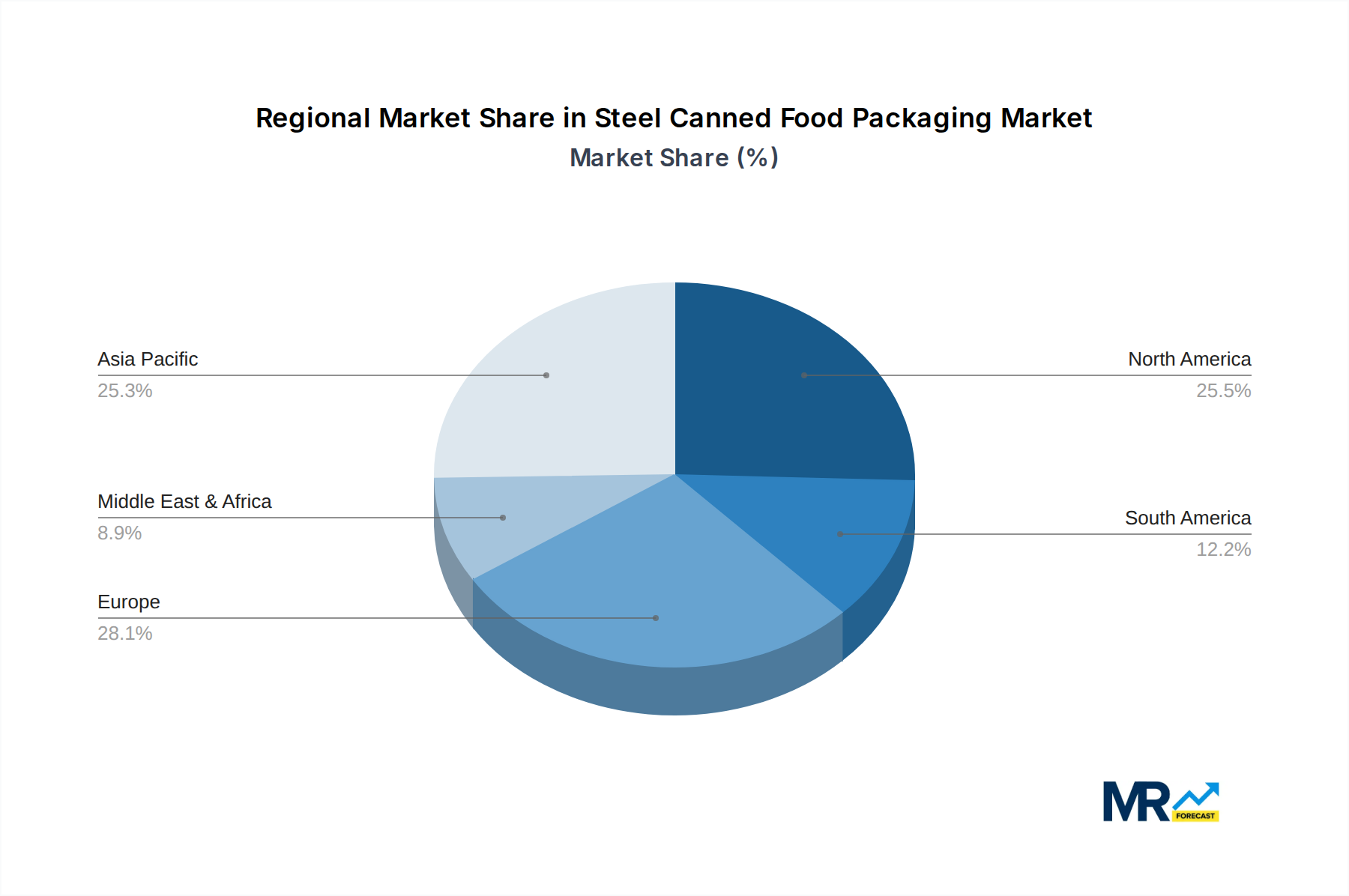

Geographically, the Asia-Pacific and North America regions exhibit strong market performance due to high canned food consumption. Emerging markets in Africa and South America offer substantial growth potential. The market's positive growth trajectory is expected to continue, albeit with regional variations influenced by economic factors and evolving consumer preferences. Intense competition drives innovation and strategic acquisitions among established players. Future market dynamics will be shaped by increasing demand for sustainable packaging, automation in manufacturing, and evolving global food safety regulations. Enhancing the recyclability of steel cans is a key focus for addressing environmental concerns and ensuring sustained market growth.

The global steel canned food packaging market is experiencing robust growth, driven by several interconnected factors. The increasing demand for convenient and shelf-stable food products, particularly in developing economies with burgeoning populations, is a key driver. Consumers are increasingly prioritizing convenience, leading to a surge in demand for ready-to-eat meals and other processed foods, many of which rely heavily on steel cans for packaging. Furthermore, the inherent safety and preservation properties of steel cans make them a preferred choice for food manufacturers seeking to extend the shelf life of their products and minimize waste. This is particularly important in regions with limited refrigeration infrastructure. The market also witnesses continuous innovation in can design and manufacturing processes, leading to lighter, more sustainable, and aesthetically appealing packaging solutions. This includes advancements in coatings and linings to enhance protection against corrosion and maintain product quality. The shift towards sustainable and eco-friendly packaging materials is also influencing the market, with manufacturers investing in recycled steel and exploring more environmentally conscious production methods. However, fluctuating raw material prices, particularly steel prices, pose a challenge to the industry's stability and profitability. Despite this, the overall trend indicates a positive outlook for the steel canned food packaging market, with sustained growth projected throughout the forecast period (2025-2033). The market is estimated to reach XXX million units by 2025 and is expected to surpass XXX million units by 2033, showcasing a significant Compound Annual Growth Rate (CAGR). This growth is fueled by the aforementioned factors and a continued focus on improving product safety and consumer convenience.

Several key factors are propelling the growth of the steel canned food packaging market. The rising global population, especially in developing nations, is driving increased demand for convenient and affordable food options. Steel cans offer an effective solution for preserving food and extending its shelf life, making them an ideal choice for mass production and distribution. The inherent strength and durability of steel cans ensure product protection during transportation and storage, minimizing spoilage and waste. The industry's continuous innovation in can design and manufacturing processes, resulting in lighter and more sustainable cans, also contributes to the market's expansion. This focus on sustainability aligns with growing consumer awareness of environmental issues, prompting a shift towards eco-friendly packaging solutions. Furthermore, the increasing adoption of advanced technologies in the manufacturing process enhances efficiency and reduces production costs, making steel canned food packaging more competitive. Finally, the robust regulatory framework supporting food safety further underscores the importance of secure and reliable packaging solutions, like steel cans, thus boosting market expansion.

Despite its growth potential, the steel canned food packaging market faces certain challenges. Fluctuations in steel prices represent a significant risk, impacting the overall cost of production and potentially affecting manufacturers' profit margins. The industry also competes with alternative packaging materials such as flexible packaging and plastic containers, which offer lower costs in some instances. Environmental concerns regarding steel production and disposal, despite ongoing efforts towards sustainability, also pose a challenge. Stringent regulatory requirements related to food safety and environmental protection necessitate continuous investments in compliance and innovation. Moreover, the market faces the challenge of adapting to changing consumer preferences, including the growing demand for sustainable and eco-friendly packaging alternatives. Finally, the economic slowdown in certain regions can negatively impact consumer spending on processed food products, thus affecting the demand for steel canned food packaging.

The Asia-Pacific region is projected to dominate the steel canned food packaging market during the forecast period (2025-2033). This dominance is attributed to several factors:

Within the segments, the Meat application is expected to hold a significant market share. The high demand for processed meat products, such as canned meats, contributes to this segment's dominance. Further, Pressurized Food Packaging Cans represent another significant segment, due to their suitability for products requiring pressure sterilization to maintain quality and extend shelf life.

The market's dynamism is also observed in North America and Europe, which, while mature markets, show consistent growth driven by innovation in packaging design, sustainable practices and increased demand for ready meals and convenient food options.

The steel canned food packaging industry's growth is propelled by the increasing demand for convenient and shelf-stable food, particularly in developing economies. Technological advancements leading to lighter and more sustainable cans are crucial. Furthermore, the industry's ability to adapt to evolving consumer preferences and prioritize sustainable practices will further fuel its growth.

This report provides a comprehensive overview of the steel canned food packaging market, covering historical data (2019-2024), current estimates (2025), and future projections (2025-2033). The study analyzes market trends, driving forces, challenges, key players, and regional variations, offering valuable insights for industry stakeholders. The detailed segmentation analysis enables a granular understanding of market dynamics within different applications and types of steel cans. The report’s forecasts provide a strategic roadmap for businesses operating in or seeking to enter the steel canned food packaging sector.

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 7.3% from 2020-2034 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately 7.3%.

Key companies in the market include Ball Corporation, Del Monte Foods, Crown Holdings, Amcor Limited, Anchor Glass Container, Siligan Containers, Ardagh Group, Greif, Toyo Seiken, Huber Packaging.

The market segments include Type, Application.

The market size is estimated to be USD 57.79 billion as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4480.00, USD 6720.00, and USD 8960.00 respectively.

The market size is provided in terms of value, measured in billion and volume, measured in K.

Yes, the market keyword associated with the report is "Steel Canned Food Packaging," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Steel Canned Food Packaging, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.