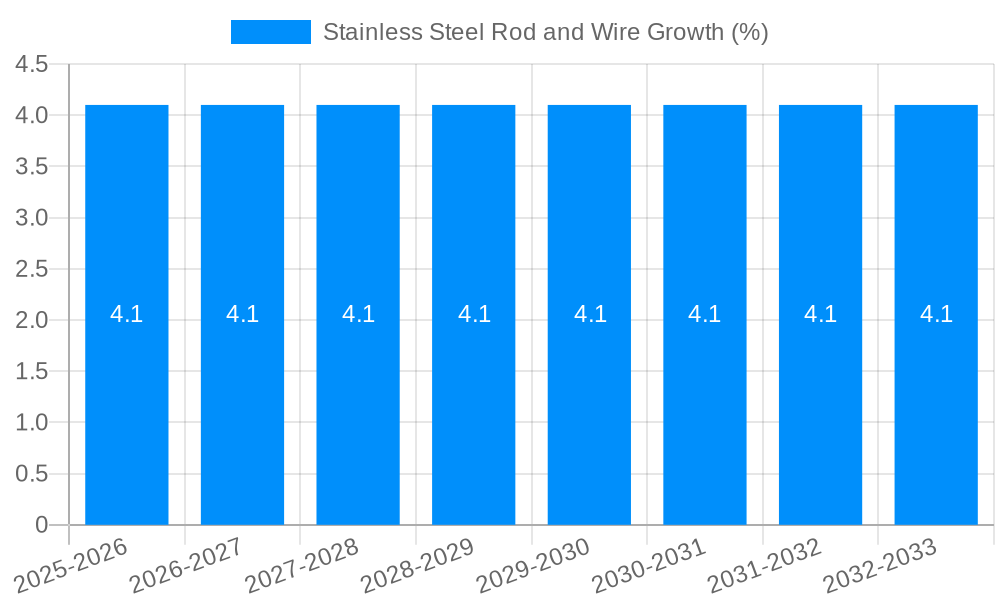

1. What is the projected Compound Annual Growth Rate (CAGR) of the Stainless Steel Rod and Wire?

The projected CAGR is approximately 4.1%.

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

Stainless Steel Rod and Wire

Stainless Steel Rod and WireStainless Steel Rod and Wire by Type (6mm, 8mm, 10mm, 12mm, Others), by Application (Automobile, Medical, Chemical, Architecture, Others), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2025-2033

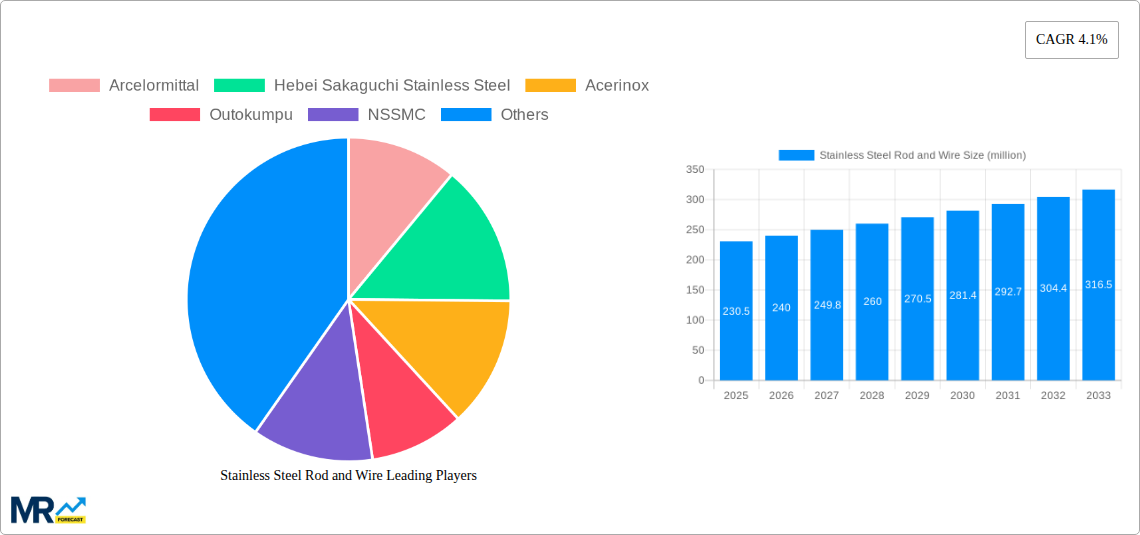

The global Stainless Steel Rod and Wire market is poised for robust growth, projected to reach a significant valuation of $230.5 million by 2025, with a Compound Annual Growth Rate (CAGR) of 4.1% expected to propel it through 2033. This expansion is largely driven by the increasing demand from critical sectors such as the automobile industry, where the inherent strength, corrosion resistance, and aesthetic appeal of stainless steel make it indispensable for various components, from engine parts to decorative elements. The medical sector also presents a substantial growth avenue, fueled by the need for biocompatible and sterile materials for surgical instruments, implants, and laboratory equipment. Furthermore, the chemical industry's requirement for materials that can withstand harsh environments and corrosive substances contributes to market momentum. Emerging applications in architecture, particularly in façade systems, structural components, and interior design, are also playing a vital role in shaping market dynamics.

The market's trajectory will be influenced by several key trends, including a growing preference for specialized stainless steel alloys offering enhanced performance characteristics, such as higher tensile strength and superior corrosion resistance. Innovations in manufacturing processes, leading to more efficient production and cost-effectiveness, will also be a significant factor. Geographically, the Asia Pacific region is expected to dominate the market share, driven by rapid industrialization, a burgeoning manufacturing base, and increasing infrastructure development in countries like China and India. While the market presents strong growth prospects, potential restraints include volatility in raw material prices, particularly nickel and chromium, and intense competition among established and emerging players. However, the intrinsic advantages of stainless steel, combined with ongoing technological advancements and expanding application areas, are expected to outweigh these challenges, ensuring a dynamic and expanding market landscape for stainless steel rods and wires.

Here's a comprehensive report description on Stainless Steel Rod and Wire, incorporating the requested elements:

The global Stainless Steel Rod and Wire market, valued at approximately $25 million in the historical period of 2019-2024, is projected for significant expansion, reaching an estimated $35 million by 2025. The forecast period of 2025-2033 anticipates a compound annual growth rate (CAGR) of XX%, indicating robust demand driven by evolving industrial landscapes and a persistent need for corrosion-resistant materials. Key market insights reveal a discernible shift towards higher-grade stainless steel alloys, particularly those offering enhanced strength, durability, and specific functional properties. The increasing adoption of advanced manufacturing techniques, such as precision rolling and drawing, is contributing to improved product quality and the development of specialized stainless steel rod and wire variants catering to niche applications. Furthermore, the market is witnessing a growing emphasis on sustainable production practices and the utilization of recycled stainless steel, aligning with global environmental imperatives. The base year of 2025 is expected to be a pivotal point, with a projected market size of $35 million, setting the stage for sustained growth in the subsequent years. This trend is underpinned by the inherent versatility of stainless steel, making it an indispensable material across a multitude of industries, from the burgeoning automotive sector demanding lighter yet stronger components, to the critical medical field requiring biocompatible and sterile materials. The architectural sector's increasing preference for aesthetically pleasing and long-lasting materials further fuels demand for stainless steel rods and wires in façade elements, railings, and structural reinforcements. The "Others" segment, encompassing diverse applications like industrial machinery, consumer goods, and electronics, also contributes substantially to the overall market dynamics. The trajectory indicates a market characterized by technological innovation, a heightened focus on sustainability, and an expanding application base that will redefine the landscape of stainless steel rod and wire consumption in the coming decade.

The stainless steel rod and wire market's ascent is fundamentally propelled by a confluence of powerful drivers that underscore the material's inherent value proposition. Foremost among these is the insatiable demand from the Automobile industry. As manufacturers strive to produce lighter, more fuel-efficient vehicles, stainless steel rods and wires are increasingly employed in structural components, exhaust systems, and interior fittings, offering superior corrosion resistance and a favorable strength-to-weight ratio. This trend is amplified by stringent emission regulations and the growing popularity of electric vehicles, which necessitate the use of advanced materials for battery enclosures and charging infrastructure. Complementing this is the indispensable role of stainless steel in the Medical sector. The biocompatibility, sterilizability, and resistance to bodily fluids and cleaning agents make it the material of choice for surgical instruments, implants, guidewires, and various medical devices. The aging global population and advancements in medical technology are continuously expanding the scope of applications for high-quality stainless steel in healthcare. Furthermore, the Chemical industry's reliance on stainless steel for its exceptional corrosion resistance against aggressive chemicals and high temperatures in pipelines, reactors, and storage tanks remains a significant impetus. This sector's continuous need for durable and safe infrastructure ensures a steady demand for stainless steel rods and wires.

Despite the promising growth trajectory, the Stainless Steel Rod and Wire market is not without its hurdles. A primary challenge is the volatility in raw material prices, particularly nickel and chromium, which are key alloying elements. Fluctuations in global commodity markets directly impact the production costs of stainless steel, leading to price instability for downstream products and potentially affecting demand, especially in price-sensitive applications. Moreover, the intense price competition within the market, driven by a large number of manufacturers, can exert downward pressure on profit margins. This necessitates a continuous focus on operational efficiency and cost optimization for producers. Another significant restraint stems from environmental regulations and the energy-intensive nature of stainless steel production. While efforts are being made towards sustainable practices, the energy consumption and potential emissions associated with smelting and refining can pose regulatory challenges and increase operational costs. Furthermore, the availability of alternative materials in certain applications, such as high-strength aluminum alloys or advanced composites, presents a competitive threat. While stainless steel offers unique advantages, ongoing material science advancements in competing sectors require continuous innovation and differentiation from stainless steel producers. Finally, geopolitical factors and trade barriers can disrupt supply chains and impact the global flow of stainless steel rods and wires, creating uncertainties for market participants.

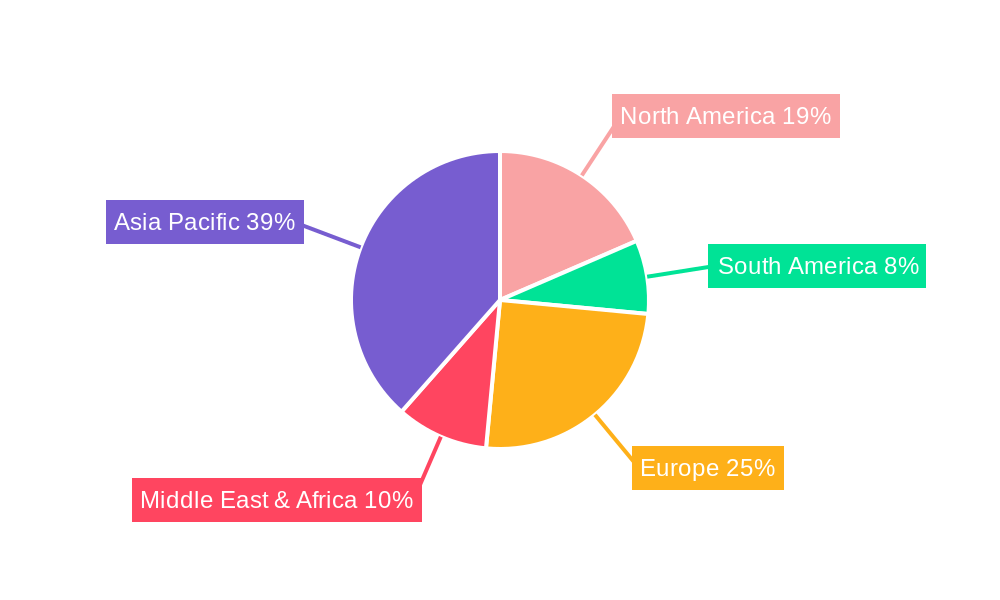

The global Stainless Steel Rod and Wire market is poised for significant regional and segmental dominance, with certain areas and applications exhibiting particularly robust growth.

Key Dominating Segments:

Type: 6mm, 8mm, and 10mm stainless steel rods and wires are anticipated to dominate the market. These sizes are widely utilized across a broad spectrum of industries due to their versatility and ease of fabrication. The Automobile sector heavily relies on these dimensions for structural components, chassis parts, and exhaust systems. Similarly, the Architecture industry employs them extensively in balustrades, decorative elements, and structural reinforcements where precise dimensions are crucial for aesthetic and functional integrity. The "Others" segment, encompassing general engineering and manufacturing, also contributes significantly to the demand for these standard sizes. While larger diameters (12mm and above) find critical applications in heavy-duty construction and industrial machinery, the sheer volume and widespread adoption of the 6mm to 10mm range position them as market leaders.

Application: The Automobile sector is projected to be the leading application segment for stainless steel rods and wires. The relentless pursuit of fuel efficiency, coupled with the increasing demand for safety and durability, drives the adoption of stainless steel in both internal combustion engine vehicles and the rapidly expanding electric vehicle market. Stainless steel’s corrosion resistance, high strength-to-weight ratio, and aesthetic appeal make it an ideal material for exhaust systems, fuel lines, chassis components, and decorative trim. The ongoing shift towards electric mobility, with its specific material requirements for battery housings, charging infrastructure, and lighter body structures, further bolsters this dominance. Following closely is the Architecture segment, which benefits from the material's longevity, low maintenance requirements, and modern aesthetic appeal. Stainless steel rods and wires are integral to the construction of facades, roofing, interior design elements, and outdoor furniture, contributing to sustainable and visually striking buildings. The Medical sector, while representing a smaller volume, is a high-value segment characterized by stringent quality standards and consistent demand for biocompatible and sterile stainless steel products used in surgical instruments, implants, and medical devices.

Key Dominating Regions/Countries:

Asia Pacific: This region is expected to remain the powerhouse of the global Stainless Steel Rod and Wire market. Fueled by robust industrial growth, particularly in China and India, the demand across the Automobile, Construction, and general manufacturing sectors is exceptionally high. China, with its massive manufacturing base and significant investments in infrastructure and automotive production, will continue to be a primary consumer and producer. India's rapid economic development, growing middle class, and increasing focus on domestic manufacturing further contribute to the region's dominance. The presence of major stainless steel producers within the region ensures a stable supply chain and competitive pricing.

North America: The Automobile industry's strong presence in the United States and Canada, coupled with increasing investments in healthcare and infrastructure, will drive demand. The emphasis on advanced manufacturing and high-performance materials in the automotive sector, particularly for lightweighting and corrosion resistance, will continue to support the growth of stainless steel rods and wires. Furthermore, the growing trend of sustainable construction and the demand for durable architectural elements will also contribute to market expansion in this region.

Europe: European countries, with their sophisticated automotive sector, stringent environmental regulations, and high standards for medical devices and architectural applications, will remain significant markets. The focus on sustainability and the circular economy will also drive demand for high-quality recycled stainless steel. Germany, France, and the United Kingdom are key contributors to this regional market.

The interplay between these dominant segments and regions, driven by technological advancements and evolving consumer preferences, will shape the future landscape of the Stainless Steel Rod and Wire market.

Several key catalysts are fueling the growth of the Stainless Steel Rod and Wire industry. The unwavering demand from the Automobile sector, driven by lightweighting initiatives and the transition to electric vehicles, is a primary growth engine. Similarly, the expanding Medical industry's need for biocompatible and sterilizable materials for implants and instruments provides consistent demand. Furthermore, the increasing adoption of stainless steel in Architecture for its durability, aesthetic appeal, and low maintenance in both residential and commercial construction projects significantly contributes to market expansion. Advancements in material science, leading to the development of specialized alloys with enhanced properties, are opening up new application avenues and driving innovation.

This comprehensive report delves into the intricate dynamics of the global Stainless Steel Rod and Wire market, offering a granular analysis from the historical period of 2019-2024 to an extended forecast period extending to 2033. The report meticulously examines the market size, projected to grow from approximately $25 million in the historical period to an estimated $35 million by the base and estimated year of 2025, with a sustained CAGR of XX% through 2033. It provides an in-depth exploration of the driving forces, including the burgeoning demand from the automobile and medical sectors, and the persistent need for corrosion-resistant materials in chemical applications. Furthermore, the report addresses the challenges and restraints, such as raw material price volatility and intense competition, while identifying key regional and segmental dominances. The analysis extends to providing insights into significant industry developments, leading players, and growth catalysts that are shaping the future of this vital market.

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 4.1% from 2019-2033 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately 4.1%.

Key companies in the market include Arcelormittal, Hebei Sakaguchi Stainless Steel, Acerinox, Outokumpu, NSSMC, Yieh Corp, Ivaco Rolling Mills (HEICO), Central Wire, Emirates Steel, Walsin Lihwa, Hindustan Inox Ltd, Shandong North New Material Co.,Ltd., Venus Wires, DAIDO STEEL, Navkar Metal, Viraj Profiles Pvt. Ltd, Aamor Inox, JAY JAGDAMBA LIMITED, Randwise Trade Houldings, Star Metal Industries, King Steel Corporation, Gunratna Metals, .

The market segments include Type, Application.

The market size is estimated to be USD 230.5 million as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3480.00, USD 5220.00, and USD 6960.00 respectively.

The market size is provided in terms of value, measured in million and volume, measured in K.

Yes, the market keyword associated with the report is "Stainless Steel Rod and Wire," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Stainless Steel Rod and Wire, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.