1. What is the projected Compound Annual Growth Rate (CAGR) of the Specialty Optical Fibers for Aerospace?

The projected CAGR is approximately 6.2%.

Specialty Optical Fibers for Aerospace

Specialty Optical Fibers for AerospaceSpecialty Optical Fibers for Aerospace by Type (Radiation-resistant Fibers, Polarization Maintaining Fibers, High-Temperature Fibers, Other), by Application (Sensing, Communication, Monitoring, Other), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2026-2034

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

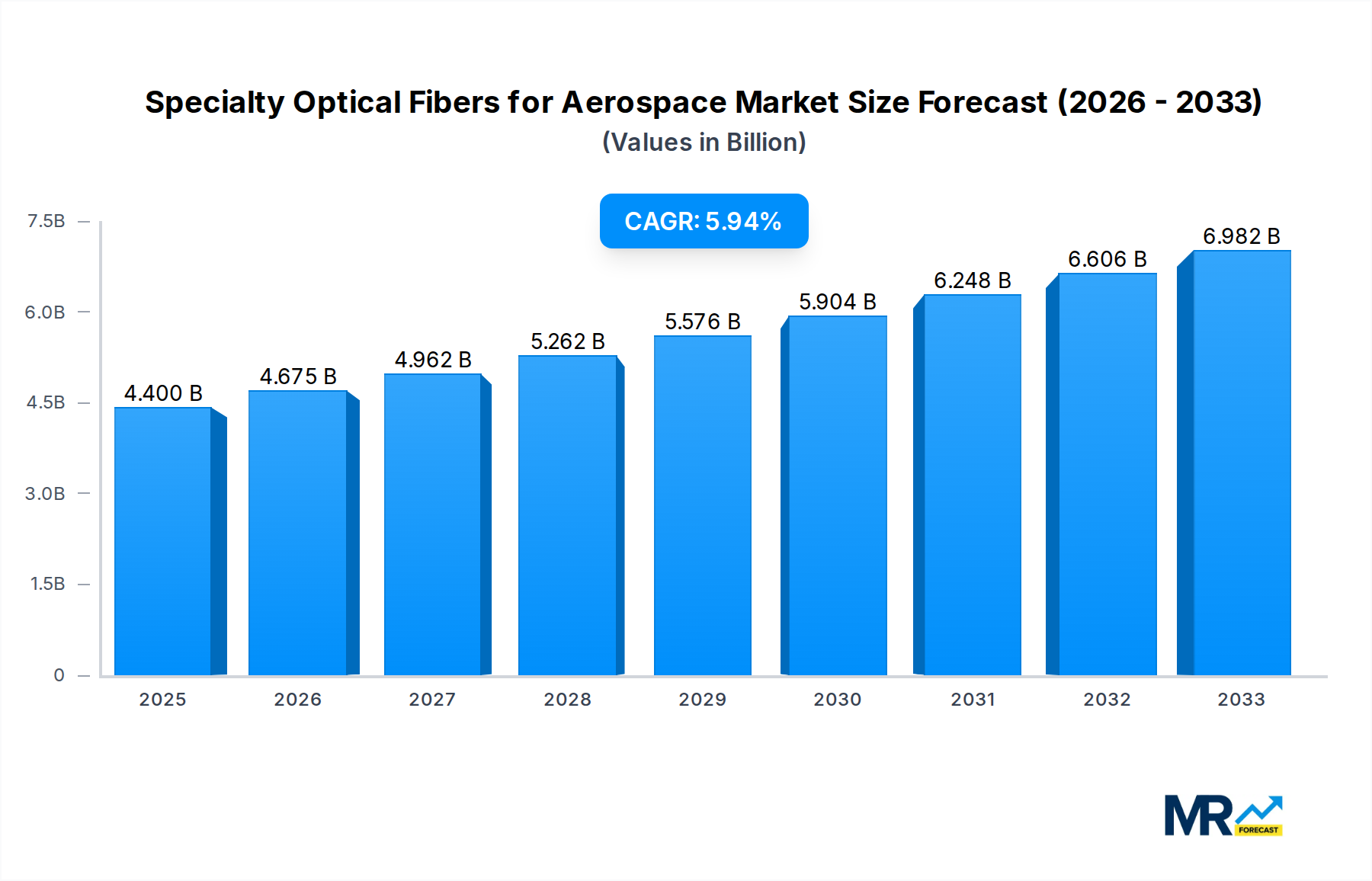

The global market for Specialty Optical Fibers in the aerospace sector is poised for substantial growth, projected to reach an estimated \$4.4 billion in market size in 2025, with a robust Compound Annual Growth Rate (CAGR) of 6.2% anticipated to extend through 2033. This upward trajectory is primarily fueled by the aerospace industry's increasing demand for advanced materials that offer superior performance under extreme conditions, lighter weight, and enhanced data transmission capabilities. Key drivers include the relentless pursuit of fuel efficiency through weight reduction, the critical need for reliable sensing and monitoring systems in advanced aircraft and spacecraft, and the expansion of sophisticated communication networks within the aerospace domain. The integration of optical fibers into critical systems such as flight control, engine monitoring, and structural health monitoring is becoming indispensable, driving significant adoption. Furthermore, the growing complexity of aerospace platforms, including the development of next-generation aircraft, satellite constellations, and space exploration initiatives, will continue to propel the demand for these specialized fibers.

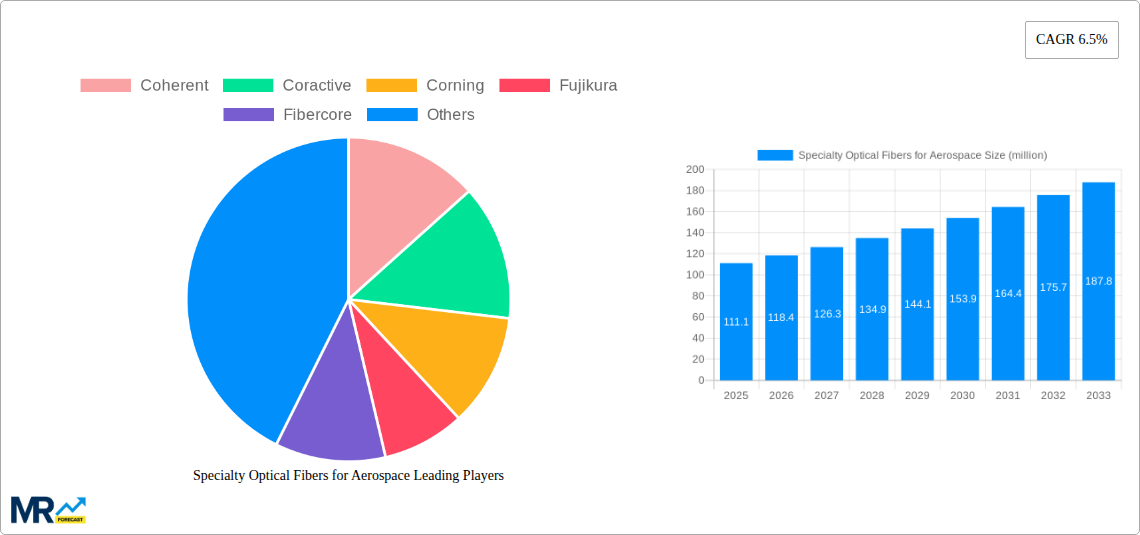

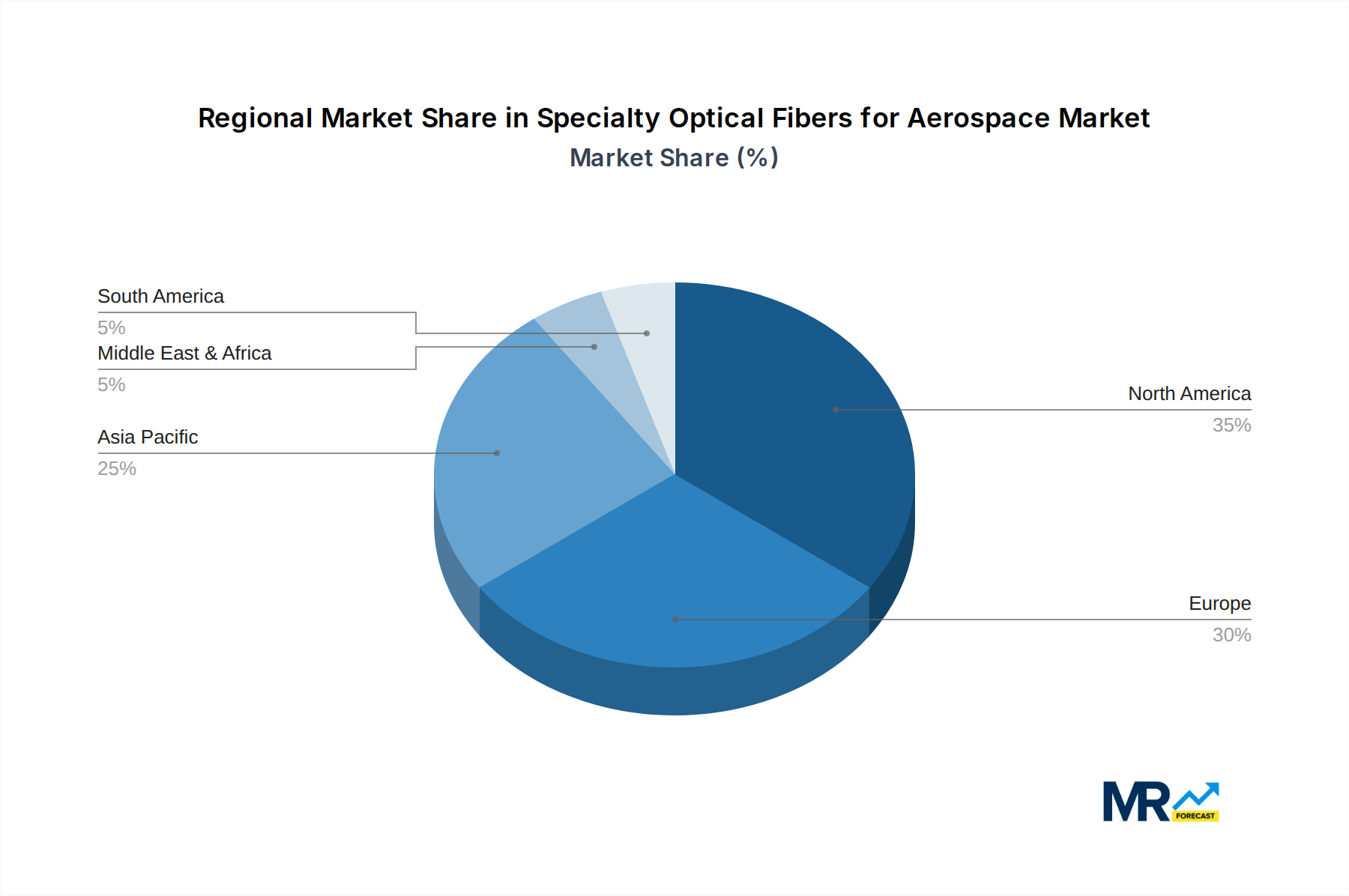

The market landscape for Specialty Optical Fibers in Aerospace is characterized by significant segmentation, offering diverse solutions to meet specific aerospace requirements. Radiation-resistant fibers are paramount for applications in space and high-altitude environments, while polarization-maintaining fibers are crucial for precise optical measurements and interferometric sensing. High-temperature fibers are essential for components operating in the extreme heat generated by engines and other critical systems. These specialized fibers are finding widespread application across sensing technologies, enabling advanced diagnostics and real-time data acquisition. In the realm of communication, optical fibers are vital for high-bandwidth data transfer, supporting the increasing data loads from sensors and avionics. The monitoring segment benefits immensely from the high sensitivity and accuracy offered by optical fiber sensors for structural integrity and environmental conditions. Geographically, North America and Europe are leading markets due to the established aerospace manufacturing base and significant R&D investments. However, the Asia Pacific region, driven by the burgeoning aerospace industries in China and India, is expected to witness the fastest growth. Leading companies like Corning, Fujikura, and Prysmian are at the forefront, investing in innovation and expanding their manufacturing capabilities to cater to this dynamic and expanding market.

The global market for Specialty Optical Fibers for Aerospace is poised for significant expansion, projected to reach an impressive $5.8 billion by 2033. This robust growth trajectory is underpinned by a confluence of technological advancements, increasing demand for advanced aerospace platforms, and the critical need for enhanced performance and reliability in space and aviation applications. The study period, spanning from 2019 to 2033, with a base year of 2025, encapsulates a dynamic market landscape where innovation is paramount. During the historical period of 2019-2024, the market witnessed steady adoption driven by initial research and development and the integration of fiber optics into nascent aerospace systems. As we move into the estimated year of 2025 and the subsequent forecast period of 2025-2033, the market is set to accelerate, fueled by evolving industry standards and the increasing complexity of aerospace missions. Key insights reveal a growing preference for fibers offering superior durability, reduced weight, and advanced functionalities, directly addressing the stringent requirements of the aerospace sector. This includes the indispensable need for radiation-resistant fibers to withstand the harsh conditions of space, polarization-maintaining fibers for precise data transmission, and high-temperature fibers capable of enduring extreme operational environments. The "Other" category, encompassing specialized fibers for niche applications, is also expected to contribute to market growth as new use cases emerge. The increasing investment in next-generation aircraft, satellite constellations, and space exploration initiatives will undoubtedly act as a primary impetus for this market expansion. Furthermore, the growing emphasis on in-flight entertainment and communication systems, as well as sophisticated onboard monitoring and sensing capabilities, is creating substantial demand for specialized optical fibers. The inherent advantages of optical fibers, such as immunity to electromagnetic interference, high bandwidth, and low signal loss, make them an increasingly attractive alternative to traditional copper wiring in aerospace. This trend is further amplified by the ongoing miniaturization and weight reduction efforts within the aerospace industry, where optical fibers offer a compelling solution. The evolving regulatory landscape, promoting enhanced safety and performance standards in aviation, also indirectly contributes to the adoption of advanced fiber optic technologies.

The ascent of the Specialty Optical Fibers for Aerospace market is propelled by several formidable driving forces, chief among them being the relentless pursuit of enhanced performance and reliability in aerospace applications. The inherent advantages of optical fibers – their immunity to electromagnetic interference, high bandwidth capacity, and lightweight nature – are critically important for modern aircraft and spacecraft, where signal integrity and weight reduction are paramount. This has led to a significant shift away from traditional copper wiring, especially in sophisticated communication, navigation, and sensing systems. The ever-increasing complexity of aerospace missions, ranging from extended space exploration endeavors to advanced aerial surveillance and communication networks, necessitates robust and dependable data transmission solutions. Specialty optical fibers, engineered to withstand extreme conditions, play a pivotal role in ensuring the uninterrupted flow of critical data in these demanding environments. Furthermore, the burgeoning satellite industry, with its rapid expansion in constellation deployment for broadband internet, Earth observation, and scientific research, is a major demand driver. These satellites rely heavily on high-performance optical fibers for inter-satellite communication and data downlink. The growing focus on miniaturization and weight optimization in aerospace design also favors optical fibers, as they offer a more compact and lighter alternative to conventional cabling. This directly translates to improved fuel efficiency and payload capacity, crucial factors in both aviation and space sectors.

Despite the promising growth outlook, the Specialty Optical Fibers for Aerospace market faces several significant challenges and restraints that could temper its expansion. One of the primary hurdles is the high cost of manufacturing and implementation. Specialty optical fibers, with their unique material compositions and precise fabrication processes, are considerably more expensive than standard fibers. This premium price point can be a deterrent, especially for cost-sensitive applications or for newer market entrants. Stringent qualification and certification processes within the aerospace industry also pose a considerable challenge. Any new material or component introduced into an aircraft or spacecraft must undergo rigorous testing and validation to ensure its safety and reliability in extreme conditions. This lengthy and expensive process can significantly slow down the adoption of novel fiber optic technologies. Limited availability of specialized manufacturing expertise and infrastructure can also be a restraint. The production of high-performance specialty fibers requires highly skilled personnel and advanced manufacturing facilities, which are not universally accessible, potentially creating supply chain bottlenecks. Integration complexities with existing aerospace systems can also present a challenge. Retrofitting older aircraft or spacecraft with new fiber optic systems may require significant modifications to existing infrastructure and control systems, adding to the overall cost and complexity. Furthermore, the perception of fragility associated with optical fibers, although often a misconception due to advancements in protective jacketing and robust fiber designs, can still be a psychological barrier for some decision-makers within the aerospace sector, who are accustomed to the perceived ruggedness of metallic cabling.

The North America region, particularly the United States, is poised to dominate the Specialty Optical Fibers for Aerospace market, driven by its advanced aerospace industry, substantial government investment in space exploration, and a strong ecosystem of leading fiber optic manufacturers and research institutions. The presence of major aerospace players like Boeing and Lockheed Martin, coupled with NASA's ambitious missions, creates a significant and sustained demand for high-performance optical fibers. This dominance is further solidified by the region's proactive approach to adopting cutting-edge technologies and its robust regulatory framework that encourages innovation.

Within this leading region, the Radiation-resistant Fibers segment is expected to be a key growth driver and a significant contributor to market dominance. The increasing number of satellites being launched, the growing complexity of space missions requiring extended exposure to harsh radiation environments, and the development of next-generation space telescopes and deep-space probes all amplify the demand for these specialized fibers. These fibers are crucial for maintaining the integrity of data transmission and sensor readings in space, where cosmic rays and solar flares can degrade conventional optical materials. The ability of radiation-resistant fibers to maintain their performance characteristics under prolonged exposure makes them indispensable for satellite communication, scientific instrumentation, and critical command and control systems in space.

Application-wise, the Sensing segment is also anticipated to play a pivotal role in the market's dominance. Specialty optical fibers are increasingly being integrated into advanced sensing systems for various aerospace applications, including:

The synergistic growth of radiation-resistant fibers and the sensing application, driven by the stringent demands of the aerospace sector and the continuous push for technological advancement, will solidify North America's leading position in the global Specialty Optical Fibers for Aerospace market. The significant investments in defense, commercial aviation, and space exploration within the United States, coupled with the presence of key industry players and research facilities, create a fertile ground for the widespread adoption and development of these specialized optical fiber solutions.

The Specialty Optical Fibers for Aerospace industry is being significantly propelled by several key growth catalysts. The relentless pursuit of lighter, faster, and more reliable aerospace platforms fuels the demand for the inherent advantages of optical fibers, such as reduced weight and immunity to electromagnetic interference. The burgeoning satellite industry, with its rapid expansion in constellations for communication and Earth observation, is a major catalyst, requiring high-bandwidth, low-loss data transmission. Furthermore, ongoing advancements in miniaturization and the development of novel fiber materials with enhanced performance characteristics are opening up new application possibilities, further stimulating market growth. The increasing focus on advanced sensing technologies for structural health monitoring and operational diagnostics in aircraft and spacecraft also acts as a significant growth driver.

This report provides a comprehensive analysis of the Specialty Optical Fibers for Aerospace market, offering deep insights into its intricate dynamics and future trajectory. The study encompasses a detailed examination of market trends, driving forces, and the challenges that shape the industry landscape. It delves into key regional and country-specific market assessments, highlighting the dominant players and segments poised for substantial growth. The report meticulously analyzes crucial segments like Radiation-resistant Fibers, Polarization Maintaining Fibers, and High-Temperature Fibers, alongside their applications in Sensing, Communication, and Monitoring. With a robust forecast period extending from 2025 to 2033, based on a 2025 base year, the report delivers actionable intelligence for stakeholders. It identifies critical growth catalysts and profiles leading industry players, providing a thorough understanding of significant developments and market opportunities. This comprehensive coverage ensures a strategic roadmap for businesses seeking to capitalize on the expanding potential of this vital sector.

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 6.2% from 2020-2034 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately 6.2%.

Key companies in the market include Coherent, Coractive, Corning, Fujikura, Fibercore, OFS, Thorlabs, Molex, Leoni, AFL, Prysmian, YOFC, FiberHome.

The market segments include Type, Application.

The market size is estimated to be USD XXX N/A as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4480.00, USD 6720.00, and USD 8960.00 respectively.

The market size is provided in terms of value, measured in N/A and volume, measured in K.

Yes, the market keyword associated with the report is "Specialty Optical Fibers for Aerospace," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Specialty Optical Fibers for Aerospace, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.