1. What is the projected Compound Annual Growth Rate (CAGR) of the Special Steel for Automotive?

The projected CAGR is approximately XX%.

Special Steel for Automotive

Special Steel for AutomotiveSpecial Steel for Automotive by Application (Passenger Cars, Commercial Vehicles), by Type (Bar, Sheet, Others), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2026-2034

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

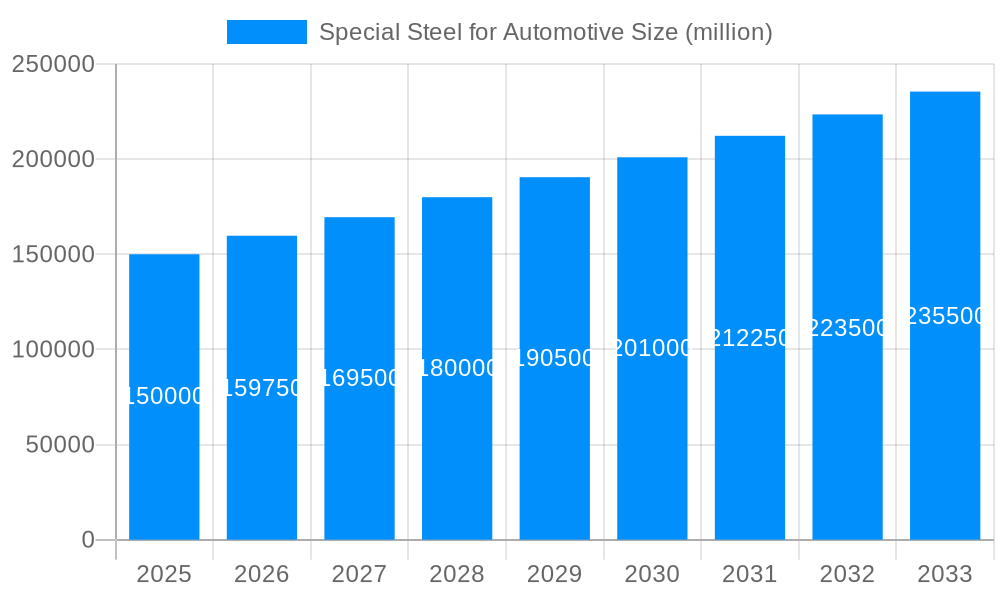

The global Special Steel for Automotive market is projected to witness robust growth, with an estimated market size of approximately $150 billion in 2025, driven by an impressive Compound Annual Growth Rate (CAGR) of around 6.5% through 2033. This expansion is primarily fueled by the increasing demand for lightweight, high-strength, and durable steel alloys in passenger cars and commercial vehicles. The automotive industry's relentless pursuit of enhanced fuel efficiency, improved safety standards, and superior performance necessitates the adoption of advanced special steels that offer a superior strength-to-weight ratio compared to conventional materials. Furthermore, the growing emphasis on electric vehicles (EVs) is a significant catalyst, as EVs often require specialized steels for battery enclosures, motor components, and structural integrity, all while aiming to minimize overall vehicle weight. This surge in demand for specialized automotive components, coupled with ongoing technological advancements in steel production, is creating a favorable market environment for special steel manufacturers.

The market dynamics are characterized by several key trends and restraints. A prominent trend is the development and adoption of advanced high-strength steels (AHSS) and ultra-high-strength steels (UHSS), which enable significant weight reduction without compromising structural integrity. This is directly aligned with global emissions regulations and the drive for sustainability. The increasing focus on stringent safety regulations, such as crashworthiness standards, further bolsters the demand for specialized steel grades. However, the market also faces restraints, including the fluctuating prices of raw materials, such as iron ore and alloying elements, which can impact manufacturing costs and profitability. The significant capital investment required for advanced steel production facilities and the presence of established players with strong market dominance can also pose barriers to entry for new competitors. Despite these challenges, the sustained innovation in metallurgy and the continuous evolution of automotive design ensure a positive growth trajectory for the Special Steel for Automotive market.

Here is a unique report description on Special Steel for Automotive, incorporating your specified requirements:

This comprehensive report delves into the dynamic global market for special steel utilized in the automotive industry. Analyzing the historical trajectory from 2019 to 2024 and projecting future trends through to 2033, with a base and estimated year of 2025, this study provides invaluable insights for stakeholders. The market is segmented by application into Passenger Cars and Commercial Vehicles, and by type into Bar, Sheet, and Others. We will explore the key industry developments shaping this crucial sector, examining the intricate interplay of technological advancements, regulatory shifts, and evolving consumer demands. The projected market size, reaching substantial figures in the millions, will be meticulously detailed across various segments.

The global special steel for automotive market is characterized by a robust upward trajectory, driven by an insatiable appetite for lighter, stronger, and more sustainable vehicles. XXX signifies a pivotal shift towards advanced high-strength steels (AHSS) and ultra-high-strength steels (UHSS) within the passenger car segment, accounting for an estimated XX million units in 2025. This adoption is fueled by the dual imperatives of fuel efficiency and enhanced safety, with manufacturers increasingly relying on these materials to reduce vehicle weight without compromising structural integrity. Sheet steel, in particular, will see continued dominance, catering to the evolving designs of body-in-white components and closures. The Commercial Vehicles segment, while historically more conservative in material adoption, is now witnessing a surge in demand for specialized alloys designed for increased payload capacity and longevity, projecting a market size of XX million units in 2025. The "Others" category, encompassing specialized components like drive shafts, suspension parts, and engine components, is expected to grow at a CAGR of X% during the forecast period, driven by niche applications demanding superior fatigue strength and wear resistance. Emerging markets are poised to become significant growth engines, with increasing vehicle production volumes and a growing awareness of the benefits of advanced steel solutions. The report will provide detailed regional breakdowns, highlighting key consumption patterns and investment opportunities. Furthermore, the circular economy principles are beginning to influence the special steel landscape, with a growing emphasis on recycled content and end-of-life recyclability, a trend that will gain further momentum in the coming years.

The automotive industry's relentless pursuit of enhanced performance, coupled with stringent global emission regulations, is the primary engine driving the special steel market. The increasing demand for fuel efficiency, directly linked to reducing carbon footprints, necessitates lighter vehicle structures. Special steels, with their superior strength-to-weight ratios compared to conventional steels, are instrumental in achieving these weight reduction goals, particularly in passenger cars where fuel economy is a major consumer consideration. The base year of 2025 projects an estimated XX million units in passenger car applications alone, underscoring this trend. Furthermore, advancements in vehicle safety standards worldwide are compelling automakers to incorporate stronger materials that can better absorb impact energy during collisions. This translates into a greater reliance on AHSS and UHSS, pushing the market towards higher-grade steel products. The commercial vehicle sector is also experiencing its own set of drivers, with fleet operators seeking to maximize payload capacities and minimize downtime due to material fatigue or failure. This is leading to the adoption of specialized, high-strength steel grades for chassis, frames, and critical structural components, projected to reach XX million units in 2025.

Despite the promising outlook, the special steel for automotive market faces several significant hurdles. The inherent complexity and higher cost of advanced steel production processes can be a barrier to widespread adoption, especially for price-sensitive vehicle segments and emerging markets. The estimated market value for "Others" applications, while growing, is constrained by the specialized nature of these components and the associated research and development investments. Another challenge lies in the evolving landscape of alternative materials, such as aluminum alloys and carbon fiber composites, which, while often more expensive, offer unique advantages in weight reduction and corrosion resistance. The report will meticulously analyze the competitive dynamics between steel and these alternative materials. Furthermore, the fluctuating prices of raw materials, particularly iron ore and alloying elements, introduce volatility into the cost structure of special steel manufacturers, potentially impacting profitability and market stability. The forecast period of 2025-2033 will examine the mitigation strategies employed by leading players to navigate these economic uncertainties. Supply chain disruptions, as observed during the historical period of 2019-2024, can also pose significant challenges, impacting production schedules and delivery timelines.

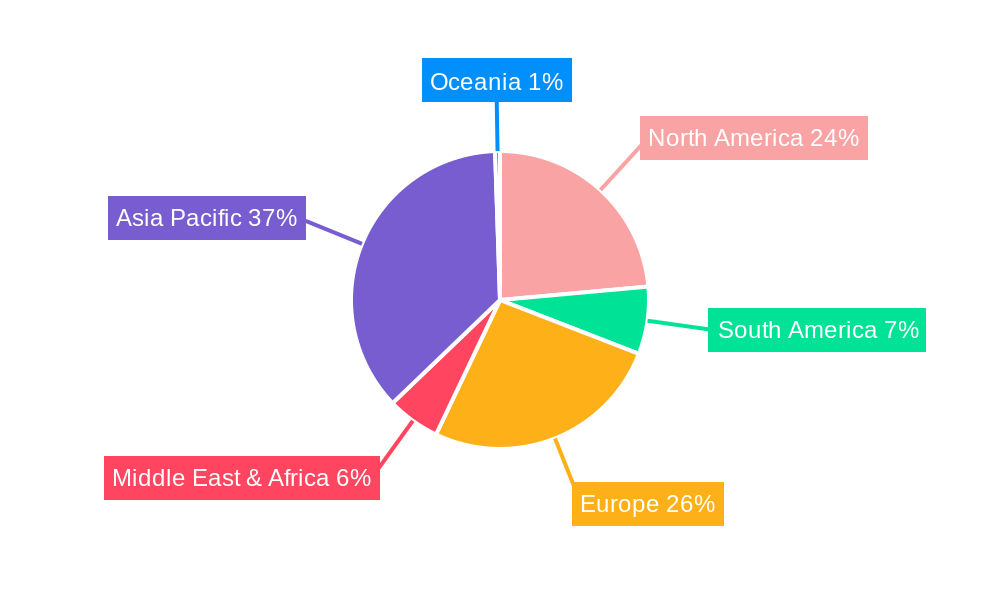

The Passenger Cars segment, particularly within Asia Pacific, is poised to emerge as the dominant force in the global special steel for automotive market throughout the study period (2019-2033). This dominance is underpinned by a confluence of factors, including the region's status as the world's largest automotive manufacturing hub, significant government support for advanced manufacturing, and a burgeoning middle class driving robust demand for new vehicles.

Asia Pacific Dominance:

Passenger Cars Segment Leadership:

The special steel for automotive industry is experiencing robust growth propelled by several key catalysts. The accelerating global shift towards electric vehicles (EVs) is a significant driver, as lighter chassis and body structures are crucial for maximizing battery range and overall efficiency. Furthermore, the increasing stringency of global safety regulations, mandating higher impact resistance and occupant protection, compels automakers to adopt advanced high-strength steels (AHSS) and ultra-high-strength steels (UHSS). The continuous innovation in steelmaking technologies, leading to the development of more sophisticated and tailor-made steel grades, also fuels growth by offering enhanced performance characteristics.

This report offers an exhaustive analysis of the global special steel for automotive market, covering the historical period from 2019-2024 and projecting trends through 2033, with 2025 serving as the base and estimated year. The study meticulously examines market dynamics across applications (Passenger Cars, Commercial Vehicles) and product types (Bar, Sheet, Others), providing detailed market size estimations in the millions for each segment. We delve into the critical industry developments, identifying key drivers such as the accelerating adoption of EVs, stringent safety regulations, and technological advancements in steelmaking. The report also addresses the challenges and restraints, including cost complexities, competition from alternative materials, and raw material price volatility. Extensive regional analysis highlights the dominant markets, particularly Asia Pacific and the Passenger Cars segment, with in-depth insights into their growth drivers and future potential. The report further identifies pivotal growth catalysts and provides a comprehensive list of leading market players.

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of XX% from 2020-2034 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately XX%.

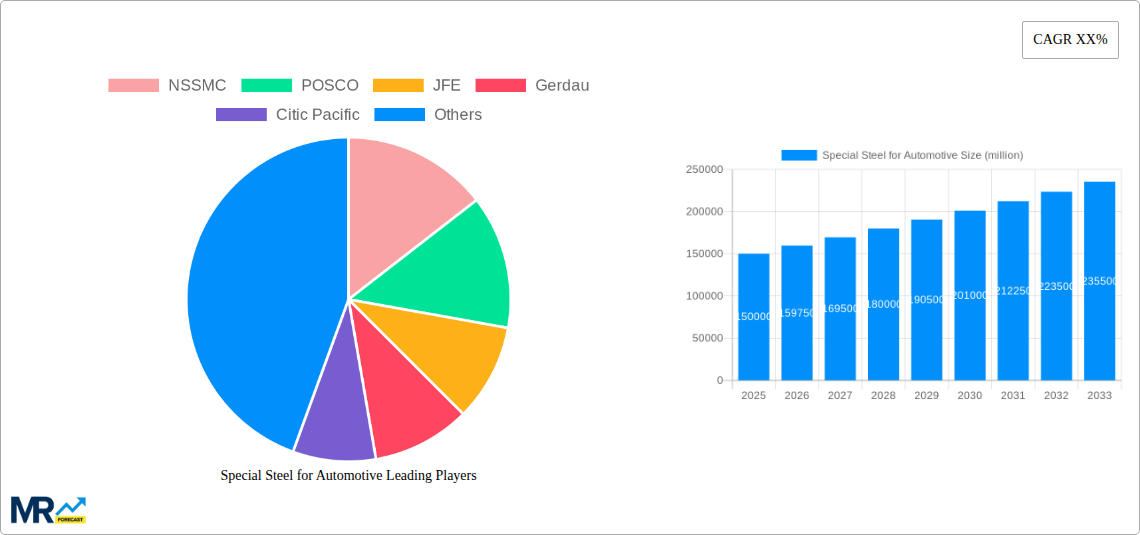

Key companies in the market include NSSMC, POSCO, JFE, Gerdau, Citic Pacific, ThyssenKrupp AG, TISCO, Aperam, Outokumpu, Dongbei Special Steel, Nanjing Steel, Voestalpine, Hyundai, AK Steel, Baosteel, DAIDO Steel, SSAB, Sandvik, HBIS, Sanyo, Ovako, Xining Special Steel, Shagang Group, Aichi Steel, Nippon Koshuha, Timken Steel, .

The market segments include Application, Type.

The market size is estimated to be USD XXX million as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3480.00, USD 5220.00, and USD 6960.00 respectively.

The market size is provided in terms of value, measured in million and volume, measured in K.

Yes, the market keyword associated with the report is "Special Steel for Automotive," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Special Steel for Automotive, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.