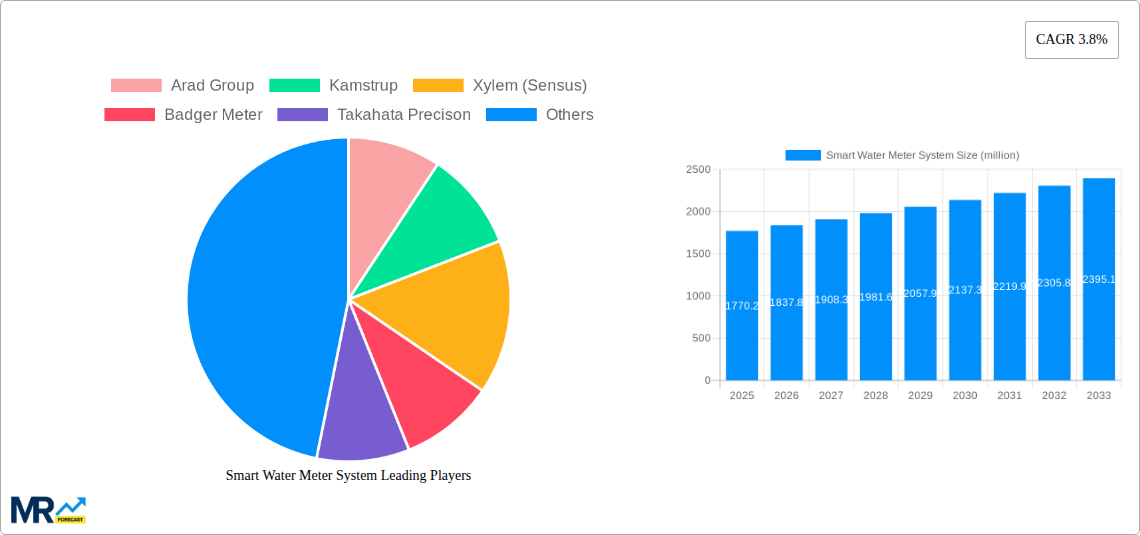

1. What is the projected Compound Annual Growth Rate (CAGR) of the Smart Water Meter System?

The projected CAGR is approximately 3.8%.

Smart Water Meter System

Smart Water Meter SystemSmart Water Meter System by Type (Pre-payment Electricity Meter, Remote Transmitting Water Meter, Electronics Meter), by Application (Residential, Industrial, Commercial), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2026-2034

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

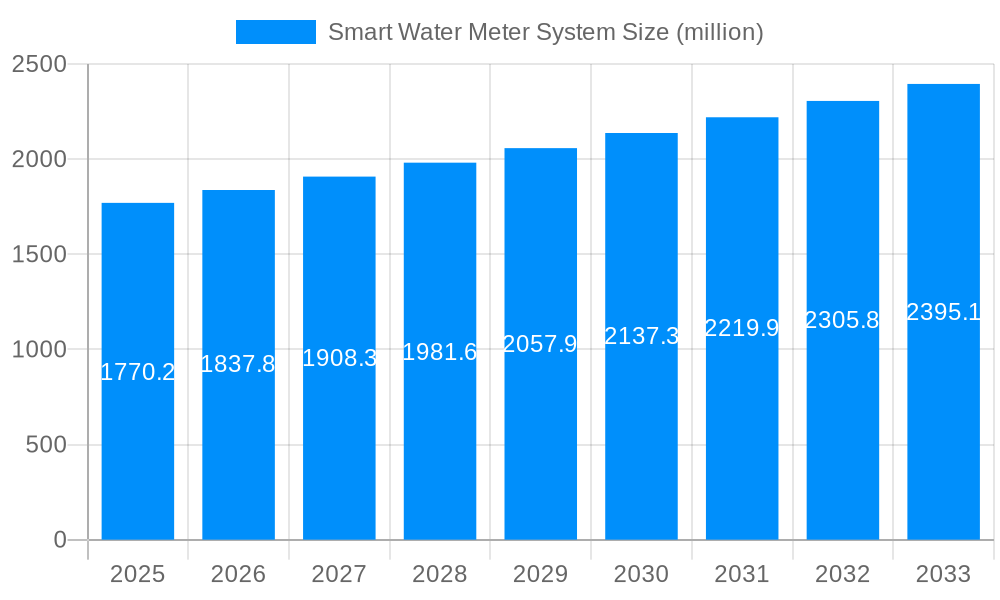

The global smart water meter system market is experiencing robust growth, projected to reach a substantial size driven by increasing urbanization, aging water infrastructure, and the urgent need for water conservation. The market, valued at $1770.2 million in 2025, is expected to exhibit a compound annual growth rate (CAGR) of 3.8% from 2025 to 2033. This growth is fueled by several key factors. Governments worldwide are increasingly investing in smart water infrastructure upgrades to improve efficiency, reduce water loss, and enhance billing accuracy. Furthermore, the rising adoption of advanced metering infrastructure (AMI) and the integration of smart water meters with data analytics platforms are creating new opportunities for market expansion. The ability to monitor water usage in real-time, detect leaks promptly, and implement targeted conservation strategies provides significant economic and environmental benefits, driving the demand for smart water meter systems. Competition in the market is intense, with established players like Itron, Kamstrup, and Xylem (Sensus) competing alongside regional and emerging technology providers. Continuous technological advancements, such as the integration of IoT (Internet of Things) technologies and the development of more robust and cost-effective smart water meters, further contribute to market dynamism.

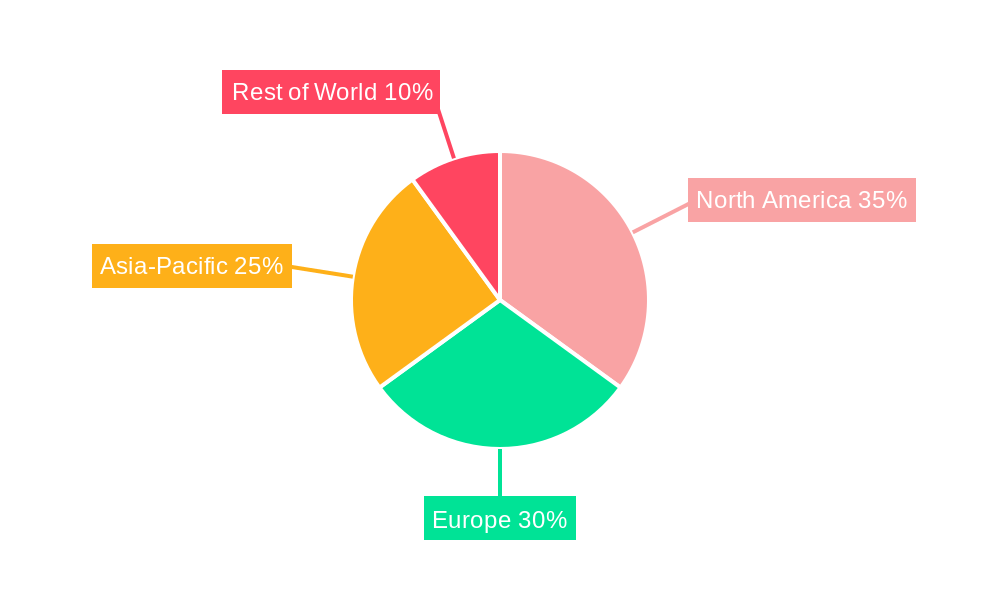

The market segmentation is likely diverse, encompassing various meter types (e.g., ultrasonic, mechanical, electronic), communication technologies (e.g., cellular, RF mesh, narrowband), and deployment models (e.g., residential, commercial, industrial). Geographic variations in water management practices and infrastructure development also contribute to regional differences in market adoption rates. While North America and Europe currently hold significant market shares, regions with rapidly growing urban populations and increasing investments in water infrastructure are expected to witness accelerated growth in the coming years. Challenges such as the high initial investment costs for smart meter deployments and cybersecurity concerns need to be addressed for sustained market expansion. However, the long-term benefits of enhanced water management are expected to outweigh these hurdles, ensuring the continued growth trajectory of the smart water meter system market.

The global smart water meter system market is experiencing robust growth, projected to reach multi-million unit installations by 2033. Driven by increasing urbanization, water scarcity concerns, and the need for efficient water management, the market showcases a compelling blend of technological advancements and evolving regulatory landscapes. The historical period (2019-2024) witnessed significant adoption, particularly in developed nations, with a notable shift towards advanced metering infrastructure (AMI) solutions. The estimated year 2025 marks a crucial point, showcasing the culmination of previous investments and the emergence of new technologies like AI-powered leak detection and predictive maintenance. This period reveals a clear preference for systems offering real-time data, improved billing accuracy, and reduced water loss. The forecast period (2025-2033) anticipates continued expansion, propelled by government initiatives promoting water conservation and smart city development. Developing economies are expected to contribute significantly to this growth, driven by increasing investment in infrastructure modernization and the need to address water management challenges. This market trend is not simply about replacing traditional meters; it's a comprehensive shift towards data-driven, proactive water resource management. This involves the integration of smart meters with broader water management systems, utilizing advanced analytics to optimize distribution networks, identify leaks promptly, and improve customer service. The increasing availability of cost-effective IoT solutions and cloud-based data platforms further accelerates this trend, making smart water meter systems more accessible to a broader range of municipalities and water utilities. The overall market landscape is competitive, with established players and new entrants constantly innovating to offer advanced features and improve their market share. Competition is largely based on providing value-added services, including enhanced data analytics capabilities, improved customer engagement tools, and robust cybersecurity measures.

Several factors are converging to fuel the rapid expansion of the smart water meter system market. Firstly, the escalating global water scarcity necessitates efficient water management. Smart meters, with their ability to monitor consumption patterns in real-time, play a crucial role in detecting leaks, reducing non-revenue water, and optimizing distribution networks. This translates to substantial cost savings for water utilities and improved water security for communities. Secondly, the increasing focus on smart city initiatives is driving the adoption of smart water metering solutions as a key component of broader urban infrastructure modernization. These initiatives often include government subsidies and incentives, making smart meter deployment more financially viable. Thirdly, the advancement of technologies such as IoT, big data analytics, and AI has significantly improved the capabilities of smart water meters, enabling more sophisticated data analysis and predictive maintenance. This leads to better operational efficiency and cost optimization for water utilities. Finally, improved billing accuracy and reduced customer disputes are additional benefits that drive the adoption of smart water meters. The ability to generate accurate, timely bills reduces administrative overhead and improves customer satisfaction. This combination of environmental concerns, technological advancements, government support, and improved operational efficiency is creating a powerful tailwind for the growth of the smart water meter system market.

Despite the significant growth potential, several challenges and restraints hinder the widespread adoption of smart water meter systems. High initial investment costs for infrastructure upgrades and meter replacements represent a substantial barrier, particularly for smaller municipalities with limited budgets. The complexity of integrating smart meters into existing water infrastructure and IT systems can also create significant implementation challenges. Ensuring the cybersecurity of smart water meter networks is crucial, as vulnerabilities could lead to data breaches and operational disruptions. Concerns about data privacy and the responsible use of customer water consumption data also need careful consideration. Furthermore, the need for skilled personnel to install, maintain, and manage these advanced systems represents an ongoing challenge. In developing economies, the lack of reliable electricity grids and internet connectivity can further restrict the deployment of smart water meters. Finally, overcoming regulatory hurdles and obtaining necessary approvals can be a time-consuming process. Overcoming these challenges requires a collaborative approach involving water utilities, technology providers, and policymakers to develop cost-effective solutions, strengthen cybersecurity measures, address data privacy concerns, and build the necessary technical expertise.

North America: The region is expected to hold a substantial market share due to early adoption of smart technologies, well-established infrastructure, and government support for water conservation initiatives. The US, in particular, is leading the way in smart water meter deployments, driven by large-scale projects and the increasing awareness of water scarcity issues.

Europe: Europe is another significant market, with several countries actively investing in upgrading their water infrastructure and adopting smart water metering solutions. The regulatory environment in Europe encourages the adoption of sustainable water management practices, driving the demand for smart meters.

Asia-Pacific: This region is expected to witness rapid growth in the coming years, driven by increasing urbanization, economic development, and government initiatives promoting smart city development. Countries like China and India are investing heavily in water infrastructure upgrades, providing a significant market opportunity for smart water meter vendors.

Commercial Segment: This segment shows strong growth due to the focus on reducing water consumption and costs in commercial buildings and industries. Real-time monitoring and leak detection capabilities offer significant cost savings in the long run.

Residential Segment: The residential segment holds a substantial share, owing to the increasing awareness of water conservation and the growing demand for advanced metering infrastructure to monitor and manage water usage efficiently.

The market dominance of North America and Europe stems from mature water infrastructure and existing technological capabilities, allowing for smoother integration of smart water meters. However, the Asia-Pacific region's projected rapid growth highlights the increasing global awareness of efficient water management and the significant investment in infrastructure upgrades in developing economies. The commercial and residential segments reflect the broad applicability of smart water metering solutions across various user groups, indicating a diversified market with numerous growth opportunities.

The smart water meter system industry is experiencing a surge in growth fueled by a confluence of factors. Stringent water regulations aimed at curbing water wastage and promoting conservation are creating a compelling case for adopting smart meters. Simultaneously, the declining cost of advanced sensors and data analytics technologies makes smart meter implementation more financially viable for utilities. Furthermore, the increasing availability of reliable and affordable internet connectivity is essential for the successful deployment and operation of these systems. These elements, combined with the rising awareness of water scarcity and the need for enhanced water resource management, are powerfully driving market expansion.

This report provides a comprehensive overview of the smart water meter system market, analyzing market trends, driving forces, challenges, and key players. It offers detailed insights into regional and segmental dynamics, along with projections for future market growth. The report also highlights significant technological advancements and industry developments shaping the landscape of this rapidly evolving sector. The in-depth analysis enables businesses and stakeholders to understand the opportunities and challenges present in this burgeoning market.

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 3.8% from 2020-2034 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately 3.8%.

Key companies in the market include Arad Group, Kamstrup, Xylem (Sensus), Badger Meter, Takahata Precison, Diehl Metering, Itron, Neptune Technology Group, Honeywell (Elster), B METERS, Sanchuan, Suntront, iESLab, Chongqing Intelligence, Ningbo Water Meter, Wasion Group, Shenzhen Huaxu, Hunan Changde, .

The market segments include Type, Application.

The market size is estimated to be USD 1770.2 million as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3480.00, USD 5220.00, and USD 6960.00 respectively.

The market size is provided in terms of value, measured in million and volume, measured in K.

Yes, the market keyword associated with the report is "Smart Water Meter System," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Smart Water Meter System, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.