1. What is the projected Compound Annual Growth Rate (CAGR) of the Smart Convenience Store?

The projected CAGR is approximately 7.41%.

Smart Convenience Store

Smart Convenience StoreSmart Convenience Store by Type (Liquor Store, Mini-Markets, Party Stores, General Store, Others), by Application (Food and Beverage, Leisure, Others), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2026-2034

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

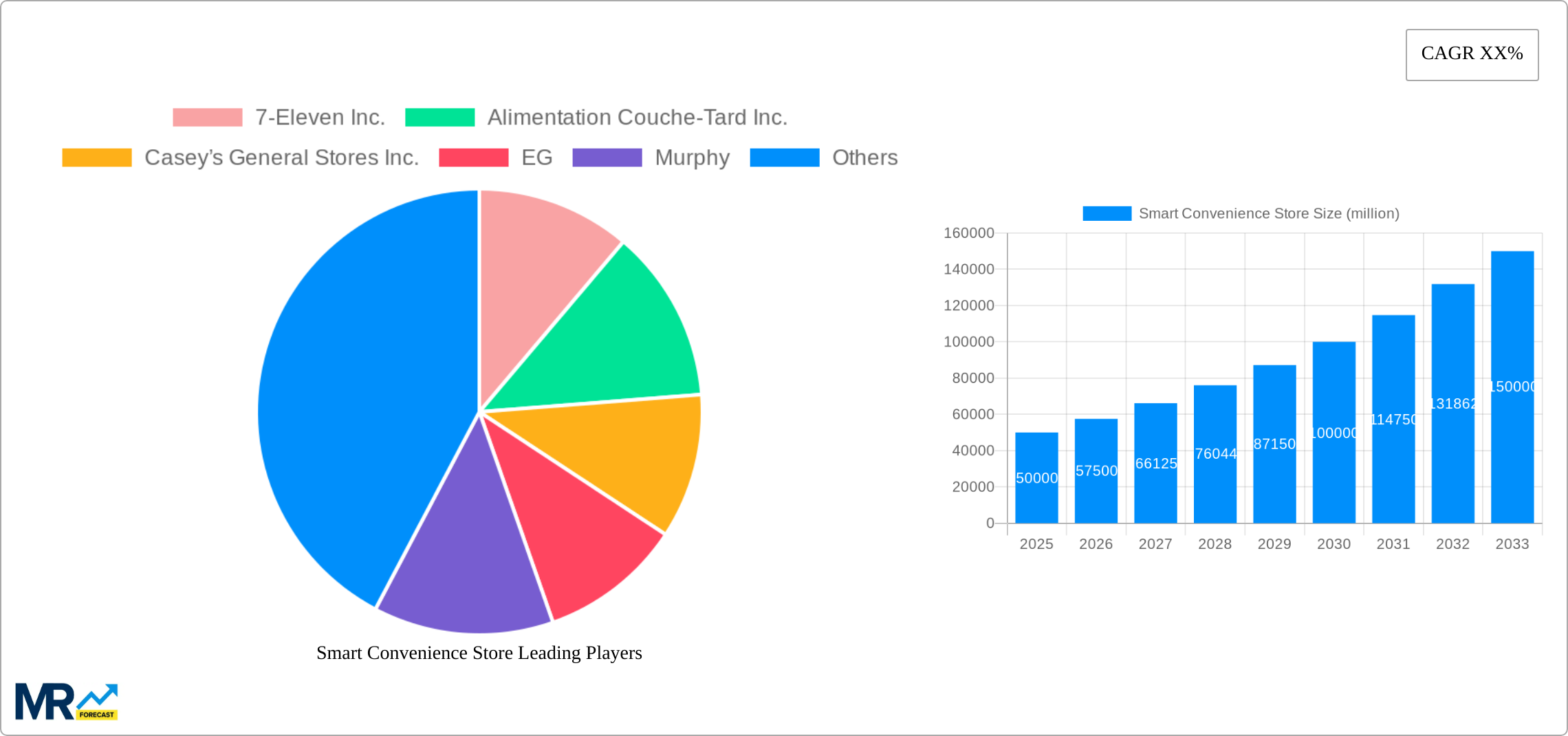

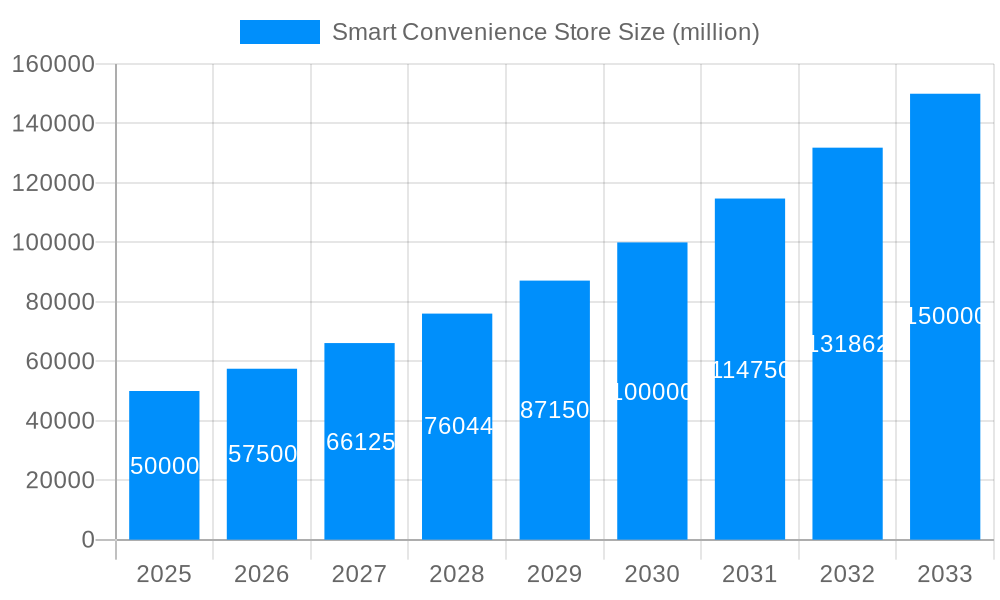

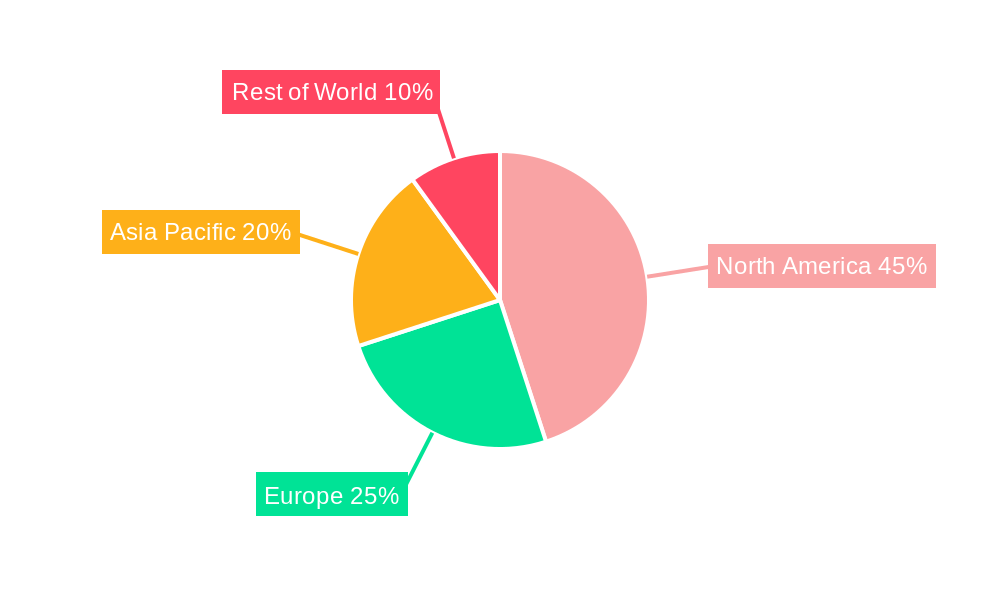

The smart convenience store market is experiencing robust growth, driven by increasing consumer demand for convenient, personalized, and technology-integrated shopping experiences. The market, estimated at $15 billion in 2025, is projected to achieve a compound annual growth rate (CAGR) of 12% from 2025 to 2033, reaching an estimated $45 billion by 2033. This expansion is fueled by several key factors. Technological advancements such as automated checkout systems, personalized offers via loyalty programs, and advanced inventory management systems are enhancing operational efficiency and improving the customer experience. Furthermore, the integration of mobile ordering and delivery services caters to the growing preference for contactless shopping and on-demand convenience. The increasing adoption of data analytics also allows for better understanding of consumer preferences, enabling targeted marketing and customized product offerings. Key segments driving growth include liquor stores and mini-markets due to their high foot traffic and established customer bases, particularly within food and beverage applications. Geographic expansion is also significant, with North America expected to retain a dominant market share, followed by Europe and Asia-Pacific, as these regions witness rapid technological adoption and rising disposable incomes.

However, the market faces challenges. High initial investment costs associated with implementing smart technologies can be a barrier to entry for smaller retailers. Data security concerns and the need for robust cybersecurity measures are also crucial considerations. Furthermore, successful implementation requires strong integration of various technological components, potentially posing logistical complexities. Competition from established convenience store chains and emerging e-commerce platforms necessitates strategic partnerships and innovative approaches to ensure market leadership. Ultimately, the success of smart convenience stores hinges on the ability of businesses to balance technological innovation with a customer-centric approach that emphasizes convenience, personalization, and seamless integration across various channels. The competitive landscape includes established players like 7-Eleven, Couche-Tard, and QuikTrip, who are actively investing in smart store technologies to maintain their market dominance.

The smart convenience store market is experiencing explosive growth, projected to reach multi-million unit sales by 2033. This surge is fueled by the convergence of technological advancements and evolving consumer preferences. Consumers increasingly demand seamless, personalized experiences, and smart convenience stores are perfectly positioned to deliver. The integration of technologies like AI-powered inventory management, self-checkout kiosks, mobile ordering and payment systems, and personalized loyalty programs is transforming the traditional convenience store model. This not only improves operational efficiency for businesses like 7-Eleven, Alimentation Couche-Tard, and Wawa, but also enhances the customer experience, leading to increased customer loyalty and higher sales. The historical period (2019-2024) witnessed significant adoption of basic smart technologies, but the forecast period (2025-2033) promises a more sophisticated and integrated approach. We're seeing a shift towards personalized offers based on purchasing history and location data, creating a hyper-targeted marketing approach that resonates with individual consumers. Furthermore, the integration of smart shelves, which automatically track inventory levels and alert staff to restocking needs, significantly reduces waste and streamlines operations. The estimated value for 2025 shows promising initial market penetration, setting the stage for substantial growth in the coming years. This report analyzes the market's trajectory, key players, and challenges, providing a comprehensive overview of the smart convenience store landscape. The integration of smart technologies isn't merely an add-on; it's a fundamental shift in how these businesses operate, manage inventory, and interact with their customers, leading to a more efficient and profitable model that keeps pace with consumer expectations. The adoption is particularly high in urban areas with high foot traffic and densely populated regions.

Several factors contribute to the rapid expansion of the smart convenience store market. The increasing demand for convenience and speed is a primary driver. Consumers, especially in urban environments, prioritize quick and easy access to goods and services. Smart technologies directly address this need, offering services like mobile ordering and curbside pickup, streamlining the shopping process. Secondly, the rise of data analytics plays a crucial role. By collecting and analyzing data on consumer behavior, smart stores can optimize product placement, inventory management, and personalized marketing campaigns. This data-driven approach leads to increased sales and reduced waste. Another key driver is the competitive landscape. Companies like 7-Eleven, QuikTrip, and Wawa are investing heavily in smart technology to gain a competitive edge, forcing others to follow suit. This creates a virtuous cycle of innovation and improvement within the industry. The ease of integration of smart technology solutions is another important catalyst, as many pre-built and affordable solutions are available on the market, lowering the initial investment costs for businesses of all sizes. Finally, the growing adoption of cashless transactions and the prevalence of mobile payment systems further simplifies the purchasing process, pushing the smart convenience store market forward. This continuous interplay of technological advancement and evolving consumer needs fuels this robust market growth.

Despite the significant growth potential, the smart convenience store sector faces certain challenges. The initial investment in implementing smart technologies can be substantial, posing a significant barrier to entry, particularly for smaller businesses. This includes the cost of hardware, software, and the necessary training for employees. Moreover, data security and privacy concerns are paramount. Collecting and storing vast amounts of customer data necessitates robust security measures to prevent breaches and protect sensitive information. Failure to address these concerns could lead to reputational damage and legal repercussions. Another challenge is the integration of various smart technologies into existing infrastructure. This can be complex and require significant modifications to existing systems, leading to potential disruptions in operations. Furthermore, the reliance on technology can introduce vulnerabilities. System malfunctions or outages can severely disrupt operations, leading to customer dissatisfaction and lost revenue. Finally, maintaining and updating the technology requires ongoing investment and expertise, which can present financial and operational strain on businesses. Overcoming these challenges requires careful planning, strategic investment, and a commitment to data security and operational resilience.

The North American market, particularly the United States, is projected to dominate the smart convenience store sector due to high consumer adoption of technology, significant investment in retail technology, and the presence of major players like 7-Eleven, QuikTrip, and Wawa. Within this region, urban areas with high population density and significant foot traffic are showing the highest adoption rates.

Dominant Segment: The Food and Beverage segment within the smart convenience store market is anticipated to experience the most substantial growth. This is driven by the increasing demand for ready-to-eat meals, grab-and-go options, and personalized food recommendations based on consumer preferences. The integration of smart refrigerators that monitor stock levels and automatically adjust ordering quantities contributes to efficiency and minimized waste. This segment's success is further amplified by the ability to leverage mobile ordering and payment solutions, offering seamless pickup experiences.

Growth within Specific Types: While various store types benefit from smart technologies, the Mini-Markets segment stands out for its adaptability. Their relatively smaller size and often centrally located nature make them ideal candidates for integrating digital point-of-sale (POS) systems, mobile ordering, and targeted advertising. This facilitates a smoother and more convenient customer experience.

Geographic Distribution: The United States leads in smart convenience store adoption due to its robust technology infrastructure, higher disposable income compared to many other regions, and the willingness of consumers to embrace new technologies. However, other developed nations with similar infrastructure and consumer behavior patterns are also showing significant growth.

The synergistic effect of technological advancement, consumer preference for speed and convenience, and aggressive investments by major players sets the stage for continued market dominance in these key areas.

The smart convenience store industry's growth is further fueled by several key catalysts. The increasing adoption of mobile payment solutions simplifies transactions and enhances the customer experience. The growing integration of loyalty programs with personalized offers encourages repeat business and customer loyalty. Finally, ongoing technological advancements are constantly introducing new capabilities, driving further innovation and improvement within the sector. These factors work in tandem to drive sustainable market growth in the coming years.

This report offers a detailed analysis of the smart convenience store market, providing a comprehensive understanding of current trends, growth drivers, challenges, and key players. It encompasses historical data, present market estimations, and future forecasts, offering invaluable insights for businesses and investors seeking to navigate this rapidly evolving sector. The report also identifies key regions, segments, and technological advancements shaping the industry's trajectory. It is a must-have resource for anyone looking to understand the dynamic landscape of the smart convenience store market and to inform strategic decision-making.

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 7.41% from 2020-2034 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately 7.41%.

Key companies in the market include 7-Eleven Inc., Alimentation Couche-Tard Inc., Casey’s General Stores Inc., EG, Murphy, GPM Investments LLC, BP, ExtraMile Convenience Stores LLC, Wawa Inc., QuikTrip Corp., Kwik Trip, Pilot Co., Sheetz, Love’s Travel Stops & Country Stores Inc., RaceTrac Petroleum, .

The market segments include Type, Application.

The market size is estimated to be USD 6.72 billion as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4480.00, USD 6720.00, and USD 8960.00 respectively.

The market size is provided in terms of value, measured in billion.

Yes, the market keyword associated with the report is "Smart Convenience Store," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Smart Convenience Store, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.