1. What is the projected Compound Annual Growth Rate (CAGR) of the Silicon Material for Solar Cell?

The projected CAGR is approximately XX%.

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

Silicon Material for Solar Cell

Silicon Material for Solar CellSilicon Material for Solar Cell by Type (Monocrystalline Silicon, Polycrystalline Silicon, Amorphous Silicon), by Application (Solar Cells, Others), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2025-2033

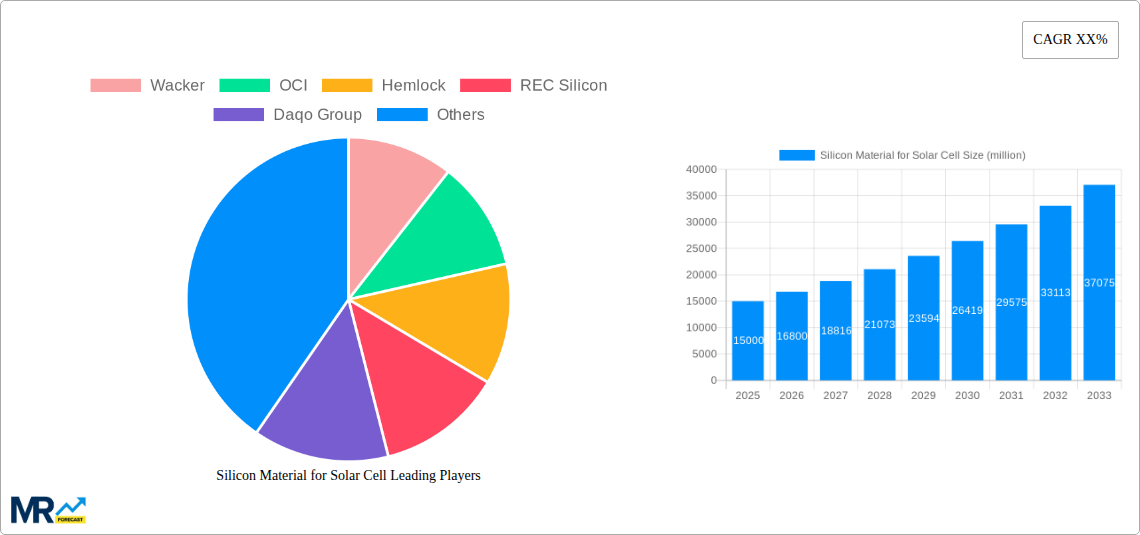

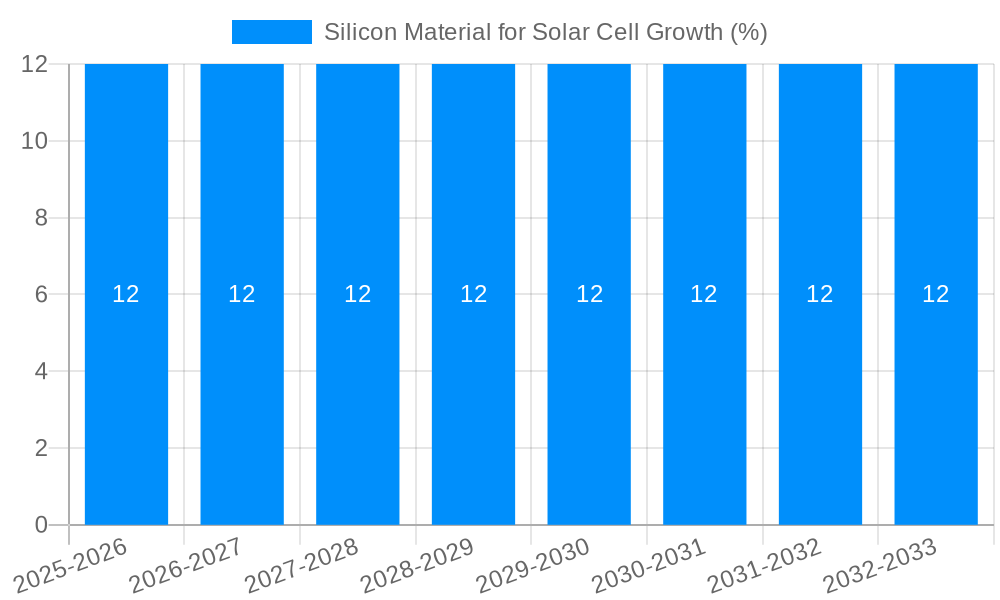

The global market for Silicon Material for Solar Cells is poised for significant expansion, driven by the escalating demand for renewable energy solutions. With a projected market size of approximately $15,000 million in 2025 and an estimated Compound Annual Growth Rate (CAGR) of 12% for the forecast period of 2025-2033, the industry is set to witness robust growth. This surge is primarily fueled by government initiatives promoting solar energy adoption, declining solar panel costs, and a growing environmental consciousness among consumers and corporations. The critical role of high-purity silicon, the fundamental building block of photovoltaic technology, in achieving energy independence and combating climate change cannot be overstated.

Key market segments include Monocrystalline Silicon, Polycrystalline Silicon, and Amorphous Silicon, with Monocrystalline Silicon expected to dominate due to its higher efficiency. Applications are largely concentrated in Solar Cells, though other niche applications contribute to market diversification. Geographically, the Asia Pacific region, particularly China, is expected to lead in both production and consumption, owing to substantial manufacturing capabilities and supportive policies. Emerging economies in this region are increasingly investing in solar power infrastructure. Conversely, the market faces restraints such as the fluctuating prices of raw materials, intense competition among key players like Wacker, OCI, and Tongwei Group, and the capital-intensive nature of polysilicon production. Nevertheless, ongoing technological advancements in silicon purification and cell manufacturing are expected to mitigate these challenges and sustain the upward trajectory of the market.

This comprehensive report delves into the dynamic global silicon material market specifically for solar cell applications. Analyzing historical data from 2019-2024 and projecting future trends from 2025-2033, with a base year of 2025 and an estimated year also of 2025, the report provides an in-depth understanding of market intricacies, key drivers, and emerging opportunities. The study leverages extensive market intelligence, including the latest industry developments and company-specific information, to offer actionable insights for stakeholders. With an estimated market size of 5,000 million units in the base year, the market is poised for substantial growth.

The global silicon material market for solar cells is experiencing a significant upward trajectory, driven by an unprecedented surge in renewable energy adoption. XXX, this trend is underpinned by increasing environmental consciousness, supportive government policies, and the declining cost of solar photovoltaic (PV) technology. Historically, from 2019 to 2024, the market has witnessed robust growth, transitioning from an estimated 4,500 million units to 4,800 million units. This expansion has been primarily fueled by the growing demand for solar panels, both for utility-scale projects and distributed generation. The shift towards high-efficiency solar cells, particularly those utilizing monocrystalline silicon, has become a defining characteristic of the market. Polycrystalline silicon, while still holding a significant share, is gradually giving way to monocrystalline due to its superior performance characteristics, leading to increased power output per unit area. Amorphous silicon, though less dominant in large-scale solar cells, finds niche applications where flexibility and low-light performance are paramount. The market is also characterized by ongoing technological advancements aimed at improving silicon purification processes, enhancing wafer quality, and reducing manufacturing costs. This continuous innovation is critical to meeting the escalating demand and maintaining the economic viability of solar energy. Furthermore, the increasing global emphasis on decarbonization and energy security is acting as a potent catalyst for the solar industry, directly translating into higher demand for upstream silicon materials. The projected market size of 5,200 million units by the end of the study period in 2033 signifies a sustained and strong expansion, reflecting the critical role of silicon in the global energy transition.

The growth of the silicon material for solar cell market is predominantly propelled by a confluence of powerful factors. Foremost among these is the escalating global commitment to combat climate change and transition to sustainable energy sources. Governments worldwide are implementing ambitious renewable energy targets and offering substantial incentives, such as tax credits and feed-in tariffs, which directly stimulate the demand for solar PV installations. This policy support translates into a consistently growing market for solar cells, consequently driving the need for high-purity silicon. Furthermore, the remarkable reduction in the cost of solar technology over the past decade has made it increasingly competitive with traditional fossil fuels. This cost-effectiveness, coupled with improvements in the energy conversion efficiency of solar cells, makes solar power a financially attractive investment for both utility companies and individual consumers. The increasing awareness among businesses and individuals regarding the environmental benefits and long-term cost savings of solar energy also plays a crucial role. As the global population grows and energy demands rise, the imperative to secure clean and reliable energy sources intensifies, further bolstering the market for solar silicon materials.

Despite the robust growth, the silicon material for solar cell market faces certain challenges and restraints that could temper its expansion. One significant hurdle is the volatility in raw material prices, particularly for polysilicon, which can impact the overall cost-effectiveness of solar cell manufacturing. Fluctuations in the price of metallurgical-grade silicon, the primary input, can create uncertainty for producers and downstream manufacturers. Another challenge pertains to the energy-intensive nature of polysilicon production. This requires significant electricity consumption, and the carbon footprint associated with energy generation for these processes can be a concern for environmentally conscious consumers and regulators. Furthermore, the market is subject to geopolitical risks and trade disputes, which can disrupt supply chains and lead to price hikes or shortages. Stricter environmental regulations concerning the manufacturing processes and waste disposal associated with silicon production can also increase operational costs for companies. Lastly, the rapid pace of technological advancement, while beneficial, can also lead to obsolescence of existing manufacturing infrastructure and require continuous investment in upgrading technology, posing a financial burden on some players.

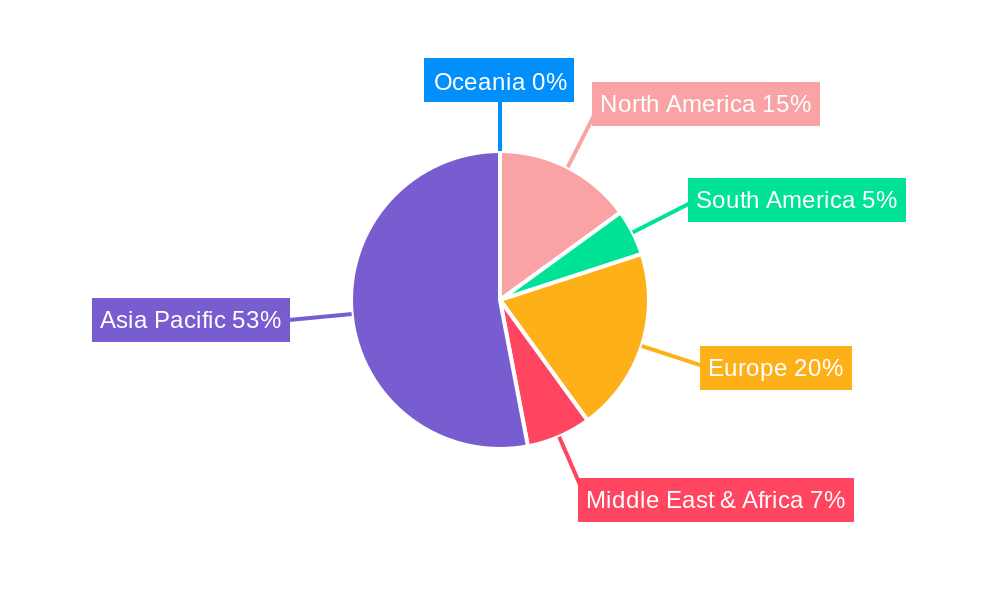

The global silicon material for solar cell market is characterized by a strong regional concentration and a clear dominance of specific segments. Among the key regions, Asia Pacific, particularly China, stands out as the undisputed leader.

Asia Pacific (China): China's dominance stems from its unparalleled manufacturing capacity across the entire solar value chain, from polysilicon production to solar panel assembly. The region's massive domestic demand, coupled with its role as a global exporter of solar products, has propelled it to the forefront. Supportive government policies, substantial investments in research and development, and a highly competitive cost structure have further solidified China's position. The sheer scale of production in China ensures that it will continue to be the primary driver of silicon material consumption for solar cells.

Europe: While not matching China's production volume, Europe remains a significant market, driven by stringent renewable energy targets, a strong emphasis on sustainability, and advanced technological adoption. Countries like Germany, the Netherlands, and Spain are at the forefront of solar deployment. Europe also boasts some high-end silicon manufacturers focusing on premium quality materials.

North America: The United States is witnessing a resurgence in domestic solar manufacturing, supported by government initiatives aimed at bolstering local supply chains and reducing reliance on foreign imports. The increasing adoption of solar power for both residential and commercial purposes is driving demand.

In terms of Segments to Dominate the Market:

Type: Monocrystalline Silicon: This segment is unequivocally the dominant force and is projected to maintain its lead throughout the study period. The increasing demand for high-efficiency solar panels, which are crucial for maximizing energy output in limited space, has significantly boosted the adoption of monocrystalline silicon wafers. Their superior crystalline structure leads to higher energy conversion efficiencies compared to polycrystalline silicon. The market for monocrystalline silicon is expected to grow at a faster rate than polycrystalline silicon, driven by advancements in ingot casting and wafering technologies that enhance performance and reduce costs. By 2025, it is estimated that monocrystalline silicon will account for over 70% of the total silicon material used in solar cells.

Application: Solar Cells: Naturally, the application segment of "Solar Cells" is the primary consumer of silicon material. The growth in this segment is directly tied to the overall expansion of the solar photovoltaic industry. As more solar farms are built and rooftop solar installations proliferate, the demand for silicon material will continue to surge. The estimated consumption for solar cells in the base year 2025 is expected to be approximately 5,000 million units.

Type: Polycrystalline Silicon: While its market share is gradually decreasing, polycrystalline silicon still holds a substantial position in the market, particularly in cost-sensitive regions and for utility-scale projects where slight efficiency differences are less critical than overall cost. Its production process is generally less complex and more energy-efficient than monocrystalline silicon, contributing to its continued relevance.

The silicon material for solar cell industry is propelled by powerful growth catalysts, primarily the escalating global imperative for clean energy and decarbonization. Supportive government policies, including subsidies and tax incentives for renewable energy deployment, are a major driver. The continuous decline in the cost of solar PV technology, making it increasingly competitive with fossil fuels, also acts as a significant catalyst. Technological advancements leading to higher solar cell efficiencies and improved manufacturing processes further enhance the appeal and adoption of solar energy, thereby boosting demand for silicon.

This report provides comprehensive coverage of the silicon material for solar cell market by offering a detailed analysis of its current state and future outlook. It meticulously examines market size, segmentation by type and application, and regional dynamics. The report delves into the driving forces behind market growth, such as government policies and technological advancements, while also identifying key challenges and restraints. Furthermore, it highlights significant industry developments, strategic initiatives of leading players, and the projected market trajectory from the historical period (2019-2024) through the forecast period (2025-2033), with a base year of 2025 and an estimated year also of 2025.

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of XX% from 2019-2033 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately XX%.

Key companies in the market include Wacker, OCI, Hemlock, REC Silicon, Daqo Group, Asia Silicon, Sinosico, Neimenggu Dunan, TEBA, Tongwei Group, GCL Power, Yongxiang, Xinte Energy, NorSun, .

The market segments include Type, Application.

The market size is estimated to be USD XXX million as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3480.00, USD 5220.00, and USD 6960.00 respectively.

The market size is provided in terms of value, measured in million and volume, measured in K.

Yes, the market keyword associated with the report is "Silicon Material for Solar Cell," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Silicon Material for Solar Cell, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.